We’ve had a couple of widely-reported contributions to discussions on housing policy in the last few days.

The first was the Concluding Statement from the staff mission responsible for conducting the latest International Monetary Fund Article IV consultation with New Zealand (usually a physical mission here from Washington, but presumably done remotely this time). These statements are not formally the official view of the IMF management, let alone the Board, but you don’t get to be a mission leader without demonstrating your soundness and ability to run a line that won’t upset the Board and management. That doesn’t mean the messages are typically consistent either across time or across countries, but it does mean the final report (and the Board review of it) won’t be materially different. Of course, it helps that New Zealand isn’t a very important country (to the IMF – we don’t borrow from them, we pose no threat to global or regional stability etc) – and that the New Zealand authorities don’t these days typically pay much heed to the IMF (in some countries, including a bigger one west of us, authorities have been very very concerned that never is heard a discouraging word from the Fund).

I used to have quite a bit to do with the Article IV processes, both from an RB/Treasury perspective, and in the couple of years I spent representing New Zealand on the Fund’s Board. Specifically, I used to be regularly involved in the final meeting between the Fund mission and Treasury/RB senior macro people on the drafts of the Concluding Statements. I guess it must have been different at times, in countries, when the Fund thought the authorities were going rogue, running reckless or dangerous policies, but if New Zealand has at times offered puzzles for the Fund, it has also been run with pretty cautious macro and financial policy approaches (low public debt, focus on balanced budgets, low inflation, stable banks, high capital requirements and so on). So whatever the Fund has to say tends to be pretty marginal or incidental anyway, and in many topics they touch on the mission team don’t actually have much specific expertise (they are mainly macro people, often very able to that narrow space). So the Fund team tended to be quite accommodating of Treasury/Reserve Bank preferences around what was said in any Concluding Statement, with a focus on “what would be helpful” to the authorities at that time. And this, of course, is only the end of days and days of meetings – often some wining and dining too (although I guess not this year) – in which staff are fully appraised of “sensitivities” and what officials (and the Minister) would prefer the Fund did or didn’t say. No doubt there are limits, but most often the remarks are about issues at the margin – either shades of policy in core areas, or matters on which the mission team doesn’t have much expertise, authority or mandate. Not often then will the Concluding Statement be troublesome for the authorities. (In fact, this is one of the downsides of the move to near-full transparency around the IMF Article IV processes in recent decades.) Favoured mantras will often, quite conveniently, be repeated back to the authorities, as little more than mantras: an example this time is “inclusive green growth”, whatever that means.

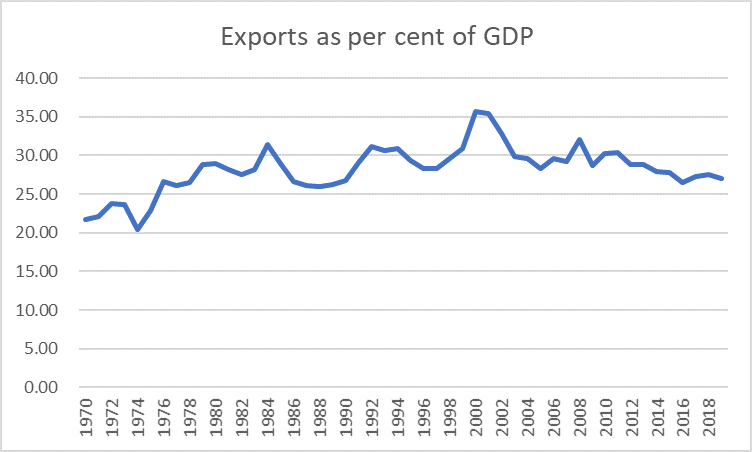

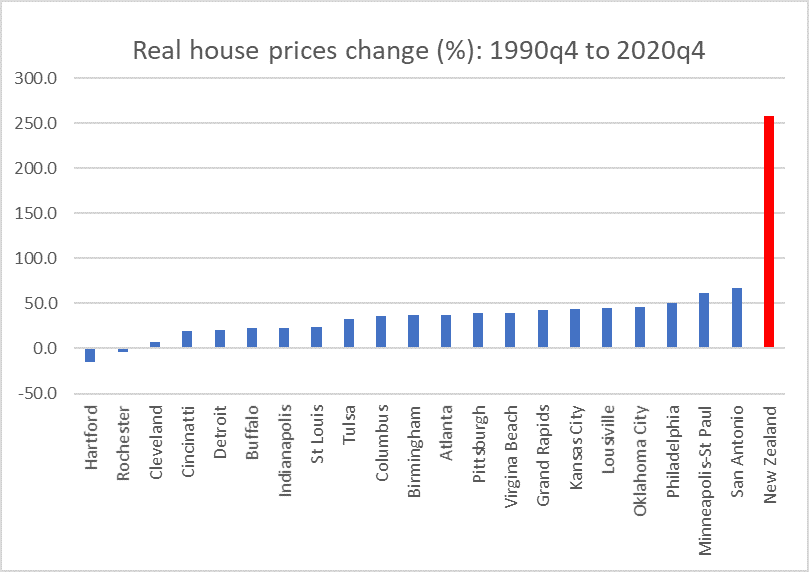

In this post I wanted to focus on housing, a rather central issue in current policy and political debate in New Zealand, arguably even a source of potential financial sector instability. What did the Fund have to say on the subject? There were several references, the first from the summary bullet points

- The rapid rise in house prices raises concerns around affordability and financial vulnerabilities. A comprehensive policy response is needed, including measures to unlock supply, dampen speculative demand, and buttress financial stability.

Surging house prices have supported household balance sheets but amplify affordability concerns for first home buyers and financial stability risks.

“Affordability” has certainly been stretched (to say the least), but it isn’t clear there is any greater threat to financial stability at this point. After all, as the report notes, household balance sheets as a whole have improved – not worsened – and if some marginal borrowers have taken on new debt at very high valuations (a) they are the marginal players, and (b) both banks and the Reserve Bank have imposed new and demanding LVR standards. Private lending standards have tightened – over the whole of the last year – not loosened. But it will have suited the authorities to have these references included.

Then we start to get to policy. The first reference reads as follows

Surging house prices should be addressed primarily through fiscal, regulatory, and macroprudential measures, though monetary policy may have a role if house prices pose risks to the inflation objective.

FIscal (tax?) measures as the main way to “address” house prices? On what planet does the Fund think this would be anything more than papering over cracks, and distracting from the core issue? But it will have suited the authorities to have it. And when they say “macroprudential measures” what they really mean is just new waves of controls. After all, the rest of the report suggests no particular reason for concern about the soundness of the financial system. It might have been nice to have seen “deregulatory” instead of “regulatory”, but I guess we can let that pass.

And what about monetary policy? Remarkably, there is no mention at all in this Concluding Statement of the government’s recent change to the Reserve Bank’s monetary policy Remit – the one that seemed designed to create the impression monetary policy was going to do something, even as the Reserve Bank itself said it wasn’t (an impression that at some international audiences have also erroneously taken). And that final half sentence? Well, it just looked like pandering as the Statement had already indicated the team’s macro view that monetary policy is likely to need to “remain accommodative for an extended period”.

They then get a little more substantive

Tackling supply-demand imbalances in the housing sector requires a comprehensive approach.

· Achieving long-term housing affordability depends critically on freeing up land supply, improving planning and zoning, and fostering infrastructure investments to enable fast-track housing developments. Steps taken to support local councils’ infrastructure funding and financing would facilitate a timely supply of land and infrastructure provision. The reform of the Resource Management Act is expected to reduce current complexities in land use that restrict infrastructure and housing development and contribute to efficiency in strategic planning. Increasing the stock of social housing also remains important, and the Residential Development Response Fund’s plans to deliver 18,000 public houses and transitional housing space, undertake rental housing reforms, and provide assistance to low-income households are welcome.

I guess the government will be quite happy with that. Suggest it is all big and complex and will take years to come to much. Oh, and that final sentence which would appear to be pure politics – you might agree, or not, with building more state houses or handing out more money to low-income people, but it bears no relationship at all to the Fund’s macro mandate, let alone to fixing the housing/land market that regulation has rendered dysfunctional. Smart active (but big) governments are clearly the thing.

But the broad thrust of that paragraph isn’t really that objectionable. Where it gets really problematic is the next paragraph.

· Mitigating near-term housing demand, particularly from investors, would help moderate price pressures. Introduction of stamp duties or an expansion of capital gains taxation could reduce the attractiveness of residential property investment. The authorities should differentiate in these approaches between first home buyers and investors, while continuing to provide selective grant and loan assistance to first-time buyers.

and this one

The deployment of macroprudential tools to address housing-related risks is welcome. The reinstatement of loan-to-value ratio (LVR) restrictions in March and further tightening for investors from May 2021 will help mitigate stability risks. Additional tools, including debt-to-income ratio limits, caps on investor interest-only loans, and higher bank capital risk weights on mortgage lending, are under consideration and could play a useful role in addressing housing-related risks.

Of the first of those paragraphs, really the less said the better. Price freezes dampen reported CPI inflation, wage freezes dampen reported wage inflation. Lockdowns reduce effective demand for, say, restaurant or cafe services. And so on. All sorts of daft, dangerous and inefficient mechanisms can be deployed to try to suppress symptoms, but most of them never should be. And nothing in that first paragraph stands up to any serious (macroeconomic, or really housing market functionality) scrutiny at all. But it must have gone over quite well in the Beehive, where “investors” seem now to be scapegoats for all ills, almost in the way that Jews were often so tarred in eastern Europe etc 100+ years ago. Just an attempt to distract from the real issues, the real policy failures.

The IMF – once concerned with functioning markets and more efficient policy regimes – is now actively touting policy interventions that differentiate by type of buyers, even though this advocacy seems to rest on no analysis whatever. And take as a particularly egregious example the mention of a stamp duty. These sort of transaction taxes are widely disliked in the economics literature – since they impede the functioning of the market directly affected and impair, for example, labour market mobility. In fact, they used to be firmly disapproved of by the IMF – which within the last five years has again recommended to the Australian and UK authorities (with very similar housing markets) that they move away from using stamp duties. So where did this suggestion come from? Either the Fund itself – in which case, serious questions should be asked about consistency of advice – or from The Treasury or the Minister of Finance? Is this an option that they are considering – perhaps (as the Fund phrasing talks of) just for the despised “investors”? The government made those idle pledges about no new taxes, but the “two minutes hate” now routinely directed at “investors” might suggest the government could get away with such a (Fund-supported) fresh distortion, at least among their own base.

And what about that “while continuing to provide selective grant and loan assistance to first-time buyers”? Surely the Fund knows – they’ve told countries often enough – that such interventions tend to flow straight into prices? And what does any of it have to do with the Fund’s macro or financial stability mandate (let alone any focus on economic efficiency?) But no doubt it went down well with the government: was “helpful to the authorities”.

I have heard a suggestion that perhaps what the Fund might have had in mind was a “temporary” stamp duty – whether just for investors or for everyone. If so, they should have said so. But if so, what planet are they on? All manner of taxes have been introduced “temporarily” over the years in many countries. Few get removed very easily – governments become addicted to the revenue, and/or happy to continue to deal with symptoms not causes. And the Fund itself – at least those of its officials with any sense of political economy – knows that.

And then there is the financial controls paragraph. These days the Fund really likes LVR restrictions, and the tighter ones still to come. In none of this is there any hint of the efficiency dimension. In none of it is there any hint of the analysis of risk (let alone of the interaction with the demanding new capital requirements – which don’t mess up the allocation of credit across sectors – the Fund has previously favoured), And having favoured very stringent LVR controls there is then no discussion about what, if any, the residual systemic risks (related to housing) might be. Instead, they allow themselves to become a channel for communicating, and apparently endorsing, the Reserve Bank’s own interventionist aspirations. If the Fund favours, for example, banning interest-only mortgages to “investors”, how does it square that preference with a regulatory restriction that already requires investors to have a 40 per cent deposit? One or other restriction might, in some circumstances, make sense. Both combined just seem like giving up on the market allocation of credit, papering over symptoms, and returning to the control mentality of ministers like Walter Nash. All ungrounded in that statutory goal that the Reserve Bank must exercise its regulatory powers over banks towards: promoting the soundness and efficiency of the financial system.

(Oh, and if the IMF believes that higher risk weights are warranted on housing, it will be interesting to see any argumentation they can advance in their final report – surely there will be none – for how the Reserve Bank has previously got it wrong: the same organisation the Fund repeatedly praised over the years for its cautious (emphasis on risk) approach in setting capital requirements, including for housing.)

If one had any doubts about the direction in which things are heading, there was the Q&A interview with the Reserve Bank Governor yesterday. It was a seriously soft interview by a TV1 political reporter, who displayed (a) no sign of any understanding of the legal framework the Bank operates under, (b) no sign of any real understanding of the housing market, and (c) no interest in doing anything but helping the Governor run his message, even feeding him loaded phrases in the questions. There was not a single serious challenging question. Not one. (Not even – an obvious question for a political reporter – about the recent change to the MPC Remit, talked up the Minister of Finance and then talked down – to the point of being almost dismissed – by the Bank.)

Orr went on and on about investors purchasing housing, but never once noted that if the land market were sorted out – and he did in passing acknowledge supply issues – the entire environment would be different: not only would houses/land not be expected to appreciate in real terms, but owner-occupier affordability would be that much greater (and without LVR restrictions it would also be easier for first home buyers). He made no attempt to tie the fresh interventions he and the government seem to be cooking up to the soundness of the financial system. In fact, he almost disavowed that as a consideration, claiming that the Bank had previously focused on systemic stability (whole financial system) but now had a new mandate that would enable it to focus on a specific asset class. Here he appeared to be referring to the direction issued to be the Bank a couple of weeks ago under section 68B of the Reserve Bank Act. It reads

I direct the Reserve Bank of New Zealand (“Reserve Bank”) to have regard to the following government policy that relates to its functions under Part 5 of the Act.

Government Policy

It is Government policy to support more sustainable house prices, including by dampening investor demand for existing housing stock which would improve affordability for first-home buyers.

As the Governor himself noted in a speech just a few days ago, no one really knows what “have regard to” (the statutory phrase) means. The Act itself provides no further guidance. But what is clear is that this direction provides the Bank with (a) no additional powers it had not already had, and (b) no change (broadening or narrowing) in the statutory goals the Bank is required to use its Part 5 (banking regulation) powers towards. Those powers must be exercised for these purposes (only):

The powers conferred on the Governor-General, the Minister, and the Bank by this Part shall be exercised for the purposes of—

(a) promoting the maintenance of a sound and efficient financial system; or

(b) avoiding significant damage to the financial system that could result from the failure of a registered bank.

It might be all very interesting to know that an incumbent left-wing government really doesn’t like non owner-occupiers buying housing, but what of it? If such activity threatens the soundness of the financial system the Bank should (have) acted anyway, and if it doesn’t well….they can’t. And any such interventions are all-but certain to detract from the efficiency of the financial system, a (statutory) consideration one never hears of from the Governor (except perhaps when he thinks banks don’t lend to people he thinks they should – but that is no definition of efficiency).

There is just nothing in the Act that allows the Bank to focus on the soundness or health or performance of anything other than the financial system (as a whole). And yet they appear to be lining up new restrictions on interest-only mortgages (see above) to help the government out politically, and pursue’s Orr’s own political agendas, not to underpin the soundness and efficiency of the financial system. (As he noted, using debt to income restrictions – which he is legally free now to deploy, if doing so would support the soundness and efficiency of the system, already buttressed by very high capital requirements – would almost certainly cut further against the government’s bias towards first-home buyers.)

Policymaking in this country has been going backwards for years. We see examples of it all the time (another recent one is of course the Climate Commission’s secrecy around its modelling, Treasury’s secrecy around relevant analysis), but the housing market and housing finance markets seem particularly egregious examples, where more interventions keep on substituting for addressing issues at source, adding ever more inefficiency and papering over the cracks (hoping prices will level off for a while and the political heat will recede) rather than cutting to the heart of the problem. It is bad enough when governments and government departments do it, worse when autonomous agencies like the Reserve Bank weigh in beyond their mandate, pursuing personal and political agendas. And whatever limited value an independent international agency like the IMF might have brought to the policy debate, is severely undermined when – supported by no analysis whatever – they just weigh in largely echoing the preferences of the moment of domestic political playersa.