Various media outlets over the last day or so have asked for my views on whether banks will, or should, pass through yesterday’s 25 basis point cut in the OCR into lower retail rates.

My bottom line was

“I think there will be political pressure on the banks to cut to some extent, but I’d be surprised if it [any cut in floating mortgage rates] was anything like 25 basis points.”

It didn’t even seem a terribly controversial point.

After all, the Reserve Bank had included this chart in the MPS yesterday

And they could have included one of credit default swap spreads for Australasian banks (as per this one at interest.co.nz).

The Bank even commented in the MPS that:

the cost of funding through longer-term wholesale borrowing has risen with the pick-up in financial market volatility (figure 4.3). The increase in longer-term wholesale costs this year adds to the increasing trend since mid-2014, which reflects a mix of global regulatory changes, concerns about commodity markets and emerging economies, and broader financial sector risks. To date, strong domestic deposit growth has limited the need for New Zealand banks to borrow at these higher rates. However, acceleration in credit growth over the past year might increase banks’ reliance on higher-cost long-term wholesale funding, leading to higher New Zealand mortgage rates.

It has been a commonplace in the recent Australian discussion that unless the Australian cash rate is lowered higher mortgage rates seem quite likely because of the rising funding spreads.

And so I was slightly taken aback to see the Governor, and his offsiders, quoted as having told Parliament’s Finance and Expenditure Committee that

“I’d expect the floating rates to come down by 25 basis points,” Wheeler told the select committee.

and that

“Banks are only raising a relatively small share of their funding from overseas at this point in time. They’re continuing to see very strong deposit growth. Most of the credit expansion that’s going on has been funded through deposits,” Hodgetts said.

Central bank governors aren’t there to provide defensive cover for banks’ pricing choices, but neither should they be winning cheap popularity points in front of committees of politicians by calling for specific cuts in retail interest rates that don’t even look that well-warranted based on their own analysis (eg the MPS quote above).

Bernard Hodgetts, head of the Bank’s macro-financial stability group, argues that rising offshore funding costs aren’t really relevant because banks haven’t raised much money in those markets recently. But surely he recognizes the distinction between average costs and marginal costs? For the banking system as a whole, the place where they can raise additional funding – much of which has to be for term, to satisfy core funding ratio (and internal management) requirements – is the international wholesale markets. And what banks would have to pay on those markets in turn affects what they are each willing to pay for domestic term deposits.

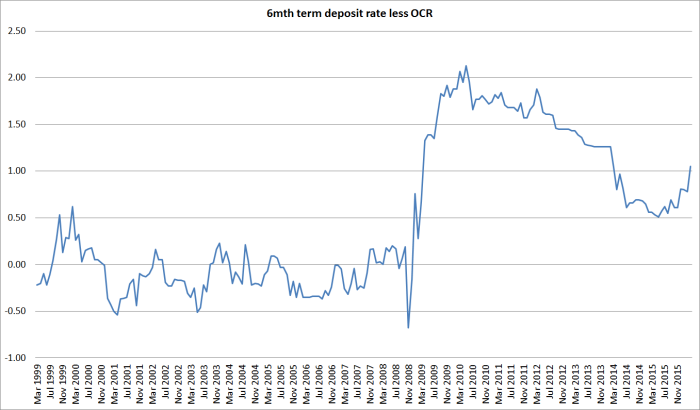

There isn’t a one-to-one mapping between rises in indicative offshore funding spreads and spreads of domestic terms deposits, but hereis a chart showing the gap between term deposit rates (the indicative six month rate on the RB website) and the OCR.

Unsurprisingly, it looks a lot like the indicative offshore funding spreads chart above.

And what about the relationship between floating mortgage rates and the OCR? Here I’ve shown the gap between the floating first mortgage new customer housing rate and the OCR. I’ve included yesterday’s OCR cut and assumed that banks eventually cut their floating mortgage rates by the 10 basis points the ANZ, the biggest bank, announced yesterday.

The resulting gap doesn’t look particularly surprising. The gap between mortgage rates and the OCR blew out during the 08/09 crisis when funding spreads and term deposit margins blew out. It came back from those peaks and has been fairly stable since – narrowing a bit further a couple of years ago, when it looked as though funding spreads might continue to narrow (and when banks were trying to get loans on their books in face of the new LVR controls). And now, perhaps, those spreads are widening out again – as one might expect given the persistence of the rise in the offshore funding spreads.

All these points are really illustrative only. I don’t have access to more precise data. But as in any business, pricing involves some judgements. Perhaps the political and customer pressures will mount and banks will find themselves having to pass more of yesterday’s OCR cut into lower retail lending rates than they would really like. But this is a repeated game. Even the Reserve Bank expects one more OCR cut before too long, and many of the banks now expect at least one beyond that. Over the course of the rest of the year, it seems likely that unless those international funding spreads start sustainably falling again, that retail interest rates will fall by less than the fall in the OCR. It has happened before – most notably in 2008/09 – and will happen again. And it works both ways: if funding spreads ever go back to pre-2008 levels, retail rates will fall further than (or rise less than) the OCR. The Reserve Bank takes those factors into account when it sets and reviews the OCR every few weeks.

From my perspective, the prospect that retail rates might fall less than the OCR is neither good nor bad, it just is. As in any business, costs are an important consideration in pricing, but retail mortgage banking is also a pretty competitive business. Banks don’t need our sympathy, but we also don’t need populist anti-bank cheap shots.

The right answer for the Governor, asked by MPs whether banks would pass on the lower OCR, would surely have been something along the lines of “That is up to them. They operate in a competitive market, and they face a variety of cost pressures. We’ll be keeping an eye on each stage of transmission mechanism – between OCR changes and eventual changes in medium-term inflation – and will adjust the OCR as required to deliver on the target set for us in the PTA”.

“They operate in a competitive market, and they face a variety of cost pressures.”

Perhaps more the truth would be:

“They operate a rigged market and are finally facing some regulatory push back although even that is unlikely to put a dent in their ever increasing profits”.

http://www.smh.com.au/business/banking-and-finance/rate-rigging-case-a-credit-negative-for-anz-moodys-20160310-gnfekl.html

LikeLike

That sort of stuff used to go on all the time with the NZ BKBM benchmark rate – and in the days before the OCR in some other rates the RB set off market rates – but note that I only described the retail mortgage market as pretty competitive. I stand by that proposition – it is one of the reasons why when funding spreads aren’t moving, OCR changes flow into floating mortgage rates almost immediately.

No market is perfect, and for a long time banks probably made a bit more money on the floating rates (for existing customers) while competing very aggressively in some of the fixed rate segments. Competitive markets require sellers willing to compete, and buyers willing to change seller.

LikeLike

‘No market is perfect’ is a bit of an apologist line for criminal behaviour. The penalties need to move to custodial sentences as opposed to fines.

LikeLike

Except that I still wasn’t talking about the CBA stuff, but about the retail mortgage market.

Having said that, I’m much less convinced that much of the shady activity in other parts of banking should be criminalized at all. I don’t have a strong view on it, but (eg) when I hear Democrats in the US saying “people should be in prison for the crisis of 08/09”, I think it is more about a search for a scapegoat than a genuine understanding of why either banks failed (mostly down to govt choices) or why western economies have been growing in such a disappointing way for the last decade (mostly probably declines in underlying productivity growth.

LikeLike

And then there’s this sort of stuff too;

http://www.smh.com.au/business/banking-and-finance/former-chief-medical-officer-sues-comminsure-for-wrongful-dismissal-20160309-gnelxz.html

LikeLike

There is usually a lag time between the key benchmark 90 day bank bill interest rates and the OCR. It currently still sits at 2.5%. That rate will have to fall first before banks would react with their retail interest rates. But it is a question of “when?” rather than “if?”

http://www.rbnz.govt.nz/statistics/key-graphs/key-graph-90-day-rate

LikeLike

If 44% of dairy farms are potentially in default. This small drop is not going to cut it. Once you are in default you at the mercy of the banks. The default interest rates can escalate to 20% to 30% interest rates a month. The intent is to wipe out any remaining equity in your property and to seek a mortgagee sale.

Grant Robertson did make a good point on a government bail out. I do wish he could be more sure of statements instead of stammering out on talk back radio that a bailout is a maybe, or a could be or a not sure, yes , yes, maybe , maybe, probably under a Labour government.

LikeLike

A bailout could take the form of Landcorp/government taking over the loan from a private bank and perhaps also direct ownership in the farms, retaining the farmer as the farm manager until milk prices recover and normal lending can be retained from private banks.

LikeLike

Landcorp? They’re a Solid Energy in waiting.

LikeLike

But why do you favour a state bailout at all? Doing so would represent a completely unnecessary additional of more moral hazard to the system. And the banks have adequate capital – and an incentive to raise more if needed.

The OCR cut, and ones to come, won’t be about stablising the dairy industry. (Although, being a little provocative, if it were not for the huge upsurge in foreign students and tourists that you frequently remind me of, the OCR cuts – and the resulting fall in the exch rate – would be much larger.)

LikeLike

When a industry that has $12 billion in GDP takes a dramatic 50% plus decline and has 44% of farms underwater with potentially $32 billion in loans affecting farms & banks plus a potential flow on multiplier effect, at some point that pain would have to spread nationally. A bailout would prevent a domino effect of a total collapse of dairy farms scenario plus supporting businesses. I think in that context I would consider it a national disaster and a taxpayer bailout would be a stabilising factor.

We should be thankful that we have foreign students and tourists surging 31% to mitigate and damped a recessionary impact.

LikeLike

“retail mortgage banking is also a pretty competitive business”. Not too sure how much competition there is when every bank appears to be making record compound profits year on year.

LikeLike

“And then there’s profitability. New Zealand’s major banks remain among the most profitable in the developed world. Here’s Standard & Poor’s (also see their chart below), which noted the “oligopolistic nature of the (NZ) system.””

http://www.interest.co.nz/opinion/80533/gareth-vaughan-argues-banks-not-passing-full-25-basis-points-ocr-cut-not-justified

LikeLike

Personally I think historical profitability ratios aren’t very relevant to this issue. After all, S&P themselves give only quite low standalone ratings to the NZ banks. MOre generally, if there are concerns about excess profits on average it is a matter for the Commerce Commission. What matters here is that the marginal cost of new market funding has been rising, which is generally going to be more relevant to product pricing than a cut in a rate which banks don’t, and won’t borrow, much at. But there is now a market test: BNZ hasn’t cut at all, and Coop has vut by 25bps. Will BNZ lose more business as a result than it is comfortable with? Only time will tell.

LikeLike