Dating back to before they took office in 2017, Labour’s stance on New Zealand immigration policy hasn’t been particularly clear. There was the 2017 policy, announced under then-leader Andrew Little, that was sold as being likely to make a big difference, but once one looked into the details (see link earlier in the sentence) it was clear it was designed not to do so. But then the leader changed, and little was heard of the policy on the campaign trail (people close to Labour told me that Ardern had made clear that she wasn’t that keen on the policy). Labour and New Zealand First then became government, explicitly agreeing to operate on Labour’s immigration policy, but apparently – so a NZ First minister told me – with an agreement to revisit the policy mid-term. If so, not that much of substance ever seemed to flow from that, although in early 2019 there was (ill-advertised) agreement in principle to changes down the track in how the residence programme was designed and run.

Then, of course, Covid intervened. There hasn’t been much non-citizen immigration at all since then, but no one envisaged that as a permanent model. And, of course, Labour secured an absolute majority at the last election, and selected a new Minister of Immigration.

Last month, the government finally got round to asking the Productivity Commission to do an inquiry into immigration policy. (I say “finally” because whether or not one approves of something like the current approach to immigration policy, that policy has clearly been one of the largest government economic policy interventions over several decades now, and the evidence-base around the economic effects of this large intervention, in the specific circumstances of the New Zealand economy, is disconcertingly light.) But then we are given to understand that the government has made up its mind anyway (which is, of course, their right as the elected government, but seems an odd ordering, when you’ve been in government for getting on for four years).

Here was the Prime Minister in her speech last week (emphasis added)

In terms of immigration going forward, last week we announced that the Productivity Commission will hold an inquiry into New Zealand’s immigration settings.

The inquiry will focus on immigration policy as a means of improving productivity in a way that better supports the overall well-being of New Zealanders.

The inquiry will enable us to optimise our immigration settings by taking a system-wide view, including the impact of immigration on the labour market, housing and associated infrastructure, and the natural environment.

This will sit aside existing work being led by the Immigration Minister around reforms to temporary work visas and a review of the Skilled Migrant Category visa.

In fact this Monday Minister Faafoi will be outlining the case for change in New Zealand’s immigration policy in a speech in Wellington.

But let me be clear. The Government is looking to shift the balance away from low-skilled work, towards attracting high-skilled migrants and addressing genuine skills shortages in order to improve productivity.

So I looked forward to reading the Faafoi speech, with interest tinged with scepticism. Specially invited guests, some from out of town, must have looked forward to it too – even if for some their interest might have been tinged with apprehension. There are a lot of champions of large-scale non-citizen immigration out there – from the Green Party (who seem keen on importing supermarket workers) to much of the “big end” of town.

As it happens, Mr Faafoi was apparently sick yesterday, and so the Minister for Economic Development Stuart Nash got the job of reading Faafoi’s speech, and was reportedly then unable to answer most questions.

The speech itself seemed to have been downgraded – the PM had trailed it as making the “case for change”, but the minister’s heading was simply “Setting the Scene”. But it was barely even that. I guess we came away with the message that “we are determined not to return to the pre-Covid status quo”, but there was almost nothing of the how – no specifics at all – and very little, in any sustained sense, about the why. There was no evidence in the speech of any rigorous thinking, analysis or research from officials – the sort of work one might normally hope for (especially for a government four years in) in advance of policy decisions and announcements. Particularly unkind observers suggested that the speech was more in the nature of “an announcement about an announcement”, of the sort that has become all too familiar. In fact, we were told that “we’ll be engaging with you [who?] over the coming months to test our thinking”, suggesting there just isn’t much there yet.

And I say all this as someone who might, possibly, be somewhat sympathetic to some elements of the broad direction the government might be heading in around immigration (even while being highly sceptical of Stuart Nash’s statist centralised approach to business and the economy, and prone to scoff every time I read another reference to the vaunted Industry Transformation Plans, in which bureaucrats take the lead in (purporting to) shaping the future of one industry after another (a tourism one got a mention last night)).

There isn’t much point trying to unpick Faafoi/Nash’s speech bullet point by bullet point (for some unaccountable reason it appears on the Beehive website with every sentence a bullet point). But in this post I just wanted to address a claim made in the speech.

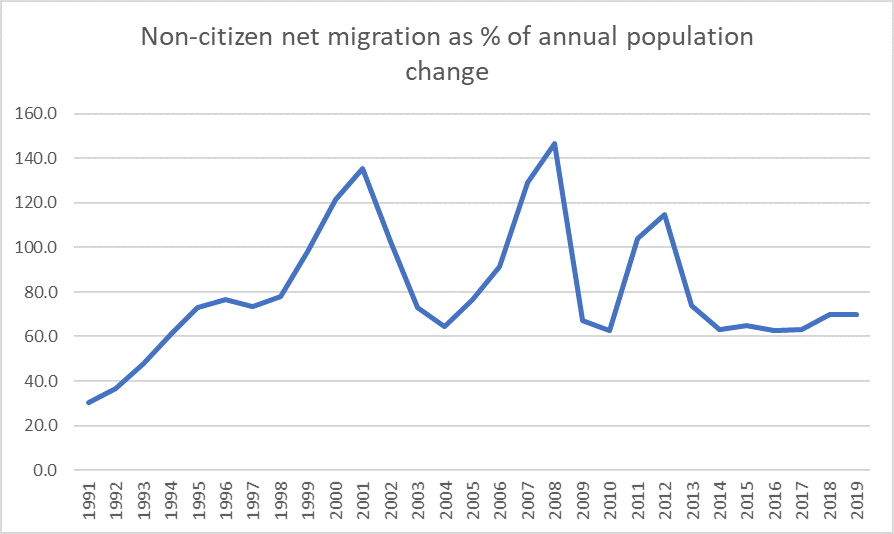

High levels of migration have contributed to 30 per cent of New Zealand’s total population growth since the early 1990s.

The “early 90s” is not only when the current broad approach to immigration was being introduced, but it is also when the current official population series begins.

Now I’m sure that one of the first things MBIE officials tell each Minister of Immigration is that to talk of “migration” isn’t very helpful in a policy context. There are inflows and outflows of New Zealanders and non-New Zealanders and the only bit policy controls is about the movement of non-citizens (arrivals, and departures for those on limited term visas). So in a speech on immigration policy, one might expect that the Minister of Immigration would focus his analysis on the movement of non-citizens. And that offers a quite different picture than the one Faafoi/Nash painted in the speech.

Here is a chart showing net non-citizen migration as a percentage of New Zealand’s population growth for each calendar year from 1991 to 2019 (I left off 2020 because the net migration numbers for that year are still estimates and the SNZ model for estimating these things for very recent periods isn’t great in normal times, yet alone Covid times)

Not even in 1991 was the contribution of non-citizen net migration quite as low as 30 per cent, and 1993 was the last time the contribution (to a first approximation, the contribution of immigration policy) was below 60 per cent. Of the year to year variation, some represents variation in the number of non-New Zealand migrants, but much represents variability in the (net) out-migration choices of New Zealanders (mostly to Australia).

There are plenty of people who will think the numbers in the chart are a good thing. I don’t, given what we know about the continuing long-run bleak underperformance of the New Zealand economy. But whether or not you welcome these trends, they are the (relatively) hard data. For decades now – well, prior to Covid – New Zealand’s pace of population growth, which is among the highest of the OECD countries, has been largely an immigration-policy-driven phenomenon. No OECD country envisages a larger share of population growth coming from non-citizen immigration, and most envisage a far smaller share. And if anything, these data are likely to understate the true population consequences of immigration, since the median migrant tends to be relatively younger, and the children of those migrants – themselves New Zealand citizens – will have further contributed to the growth of the population.

Rapid (policy-led) population growth in such a remote location appears to have impeded the prospects for any reversal of the decades of productivity underperformance. It has skewed the economy inwards, persistently overvaluing the real exchange rate and thus crowding out potential export industries. Wage growth in New Zealand has been weak, but that isn’t directly some immigration phenomenon – such discussions, including the Minister’s, consistently ignore the demand effects of high immigration – and the data show that, for the economy as a whole, wage growth has tended to run quite a bit ahead of growth in the economy’s earnings capacity (nominal GDP per hour worked).

When the government finally gets round to specifics one can only hope their policy decisions are based on better analysis, including the some robust economic analysis of the specific New Zealand experience, than was evident in the speech last night.

And when the champions of mass-migration splutter at the general thrust of the government’s aspirations, perhaps they might offer some thoughts on what it is about New Zealand that means that – in their view – we need to be uniquely heavily dependent on large scale non-citizen immigration.

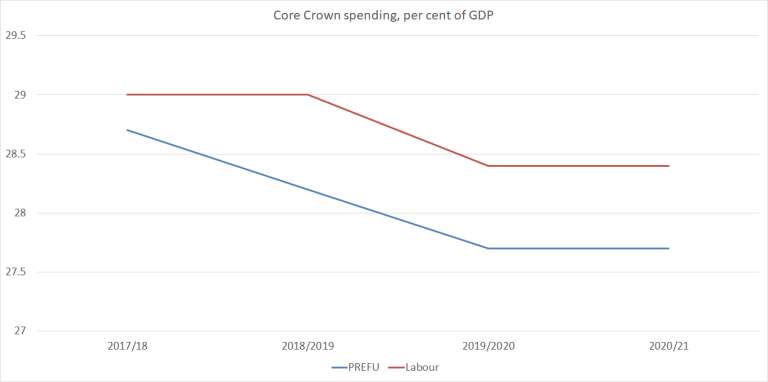

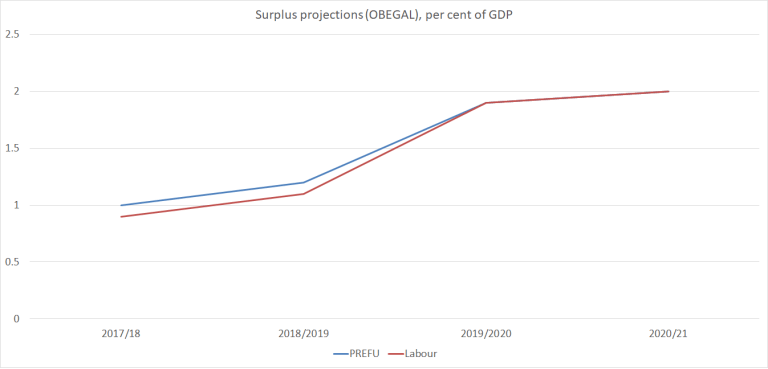

When net core Crown debt is already as low as 9.2 per cent of GDP – not on the measure Treasury, the government and Labour all prefer, but the simple straightforward metric – what is the economic case for material operating surpluses at all? With the output gap around zero and unemployment above the NAIRU, it is not as if the economy is overheating (the other usual case for running surpluses). Even just a balanced budget would slowly further lower the debt to GDP ratios. One could mount quite a reasonable argument for somewhat lower taxes (if you were a party of the right) or somewhat higher targeted spending (if you were a party of the left, campaigning on structural underfunding of various key government spending areas).

When net core Crown debt is already as low as 9.2 per cent of GDP – not on the measure Treasury, the government and Labour all prefer, but the simple straightforward metric – what is the economic case for material operating surpluses at all? With the output gap around zero and unemployment above the NAIRU, it is not as if the economy is overheating (the other usual case for running surpluses). Even just a balanced budget would slowly further lower the debt to GDP ratios. One could mount quite a reasonable argument for somewhat lower taxes (if you were a party of the right) or somewhat higher targeted spending (if you were a party of the left, campaigning on structural underfunding of various key government spending areas).