I watched the TVNZ Q&A interview with the Prime Minister yesterday. Apparently, the National Party has a widely-distributed brochure suggesting that interest rates are set to rise if the Labour Party takes office after the election. I haven’t seen the brochure, but the Prime Minister seemed determined to defend the claim, even as he had to concede that – of course – he couldn’t guarantee that interest rates would not rise over the next three years if his own party was re-elected. When pushed, his claim seemed to reduce to the proposition that interest rates were more likely to rise, and perhaps might rise more, if Labour was in office.

I know that a lot of people now have a lot of debt, and most New Zealand loans reprice pretty frequently (floating rate or short-term fix). But no serious person will argue that interest rates are quite low at present because the economy is doing well. Market interest rates around the advanced world (and central bank policy rates) have been very low for some years now, despite all the public and private debt, because demand (real economic demand) at any given interest rate isn’t what it was. Population growth has slowed in most countries (not New Zealand of course), productivity growth has slowed, and there just don’t seem to be the number of profitable investment opportunities there were. Globally, higher interest rates would, most likely, result from some improvement in the medium-term health of the economy. That would be true here as well (with the caveat that ideally one day some government would make the sorts of policy changes that would allow the persistent gap between New Zealand and “world” interest rates to close.)

But the Prime Minister’s claims about interest rates were also odd because:

- actual retail interest rates (those ordinary people pay and receive) have been rising over the last year, and

- both the Reserve Bank and The Treasury have official published projections showing policy interest rates rising over the next three years.

The increases in actual interest rates over the last year havn’t been large (about 25 basis points for floating rates, and something less for deposit and business overdraft rates). But as we’ll see, those are large changes compared to the sorts of effect the Prime Minister seemed to be talking about.

And what about the next few years, on current policies (monetary and fiscal)? These are the projections from the latest Reserve Bank Monetary Policy Statement and from The Treasury’s PREFU.

The Reserve Bank doesn’t expect much of an increase in the OCR over the next three years, but it is an increase nonetheless. The Treasury seems quite gung-ho – by the time of the next election, they expect we’ll have seen 150 basis points of interest rate increases. I suspect that Treasury’s numbers are too high, but both sets of projections are (a) upwards, and (b) well within the historical margins of uncertainty. Neither agency gives enough weight, at least in what they are saying in public, to the possibility – again well within historical bands of uncertainty – of materially lower interest rates. It seems unlikely that the Prime Minister would welcome a world in which such interest rate cuts were required.

The Prime Minister’s specific claim seemed to be that the Labour Party’s fiscal policy would result in higher interest rates than the fiscal policy adopted by the National Party. He attempted to muddy the water with talk of what any Labour coalition parties might demand, but of course on current polling it seems likely that any National-led government would also have to face coalition party demands. So, for now, lets just focus on actual main party plans – National’s as per the PREFU, and Labour’s as per their published fiscal plan.

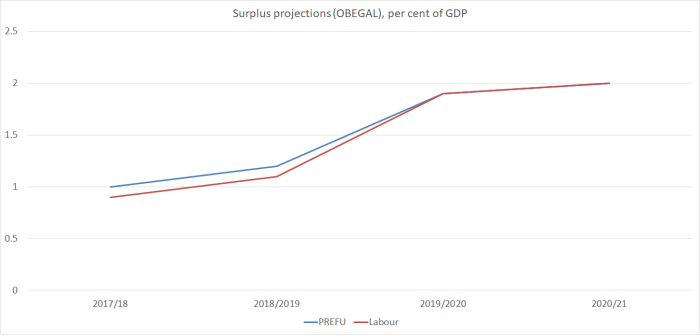

There would seem to be two plausible channels through which fiscal differences might mean different interest rates. The first would be if Labour was to run materially lower surpluses, or even deficits. The increased demand that would flow from those annual spending or revenue choices might, all else equal, lead the Reserve Bank to raise the OCR. But here (as I’ve shown before) are the two surplus tracks.

They are all but identical, especially when one bears in mind that the Reserve Bank is typically looking a couple of years ahead in setting interest rates. If Labour does take office, no Reserve Bank Governor – acting or otherwise – is going to be looking at that track, with a slight difference in 2018/19 and none beyond that – and altering his or her interest rate projections.

The other channel is through a stock effect; the effect of a higher accumulated stock of debt. The Minister of Finance has attempted to highlight that Labour’s plans involve around $7 billion more of net core Crown debt in 2020/21. Sounds like a lot of money. In fact, the difference is 2.2 per cent of GDP. And around half that difference doesn’t show up in a true net debt series (such as that reported by the OECD) at all: it is the additional $3 billion of contributions to the NZ Superannuation Fund. I don’t happen to think that resuming those contributions is particularly sensible, but both main parties do – their only difference is timing – and if contributions to the NZSF add a bit more risk (variability) to the Crown balance sheet, they don’t make us poorer. It is very very unlikely that raising a little more gross debt to put money in an investment fund like the NZSF will have any effect at all on New Zealand retail interest rates.

But what does the research show? Disentangling the determinants of New Zealand interest rates isn’t easy, and I’m not aware of (m)any new studies over the last decade or so. But a couple of prominent New Zealand economists did some interesting modelling work on the issue back in 2002, for Westpac. Adrian Orr is now head of the NZSF – and perhaps a contender for being the next Governor – and Paul Conway is head of research for the Productivity Commission. They looked at the impact of net government debt (not idiosyncratic national definitions, but drawing from international databases), and this is what they found

Table 2 shows the marginal and total impact of government debt on real bond rates. Moving from a net debt level of 10% of GDP to 20% of GDP adds only 3bps to real rates and the total contribution of debt to the risk premium is only 6.5bps.

As one might expect, the effects were quite a bit larger when debt levels were a lot higher than they are in New Zealand.

On these internationally comparable net debt measures, current net government debt in New Zealand is about 9 per cent of GDP, and on both National’s plans and Labour’s will fall from here. Labour reduces public debt a bit less than National does over the next few years, but recall that by 2020 even on the Treasury measure of net debt the difference was 2.2 per cent of GDP. Applying the Orr/Conway model results (that 6.5bps for 10 percentage point change in debt), and even that increase will produce only around a 1 basis point change in interest rates (with significant margins of uncertainty around those estimates). And these are long-term government bond rates they were modelling. Any effect on short-term retail rates – probably zero – would be indiscernible.

Are they other possible differences in interest rates that might show up depending on who wins the election? These ones occurred to me:

- both parties, but perhaps particularly Labour, look likely to have some difficulty keeping to their announced spending plans in the next few years, given baseline cost and population pressures and the recent electoral auction. Whether that would result in smaller surpluses depends on what other offsetting actions respective governments might take (and, of course, what happens to revenue flows).

- one reason why Labour’s net debt numbers are a bit higher than National’s is Kiwibuild. In the Labour fiscal plan, they allow $2 billion of new and additional debt to get the Kiwibuild programme going (intending to roll that forward as new houses are built and sold). I suspect that much of the Kiwibuild activity will displace private sector construction, but if it doesn’t – and it actually adds to total construction activity – that would put more pressure on available resources and – all else equal – increase the chances of OCR increases in the next few years. But since both sides agree that more houses need to be built, it is hard to see how either could describe any such increase in the OCR as a bad thing – if anything, in their own terms, it would be a mark of success.

- Labour is talking about reducing net immigration inflows. I’m a bit sceptical as to whether they would carrry through on that, given the evident decision to downplay the issue since Ardern took over. But if they do follow through, there would be a reasonably material reduction in overall demand and resource pressures over the next 12-18 months (especially as their proposed cuts are focused on the student sector). All else equal, that would reduce the chances of OCR increases in the next couple of years.

- Labour is promising Reserve Bank reforms. Much is likely to depend on the key individuals they appoint, but – all else equal – their proposal to add an unemployment objective would be likely to reduce the chances of near-term OCR increases. (In the longer-term there is a risk, that would have to be managed, that such a reform could slightly increase longer-term inflation expectations, and thus the level of nominal interest rates.)

In the end, this is fairly silly debate. The differences in fiscal policy are small, and the track record of the two main parties over 30 years now is of pretty responsible fiscal management. Debt levels are low and, absent a severe crisis, near-certain to remain so.

And interest rates do move around. In well-managed countries they most often rise when economies have been doing pretty well, and they fall when something bad happens. What will determine what happens to interest rates – market and official – over the next three years? It won’t (overwhelmingly) be our choice of Prime Minister, but – in the famous phrase of Harold MacMillan, former British Prime Minister – “events, dear boy, events”.

And we, they (politicians) and the Reserve Bank should fear the sort of events that could yet take our interest rates quite a bit lower than they already are.

It’s hard to see how Labour’s policy mix would materially impact interest rates relative to a National party baseline. Their fiscal stance would be modestly easier and distributed more to lower income households and that coupled with higher low-end wages may provide some support – but then they’re likely to reduce immigration and that would take demand from the economy while they’re also likely to support a more dovish RBNZ. In the longer term this may push up long-rates but it’s probably likely to see lower rates, at least initially.

With the ToT at record levels and demand sluggish it’s hard to see the C/A deficit widening significantly under either policy path – the C/A is going to be driven more by global interest rates and the ToT. With a more dovish RBNZ and greater policy uncertainty the NZD is likely to be weaker, perhaps materially (>5%) but given the very low exchange rate pass through its hard to see that having much impact on inflation and the rbnz would look through it in any case.

It’s a shame that National has decided to campaign negative. It worked in the US with Trump and in the U.K. but I’m not sure kiwis are receptive to it and if they are I’d say we’d be seeing much stronger polling for NZF.

LikeLike

I guess after nine years there isn’t much positive to campaign on (housing, productivity, water, standards in public life? )

LikeLike

I do not think National is running a negative campaign when it is clearly pointing out the significant holes in Labours budgetting numbers.

Monorail will cost from $5 to $15 billion not the measly $2 billion.

Len Brown’s intercity rail tunnel already has a couple of billion shortfall just to get a Mt Eden from $2 billion will likely cost $4 billion.

Kiwibuild is way off the budgetting trail. The $2 billion offered by Labour will only cover the upfront land cost. It will cost another $4.5 billion to build the 10,000 houses needed within 12 months plus another $2 billion for infrastructure

Education has a $300 million shortfall

Health has another $300 million shortfall.

Clearly there is a form of a inheritance tax when you inherit your parents property, that becomes a second property which will trigger CGT on the eventual sale. Labour either does not understand the transaction or is just lying.

Also loss of negative gearing on Investment property is planned to occur almost as soon as Labour takes government. That is a tax change. This no tax change being bandied around by Jacinda Ardern is just another lie.

Also National is planning a tax cut so any reversal of that tax cut is a tax increase which Jacinda denies. Therefore the negative campaign is being run by Jacinda Ardern not National.

LikeLike

The bigger issue for the RBNZ – and interest rates – is the increasingly clear evidence of a flattening Phillips Curve. To get inflation up to the 2% mid point on a sustainable basis will require much higher wage inflation and to achieve that we need lower unemployment; in other words there’s growing evidence the NAIRU is a lot lower than the RBNZ or Treasury believe (my own calculations are around 3.5%) in line with your views Mike.

LikeLike

An increase in wages substantially in NZ would not move inflation up to 2%. You ignore the overproductive capacity globally. Also the internet provides transparency to pricing worldwide with sites like Alibaba and Amazon giving access to the cheapest products available in the world. Our retailers and manufacturers compete with the cheapest products globally. Oil prices still continue to fall as EV cars become more available. This feeds into reduce freight and transportation costs and cheaper cost of materials for most of our consumer products which are plastic also a product of oil.

LikeLike

The Labour policy is to increase the minimum wage and to give the unions much more power. Some local authorities are moving to ‘a living wage’. Neither of these increases are driven by market forces.

Additionally there will be ‘flow-on’ relativity increases.

So there is an arguable case that for a short period wage rates and unemployment will be totally out of synch.

LikeLike

to my mind, as a debtor nation (mainly via the Australian owned banks), the NZ private sector borrower will remain a ‘price taker’ for a while yet: not that any government wants to put that on the Sunday morning breakfast menu…!

LikeLike

Without costing out Labours proposals I would never comment on their costs or potential for fiscal slippage and I wouldn’t make strong assertions either way but what I’d say is that some of the ideas being floated are not necessarily the right solutions but they are asking the right questions.

The Auckland Airport should be linked up to the southern rail network and they could easily run trains into britomart via that – for a fraction of the cost of a monorail and that’s probably a good solution.

As for getting rid of negative gearing on investment properties and having a CGT for those who make their money speculating in property all I can say is “bring it on.” And while they’re at it, clamp down on corporations taking the mickey out of us via transfer pricing to avoid tax and stop corporate welfare. If Tiwai Point can’t work as a stand alone or Sky City convention centre then let them fail.

Auckland ratepayers – and I am one – are being taken for a ride with this population ponzi. Much of our infrastructure and housing problem stems directly from this government’s abandonment of our borders. And as Michael had pointed out, the demand stimulus – which has fed the improved fiscal situation – had pushed up the NZD and caused so much distortion in the economy whether it’s inflated house prices or the under-performance of the tradable sector.

For mine, the key issue this government faces is that it’s forgotten how to listen. I’m not anti-National and I don’t believe Michael is either but people who think for themselves and who are prepared to stand up and challenge what’s happening have been automatically discounted. It’s a shame. I for one am heavily invested in my country…

LikeLike

The National government under John Key and now Bill English has never avoided asking the questions. The problem is not with government. The problem has been that NZ economists advice to government has been badly misguided. The problem is the answers not the questions.

LikeLike

Removing negative gearing is just discrimination against a small business that is offering accommodation to those that need to or want to rent. How is negative gearing speculation when it fulfill a business need. Housing meets one of three fundamental needs, food, shelter and procreation. getting rid of tax losses is just another nanny state approach dictating to people how and where they should invest. Most property investors are you working mums and dads saving through an investment property for a retirement income. Small business tax rules should be applied consistently rather than try and carve out bits and pieces and create distortions.

LikeLike

It is easy to say just link up and it is easy to say build monorail. Don’t forget there is private owners to deal with at every step of the way. Yes we do have the Public Works Act that allows for repressive regime type compulsory acquisitions but the National government chooses to respect and to provide full public consultations, compensation and voluntary departure before exercising the Public Works Act. That times time and alot of effort by the government.

Jacinda Ardern proposes to strip away those private ownership rights to force her monorail in and tax tax and more tax to fund her pet projects.

LikeLike

Our largest industries are International students and tourism which is a $15 billion industry. These are service based. Service equates to more people. It goes hand in hand. You can’t have one without the other and only miracle workers like NZ economists can imagine maintaining and growing a $15 billion service industry without more people. It is this sort of poor mathematical logic that has distorted the governments decision making.

LikeLike

Listening to Catherine Ryan’s interview with Bill English on RNZ this morning showed how completely biased against the National government she was. Bill English put up a fantastic interview even with Catherine clearly aggresively trying to trip him up. And everytime he clearly showed that he was a very capable leader and debater she quickly changed the subject. Very poor interviewer and a very clear bias towards labour and Greens policy debating Labour and Greens policy on their behalf and trying to foist a Wealth tax onto even the National government. Good thing that Bill English made it very clear it is never going to happen under National.

LikeLike