Checking back over my notes from the last Monetary Policy Statement press conference, I see that Graeme Wheeler told the assembled journalists that he would shortly be doing a speech that would answer many of their questions. He was, for example, asked whether he thought his critics had been fair and whether he had ever allowed his judgement to be clouded by those criticisms. Perhaps unsurprisingly, there was nothing on any of those sorts of points – or any of the others he suggested he would cover – in the speech he delivered yesterday to the Northern Club, safe from any further journalistic scrutiny.

In his term as Governor, Graeme Wheeler has given about 20 on-the-record speeches. The first one was to a private Auckland club, and so was the last one. And all the ones in between were given either to bureuacratic/academic audiences, or to business and finance ones. It will have been very much the same for the off-the-record addresses the Governor gives to commercial bank business clients the morning after each MPS. And unlike the practice of his RBA peers (who mostly put Q&A sessions up on the website), people not at these functions – generally accessible only to invited guests – don’t have access to his responses to questions. When his preferred audiences skew strongly towards one set of economic interests – so the questions and comments reflect their perspectives – that should leave us rather uncomfortable. Perhaps union groups or community groups, for example, wouldn’t have had any interest in the Governor speaking? But across the whole country, across five years, that seems unlikely. It should be something for the new Governor – whoever he or she is – to reflect on.

But this post is mainly about some of the points of substance of yesterday’s speech.

When, three weeks out from a general election, a press release turns up extolling New Zealand’s economic performance, one might have supposed it was a party political message on behalf of the incumbent government, or at least from one of their lobby group supporters. But this was from the outgoing – supposedly apolitical – central bank Governor.

His press release was headed “Reserve Bank policy a key driver in economic performance” and the opening sentence read

The Reserve Bank’s monetary policy has been an important driver in the last five years behind above-trend growth in the economy and employment,

Which is quite a curious claim – even without digging into the data – because generally the Reserve Bank shouldn’t be having that much influence on the performance of the economy. And the Bank’s main job is to keep inflation near target – and on that count it has repeatedly undershot throughout Wheeler’s term. Prima facie, that might suggest that, on average, monetary policy hasn’t done enough.

Wheeler’s claim seems to rest on the proposition that “during this time [the last five years] monetary policy has been stimulatory, with the Official Cash Rate averaging 2-3 percentage points below the neutral interest rate”. Since the OCR has averaged 2.55 per cent over his term, he seems now to be saying that the neutral OCR was between 4.5 and 5.5 per cent on average over the course of his term. I doubt there would now be many takers for that view, and if anything views on what a neutral interest rate might be have been being revised downwards. They have further to go.

But, let’s suppose that Wheeler is right on that count. If so, surely we should have expected a supercharged performance of the New Zealand economy. After all:

- although it is never mentioned in the speech, the terms of trade have been 10 per cent higher on average than they were during the Bollard decade,

- we’ve had a huge boost to demand from the repair and rebuild process in Canterbury (the initial disruptions and losses of output were all in his predecessors’ term),

- we’ve had another big population surge, and

- there have been no serious recessions or financial crises abroad.

Throw in highly stimulatory monetary policy, and we should surely have seen something pretty impressive. At very least we might have expected inflation to be at, or perhaps a bit above, target.

I don’t like to hold central banks to account for medium-term real economic outcomes. Central banks just don’t have that much power. So I don’t blame Graeme Wheeler or the Bank for, say, five years of zero productivity growth, while I do hold him responsible (solely responsible) for five years of undershooting (core) inflation.

But it is the Governor in his speech, only three weeks out from an election, who is actively trying to suggest not only that the New Zealand economy has done well in the last five years, but that he and the Bank deserve credit for that. Neither is true.

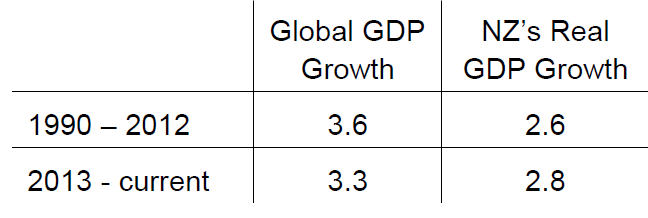

He includes a table which I’ve reproduced part of here, showing annual average growth rates

Inflation targeting began in New Zealand formally in early 1990. So Wheeler’s story is that while the world economy has done a little worse during his term that it was doing in the previous 20 years, the New Zealand economy has actually grown faster than it managed in the previous 20 or so years. Put that way, New Zealand’s performance looks good, and Wheeler appears to want to claim a considerable portion of the credit.

But this is the same nonsense that we get from the government, boasting about headline GDP numbers, and keeping very quiet indeed about the per capita performance. Over the Wheeler term – not directly influenced by him at all – New Zealand’s population is estimated to have increased by 8.5 per cent. Advanced countries in total have had a population increase of less than 2 per cent. Not surprising, headline GDP numbers here look moderately respectable.

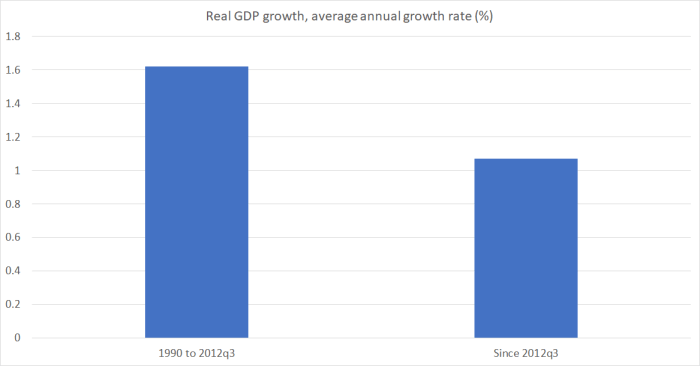

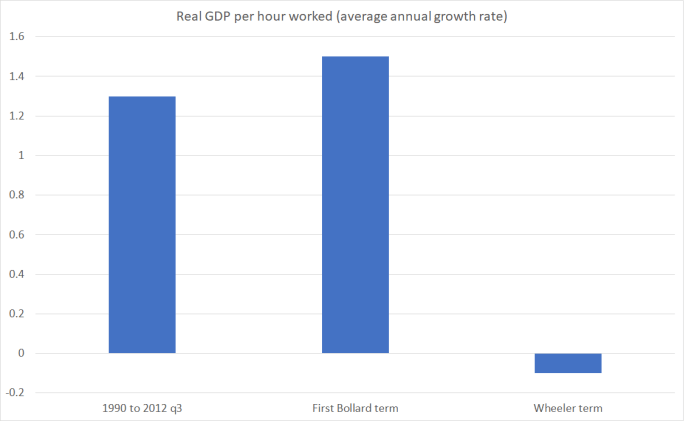

But how does per capita growth in real GDP compare? In this chart, I’ve shown the average annual growth rate in real per capita GDP for, on the one hand, the 22 years from when inflation targeting began to the end of Alan Bollard’s term as Governor, and on the other for the Wheeler term. Remember that in the first period there were three recessions, two quite severe ones, and in the more recent period there have been none.

The only other gubernatorial term in which there wasn’t a recession was Alan Bollard’s first term (to September 2007). Over that five year period real per capita GDP growth averaged 2.3 per cent per annum.

What about productivity? Wheeler does acknowledge that “labour productivity has been disappointing”, suggesting that this is a problem most other advanced countries have but consigning to a footnote the recognition that New Zealand has had no labour productivity growth at all in recent years (unlike, say, Australia or the United States).

Here is how New Zealand’s labour productivty growth has been over (a) the whole pre-Wheeler inflation targeting period, (b) the last gubernatorial term without a recession (which also featured a housing boom and material lift in the terms of trade) and (c) the Wheeler term.

To repeat, productivity is not something the Governor has much influence on, but…..it was him that was claiming credit for the “strong” performance of the New Zealand economy.

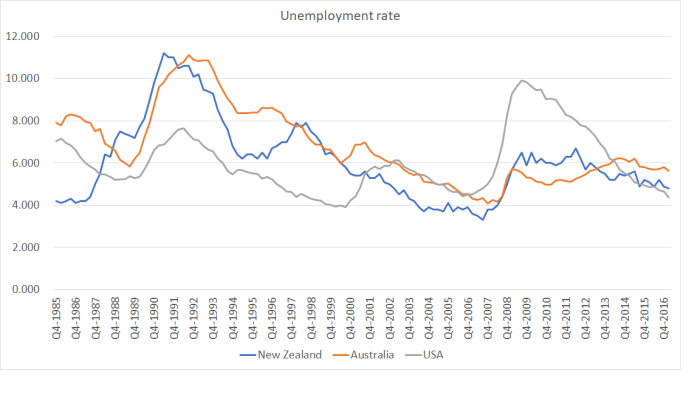

How about the labour market? The Governor highlights that employment growth has been faster in his term than in the earlier inflation targeting period, but doesn’t mention that working age population growth has also been much faster during that period. Actually, the rate of job creation relative to population growth hasn’t been at all bad in recent years – surprise increases in population create big increases in labour demand – but it is worth remembering that the quarter Wheeler took office saw unemployment at 6.7 per cent, the highest rate in the previous 13 years. So we’d have hoped to see employment rising strongly and unemployment falling. As it is, the unemployment rate averaged 4.8 per cent in the Bollard decade (boom and bust) and has averaged 5.4 per cent in the Wheeler term – and all this as reasonable estimates suggest that the non-inflationary unemployment rate (the NAIRU) has probably been falling.

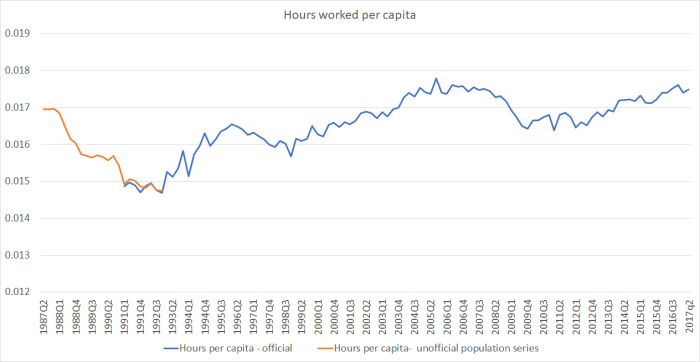

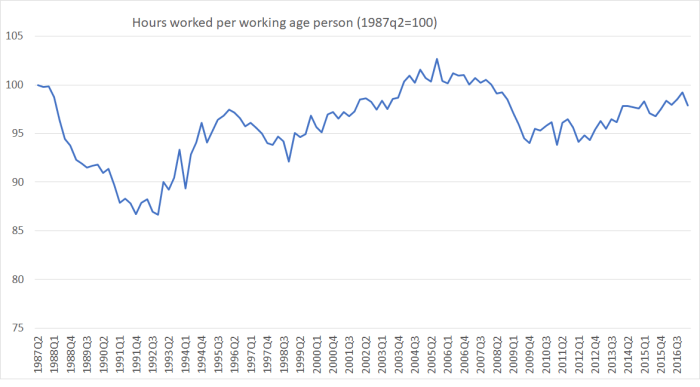

Even on the labour side of things, here is hours worked per person of working age.

Yes, the series has been recovering during the Wheeler term, from recessionary troughs, but is still not to the average levels prevailing for the four or five years prior to the recession. Perhaps those levels might have amounted to “over-full” employment, but the unemployment numbers don’t suggest we are at that sort of point now.

I’m really not quite sure what Graeme Wheeler thought he was doing in making these claims. I don’t really suppose that he intended to be party political – although the timing is such that he should have been more circumspect – and actually in a way his claims, if valid, would actually suggest some serious problems in the economy – if we could only manage such feeble outcomes even with highly stimulatory monetary policy. But I guess it was mostly an attempt at distraction, to keep the focus away from what might otherwise have been.

Wheeler couldn’t do anything about (a) the aftermath of Canterbury earthquakes or (b) the migration influx (in any case only a touch larger than his predecessor had had to deal with), both of which have skewed the economy away from the non-tradables sector, probably helping to explain the distinctively poor New Zealand productivity performance. He can’t do much about the neutral interest rate – whatever it really is – or about the troubling medium-term level of the real exchange rate. But he could have done quite a lot about inflation. Had he taken the steps that would have had core inflation averaging around 2 per cent – instead of 1.4 per cent – we’d have had a lower unemployment rate sooner, faster growth in per capita GDP (not indefinitely, but over this period), and stronger growth in employment and working hours. He’d have delivered on his primary statutory mandate, and most New Zealanders would have been better off.

Humans make mistakes, and institutional structures that put lots of power in the hands of one person are particularly prone to mistakes. The Reserve Bank of New Zealand is a good example of that, over the terms of successive Governors. There are some things to be said for Wheeler’s stewardship – as I’ve noted previously, core inflation has been quite remarkably stable during his term – but he seems determined to never acknowledge a mistake, even with the benefit of several years hindsight. Individuals and institutions that don’t even recognise mistakes struggle to learn from them. The Governor can repeat as often as he likes that local market economists and the relevant desk officer at the IMF thought the Reserve Bank was doing the right thing in 2014 (while ignoring the alternative minority voices). The fact remains that they weren’t doing the right thing, when judged against their own mandate. They remain the only advanced country central bank to have had two tightening phases since the last recession, and to have had to unwind them both. Some acknowledgement of, and regret for, those mistakes might have been a gracious way for the Governor to have left office. But I guess it is hard for leopards to change their spots.

I don’t want to spend any material time on the Governor’s treatment of housing market issues. There is still no sign that they really understand the issues that have driven house prices to such unaffordable levels. And I’m not going to bore you by running through the issues around LVRs again except to note that (a) there is no attempt to evaluate the Bank’s interventions against the only criteria the matter, the statutory responsibility to promote both the soundness and the efficiency of the financial system, and (b) my jaw almost dropped when I found no reference to any adverse effects on anyone of the LVR restrictions, except the rather self-pitying observation that “we were conscious that the introduction of LVR restrictions would make life difficult for the Bank”. Not nearly as difficult as it makes things for willing lenders and willing borrowers to put in place credit facilities……

The final point I wanted to touch on was the Governor’s disconcerting complacency about the next recession. The Govenor notes

If growth in the global economy slows because of debt-related or other issues, our economy will be affected. However, there is scope to help buffer against such shocks. We have greater room for monetary policy manoeuvre than central banks in many advanced economies. Our Official Cash Rate is 1.75 percent – above the zero and negative policy rates of several advanced country central banks – and the Bank has not grossed up its balance sheet by buying domestic assets. Similarly, with budget surpluses and low net Government debt relative to GDP, the Government has flexibility on the fiscal policy side.

Frankly, the issue that should be concerning the Bank isn’t some modest “slowing” in the global economy, it is the next serious global recession, the seriousness of which is likely to be accentuated by the fact that monetary authorities in most of the advanced world have very little scope to cut interest rates much. And there is about as little scope in most of those countries to do much with fiscal policy. In a typical US recession, for example, policy rates have been cut by around 7 percentage points. At present, the Fed funds target is around 1 per cent.

In a typical New Zealand recession, the OCR (or equivalent) has fallen by perhaps 5 to 6 percentage points (our exchange rate tends to fall too, unlike in the US). But our OCR is now 1.75 per cent, and inflation is well below target (the Bank thinks things are heading back to target, but their own official stance at present is neutral). And while it is fine to note that our fiscal accounts aren’t in bad shape, in any serious recession they will look a great worse quite quickly (in flow terms). There is some technical room for additional discretionary fiscal stimulus in a downturn, but the practical political room for additional discretionary stimulus has never been that large anywhere – see, for example, the battles in the US in early 2009 around the stimulus package.

So while it is better to be in our position than that of some other countries, our position isn’t very good either – and our Reserve Bank is responsible for our position, not that of other countries. Going into the 2008/09 recession the Bank could say with confidence that we would cut as far as was needed – and starting from 8.25 per cent, no one doubted our capacity. Going into the next serious recession, if starting from around the current level of the OCR, no one will believe the Bank can do, or the government will do, that much.

Throughout his term, Graeme Wheeler appears to have done precisely nothing to position the Bank to cope with the next serious downturn – despite all the advance warning, and experiences of other countries running out of conventional capacity. The issue has never appeared in his Statement of Intent, or in past speeches. He hasn’t got inflation back up to target, which would have led to nominal interest rates stabilising at a higher level than they are now. He hasn’t done anything about addressing the institutional issues that make the near-zero interest rate bound a practical problem. And, despite all that, he objects to any suggestion of raising the inflation target

It is not clear that central banks could readily increase inflation to these levels and attempting to do so would further stimulate asset markets, at least in the short run. Raising an inflation target when productivity growth is weak makes little economic sense.

Perhaps it is too late in some countries – although the largest of them, the US, has been raising interest rates, suggesting that a lower track of rates would produce somewhat higher inflation – but it clearly isn’t here. And as for the productivity argument, he has that quite back to front. In a climate of weak productivity growth, and weakening global population growth, the case for a higher inflation target is stronger than otherwise – precisely because there is more chance than otherwise that the near-zero bound would prove binding.

I guess the Governor has got to the end of his term and these particular risks haven’t crystallised. Now it will be someone else’s problem, and I don’t suppose the Governor will have to worry about being one of those caught unemployed for a prolonged period in the next recession. Forecasting is hard, and anyone can make mistakes. But failing to actively address this sort of foreseeable risk – timing unknown of course – is close to derelicition of duty in someone entrusted personally with all the powers of Governor of the Reserve Bank. Getting on with some serious work in this area should be a priority for the new Governor, and for the Treasury/Minister of Finance.

(And I suspect that the key clue to Wheeler is the “asset markets” reference in that last quote. There and throughout the speech his concerns about asset markets are pervasive. And yet there is little sign of analysis that offers insights into those markets, and no sign of any Reserve Bank statutory responsiblity for such markets.)

Finally, it was interesting that in his reflections the Governor chose not to touch on the governance issues. We know that he has favoured change (making he and the deputies he appointed collectively responsible under law). And we know that the Opposition parties favour change. And we know that Steven Joyce is sitting on (and refusing to release) a report to The Treasury commissioned from former State Services Commissioner, Iain Rennie on possible governance reforms. It would, nonetheless, have been interesting and timely to have heard the Governor’s reflection on the issue, in light of his five years’ experience.

I keep wondering why the Rennie report is being kept secret – months after it was completed. One possibility is that Rennie is recommending reasonably substantial changes, going further than the Minister of Finance might have envisaged when he asked for the work to be done. Whether that is so or not, there doesn’t seem to be any legitimate (OIA) reasons for the report (from a consultant to a ministry) to be kept secret.

And reform is overdue – we shouldn’t be running a system where when the outgoing Governor opines on what will happen to LVR limits everyone knows that a month from now his views will mean nothing and there will be a different single decisionmaker in place. Well-governed institutions are typically built around greater continuity and resilience to the preferences of single individuals.