The centrepieces of the two weekend TV current affairs shows were political debates: The Nation had Phil Twyford and Amy Adams on housing, and Q&A had Grant Robertson and Steven Joyce on the economy more generally (but with a large chunk on housing). I only saw the Q&A debate, but I have glanced through the transcript of Twyford/Adams.

In the course of his debate, Phil Twyford was asked how much house prices should be relative to income. His response was excellent

Twyford: Ideally, they should be three times. If we had a housing market that was working properly, your housing would be— the median price would be about three to four times the median household income.

Grant Robertson repeated those sorts of numbers in his exchange with Steven Joyce. It was good, clear, encouraging stuff. A reminder of just how totally out of whack things are in the New Zealand house and urban land market. And a suggestion that the main opposition party wants things to be materially different and better.

But I can’t help wondering in which decade they expect things to be more or less okay again. In time for, say, my children – perhaps 10 to 15 years from now – or will it only be the grandchildren?

Don’t get me wrong. Watching the Robertson/Joyce debate, as someone who has no idea who he will vote for, I thought Robertson had much the better of the housing side of the debate. The current government seems reduced to some mix of lamenting that it is “a global problem”, reluctantly conceding that Auckland prices are a bit too high, and claiming that just over the horizon there is a wave of supply that will substantially address the problems. So if I’m critical of Labour here, take for granted that almost all the criticisms apply with more force to National.

Here is Phil Twyford avoiding suggesting that Labour wants house prices to come down

So is it Labour’s goal to get it down to that – about four times?

Twyford: We want to stabilise the housing market and stop these ridiculous, year on year, capital gains that have made housing unaffordable for a whole generation of young Kiwis.

But in essence, you’re going to drop the value of houses, if you want them to be four times the price of the average income.

Twyford: Well, we’re going to build through KiwiBuild. We’re going to 100,000 affordable homes.

I want to come to KiwiBuild in a moment. I just want to talk to you about the price.

Twyford: That will make housing affordable for young Kiwi families. That’s our policy.

Stabilising the housing market, and ending rapid house price appreciation, isn’t a recipe for fixing up the housing market for the current generation of young people.

Grant Robertson was much the same – reiterating the goal of house prices of 3 to 4 times income, but he couldn’t or wouldn’t say how long it would take. There was plenty of talk about building “affordable houses” (around $600000?) and “cracking down on speculators” and beyond that it all seemed to be down to growing incomes. But there wasn’t even a mention of freeing up land supply – a topic where formal Labour policy looks better than anything else on offer from major parties. Even though, the largest single component in the increase in New Zealand (especially Auckland) house prices has been the land component.

On the other side of the exchange Steven Joyce was taunting Robertson with the suggestion that “Labour wants to crash house prices with a punitive capital gains tax” – as if, whatever the (de)merits of a CGT, much lower house prices would be the worst thing in the world.

Lifting growth in productivity and real incomes is highly desirable. All else equal, flat nominal house prices and faster income growth is a recipe for improved housing affordability. But how long might it take on reasonable assumptions?

I’ve shown similar charts on this point previously. Here I assume a starting point of a price to income ratio of 10 (around current Auckland levels) and that (a) nominal house prices hold at current levels for the indefinite future, and (b) incomes grow at a rate equal to 2 per cent (midpoint inflation target) plus the rate of economywide productivity growth. I’m just going to assume that the 2 per cent average inflation could be achieved quite easily if the government wanted to. Productivity is the harder issue. Here I’m showing four lines using:

- actual productivity growth (GDP per hour worked) over the last decade (just under 0.6 per cent per annum),

- actual productivity growth over the last thirty years (for which we have quarterly real GDP and hours data), of just under 1.2 per cent per annum,

- productivity growth of 1.5 per cent per annum, and

- productivity growth of 2 per cent per annum.

The straight line on the chart is at a price to income ratio of 3.5 (ie the midpoint of the 3 to 4 times income Labour is talking of).

On the best of these scenarios, price to income ratios get to 3.5 in about 27 years time. If we manage productivity growth equal to that for the last 30 years – which itself would be quite an achievement at present – we’d be waiting almost 35 years.

Affordable housing, and a functional housing market, for the current generation simply requires a fall in nominal house prices. And yet no major party politicians seems to have the courage, or the self-belief (in their ability to communicate and take people with them), to make that simple point.

For most existing home-owners, the market value of their house does not matter a great deal. A large proportion of home-owners have a modest mortgage or none at all, so negative equity isn’t a risk. And since most people retire in the same city they’ve spent their working lives in, their house price doesn’t even affect very materially their own expected future purchasing power.

Fear of falling house prices seems to reduce to two particular dimensions:

- people who, having bought in perhaps the last five years, would find themselves with negative equity if house prices fell markedly (in turn divisible between new owner-occupiers and purchasers of additional rental properties), and

- some generalised fear that a fall in house prices goes hand in hand with economic disaster, serious recessions and the sort of experience the US or Ireland had.

The latter is mostly a category error. In both the US and Ireland, there was material overbuilding (excess stocks of actual houses). There is no prospect of that situation in New Zealand on any of the policies of the major parties. In Ireland, the situation had been compounded by joining the euro, which gave Ireland interest rates set in Frankfurt that bore no relationship to the needs of the Irish economy. In the US, there had been persistent official efforts – from Congress, the Fed, and successive Administrations – to encourage, or compel, the financial system to take on housing lending risk that the private sector would be unlikely to have assumed willingly. None of that resembles New Zealand. Not only do we set our own interest rates, but to the extent there is state involvement in the housing finance market it is reducing the supply of credit.

A severe recession could, at least for a time, lower New Zealand house prices. Recessions – severe or otherwise – aren’t things to welcome. But the sort of land market liberalisation (with associated infrastructure rules) that might, as a matter of policy, set out to materially lower New Zealand house and land prices would be most unlikely to materially dampen demand or economic activity. If anything, it could represent a material boost to demand, as building became more affordable. (And if some people would find themselves with negative equity, whole swathes of younger generations would suddenly face new opportunities and less of a desperate need to save.)

What about the people facing negative equity? I don’t have any particular sympathy with those who’ve purchased investment properties in recent years and might face being wiped out. They’d have taken a business and investment risk – in this case on the regulatory distortions never being fixed – and lost. That happens in all sorts of market – think of the people with exposures to shares after 1987, or in finance companies 10 years ago. Or those with businesses based in import licenses in earlier decades. It is tough for them individually, and almost all of them have votes. But it was a business risk, and a conscious voluntary choice.

I’m much more sympathetic to those who bought a first house and could face a large chunk of negative equity. I touched on this in a post a few weeks ago

No one will much care about rental property owners who might lose in this transition – they bought a business, took a risk, and it didn’t pay off. That is what happens when regulated industries are reformed and freed up. It isn’t credible – and arguably isn’t fair – that existing owner-occupiers (especially those who just happened to buy in the last five years) should bear all the losses. Compensation isn’t ideal but even the libertarians at the New Zealand Initiative recognise that sometimes it can be the path to enabling vital reforms to occur. So promise a scheme in which, say, owner-occupiers selling within 10 years of purchase at less than, say, 75 per cent of what they paid for a house, could claim half of any additional losses back from the government (up to a maximum of say $100000). It would be expensive but (a) the costs would spread over multiple years, and (b) who wants to pretend that the current disastrous housing market isn’t costly in all sorts of fiscal (accommodation supplements) and non-fiscal ways.

Those numbers were made up on the the fly, but even on later reflection they look like a reasonable basis for something that might not be unreasonable, and also might not be unbearably expensive. It would recognise that people need to bear some material risk themselves (a 25 per cent fall in nominal house prices is not small). But it is also designed in recognition of the fact that since 2013, it has been hard for first home buyers to get a mortgage above an initial LVR of 80 per cent, so that not many would be in negative equity now even if house prices fell by 25 per cent from here.

Since many people will stay in their existing house for a long time if they have to, and the scheme only compensates if the house is sold, that also limits the potential fiscal cost. In fact, the biggest pool of owner-occupiers who would sell at a material loss would be those forced in the event of new severe recession (unemployment is typically the biggest threat to the ability to service mortgage debt) and (a) those people would naturally command a degree of public sympathy and (b) land liberalisation would be a stimulatory policy, reducing the chances of a near-term future recession. There would be some voluntary sellers, to capture the compensation, but the cost of selling and buying a house, and of moving house, is not trivial. If 100000 households were to claim the maximum compensation of $100000 that would be total additional government expenditure of around $1 billion, spread over a considerable period of time. And to claim $100000, you’d have to have bought say a $1 million first house and seen house prices fall 45 per cent from your entry price.

It isn’t a perfect scheme by any means, and lots of details would need to be fleshed out. One could relatively easily restrict it to apply only to those in a first owner-occupied house, again the people who will naturally command the most sympathy anyway. But if something of this sort could be done for, say $1 billion, and it helped the pave the way for a genuine structural fix in the housing market – a willingness to actively embrace lower house prices – it would seem likely to offer more value than, say, the least valuable of the proposed 10 new “roads of national significance”, which are estimated to cost on average just over $1 billion each. How much congestion is there on the existing road from Levin to Sanson?

And three final points on housing:

- it was depressing to read the housing section of Jacinda Ardern’s campaign opening speech. It wasn’t the focus of her speech, but – just like Andrew Little at his conference speech earlier in the year – there was reference to dealing to “speculators”, barring foreign purchasers, and to the state building more houses, but not a word – not even hint – about freeing up the land market in a way that might make those price to income aspirations achievable,

- it was slightly strange listening to Robertson and Joyce debating the possibilities of a capital gains tax, focused on housing. Weirdly Robertson didn’t take the opportunity to rule out applying a CGT to unrealised gains – even though he surely really realises that, whatever the theoretical appeal, there is no way anyone is going apply a CGT to anything other than realisations. But it was even more strange to hear this debate going on after both sides were insisting they “had a plan” to fix housing. If they really did then surely there would be few/no systematic capital gains in the housing market for decades to come?

- and finally, Steven Joyce ran his line that house prices are a global problem. This seemed to be a variant of the sort of “problems of success” line John Key often ran. Out of curiosity, I dug out the OECD’s real house prices series this morning. They don’t have data for quite every country, but here is the change in real house prices from 2007 to 2016 (annual data) for the countries they have the data for. There are a few countries that have done worse, but not many. In the median OECD country, real house prices have fallen over the last decade.

Mostly, the countries that have been about as bad as us have also had quite rapid population growth (Israel, Australia and Luxembourg in the lead on that count) – not, of course, that either Finance spokesperson suggested doing anything about that.

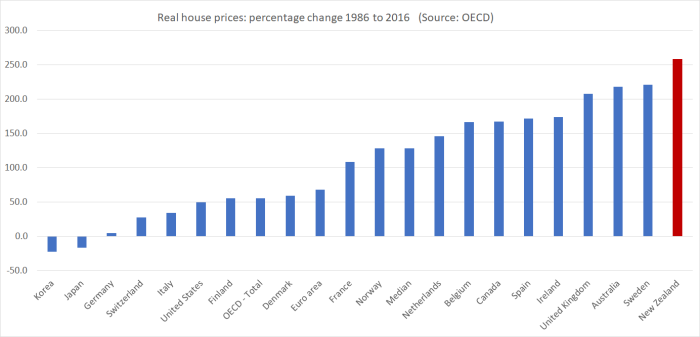

What about a longer-term comparison. There are lots of gaps in the OECD data for earlier decades, but here are real house prices increases for the countries they have data for over the three decades to 2016.

Worst of them all, without even the income growth to match.

We need to face up to the importance of lowering house prices, of adopting policies likely to sustainably make that happen, and – if necessary – consider compensation packages for some to help make that transition possible.