There was a story buried deep in the Dominion-Post this morning that caught my eye. The heading was “Profits up as wages stand still“, and the article was prompted by the release yesterday by Statistics New Zealand of some summary results from the Annual Enterprise Survey.

In their media release yesterday, SNZ – true to their apparent policy of accentuating the positive – was at pains to highlight the increase in profits over the 2015/16 year. Overall, operating profits in the business sector had risen by 8.6 per cent – rather faster than the increase in nominal GDP.

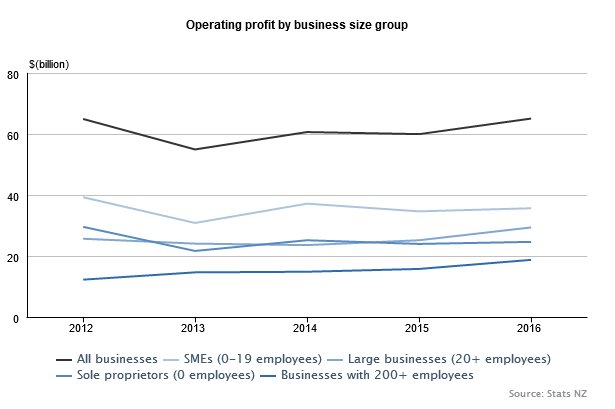

But it was this chart in the SNZ release that caught my eye

Profits had certainly increased quite a bit in 2015/16, but look at that top line. Total profits in 2015/16 were no higher ($bn) than they had been in 2011/12, and yet over that period nominal GDP had increased by just over 17 per cent. On this measure, profits as a share of GDP would have fallen quite a bit over those four years.

In the Dom-Post article, the journalist had juxtaposed the increase in profits over the last year with the very weak increase in wages, at least according to the Quarterly Employment survey. Lobby group representatives were quoted in a fairly predictable way.

Council of Trade Unions economist Bill Rosenberg said the statistics were more evidence that the share of income going to wages and salaries was falling.

“That indicates wages are not keeping up with what the economy’s income could actually afford.”

The share of income going to wages in New Zealand was low internationally, he said. “To see it fall further is very disturbing. It is an indication we are a low-wage economy.”

and

Kirk Hope, chief executive of BusinessNZ, said the increase in company profits meant jobs were more secure.

It was also positive for “the many thousands of New Zealanders”, including Kiwisaver investors, who now owned shares and who would be receiving increased dividends, he said.

“Wage growth is not the only responsibility companies must address.

“A proportion of company profits must be reinvested to safeguard the future existence of the company; without that investment there will be no ability to maintain or grow jobs.”

Business profits can jump around significantly from year to year, but even taking a longer-term view, Statistics NZ figures show they appear to be greatly outstripping pay rises.

And when the journalist did take a long-term perspective, he looked at profit increases since 2009, and compared them to wage increases since then, even though 2009 was the worst of the severe recession, and profits are typically much more cyclically variable than wages.

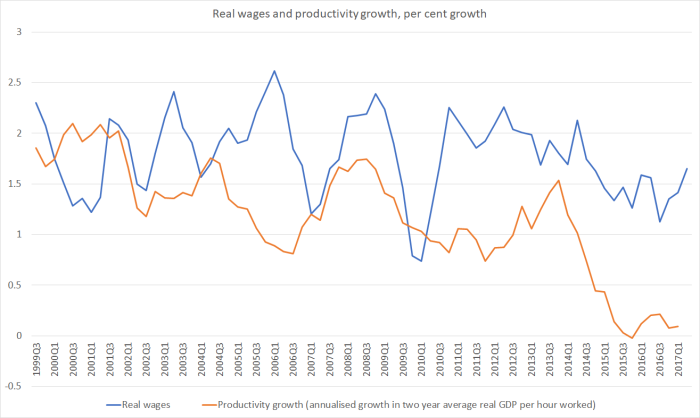

But, as I noted in a post the other day, if one uses the more-stable and better-constructed Labour Cost Index measures, it looks as though real wages in recent years have been materially outstripping the (non-existent) productivity growth. Real wage inflation hasn’t been high in absolute terms, but it has been a lot faster than any gains in productivity.

In the wake of that post, I’d also gone back and dug out from the national accounts the data on the wages and salaries (“compensation of employees”) share of GDP. The data go all the way back to 1972.

Broadly speaking, the national accounts suggest that the labour share of GDP has been increasing for almost 15 years now (the latest data are the year to March 2016). Even from the peak of the last boom (year to March 2008) to now, the labour share of GDP has increased a bit further.

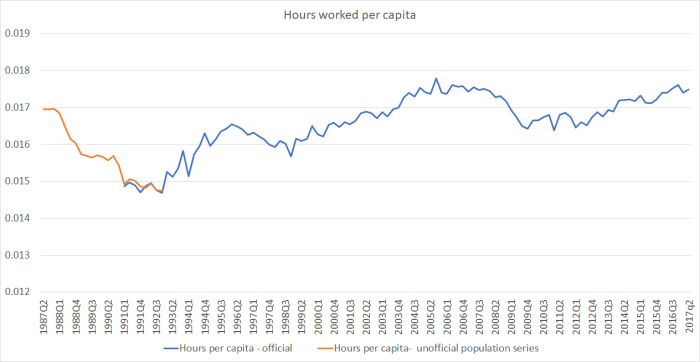

And it isn’t because more people are working more hours. Here is a chart of hours worked per capita.

Total hours worked per capita are still slightly below the previous cyclical peak. To the extent that the labour share of GDP has been increasing, it looks to have been a result of relatively good (relative to productivity) increases in wages.

As for profits, they are (more or less) the inverse of the labour share of income: they’ve been falling over the last 15 years.

Overall economic performance remains dismal, redeemed only by the strength of the terms of trade. But relative to that disappointing performance – weak productivity growth, growth skewed to the non-tradables sector – labour (as a whole) doesn’t seem to have been missing out.