Consistent to the end, the outgoing Governor of the Reserve Bank today both refused to accept that he’d made any mistakes, while refusing any comment at all on some of the more searching questions.

The news conference was on the occasion of the release of his statutory monetary policy accountability document, the Monetary Policy Statement. It was the last opportunity journalists will get to question him. And yet faced with questions about the Toplis affair (his use of public resources, including his senior managers, to attempt to close down critical commentary from an employee of an organisation the Bank regulates), he simply refused to comment. I’m sure he is now feeling quite embattled and defensive, but surely it should be unacceptable for a powerful public official to simply refuse all comment on such a chilling example of abuse of executive office? If he doesn’t think it is an abuse, and thinks somehow people shouldn’t be allowed to aggressively criticise him, he should at least have the decency to say so openly. I hope members of Parliament use their opportunity this afternoon to ask questions on this matter, and to insist on answers.

The Governor also tried to avoid most questions about his term in office (but was happy to provide a long answer to a curious question about risks around North Korea, on which he has (a) no accountability, and (b) no more knowledge than the rest of us). Apparently there is a speech coming – which may be interesting, but it provides no opportunity for follow-up challenge or scrutiny. Asked if his critics have been fair, and if at times their criticism may have clouded his judgement in decisionmaking, he claimed he will cover that in his speech. If so, that should be interesting. Asked also about:

- what surprised him about the economy in the last five years,

- about his inflation record in the last five years, and

- what his successor should worry about

he refused to provide any answers, and simply referred everyone to the forthcoming speech.

One journalist finally voiced a widespread concern and asked if the Governor had been open enough with the media, noting that the Governor appeared not to have given a single live interview in five years. The Governor claimed to have been pretty open, citing the press conferences he holds. He also claimed that his colleagues do interviews, but simply never engaged with the fact that he personally is legally responsible for the exercise of a great deal of power – not just monetary policy, but in regulatory policy areas – and simply doesn’t face up, ever, to anything but soft-ball interviews. A press conference, with 20 other media and where the Governor gets to decide whose questions to take when, is simply very different from a sustained searching interview – whether on Morning Report or one of the TV current affairs shows.

Towards the end of the interview, the Governor seemed to change tack a little. After repeated questions about his stewardship, he came out claiming that things have actually gone pretty well really over the last five years, and that the Reserve Bank deserves credit for that. It was like a performance straight from the National Party advertising unit. Growth had, we were told, averaged 3 per cent and there had been plenty of employment growth. Even house price inflation was somehow claimed as to their credit (I think the fact that it is temporarily low in Auckland). Oh, and core inflation averaging 1.5 per cent – when he had explicitly accepted a task of keeping it around 2 per cent – was also apparently just fine. These results should, apparently, dispel any suggestion that, even with hindsight, monetary policy had on average been too tight.

He did acknowledge in passing that there hadn’t been much productivity growth – which isn’t his fault – but there was no mention at all of the weak per capita GDP growth (by comparison with earlier recoveries), no mention of an unemployment rate that has been above even the Bank’s too-high NAIRU estimate for eight years now, and no mention of a very high labour underutilisation rate. And even on the inflation front, he seemed to want to blame all the problems on the rest of the world: low tradables inflation, as if a persistently high exchange rate had nothing to do with that. He attempted to claim that non-tradables inflation (averaging around 2.2 per cent) had been just fine, when everyone recognises that getting core inflation near 2 per cent would have required non-tradables inflation rather nearer 3 per cent (which shouldn’t really have been hard amid a big building boom). And non-tradables is what the Reserve Bank has the greatest degree of medium-term influence over. If the Bank deserves credit for the last five years – whether for style and communications, or for specific policy – it can only have done so relative to a particularly low benchmark.

Even now, said the Governor, he was quite comfortable with his decisionmaking in 2014 and 2015 – when he unnecessarily raised the OCR by 100 basis points, and then was slow and reluctant to reverse those cuts. I’m not sure what he thinks he gains by never ever conceding any mistakes. He’s human surely. We all make mistakes.

All in all it was a pretty disappointing, if not overly surprising, performance. Whoever takes up the job of Governor next year will surely face a huge challenge, in shifting the organisational culture – which must have been infected by Wheeler’s approach – and lifting performance.

And all that was before even getting to the content of this Monetary Policy Statement.

There was the odd good thing I noticed. LUCI, the ill-fated Labour Utilisation Composite Index – sold for a year or so as a measure of absolute tightness in the labour market, before they finally realised that it was mainly an indicator of changes in that tightness (a difference that matters quite a lot) – seems to have quietly exited the stage.

But there were various more troubling points:

- they were at pains to note that their estimate of the neutral OCR has carried on falling. But, as in the chief economist’s speech a couple of weeks ago, there was no attempt to translate that into estimates of how neutral mortgage rates, or neutral deposit rates have changed. As I noted then, widening spreads between the retail interest rates and the OCR suggest that if we take the Bank’s neutral OCR estimates seriously, their implicit estimates of neutral retail rates have been rising. That seems seriously implausible. It matters because the Bank keeps talking – and forecasting – on the basis that monetary policy is highly stimulatory. It almost certainly isn’t.

- and although they did note that mortgage interest rates are higher than they were last year, there was no attempt anywhere in the document to explain why the Bank considers that monetary conditions need to be tighter now than they were last year (especially as growth and core inflation have been surprising on the low side).

- it was quite surprising how upbeat they appeared to be on the global economy. In fact, their upside scenario is one in which global inflation picks up quite a bit. That migth have seemed a plausible possibility a few months ago, but with US inflation ebbing and no real signs of any increase in core inflation anywhere else, it looks (frankly) a little desperate. Perhaps it is a reflection of the Governor’s continued conviction that global monetary policy is highly accommodative/stimulatory? Were it actually so, one might have expected an increase in inflation before now.

- the Bank seems focused on the idea that the labour market is almost at capacity. Their projections have the unemployment rate levelling out at 4.5 per cent, suggesting that is their estimate of the NAIRU. Between demographic factors on the one hand, and wage inflation outcomes on the other, that seems unlikely.

But perhaps my biggest puzzle is where all the forecast growth is coming from.

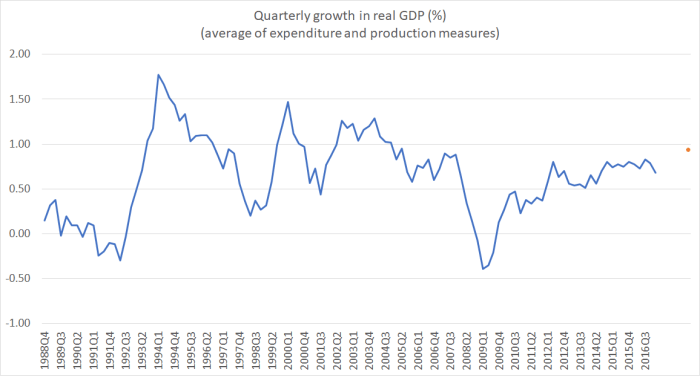

Over the next six quarters, the Bank projects that quarterly GDP growth will average just over 0.9 per cent. This chart shows six-quarter moving average of GDP growth (in turn, averaging the production and expenditure measures).

The orange dot shows the forecast for the next six quarters. Their projections suggest that the economy will grow more rapidly over the next 18 months than it has managed on a sustained basis at any time in the current recovery. You might not think that the difference looks large, but:

- the Bank already recognises that monetary conditions are tighter than they were last year,

- the Bank is forecasting a substantial reduction in the net migration inflow, and no one seriously doubts that unexpectedly rapid population growth has been the biggest single driver of headline GDP growth in recent years. However much immigration adds to supply, it adds a lot to demand.

So why are we to expect a sustained growth acceleration from here? Although it isn’t stated in the document, I hear that the Bank is invoking the expected fiscal stimulus (from promised measures announced in the Budget). In isolation that might make some sense, but against the projected halving in the net migration inflow and the actual tightening in monetary conditions, it doesn’t really ring true. If anything, the risk now has to be that over the next 18 months, headline GDP growth averages lower than we’ve seen in the last couple of years.

In many respects, the MPS is just another production in the long line of Reserve Bank documents that hold out the promise of higher medium-term inflation, but with little reason to expect it to happen. But I was interested in one line in the policy section of the document. Often the Bank sounds quite complacent about non-tradables inflation, suggesting that everything is under control. But this time they explicitly note that “a strong lift in non-tradables inflation is necessary for inflation to settle near the target midpoint in the medium-term”. That, for central-bank-speak, is a pretty strong statement. It might seem to argue for a more aggressive easing.

But they seem torn. On the one hand, they go on to note that even “higher levels of growth may not be accompanied by significant increases in inflationary pressure”. On the other, there is another strong statement about wage inflation: “increasing capacity pressure is likely to support wage growth in the near term“. I guess that is quite a benchmark they’ve set for themselves – and quite a surprising one after all these years of one-sided forecast errors. If it doesn’t happen, and there seems little obvious reason why it should start now, I hope the Governor’s successors will be revisiting the stance of policy.

You might be wondering, so why not just cut the OCR and “give growth a chance”? The Governor’s response to that is

an easing of policy, seeking to achieve a faster increase in inflation, would risk generating unnecessary volatility in the economy

I’m not quite sure what standards he is judging “unnecessary” by here? It isn’t as if growth has ever been particularly rapid in this recovery (see chart above). It isn’t as if unemployment has ever dropped, even temporarily, below the NAIRU. It isn’t as if inflation has been surprising on the upside. It isn’t as if productivity has been rocketing away. It is as if the Bank is simply allergic to taking any steps that might possibly run a risk of (core) inflation going over 2 per cent, after all these years below. In practice, it looks a lot like 2 per cent inflation represents a practical ceiling, rather than a target midpoint.

The Governor concluded his press release claiming that “monetary policy will remain accommodative for a considerable period”. Fortunately, he will have no say in that matter. Unfortunately, since we know neither who will be making the decisions, or what PTA they will be working towards – recall that Labour, with the support of eminent economists like Lars Svensson, favour adding an explicit unemployment objective (to help make clear why we have active monetary policy in the first place) – there isn’t really much information in that statement at all. Much of the uncertainty is inevitable – no one knows the future – but quite a bit would be avoidable if we had a better statutory mechanism for Reserve Bank decisionmaking.

The search for the new Governor presumably goes on (the Reserve Bank Board would, on normal schedule be meeting next week). Should the Opposition parties win power, I hope that one of their first actions (because time is pressing) will be a quick amendment to the Reserve Bank Act, to give the Minister of Finance the power almost all his overseas peers have, to appoint directly as Governor someone with whom he is comfortable, not someone the outgoing government’s Board delivers up to him. In fact, it would be a sensible change whichever group of parties forms the next government.