So far this year, there has been only a single on-the-record speech from the Reserve Bank Governor, and none at all [UPDATE: actually one] from his Deputy Chief Executive (and incoming – although unlawful – acting Governor) Grant Spencer. But there have been quite a few speeches from the next tier or two down – in some cases probably as part of Wheeler-backed bids for the governorship. Geoff Bascand – currently, in effect, chief operating officer – is probably the only really serious internal contender, and I still intend a post on the speech he gave last week on matters – New Zealand’s external indebtedness – well outside the range of his day job.

But yesterday there was another speech from Assistant Governor and Head of Economics, John McDermott, delivered to an Auckland corporate/fx audience. The speech was put out under the rather groan-inducing heading Looking at the Stars. In formal economic models, the equilibrium values of variables are often denoted with an *. Thus, r* – or “r star” – is the equilibrium, or neutral, interest rate. McDermott’s speech was an attempt to explain how the Bank uses some of these equilibrium variables (“the” output gap, “the” neutral interest rate, and “the” equilibrium exchange rate) in setting monetary policy.

I had various picky concerns about the speech, but I won’t bore you with those.

The speech was pretty consistent with the sort of speeches McDermott has given over the years. In his role, he is (among other things) the Governor’s chief adviser on the New Zealand economy and monetary policy. He’s had the job for 10 years now, and yet there is still a pervasive tone of the textbook about his speeches. Models – disciplined ways of thinking through issues – have a role to play, probably in all areas of policy. But in his speeches McDermott never seems to have found a way of successfully conveying a nuanced understanding of the economy and policy issues, in a way that doesn’t leave too much of the formal architecture on display. It is quite a contrast to successful senior policymakers in central banks in other countries.

At times, it is as if he doesn’t feel comfortable without the formal apparatus, even when he knows the rather severe limitations of those tools and techniques. Here is an example of what I mean. In the conclusion to his speech, McDermott states that

To set monetary policy we need to know [emphasis added] where the key macroeconomic factors (such as interest rates, output, and the exchange rate) are tracking relative to their equilibrium levels, denoted by our ‘stars’. These stars are unobservable and complex to estimate, so we use a range of techniques to help form our view of their values over time. Like the night sky, our stars keep moving.

Earlier in his speech he had noted that these equilibrium values “are the anchors around which we aim to stabilise the economy”.

Such in a world – in which the Reserve Bank, and others, knew where these equilibrium levels are, and how they are changing – might well be great. (Although even then a single instrument – the OCR – just can’t manage three other variables, in addition to inflation.) But it isn’t the world we live in.

In fact, McDermott more or less acknowledges that. Take the output gap – the difference between actual GDP and estimates of potential GDP – as an example. There have been huge revisions to the Bank’s estimates of the output gap over time (I’ve illustrated this previously, but it isn’t contentious – everyone recognises the point), and McDermott himself states in the speech that “we have a range of uncertainty with respect to the output gap; around 2 per cent of potential output.”. In a series which the Bank estimates has only flucuated in a range of -3 to +3 in the last 25 years or so, those margins of error are large enough that only rarely can the Bank even be confident which sign the output gap has. If knowing potential output and the output gap is as essential to monetary policy making as McDermott claims in this speech, we might as well give up completely. They don’t know, and neither does anyone else with any great confidence.

The conceptual framework might well be useful – you are more likely to need to tighten if the economy is running above capacity – but real-time empirical representations of this sort often aren’t very much use at all. In fact, one of the more obvious gaps in the speech is there are no observations, or charts, illustrating how the Bank’s view of these equilibrium values goes on changing. It isn’t so much that 2017’s neutral interest rate might be different from 2007’s, but that the 2017 estimates of the 2007 neutral interest rate may be very different to what the Bank thought the 2007 neutral rate was when it was making policy in 2007. For some research purposes – making sense of economic history etc- that doesn’t matter, in fact it is how knowledge advances. But actual policymakers have to operate in the knowledge that they are highly likely to be wrong in their contemporaneous estimates of these equilibrium relationships. And there is simply nothing of that in this speech.

If the errors was just randomly distributed it might matter less. But some of them are rather more systematic. Neutral interest rates are a good example. Most people now accept that neutral interest rates are lower than they were, but most – including most policymakers – have been slow to adjust those estimates. That is a natural human tendency, but it also means that any policymaker who puts a great deal of weight on their current estimates of neutral interest rates will think any particular level of market interest rates is further from the “true” neutral rate than will actually turn out to have been the case. Monetary policy will then have been run too tight. One could mount a reasonable argument that that is a material part of the story of what has gone on at our Reserve Bank. Recall that the Governor keeps asserting that monetary conditions are extremely stimulatory – suggesting he has in mind quite a strong view about what “the” neutral interest rate is. Recall too McDermott’s comment that the Bank seeks to use these equilibrium relationships as “anchors around which we aim to stabilise the economy”. There has been a strong sense over the years of the Reserve Bank constantly wanting to get the OCR back much closer to its estimate of the neutral rate.

Actual policymaking isn’t always that bad. How could it be when on the one hand they think the economy is running at full capacity (one equilibrium concept they tell us they rely on), while the OCR is a whole 175 basis points below neutral (the other main equilibrium concept they tell us they rely on knowing). But it hasn’t been very good either. And the policy communications – examples like this speech – are pretty consistently poor.

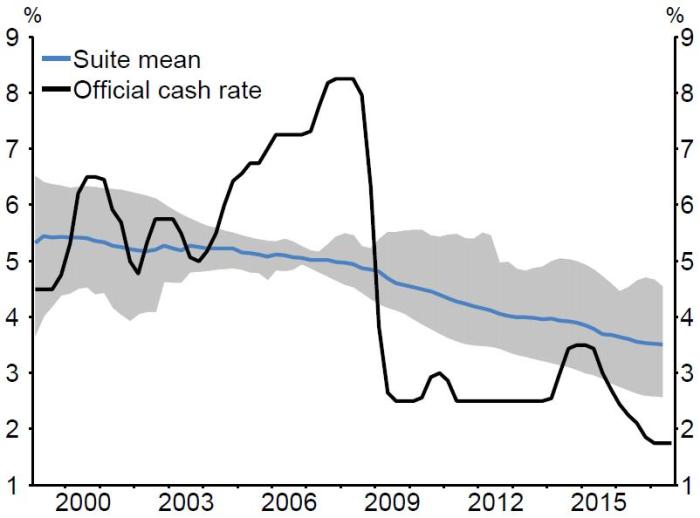

Sometimes I even worry about basic levels of apparent competence. McDermott includes this chart in his speech

Figure 1: Nominal Neutral OCR and Actual OCR

Source: RBNZ estimates

This is their current estimate of how the neutral OCR has tracked over the history of the series (the OCR was only introduced in 1999). They have a suite of tools and models that produce a range of estimates – the grey band – and the blue line is the mean of those estimates. In the text, McDermott says the Bank is now using 3.5 per cent as the neutral OCR in their modelling and forecasting, which is about where the blue line is at present.

There is some economic discussion around the chart

Over time, the neutral interest rate has been slowly falling; a trend that has been seen in many countries around the world. Economic theory tells us that changes in neutral real interest rates reflect changes in real economic factors such as population growth, productivity growth, preferences for savings, and world conditions. A combination of these factors appears to have been contributing to the fall in neutral, both in New Zealand and abroad.

Which all sounds fine, and sounds consistent. But then you remember that the neutral interest rate the Reserve Bank is using is the OCR, and the OCR is an interest rate that isn’t paid by any borrower, or received by any saver, in the wider economy. For those one has to look at data on, say, term deposit rates or floating mortgage rates.

Start with the chart above. The Bank says its estimate of the neutral OCR is now 3.5 per cent. But go back a decade – July 2007 was just before the financial crisis stresses really started to infest funding markets globally – and the blue line looks as though it would be almost bang on 5 per cent. If I recall rightly, at the time we thought the neutral OCR was much higher than that – perhaps as high as 6.5 per cent – but as things stand now the Reserve Bank is telling us it thinks the neutral OCR has fallen by 1.5 percentage points over the last decade.

That might sound like a lot. In fact, it is nothing at all. Here’s why. In July 2007, the OCR was 8.25 per cent. At the same time, the Reserve Bank’s measure of six month term deposit rates was 7.98 per cent, and the Bank’s measure of new floating first mortgage rates was 10.35 per cent. Term deposit rates were 27 basis points below the OCR, and first mortgage rates were 210 basis points above the OCR.

Right now, the OCR is 1.75 per cent and has been all year. Last month (latest data), the term deposit rate indicator was 3.31 per cent (156 basis points above the OCR) and the indicative new first mortgage rate was 5.84 per cent (409 basis points above the OCR).

In other words, the margins between the rates people are actually paying/receiving and the OCR have blown out enormously – in fact by around 190 basis points. Implicitly, the Reserve Bank has revised upwards its estimates of neutral retail interest rates.

Those spreads between the OCR and retail rates can and do move around, so I’m not suggesting you focus on the difference between the 150 point cut in the neutral OCR, and the 190 point increase in spreads between the OCR and retail rates. The real point is that, despite the fine words in the chief economist’s speech about reasons why neutral interest rates here and abroad have probably fallen – perhaps quite considerably – the Reserve Bank has made practically no adjustment of substance at all. As they’ve always said, it is retail interest rates – not the OCR – that affects spending and investment choices.

I can’t believe McDermott doesn’t know all this – we used to have charts presented with each set of forecasts illustrating how the spreads had changed since before the crisis – but if that is right, what is the explanation for how the speech is written? And is this the sort of presentation that has the Governor still asserting that monetary policy is highly stimulatory, even as inflation continues to track “broadly sideways”?

In a way, these things shouldn’t matter. A prudent central bank would simply treat current interest rates as a starting point, and look for actual data – new developments – suggesting a case for change. But at our central bank it does seem to matter to some extent, because we have key policymakers out asserting that they “know” what the equlibrium values are, and can/should use them to make monetary policy. What say instead the Reserve Bank had assumed a 150 basis point fall in neutral mortgage rate? That would translate to a neutral OCR of around 2 per cent at present. It seems at least as plausible as the Bank’s own number – with inflation persistently below target, an output gap they think is near zero, and unemployment persistently above the NAIRU. Then presumably we would be hearing quite different rhetoric from the Governor about just how stimulatory, or otherwise, monetary policy is.

Changing tack, the other thing that is striking about the speech is the reminder of just how little focus the Reserve Bank puts on the labour market. Labour is by far the biggest input to the economy, and also the market in which the rigidities and slow price adjustments – a key concern for monetary policy – are most prevalent. And yet it hardly rates a mention in McDermott’s speech. Many other central banks – and forecasters – find the concept of the NAIRU (the non-accelerating inflation rate of unemployment), and the gap between actual unemployment and the NAIRU, as a useful (even central) part of their forecasting and analysis framework. That is partly because the unemployment itself is a directly observed and, in principle, is a direct measure of excess capacity (more so, certainly, than the output gap). But it is also because policy is supposed to be about people, and ability of people to get a job when they want a job is one of the key markers of a successfully functioning economy. We have active discretionary monetary policy because the judgement has been made that without it the inevitable shocks that hit the economy would leave countries too prone to prolonged periods of unnecessary unemployment (Greece is the extreme contemporaneous example). Voters don’t greatly care about unemployed machines, but they do care about unemployed people.

Contrast the Reserve Bank of New Zealand’s approach to that of the Reserve Bank of Australia – with a very similar inflation target. Yesterday, the RBA Governor was out with a thoughtful nuanced speech on labour market issues, in which he observed that “the unemployment rate is still around 1/2 a percentage point above estimates of full employment in Australia”. He referenced a clear and useful recent Bulletin article on “Estimating the NAIRU and the unemployment gap” which opens with this clear and simple statement

Labour underutilisation is an important consideration for monetary policy. Spare capacity in the labour market affects wage growth and thus inflation (Graph 1). Reducing it is also an end in itself, given the Bank’s legislated mandate to pursue full employment. The NAIRU – or non-accelerating inflation rate of unemployment – is a benchmark for assessing the degree of spare capacity and inflationary pressures in the labour market. When the observed unemployment rate is below the NAIRU, conditions in the labour market are tight and there will be upward pressure on wage growth and inflation. When the observed unemployment rate is above the NAIRU, there is spare capacity in the labour market and downward pressure on wage growth and inflation. The difference between the unemployment rate and the NAIRU – or the ‘unemployment gap’ – is therefore an important input into the forecasts for wage growth and inflation.

You’ll see nothing of the sort from the Reserve Bank of New Zealand. It is as if they fear that somehow talking about ordinary people, and the overall balance in the labour market, will somehow be betraying their mission. But their mission is about people’s lives, jobs, and opportunitites.

I’m not suggesting that at present the RBA is running policy any better than the RBNZ is – in both countries there looks to me a case for thinking about possible further rate cuts – but the RBA certainly communicates much better, and in a way that suggests both a grounded story about what is happening in Australia and the world, and an identification with the interests of ordinary Australians.

That is part of the reason why, somewhat reluctantly, I’ve come to the view that the Labour Party is right to campaign on amending the Reserve Bank Act to add a focus on unemployment to the goals of monetary policy. It should be implicit in the current way the Act is currently written, but in practice it seems to have become something the Bank is uncomfortable with, rather than something central to their reason for being. Phil Lowe and Janet Yellen – or their respective decisionmaking boards – aren’t some rampant wet inflationistas, and yet they manage to talk openly and sensibly about these issues, and find it a useful framework for analysis and communication, in a way that seems beyond our Reserve Bank. We’ve got to the point where far-reaching is needed at the Bank – in its legislation, its ethos, and in its senior people.

I’ve always been a bit hesitant about suggestions that the Reserve Bank operates primarily in the interests of one group of New Zealanders over another – that hesitancy shouldn’t be surprise; after all, I sat round the monetary policy decisionmaking table for a couple of decades and we all want to believe that we serve the public interest. But, with the benefit of a bit more detachment, I increasingly worry that the Bank – unconsciously rather than deliberately – reflects more the perspectives and interests of what the Australians talk of as “the big end of town”, than of ordinary New Zealanders.

There are just a couple of illustration of what bothers me. After each MPS the Reserve Bank runs (or at least did when I was there) a series of presentations around the country to explain its thinking. In some ways they worked quite well – we spread out across the country (usually the three main centres plus one provincial centre a quarter) the morning after the MPS. I enjoyed participating. But all these functions were hosted by the banks, and the invited attendees were the banks’ business, corporate and financial customers – in smaller provincial areas, they were often hosted in a bank’s business customer lounge. Never once did we do those talks to union-organised gatherings of interested employees, to church or community groups, to students, to meetings of beneficiaries or the like. Don’t get me wrong – the Bank does, or did, accept some invitations in the course of the year to talk to other groups, but the big events are about corporate audiences.

It struck me again yesterday when I picked up John McDermott’s speech. It was delivered to HiFX (presumably staff and invited clients), a “a UK-based foreign exchange broker and payments provider that has been owned by Euronet Worldwide since 2014”. Out of interest, I looked back through the other on-the-record speeches McDermott has done during Graeme Wheeler’s term of office. They were to audiences at:

- Federated Farmers

- FINSIA (a financial sector training group)

- NZICA CFOs and Financial Controllers

- Goldman Sachs Australia

- Macroeconomic Policy Meetings, Melbourne

- Bay of Plenty Employers and Manufacturers

- Wellington Chamber of Commerce

- Waikato Chamber of Commerce/Institute of Directors

Each a perfectly worthy audience in its own right no doubt. But there is something of a pattern – it is an employers and financial sector focus, rather than (m)any groups broadly representative of the citizenry. When the people you talk to are mostly rather comfortable, it must to an extent influence the way in which you as an organisation end up thinking. Few if any of those audiences would be much bothered if the unemployment rate had been above the NAIRU for, say, eight years and counting.

McDermott told us about how he was looking at “the stars”. In fact he knows almost nothing particularly useful about them – and if there is a criticism it isn’t that he doesn’t know the unknowable, but that he keeps asserting against all the evidence that he can. Perhaps he and his colleagues would be better off keeping a cold hard eye on the ground, on the things we know rather better – a (core) inflation rate still well below target, wage inflation still very subdued, and an unemployment rate still persistently high. And talk to us in language that suggests a care about the interests of ordinary New Zealanders.

Here is a hypothetical for you

Assume you are willing to apply for the upcoming job of governor

What sort of TPA handcuffed manacled agreement would you accept

Frankly, if the NZ government were to look overseas to fill the job, there is a huge risk no-one would apply for the job

LikeLike

They shouldn’t look overseas – at least other than NZers abroad – for a job that wields so much, largely untrammelled, power at present.

If it were me, and the Act wasn’t changed, I would leave the PTA largely as it is, but replace wording about avoiding unnecessary variability in the exch rate, int rates, and output, with something along the lines of “promoting the maintenance of full employment, as far as that is consistent with keep medium-term inflation near target”

In many respects, the PTA is the least of the problems. Individuals and culture matter more, but there is a place for legislative change (both governance and goal) to reinforce the prospects of sustained change.

LikeLike

Actually, Michael, you’re wrong about Grant Spencer – he gave a public speech in March on the review of bank capital requirements:

http://www.rbnz.govt.nz/news/2017/03/reserve-bank-outlines-plans-for-bank-capital-review

LikeLike

Oops. Thanks for pointing that out. now corrected in the post.

LikeLike

The problem is that the real N.Z. economy will not bend to fit the Reserve Banks model of it. The Bank needs to get the real world to change then all will be well with them. They will have a perfect model and be able to make perfect predictions on interest rates, growth, inflation etc.

LikeLike

…sorry being thick no doubt (!!) but just to clarify: the 190bps spread change? [calc: 2007 (210- -27 = 237) and now (409-156 = 253)]

LikeLike

Mortgage rate- OCR: 2007 210bps , 2017 409bps so change in spread +199bps

TD – OCR: 2007 -27bps 2017 +156 bps so change in spread +183 bps

Probably should have included a nice table in the post to have made things clearer.

LikeLike

…ah got it, cheers; just thinking out loud, the fall in the ‘absolute level’ of retail mortgage interest rate is likely to have had a positive impact on households that stayed in work and repriced mortgage debt (think the BOE calls this the “cash flow” channel); take the point on the spread but the overall servicing cost has fallen materially post crisis? further, it would be difficult for the RBNZ to somehow influence credit/risk premiums unless the latter are being set in markets at levels that indicates system stress? (think I might be confusing your point…)

LikeLike

Again, i probably wasn’t clear enough – I had to dash out to something else and rushed the post.

I’m not suggesting that RB can influence credit/risk/liquidity premia at all, just that the setting of the OCR (and the neutral OCR) are influenced by developments in those variables. If global funding spreads rise 100 bps, the RB can – and typically will – offset that effect by lowering the OCR to something like the same extent.

It is also important to distinguish the cycle from the trend. The RB thinks (no doubt correctly) that the economy was overheating in 2007. They wanted interest rates (retail rates, facing actual borrowers/savers) above neutral. At present, they think the output gap is around zero, so sensibly interest rates will be rather lower relative to whatever neutral now is. My point is really that if we suddenly had a surge in demand and a big positive output gap, and the RB again wanted the OCR 325bps above neutral – as they think it was in mid 2007 – that would result in retail rates now higher than the retail rates we had in 2007. That is because they haven’t pulled down the neutral OCR enough to offset the increase in those funding spreads (TD and mortgage less OCR).

Clearer?

(it may well be that the RB is still assuming the wider funding spreads are temporary, and forecasting them to run off over time, but even if so that is unlikely to show up in their suite of models that generate the grey band in the chart above)

LikeLike

NZ household lending and household savings more or less equate which means that higher or lower interest rates do not affect spending behaviour generally. Higher interest rates do affect the farming sector with its $60 billion debt and does affect commercial lending. Therefore the overheating in 2007 could never have been contained by higher interest rates other than by damaging business and the productive sector and causing massive job losses which pretty much lead to the decimation of NZ industry and productive capability which is not exactly how any other Central bank intends to slow down a overheated market nor intended by parliament when those powers of invention was given to the RBNZ central bank governor..

LikeLike

….yup, I think so; two cents: often thought the “credit crisis” was as much about the misallocation of the quantity of credit as it was about the mispricing of risk premiums (on bank loans; IG/HY spreads etc.); makes me think future demand can only materially run ahead of potential supply if the quantity and pricing of credit is once again ‘wrong’; but in the current market discipline / bail in world, shouldn’t demand be contained via risk premiums first rather than via official cash rates?; that some think there is a natural level for the OCR seems somewhat unnatural given marginal risk taking (and the pricing thereof) drives incremental economic activity.

LikeLike

? Surely the RBNZ can estimate the neutral interest rate (NIR) at any point of time by looking at real data, i.e the yield curve. The NIR would leave the short end of the curve near flat, say out to maybe 2 years & might take a few iterations of their models to account for feedback, i.e change the OCR to the NIR & then interest rates along the curve will also move.

Also re the NAIRU – given we as a society choose to target price stability rather than full employment, isnt there then a sound argument that the unemployed should be paid the minimum wage? (maybe they are already as the benefit is enough to get by on, maybe?)

Has me thinking that everyone should get the universal basic income and then the actual minimum wage could be set to zero, No one would take a $0 wage (transport & time costs to get to and from work etc) so a natural gap would open up between the UBI and market minimum wage.

LikeLike

A neutral interest rate needs to account for where our interest rates is positioned in relation with our major trading partners. Currently it is positioned too high which flows onto a higher NZD which affects our global competitiveness and encourages too much importation of goods decimating our local manufacturing industries.

LikeLike

i largely agree with you, but this concept of neutral isn’t about where one thinks ideally it should be, but where the data tell you it is – the rate consistent with keeping inflation around target.

LikeLike

What it probably can get from the yield curve is the market expectation of the average actual rate over a long horizon (eg take our longest indexed bonds, add the inflation target and you’d get something like 4.5% as a normal expected govt bond rate). that is a bit different from what the RB is trying to do. but I’m sure yield curve data is one component in their suite of models.

I’m deeply deeply opposed to a UBI for working age people (while having no particular problem with one for say over 70s). I’ve been tempted at various times to do a post on the issue, but haven’t yet gotten round to it.

The natural rate of employment (not quite the same as the NAIRU – that RBA article has a good discussion) is itself a product of things like benefit systems, labour market regulation, min wage laws, demographics etc. With no welfare at all – something I’m not of course suggesting – the natural rate would be quite a bit lower, as the unemployed would become more desperate more quickly (US studies show much more aggressive and successful search as people appraoch the end of their unemployment benefit entitlements).

LikeLike

Michael

Since the 1980’s NZ management of monetary/credit conditions has gone from a regime of direct controls (reserve asset ratios, restrictions on bank deposit rates, controls on mortgage and other lending rates, etc) though various interest rate and signaling mechanisms, to the current model which is actually close to what existed before the 1984 deregulation.

In this context; that the relationship between OCR and bank rates have changed markedly since 2008 can be no surprise. The relationship between wholesale and retail rates have also flipped thanks to the RB’s imposition of funding ratios.

What I found interesting in your report of the speech is that RBNZ doesn’t appear to have developed a comprehensive view of the various tools it now has at its disposal. Its very clear that having an OCR that is consistent with highly accommodating monetary policy is irrelevant if the various other monetary/credit control tools are restrictive.

The Soviet approach of low prices and queues now seems to pertain for credit in NZ.

Perhaps this model is better, although that will depend on how you define “better”, but my question is whether you think RBNZ has a full appreciation of the effect of the wide ranging bag of tools it now uses to control credit?

Tim

LikeLike

Short answer: no. Having said that, on the mon pol side it isn’t the prime cause of their problems.

(Abbreviated response as I’m trying to finish a speech text which will touch on some of these issues, and which i’ll post later in the week)

LikeLike

[…] disagreeing with him, especially openly (some of my other concerns were outlined in this earlier post on one of his 2017 speeches). There is often a testiness about his reactions – combined […]

LikeLike

[…] not typically been a fan of McDermott’s speeches (eg here) but this one reads quite well, It is mostly a background account of how inflation targeting […]

LikeLike