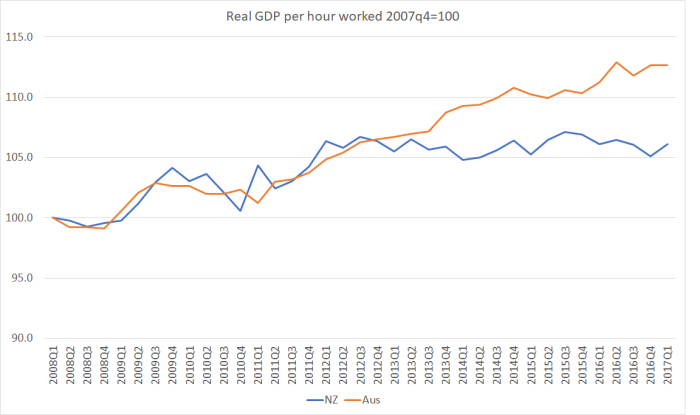

I’ve shown previously various iterations of this chart, real GDP per hour worked for New Zealand and Australia.

It isn’t exactly an encouraging picture for New Zealand. Then again, it is also a bit surprising. For all of New Zealand’s underperformance over the decades, we haven’t usually diverged that badly from Australia over such a short period (the last four years or so).

That chart is for the whole of each economy, and just uses a crude measure of total hours worked. The ABS and SNZ also produce annual data – with quite a lag – in which they look only at the more readily measureable market sector of the economy (from memory around 85 per cent of the economy) and also attempt to adjust for changing labour quality over time (eg improvements in education and thus, in principle, human capital).

Here is that chart for labour productivity, indexed to 1000 in 1997/98, the first year for which the data are available for both countries.

The picture is much the same – a new large gap has opened, in Australia’s favour, in the last few years.

Presumably part of those measured productivity gains in Australia reflects the massive private sector investment boom in the minerals and energy sectors that peaked back in 2011/12.

But out of curiosity I wondered how Australia had done recently relative to other advanced economies. Using annual data from the OECD, percentage total growth in real GDP per hour worked over the five years 2011 to 2016 had been as follows:

Australia 5.3%

OECD Total 6.3% (and OECD median country, 5.7%)

G7 5.5%

EU 4.3%

Even the euro-area as a whole (2.5 per cent) just beat out New Zealand (2.3 per cent). In that light, Australia’s relatively strong productivity performance didn’t look so anomalous at all.

Over that five year period, these are the OECD countries that managed more than 10 per cent productivity growth: Estonia, Hungary, Korea, Latvia, Poland, Slovakia, and Turkey. In fact every single one of the emerging OECD countries (the former eastern bloc countries and Korea) – all with lower initial levels of productivity than New Zealand – managed stronger productivity growth than New Zealand did. All but Slovenia had faster productivity growth than Australia. That is what convergence – supposedly the goal for New Zealand – is supposed to look like.

Of course, several of these emerging countries had had a much worse experience – even on productivity, which often isn’t very cyclical – than New Zealand over the crisis/recession period around 2008/09. But even if one looks at, say, the last decade as a whole, they are mostly catching up (often quite rapidly) and we are not. In fact, relative to Australia – typical closest comparator, and the place where so much of the New Zealand diaspora dwells – we are getting further behind.

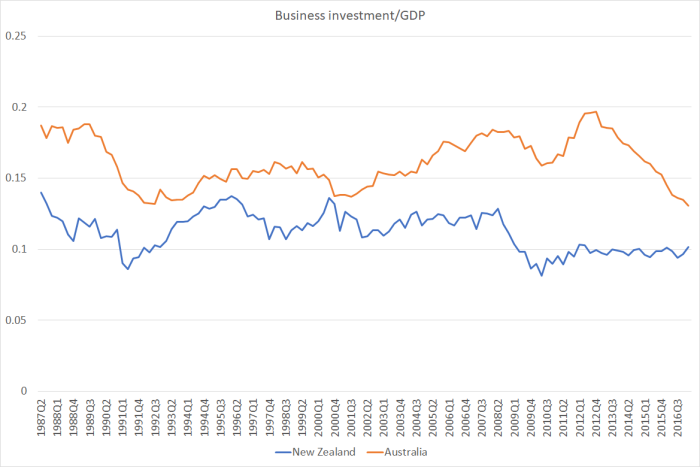

I ran a chart a few weeks ago about how low investment has been in New Zealand. As I noted of business investment it “is now smaller as a share of GDP than in every single quarter from 1992 to 2008. And this even though our population growth rate has accelerated strongly, to the fastest rate experienced since the early 1970s.”

Of course, an important story out of Australia is how business investment has fallen back since the peak of the mining investment boom. Here is the business investment proxy (total investment less general government investment less residential investment) for the two countries.

Business investment in Australia, as a share of GDP, has fallen very dramatically over the last few years. But it was a very big boom – we had nothing of the sort in New Zealand. And even at current levels, Australia’s busines investment still materially exceeds the share of GDP devoted to business investment in New Zealand. In fact, the gap between the two lines isn’t that dissimilar to the typical gaps that prevailed before the mining investment boom got underway in the mid 2000s.

Then again, over the last 25 years Australia’s population growth has averaged a little faster than New Zealand’s. All else equal, faster population would generally require a larger share of current GDP to be devoted to business investment just to maintain the average quantity of capital per worker.

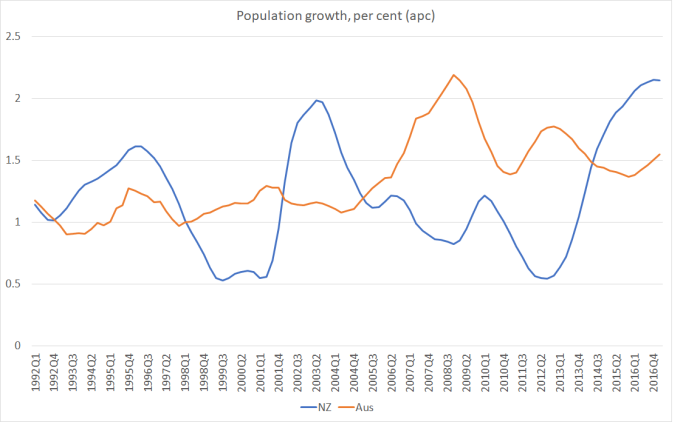

But here is the chart of the two countries’ population growth rates

Australia’s current population growth rate (1.5 per cent) isn’t much above the 25 year average (1.3 per cent). In New Zealand, the average population growth rate over the last 25 years has been 1.2 per cent, but in the last 12 months the population has increased by 2.1 per cent. We have lots (and lots) more people, but firms presumably have not been finding it profitable to increase investment (on average across the whole economy), in ways that might suggest some possibility of the sort of productivity growth that might finally allow New Zealand to join the club of fast-growing countries, catching up to the wealthier countries in the OECD.

Not that our politicians give any sense of being worried. An ill-governed place like Turkey – not richer or more productive than New Zealand in our entire modern history – might shortly go past us. Countries that labour under communist regimes thirty years ago might go past us. But none of our leaders seems to care. None of our parties has a platform that suggests they care, let alone offering a programme that might make a real difference.

One way of describing it is to say when you are targeting the global market, a high level of investment makes sense, but if you are targeting the cosy domestic market, opportunities soon become saturated. So we see firms in Australia and NZ now returning money to shareholders. One wonders about the impact on national saving.

LikeLiked by 1 person

Maybe the sort of tax changes Gareth Morgan is advocating would encourage more productive investment, and Act’s lowering of the company tax rate and top marginal rate for individuals. The rest of them have policies that would make things worse.

LikeLike

Yes, lower taxes on business activity are well overdue. I’m more sceptical about Gareth’s proposal – altho at least he recognises a problem. I covered his tax scheme here https://croakingcassandra.com/2016/12/16/gareth-morgans-tax-policy/

apart from anything else, most people reckon we have too few houses (for the number of people) not too many.

LikeLike

House numbers would appear to be changing quite quickly. Property Managers I interact with tell me they have properties to rent and no big queues . Of course they have a list of people that need to live under a hedge for a while till they learn to be respectful of the houses they rent.

New house prices are under pressure as well here in the Bay.

I suspect we will be seeing the usual crash in the building market before too long. Same old same old gold rush. Think we will see some property developers in strife.

LikeLike

Did you ever do that post on capital taxes vs company tax? Because I think the distinction is important and yet hardly ever discussed.

LikeLike

no, I haven’t yet. Agree it is important.

(sadly of course the political debate if anything is favouring more company tax – at least from foreign companies – and (at least) no reduction in capital income tax)

LikeLike

The deceptive use of large-numbers

“Presumably part of those measured productivity gains in Australia reflects the massive private sector investment boom in the minerals and energy sectors that peaked back in 2011/12”

At a granular level

For the period 2000 thru 2011 the minerals boom was largely the establishment phase with massive amounts of off-shore capital being poured in by the 3 foreign majors RIO,BHP,XTA, then in 2011 at the conclusion of the establishment phase, turned into the extractive phase using all the introduced modern technology toys of remote driven driverless dump-trucks and driverless kilometre long trains which on a Total Factor Productivity basis should be accretive

The main employers of operational mining staff were operational mines whereas the mines that were in the establishment phase were employing largely engineers and mineralogists and pilots, ie mainly professionals and not many shovel-hands

LikeLike

The TFP impact is a bit unclear. HIgh prices encouraged heavy investment in mines with low ore grades, which may in principle have boosted profits (and will have boosted labour productivity) but will probably have lowered TFP

But yes, the shift from the labour-intensive construction phase, to the low-labour productiion phase, is part of the timing story of the boost to Australia’s LP.

Of course, as many will note, much of the GDP gain is not accruing to Australians, but to overseas shareholders of the mining companies.

LikeLike

Did you spot a differential K/L story in this when you were looking at the Australia-NZ comparison Michael? Nevertheless, it is a concern in itself that the NZ’s Q/L growth slowed so markedly, despite using quality-adjusted labour for the market sector.

I am not sure how much the ChCh earthquakes might be affecting some of these statistics. They must have reduced the capital stock on impact, although payments by overseas reinsurers reduced the wealth loss. But low overall business investment is interesting given the extent of the ChCh rebuild. Presumably rebuild in ChCh by Fletcher Building etc counts as investment (adding to the capital stock), but perhaps not as private investment? But perhaps the numbers are too small to change the picture materially.

LikeLike

Hi Bryce

There is no doubt that on average Aus is more capital intensive than NZ – some of that is capital-intensive industries we don’t have much of (mining etc) but it is also the case in sectors that exist in both countries (consistent with the fact that wages in Aus are higher).

Re Chch, I included a chart in a post the other day showing how net capital stock/GDP had been pretty stable for several decades. In the investment numbers, the earthquake rebuild will have made some difference – more so in the residential investment numbers than elsewhere. From memory the peak annual rebuild expenditure was less than 2% of GDP, so at most our investment/GDP ratios have been flattered to that extent (but there will have been some crowding out of other private investment that would otherwise have occurred – eg part of the motivation for the RB tightenings in 2014 was the rebuild pressure on scarce resources.

LikeLike

have you tried throwing in whole milk powder, iron ore, coal, lithium etc in the productivity – investment mix. If iron ore was 150 these charts would look very different. Also mineral investment is a different kettle of fish to bring in Fillipino’s and milking a few cows. I struggle to see how these productivity studies between nations who produce different products are relevant surely?

LikeLike

all international comparisons are difficult, but are worth the attempt to the extent they shed light on eg policy choices, options, issues etc

LikeLike

When Emirates Team NZ was racing in Bermuda, they were cheered on by a huge number of New Zealanders waving NZ flags which completely swamped US supporters and totally embarrassed Oracle Team USA. I was tempted initially to take a couple of weeks off work myself to head out there but the 31 hour flight time proved too daunting for me.

I am starting to think all these complaints about vacant houses owned by migrants are actually New Zealanders staying 6 months in NZ and 6 months overseas on holidays to avoid being a NZ tax resident.

LikeLike

Given that both our countries operate very similarly with many shared multinational corporations and very similar type companies, and our mega cities swamped by migrants tourists and international students. There really is no real reason for the substantial widening gap unless the productivity gap is mainly due to the mining industry. Your data selection set must be wrong.

LikeLike

In fact, when my hotel safe went on the blink and I could not get access to my cash stored in the room hotel safe, it was clear that the battery has run down on the electronic safe which was not connected to the mains. 1 maintenance officer and 2 engineers came up to swap 1 battery. I asked them why?

They said, the maintenance officer cannot change batteries. Only can engineer can. The qualified engineer must be accompanied by an apprentice engineer to learn how to change a battery. I do not believe your dataset is correct. There is no way that Australians are more productive than new Zealanders.

LikeLiked by 1 person

This was in my Goldcoast hotel room.

LikeLike

They are official data from the respective official stats agencies, calculated in very similar ways in the two countries. Of course, the mining sector is a big factor in the longer-term levels difference between the two countries – whole new resources they’d didn’t know they had, and which we either don’t have or won’t exploit.

LikeLike

Australia builds submarines and frigates. It has significant heavy industries. Although it is in the process of closing it’s car manufacturing industries plus allied component manufacturing. It does have heavy industries.

New Zealand has shut down it’s Railway workshops, and now A&G Price in Thames, both heavy industrial. Did not understand Rail engine choice of buying $30 million Chinese rail versus Dunedin quote $60 million. On a circulation of $30 ml money into the community basis the decision to go Chinese import is questionable. Then there is Fletcher’s who have a 20 year history of borderline business disasters. NZ has a history of inability to export business smarts

LikeLike

Australia’s Economy Sector breakdown:

Services: 73%, Mining: 7%, Construction:9%, Manufacturing:7% (2016) Wikipidea

NZ Economy Sector breakdown:

Services 71%, Mining 2%, Construction 6%, Manufacturing 13%, Primary Industries 8% (2016)

Click to access nzefo-16.pdf

Goods producing industry or manufacturing in NZ is actually a higher percentage than Australia’s economy. The sector breakdown seems to suggest a very similar type of economy. Theirs slightly higher in mining and ours slightly higher in the primary industries. Their primary industries percentage is not even worth a separate category in their sectoral breakdown.

LikeLike

I await your response to the RBNZ’s Turner report

LikeLike

…takes the mind back to the PCs “Achieving NZ’s productivity potential” report; still pondering their point re growth in NZ employment being driven mainly by the service sector; not sure it offers a reason why this is or should continue be the case and the link back to low business investment….(other than perhaps those margins on avocado smash remain healthy!!)

LikeLike

I’m especially intrigued by the flatline business investment, despite massive inward migration, coupled with low inflation. Could it be that the increase in labour has driven down wages (hence low inflation) as a counterbalance to business investment. And could it be that this is a consequence of either inefficient or uncompetitive markets, or both? In terms of finding a root cause for the lack of investment driven productivity, while always multi-causal, I’d like to see strong policing of competition policy.

LikeLike

I’d be surprised if it was mainly a wages story – productivity has been so non-existent in the last five years that real unit labour costs to employers have probably been rising.

My own story puts much more emphasis on the exchange rate – so high it makes it hard to develop/grow potential high performing businesses from NZ. Rapid population growth and the inevitable rebuild process are part of the story why the exchange rate has been so high. Relatively low productivity activities in effect crowd out other possibilities.

Re competition, I don’t enough to offer much comment, although I’d be a little sceptical that the competition position has got so much worse in the last decade.

LikeLike