A few days ago I ran a post on the cross-country relationships between population growth on the one hand, and residential, government, and business investment on the other. Using OECD data, averaged for each country over a couple of decades, it was apparent that (a) as one would expect, residential investment makes up a larger share of GDP in countries with faster population growth (people want a roof over their head, but (b) business investment as a share of GDP was smaller the faster the population growth a country had experienced. New Zealand’s experience was quite consistent with these relationships. That should prompt some introspection on the part of those – bureaucrats, politicians, and other lobby groups – who champion our large-scale non-citizen immigration programme, the largest such active migration programme (at least for economic reasons) in per capita terms anywhere in the world.

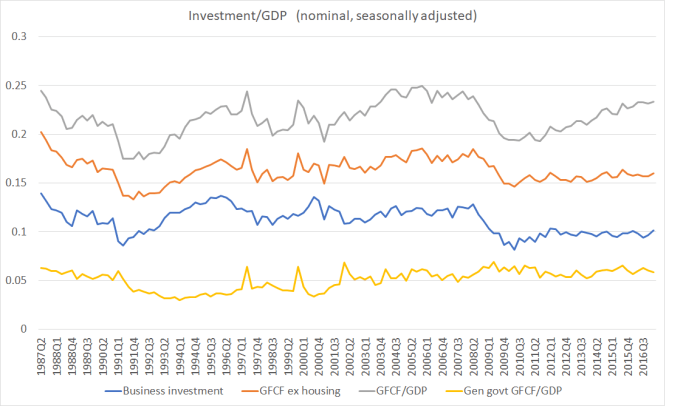

But today, I justed wanted to look at New Zealand’s own data on investment, and particularly the experience in the current cycle. My starting point is this chart, using the components of gross fixed capital formation (“fixed investment” in the national accounts), as a share of GDP, going back to the 1987 when the official quarterly national accounts begin.

As I noted the other day, “business investment” isn’t an official SNZ category – it would be great if they actually started publishing one – but instead follows the OECD practice of subtracting general government investment (schools, roads etc) and residential investment from total investment. It isn’t fully accurate, to the extent that some residential investment is done directly for the government (so there is some double-counting) but (a) the effect should be small, and (b) it is a consistent treatment through time.

And in case anyone is wondering what the spikes in 1997 and 1999 are, they are navy frigates.

Three things struck me from this chart.

- First, total investment as a share of GDP (the grey line) has been rising quite strongly from the trough in 2009 and 2010, but

- Second, total investment ex residential investment (the orange line) has barely recovered at all, and

- Third, business investment (as proxied by the blue line) has not only barely recovered, but is now smaller as a share of GDP than in every single quarter from 1992 to 2008. And this even though our population growth rate has accelerated strongly, to the fastest rate experienced since the early 1970s

The difference between the orange and grey line is residential investment. It has picked up a lot as a share of GDP, but then it would have been extremely worrying if that were not the case. After all, we had a series of destructive earthquakes in Canterbury, and huge volume of resources had to be devoted to simply restoring the existing housing stock. And we’ve had a big acceleration in population growth. Residential investment as a share of GDP is now higher than at any time in thirty years, although house and land price developments suggest that residential land is still being held artificially scarce.

Businesses invest when they see opportunities and can raise the finance (internally or externally to take advantage of the opportunities). There will always be some financing constraints – firms that don’t have the retained earnings or can’t persuade someone else to provide additional debt or equity – but it is a little hard to believe that, as this stage of the cycle, those financing constraints are much different than usual. It suggests that firms just don’t see the investment opportunities in New Zealand to anything like the extent they once did, even though the population is growing as fast as it ever has in modern times. It is at least suggestive that the persistently high real exchange rate might be an important part of the explanation.

New Zealand’s quarterly national accounts data go back only to 1987, but the annual national accounts data go back to the year to March 1972. Here is business investment as a share of GDP right up to the year to March 2017.

Not much above recessionary levels (1991 or 2009), and showing no sign whatever of picking up. And that is even though the population (and employment) are now much higher than would have been foreseen just a few years ago. Investment goods do appear to have got (relatively) cheaper over time, but that seems unlikely to adequately explain how firms saw investment opportunities of around 12 per cent of GDP in the two growth phases, but only around 10 per cent now (especially as we know we’ve now had no productivity growth for five years).

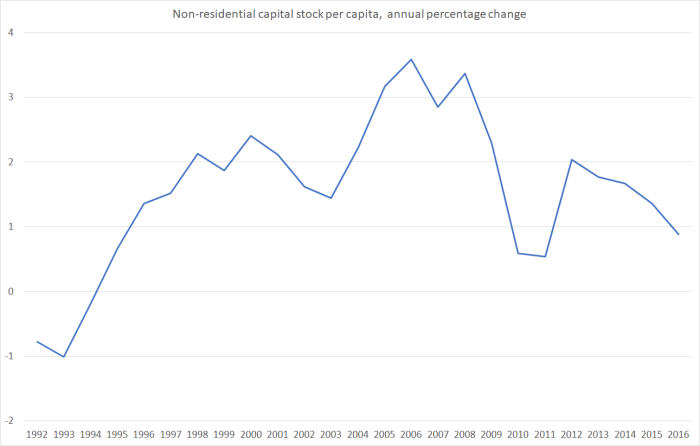

Statistics New Zealand also produces annual estimates of the capital stock. The latest observation is for the end of March 2016, but the earlier charts suggest there is little reason to think the story for the most recent year will be any more encouraging when the March 2017 data are released later this year. This chart shows the annual growth rate is the estimated per capita real net capital stock (excluding residential dwellings).

This indicator uses all the non-residential capital stock (ie including that belonging to the government sector). As government investment has held up more strongly than business investment (see the first chart above) and as employment has been rising faster than population, the picture for business investment per employee would probably look even more disconcerting.

And, of course, all the official capital stock numbers use reproducible capital only. In New Zealand, in particular, land is a major input to significant parts of business production. The quantity of land is fixed (improvements to the land are included in the investment numbers above), and that fixed quantity is spread over ever more people.

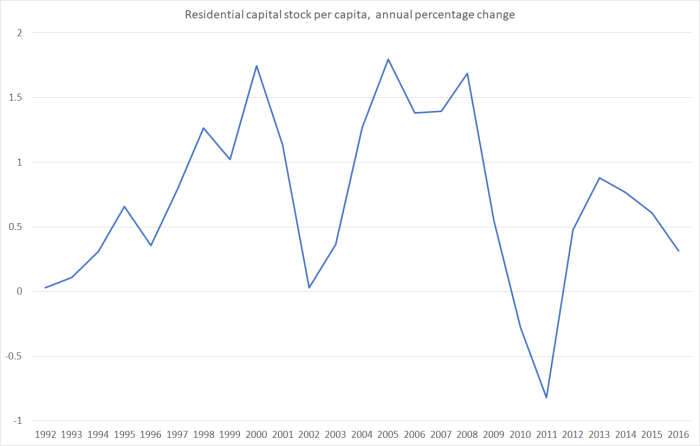

Given our very serious housing situation, with house price to income ratios among the highest anywhere in the advanced world, it should be a bit troubling when really the least poor bit in the investment data is residential investment. But lest I inadvertently comes across sounding upbeat on that score, here is annual growth in the SNZ real residential capital stock per capita.

But perhaps this too is some sort of “sign of sucess” or “quality problem”? Most people, I suspect, would settle for signs that if we are going to have rapid policy-driven population growth, that businesses would then find it remunerative to invest much more heavily, whether in building houses or producing other stuff to sell here or abroad.

I know you don’t necessarily agree with me but i still believe increased compliance cost over the last few years has reduced the enthusiam for expansion, As a small busines w have just spent over $5,000.00 to upgrade our H&S documentation to protect us incase of any accidents in the business.

Being associated with farming in Canterbury farmers are now facing significant costs to put inplace nutrient plans. These compliance costs may not be a problem for large cpmpanies but being a nation of small businesses they are not only significant in terms of financial costs but also take time and demend that extra skils are learnt.

Time and energy taken away from an individual growing a busines and investing in it. .

LikeLike

Alastair

I don’t disagree at all that rising burdens of regulation will have deterred some investment activity. If there is a difference it is probably only (a) a sense that rising regulatory burdens seem like a phenomenon in other countries too, and (b) even to the extent they aren’t whether the effects are large enough to explain the scale of NZ’s long-term economic underperformance.

LikeLiked by 1 person

It is easiest to think of myself. 40 years of work and various inheritances and I ought to be worth about $1m. However housing insanity in Auckland has left us worth double that. Children have left home so we have the potential to downsize and also sell one of our properties which would leave us with about $1.5m to invest. Since we intend to live in NZ it makes sense to invest in NZ. For the sake of this argument lets ignore issues with spreading risk.

Consider the options. Put it in a safe term deposit but it will earn little and that will be taxed and interest rates could go as per the UK or inflation as per the seventies. Put it in an investment company but our experience is reading about how they failed. Find a business and invest in it – too risky because there is an asymmetry of knowledge – the bosses may know what is going to happen but the investor doesn’t, so invest in something big such as an electricity supplier – similar but slower for the risks to materialise.

So how can I invest and not be at a risk disadvantage to the professionals? Housing of course, We know almost as much about property and location and rents as any real estate agent. So buy nearby so we can see it frequently, be very careful with selecting tenants, don’t be greedy, minimise taxable earnings. And if I go gaga and the government takes our wealth to pay for my care well at least my wife will retain a big house (I’m guessing the government wouldn’t evict her). Kiwisaver is the only alternative I can think of.

That level of ignorance about investing is duplicated by other baby boomers. Unless the government makes owning property less safely profitable we will not be investing directly or indirectly in businesses. [Unless one of our kids starts one.] It is sad because I’d like to support NZ business helping to make our children’s country wealthier. It will probably take a large drop in property prices to kick us home-owning baby boomers into action.

LikeLiked by 1 person

Why wouldn’t you put money in a range of equity unit trusts? You get exposure to the whole economy, equity returns rather than fixed interest, and don’t face the asymmetric information problems (at least more than the market as a whole, and in buying into funds investing in listed companies, they are also companies folllowed by market analysts) or an excess exposure to any particular company/sector.

LikeLiked by 1 person

The concept of leverage blows your investment returns in a range of equities out of the water. An average 10% price increase in property per annum equates to a 50% return on your investment based on 20% equity LVR. Therefore say $100k invested in a property returns you $50k per year each and every year forever. Of course some years higher and some years lower.

When economists remark about why they cannot understand New Zealanders love affair with property, That is why I suggest best that our next RB governor needs to be a Chartered Accountant.

LikeLike

Well-informed economists recognise that NZers are no more likely to hold property than people in other countries, although the particular vehicles it is held through vary country to country depending (substantially) on the details of the tax system. Our system is much more neutral across classes of taxpayers than the tax systems of most other countries (which often have highly preferential treatment for funds held in, eg, superannuation funds. or rule out loss-offsetting). Of our rental properties, more are held by individuals than is the case in other countries. The offset is that more of other stuff is held by other entities.

(in our case, the prevalence of standalone homes also tends to lead to direct holdings by individuals. It is easy for, say, a big institutional holder to own and manage a 500 unit apartment complex. Managing 500 individual homes scattered across suburbs isn’t a model many institutional owners, even abroad, have yet mastered.

As for the next Governor, character, good judgement, and openness to disagreement are, in my view, more important than specific technical or professional qualifications/background.

LikeLike

Looking at my own business and others I am around I see we are investing in lots of new plant. Small stuff with not a high value but none the less sensible in terms of individual productivity. Most of it computer controlled in some way.

The interesting thing about this is the cost and here I would like to suggest that we can lay the blame (for want of a better term), at the feet of the Chinese. They have developed their ability to produce modern plant at a fraction of the cost of what we were paying the Germans, British and the Japanese.

I can buy better machines for thousands less in cost than I could 10 years ago. Our industry is lapping them up.

A good example is cars or even trucks. In the case of cars, look what has happened to value for money. We used to buy over inflated poor quality Fords and Holdens at 60-70 k. Not anymore, the have meet their maker and as well we have stopped subsidizing the Aussie trade unionist. Easy to buy a great ute at under 30k these days. Does the same or better job at half the price. Trucks too, bigger, smarter more reliable, and use less fuel.

If we take the cost of steel used to build say a machine 20 years ago, look at that cost now and the ability using CAD to design better we can imagine why the difference. Apply that to many other products and you can see why companies are having to invest less. (Cars being the exception because we now seem to have to need to new one every three years. Driven by tax advantages using leases. That should be removed because cars last longer than 3 years and cars are generally are not a productive item but much more a vanity project).

Look at rail. They have just landed 100 container wagons for probably less cost than they could have 20 years ago. Concrete trucks; those revolving drums you see are now all made in china and from what I have been told cost way less then we used to make them for.

So what has happened to many domestic items and general merchandise has also happened to capital plant.

What I think is interesting about this is that this would explain the lack of apparent investment in many countries, not just our own. Doesn’t mean it’s not there but it is just costing less. In NZ the land of small businesses means that its many smaller transactions as we no longer have big paper mills or hydro’s etc to push the graph up except where say Airnz or the Govt. make a major purchase. The oil industry even hasn’t made big purchases for a long while. i.e. we are not growing major new capital intensive businesses. I would hazard a guess and say that our last major investment has been in fibre to everywhere.

It seems to me that the most important investment we should be making and where we are failing miserably is in R & D. Back in the late 80’s I recall seeing that the Japanese were spending anything from 4 – 10% of income on R & D. Our spending barely makes a blip.

LikeLiked by 1 person

You are right. We tend to get misled by Economists that adjust for inflation and present charts that are so called inflation adjusted. But how do you adjust for the deflation of computer equipment costs for example. My first experience with a computerised desktop was $50,000 and it sat in the corner because no one knew how to use it. My next computer experience was a $1 million Wang mini computer that sat in a air conditioned cooling room. All that computer capability now sits on my Iphone for $1,000.

LikeLike

Given your analysis in this post then why do august business organs such as the National Business Review seem to report on a narrative that is totally at odds with what is described above?

There seems to be a general assumption amongst the NZ business establishment that there are the general conditions of a boom but the analysis doesn’t appear to bear this out?

https://www.nbr.co.nz/tags/business-investment

LikeLike

Back when Labour came to power in 1999 we had several years when businesses were much more pessimistic than the actual data warranted (business surveys materially more pessimistic than the reality that eventuated). Under this government, it has been the other way round – more confidence than reality. I’m sure it isn’t people consciously distorting their response, but equally it does seem to be a systematic bias – under the Nats, businesses (and business media) want to believe.

Of course, total demand is growing quite strongly – GDP growth is reasonable even if per capita growth is very weak – and so many domestic-focused businesses are doing pretty well. Even in export sectors, some bits are doing well (the tourism boom) but in aggregate export growth is pretty subdued, to say the least, and of course businesses that have simply never set up(partly as a result of 10+ years of a high exchange rate) don’t get to respond to business surveys or to be interviewed by NBR (or even Radio NZ which – despite its general leftward tilt – sings from much the same upbeat song book when it comes to business/econ data).

LikeLiked by 1 person

The Nats hand out more money to their supporters whereas labour hand it out to theirs. Oh and do other bits of Law each way as well.

Interesting to see the number of oversea’s trusts that have been extinguished sine the reporting regime has changed. But there wasn’t a problem, except for our exchange rate.

LikeLike

Micheal from reading your analysis over the last few years I suspect the formula for high per capita income is fairly simple. You need a large political geographic conglomerate, 100+ million people, in a temperate zone, with a stable liberal capitalist government that controls corruption. Examples USA, the EU block, and China heading that way. The only exception is if you have valuable natural resources. One benchmark test is if you have a local competitive auto industry.

Japan at a bit over 100 million people is marginal. Australia misses on population but gains on natural resources, India is to tropical, U.k. with 30km of water between it and the EU is marginal geographically.

New Zealand did have a natural resource in Agriculture but this has been diluted by population. The excess has to be employed in “junk’ industries such as tourism. Tourism employs over three times the number of people as agriculture to achieve the same exports.

Our only options to have high incomes is to either, reduce the popu;ation to less than two million to take advantage of agriculture, increase population to over 100 million to achieve efficiencies of scale or find a big gold deposit.

LikeLiked by 2 people

I’m pretty sympathetic to that sort of story, altho i think you are probably a bit harsh on the prospects of the UK and Japan (not only do both have a lot of people, but they are also close to other places that generate lots of wealth for lots of people – Japan increasingly so).

I once ran a post here suggesting that the optimal population for NZ might be 2m or 200m, but I’m no longer convinced by the 200m option. The distance is still so great that i suspect the 200m would either find themselves in some sort of Latin American middle income outcome, or most would leave again if they could for places in more propitious locations.

We aren’t going to get back to 2m again, but – say – largely ending economic immigration would more or less stabilise our population at current levels. With good institutions, able and energetic people, lower regulation and lower corporate tax rates, and a willingness to use the mineral resources under our ground and sea, I’m pretty optimistic that we could get ourselves (productivitiy and per capita income) at least back up to the median of the old OECD countries, which was more or less where we were in say 1970. Our number 1 ranking of 1913 might be a stretch now, but even OECD median would be a huge improvement on where we are now.

LikeLiked by 1 person

With Australian cities in the past being an easy access with 600k kiwis living there, migrants have in the main been a replacement for departing kiwis. Going forward I anticpitate more kiwis returning to NZ with Australia’s economy weakeniing and the easy access to Australia being rapidly shut down, population in NZ will continue to grow even if we got rid of new migration.

My daughter touring Europe currently has only 6 months plan on being away. Previously I would have encouraged her to go to Australia or stay on in Europe for a bigger corporate ladder to climb but now I would encourage her to stay in NZ because being treated as a dirt class in Australia is not the best start in life and the whole disaster unfolding with the refugee situation in Europe makes it rather a powder keg.

LikeLike

Our excessive investment in agriculture is not due to our population growth. We export most of our agriculture production. 90% of our milk gets exported. We do not need 10 million cows to feed our tiny population. Only 30% of our agricultural production actually benefits our local economy through spending in the local economy. Economists look at gross GDP per capita in their equations which is simply wrong when you are dealing in livestock. It takes 10 million cows to generate $10 to $15 billion in export GDP. It takes 1.5 million Aucklanders to generate $75 billion in GDP.

LikeLike

….big fan of Country Calendar: always thought a (publicly funded) telly show featuring the stories of people developing business ideas / growing SMEs would be quite tasty (like the craft beer using malts grown by the Canterbury farmers per most recent episode – growing their exports nicely it would seem..!)

LikeLiked by 1 person

GDP per capita is a very significant statistic but occasionally we should remind ourselves that it is not the be all and end all. While changing in Glenfield leisure centre I overheard an elderly fat Chinese man talking to what by appearance I judged to be a middle aged plump Turk/Iranian. They were discussing in sad tones how hard it is to run a business in NZ until one of them suddenly said “But it is a great country to live in” and the other cheerfully agreed.

It was watching the overcrowded, over-built suburb of Ealing in the background of the news stories about the Grenfell Tower fire that reminded me why Auckland (despite our council) and New Zealand is so much better than my country of origin. New Zealand is still a great place to bring up a family assuming you have at least a medium income.

OK this is supposed to be a forum for economic ideas.

LikeLike

Great place to live – so long as you don’t value museums, art galleries, “history” or proximity thereto – but not a great place to build profitable outward-oriented businesses. Or at least that was how i summarised it to my audience the other day.

And given a choice between towns in pretty easy distance of London, I can easily see why many would prefer even the UK on lifestyle grounds.

But, yes, as always, income and income-earning potential are only ever means to greater ends. And home is home.

LikeLiked by 1 person

Big topic. Many aspects. Many dimensions. Sure.

The NZX is supposed to be the market where capital is created or allocated or finds homes

NZ reacted badly to the 1987 market crash and never recovered as soon as other global markets did. Lot of people lost a lot of money. NZX was in excess of

200-300 companies on the main board. Today it look like about 50 of substance if it’s lucky. The carcass of most of the companies of any quality were

picked over by offshore raiders and never replaced. Kiwi’s confidence in the stock market has never re-surfaced

Then

There was the sad episode of the 2009 Finance companies fiasco. Many if not most of those who lost money in this were people who vividly remembered the

1987 crash and never returned but were happy to put their money in a “safe place” – where else could they put their money. (I acknowledge that with the

passage of time people forgot the simple rule of risk and reward and the grape-vine took control. But it also exposed the terrible weaknesses in market

supervision etc

Now we have seen the emergence of the foreign businesses that exploit stupid tax laws of stupid governments that are too stupid to do anything to protect

the minions and permit Mossack Fonsaker Panama papers saga to go on unfettered

Example:- Government Judith Collins examination of Petrol companies in New Zealand and we now discover Commerce Commission does not have the power to

investigate – but they will be given the power to investigate after the election – maybe

See the following two links of the performance of the two largest petrol suppliers in Australia – they have never paid tax – it is siphoned out though tax

havens – do you think they are playing nice in New Zealand or are they extracting the capital out like the do everywhere else

Shell

https://www.michaelwest.com.au/shell-tax-ripped-out-as-in-house-deals-double/

Chevron

https://www.michaelwest.com.au/chevron-parents-leave-ato-an-orphan/

Australia has established compulsory Superannuation in 1990 – in the year 2000 it was a $1 trillion baby elephant – in 2010 it neared $2 trillion and now

it will reach $3 trillion on 2020

http://www.smh.com.au/money/super-pool-to-reach-3-trillion-in-just-three-years-20170707-gx6u76.html

The fund managers go looking for placed to invest their pooled funds. Looking for companies to invest in because they have the funds and the size. In AU

the largest segment are Self Managed Super Funds (SMSF’s) the next largest segment are Industrial Funds run by unions, followed by Retail funds run by the

banks. NZ doesn’t have that diversity. It is largely controlled by the banks and NZ Government doesn’t allow SMSF’s

That’s where IPO’s get their starter monies from – the Superannuation Industry which is hungry for a home. NZ, in the 10 years I have been watching,

actively discourages this amalgamation and agglomeration leaving it to the individuals who have money but not the size and thus move into housing

The residential housing industry is home to too much laundered money brought in from overseas while the government prevaricates on tranche 2 of the AML

Act having dragged the chain for over 10 years. US wanted it done in 2002, AU did it in 2006, NZ partially in 2015 tranche 1

LikeLike

2008/2009 recession was engineered by the RBNZ. It did not need to have occurred. The finance company fiasco did not need to occur and $6 billion of mum and dad investors did not need to have lost their life savings and an entire building industry did not need to be decimated. It was frustrating to watch how inept the Reserve Bank governor’s decision making process was. It was reckless and insufficient thought given to the long term repercussion of such aggressive interest rate hikes.

Even our traditional banks were under immense pressure to lend out with too much savings deposits seeking the high interest rates desperately dropping all manner of bank credit controls in launching the low documentation loan products. Bank instability was high not from not from house prices but from higher and higher interest rates.

LikeLike

Thanks Micheal for your last comment. Hopefully we know the problem and how to solve it. Just need to educate those that run the country ! cheers.

LikeLike

Are we investing in the right things with our merger R&D spend, as a country 93% plus is covered in water one would suggest at a national level a marine based focus would offer the biggest possible return. Given emerging tech around driver-less cars & the like, much of it could be applied to deep water exploration combined with long term global mineral demand that will see marine mineral recovery become a dominant source NZ could easily become very rich IF we treat it like an developing economy project (exempt from free trade agreements, major SOE involvement, NASA like research & publication).

What we don’t see is how (in)effective the under taken R&D investment is. I can’t read “Tragedy at Pike River Mine”, without thinking it was just another day in a New Zealand development program. Poor quality management cutting more corners to make up for the previous corner cutting that didn’t work. If you keep cutting corners all you do is keep circling the drain.

Not all “increased compliance cost” we hear about is real, the requirements for scaffolding on house building sites apparently has reduced build costs by about 10K per house due to the increased ease of access. Much of the intent behind the greatly hated (by pilots & CEO’s mostly) aerospace regulations is actually pretty close to best practice and recent actions to reduce regulation (in the US) will actually increase the engineering cost aspects of R&D’s programs

From an engineering point of view, there is lots of low hanging fruit for to make the R&D spend go farther: most of which can be described as increased discipline such as (noting that the lack of discipline often starts with understaffing):

Develop & maintain a corporate memory AKA write down what we actually did, so lessons aren’t lost.

For product development, CAD tends to drive companies to ineffective document system particularly if they are trying to engineer on the cheap, one maybe able reduce parts drawings by ~40% just by a better drawing system system.

Software training on things like Word & CAD, so you can actually have effective templates that everyone can use.

LikeLike

Pike River Mine is just an example of management doing their best to make a profit in the face of declining coal prices worldwide. They cut corners to save jobs. That mine should have been closed a long time ago. Unfortunately it is for health and safety reasons the mine remain closed. No one wants to be the final decision maker if they reopen and there is another loss of life.

LikeLike

The fact that the first 5% of a project sets the cost of the remaining ~80% and that there was much corner cutting in that first 5% (well before the mine was started), which caused the mine to have such a limited probability of success (high costs, low value produce, etc). It is a pity that health and safety aspects dominate the pike story because they are only the symptoms of what went wrong.

LikeLike