The centrepieces of the two weekend TV current affairs shows were political debates: The Nation had Phil Twyford and Amy Adams on housing, and Q&A had Grant Robertson and Steven Joyce on the economy more generally (but with a large chunk on housing). I only saw the Q&A debate, but I have glanced through the transcript of Twyford/Adams.

In the course of his debate, Phil Twyford was asked how much house prices should be relative to income. His response was excellent

Twyford: Ideally, they should be three times. If we had a housing market that was working properly, your housing would be— the median price would be about three to four times the median household income.

Grant Robertson repeated those sorts of numbers in his exchange with Steven Joyce. It was good, clear, encouraging stuff. A reminder of just how totally out of whack things are in the New Zealand house and urban land market. And a suggestion that the main opposition party wants things to be materially different and better.

But I can’t help wondering in which decade they expect things to be more or less okay again. In time for, say, my children – perhaps 10 to 15 years from now – or will it only be the grandchildren?

Don’t get me wrong. Watching the Robertson/Joyce debate, as someone who has no idea who he will vote for, I thought Robertson had much the better of the housing side of the debate. The current government seems reduced to some mix of lamenting that it is “a global problem”, reluctantly conceding that Auckland prices are a bit too high, and claiming that just over the horizon there is a wave of supply that will substantially address the problems. So if I’m critical of Labour here, take for granted that almost all the criticisms apply with more force to National.

Here is Phil Twyford avoiding suggesting that Labour wants house prices to come down

So is it Labour’s goal to get it down to that – about four times?

Twyford: We want to stabilise the housing market and stop these ridiculous, year on year, capital gains that have made housing unaffordable for a whole generation of young Kiwis.

But in essence, you’re going to drop the value of houses, if you want them to be four times the price of the average income.

Twyford: Well, we’re going to build through KiwiBuild. We’re going to 100,000 affordable homes.

I want to come to KiwiBuild in a moment. I just want to talk to you about the price.

Twyford: That will make housing affordable for young Kiwi families. That’s our policy.

Stabilising the housing market, and ending rapid house price appreciation, isn’t a recipe for fixing up the housing market for the current generation of young people.

Grant Robertson was much the same – reiterating the goal of house prices of 3 to 4 times income, but he couldn’t or wouldn’t say how long it would take. There was plenty of talk about building “affordable houses” (around $600000?) and “cracking down on speculators” and beyond that it all seemed to be down to growing incomes. But there wasn’t even a mention of freeing up land supply – a topic where formal Labour policy looks better than anything else on offer from major parties. Even though, the largest single component in the increase in New Zealand (especially Auckland) house prices has been the land component.

On the other side of the exchange Steven Joyce was taunting Robertson with the suggestion that “Labour wants to crash house prices with a punitive capital gains tax” – as if, whatever the (de)merits of a CGT, much lower house prices would be the worst thing in the world.

Lifting growth in productivity and real incomes is highly desirable. All else equal, flat nominal house prices and faster income growth is a recipe for improved housing affordability. But how long might it take on reasonable assumptions?

I’ve shown similar charts on this point previously. Here I assume a starting point of a price to income ratio of 10 (around current Auckland levels) and that (a) nominal house prices hold at current levels for the indefinite future, and (b) incomes grow at a rate equal to 2 per cent (midpoint inflation target) plus the rate of economywide productivity growth. I’m just going to assume that the 2 per cent average inflation could be achieved quite easily if the government wanted to. Productivity is the harder issue. Here I’m showing four lines using:

- actual productivity growth (GDP per hour worked) over the last decade (just under 0.6 per cent per annum),

- actual productivity growth over the last thirty years (for which we have quarterly real GDP and hours data), of just under 1.2 per cent per annum,

- productivity growth of 1.5 per cent per annum, and

- productivity growth of 2 per cent per annum.

The straight line on the chart is at a price to income ratio of 3.5 (ie the midpoint of the 3 to 4 times income Labour is talking of).

On the best of these scenarios, price to income ratios get to 3.5 in about 27 years time. If we manage productivity growth equal to that for the last 30 years – which itself would be quite an achievement at present – we’d be waiting almost 35 years.

Affordable housing, and a functional housing market, for the current generation simply requires a fall in nominal house prices. And yet no major party politicians seems to have the courage, or the self-belief (in their ability to communicate and take people with them), to make that simple point.

For most existing home-owners, the market value of their house does not matter a great deal. A large proportion of home-owners have a modest mortgage or none at all, so negative equity isn’t a risk. And since most people retire in the same city they’ve spent their working lives in, their house price doesn’t even affect very materially their own expected future purchasing power.

Fear of falling house prices seems to reduce to two particular dimensions:

- people who, having bought in perhaps the last five years, would find themselves with negative equity if house prices fell markedly (in turn divisible between new owner-occupiers and purchasers of additional rental properties), and

- some generalised fear that a fall in house prices goes hand in hand with economic disaster, serious recessions and the sort of experience the US or Ireland had.

The latter is mostly a category error. In both the US and Ireland, there was material overbuilding (excess stocks of actual houses). There is no prospect of that situation in New Zealand on any of the policies of the major parties. In Ireland, the situation had been compounded by joining the euro, which gave Ireland interest rates set in Frankfurt that bore no relationship to the needs of the Irish economy. In the US, there had been persistent official efforts – from Congress, the Fed, and successive Administrations – to encourage, or compel, the financial system to take on housing lending risk that the private sector would be unlikely to have assumed willingly. None of that resembles New Zealand. Not only do we set our own interest rates, but to the extent there is state involvement in the housing finance market it is reducing the supply of credit.

A severe recession could, at least for a time, lower New Zealand house prices. Recessions – severe or otherwise – aren’t things to welcome. But the sort of land market liberalisation (with associated infrastructure rules) that might, as a matter of policy, set out to materially lower New Zealand house and land prices would be most unlikely to materially dampen demand or economic activity. If anything, it could represent a material boost to demand, as building became more affordable. (And if some people would find themselves with negative equity, whole swathes of younger generations would suddenly face new opportunities and less of a desperate need to save.)

What about the people facing negative equity? I don’t have any particular sympathy with those who’ve purchased investment properties in recent years and might face being wiped out. They’d have taken a business and investment risk – in this case on the regulatory distortions never being fixed – and lost. That happens in all sorts of market – think of the people with exposures to shares after 1987, or in finance companies 10 years ago. Or those with businesses based in import licenses in earlier decades. It is tough for them individually, and almost all of them have votes. But it was a business risk, and a conscious voluntary choice.

I’m much more sympathetic to those who bought a first house and could face a large chunk of negative equity. I touched on this in a post a few weeks ago

No one will much care about rental property owners who might lose in this transition – they bought a business, took a risk, and it didn’t pay off. That is what happens when regulated industries are reformed and freed up. It isn’t credible – and arguably isn’t fair – that existing owner-occupiers (especially those who just happened to buy in the last five years) should bear all the losses. Compensation isn’t ideal but even the libertarians at the New Zealand Initiative recognise that sometimes it can be the path to enabling vital reforms to occur. So promise a scheme in which, say, owner-occupiers selling within 10 years of purchase at less than, say, 75 per cent of what they paid for a house, could claim half of any additional losses back from the government (up to a maximum of say $100000). It would be expensive but (a) the costs would spread over multiple years, and (b) who wants to pretend that the current disastrous housing market isn’t costly in all sorts of fiscal (accommodation supplements) and non-fiscal ways.

Those numbers were made up on the the fly, but even on later reflection they look like a reasonable basis for something that might not be unreasonable, and also might not be unbearably expensive. It would recognise that people need to bear some material risk themselves (a 25 per cent fall in nominal house prices is not small). But it is also designed in recognition of the fact that since 2013, it has been hard for first home buyers to get a mortgage above an initial LVR of 80 per cent, so that not many would be in negative equity now even if house prices fell by 25 per cent from here.

Since many people will stay in their existing house for a long time if they have to, and the scheme only compensates if the house is sold, that also limits the potential fiscal cost. In fact, the biggest pool of owner-occupiers who would sell at a material loss would be those forced in the event of new severe recession (unemployment is typically the biggest threat to the ability to service mortgage debt) and (a) those people would naturally command a degree of public sympathy and (b) land liberalisation would be a stimulatory policy, reducing the chances of a near-term future recession. There would be some voluntary sellers, to capture the compensation, but the cost of selling and buying a house, and of moving house, is not trivial. If 100000 households were to claim the maximum compensation of $100000 that would be total additional government expenditure of around $1 billion, spread over a considerable period of time. And to claim $100000, you’d have to have bought say a $1 million first house and seen house prices fall 45 per cent from your entry price.

It isn’t a perfect scheme by any means, and lots of details would need to be fleshed out. One could relatively easily restrict it to apply only to those in a first owner-occupied house, again the people who will naturally command the most sympathy anyway. But if something of this sort could be done for, say $1 billion, and it helped the pave the way for a genuine structural fix in the housing market – a willingness to actively embrace lower house prices – it would seem likely to offer more value than, say, the least valuable of the proposed 10 new “roads of national significance”, which are estimated to cost on average just over $1 billion each. How much congestion is there on the existing road from Levin to Sanson?

And three final points on housing:

- it was depressing to read the housing section of Jacinda Ardern’s campaign opening speech. It wasn’t the focus of her speech, but – just like Andrew Little at his conference speech earlier in the year – there was reference to dealing to “speculators”, barring foreign purchasers, and to the state building more houses, but not a word – not even hint – about freeing up the land market in a way that might make those price to income aspirations achievable,

- it was slightly strange listening to Robertson and Joyce debating the possibilities of a capital gains tax, focused on housing. Weirdly Robertson didn’t take the opportunity to rule out applying a CGT to unrealised gains – even though he surely really realises that, whatever the theoretical appeal, there is no way anyone is going apply a CGT to anything other than realisations. But it was even more strange to hear this debate going on after both sides were insisting they “had a plan” to fix housing. If they really did then surely there would be few/no systematic capital gains in the housing market for decades to come?

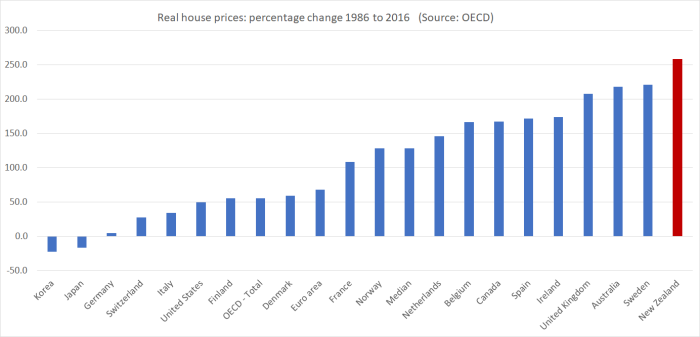

- and finally, Steven Joyce ran his line that house prices are a global problem. This seemed to be a variant of the sort of “problems of success” line John Key often ran. Out of curiosity, I dug out the OECD’s real house prices series this morning. They don’t have data for quite every country, but here is the change in real house prices from 2007 to 2016 (annual data) for the countries they have the data for. There are a few countries that have done worse, but not many. In the median OECD country, real house prices have fallen over the last decade.

Mostly, the countries that have been about as bad as us have also had quite rapid population growth (Israel, Australia and Luxembourg in the lead on that count) – not, of course, that either Finance spokesperson suggested doing anything about that.

What about a longer-term comparison. There are lots of gaps in the OECD data for earlier decades, but here are real house prices increases for the countries they have data for over the three decades to 2016.

Worst of them all, without even the income growth to match.

We need to face up to the importance of lowering house prices, of adopting policies likely to sustainably make that happen, and – if necessary – consider compensation packages for some to help make that transition possible.

I’ve struggled for a while to understand the focus on a CGT. As I understand it the Australians have had one (that excludes the family home) since 1985, and, based on the graphs above this has had little or no impact on real house price growth. It appears (albeit, without any in-depth analysis on my behalf) to be an answer that doesn’t solve the problem of rising house prices.

LikeLiked by 1 person

That was certainly the conclusion the Reserve Bank always reached when it was commenting on the CGT issue. On introduction there might be an initial effect, modestly lowering prices, but the international experience suggests the effect would be quite limited (in size and duration). of course, if they did put one on unrealised gains the effect would be larger.

I think the case for a CGT is mostly a (perceptions of) fairness one. But fix housing supply and any future real capital gains will be non-systematic and not readily forecastable (and gains and losses will balance out, so there won’t be any expected revenue).

LikeLiked by 1 person

The exclusion of own home from the CGT equation makes it a difficult tax to administer. Even the Bright Line Test will increasingly be a problem administering when people know enough to go live in their investment property before selling.

LikeLike

The price to income ratio in Auckland at 10 (possibly lower since recent drops) is horrendous and would need a halving of values to bring it to a reasonable 5.

However that is not all that FHBs can wish for. That nominal ‘price’ is probably currently a 200sqM house on a medium sized section and not on the outskirts. The already affordable property is at $650k and is smaller (say 120sqM and on a smaller site further out). Hence a 25% drop in prices would force a price closer to $500k and that starts to look better. Building costs are not likely to offer a 25% fall but site values are more price flexible and Auckland Council might have to rethink some of its charges and recover some out of future rates revenues.

Maybe, maybe.

LikeLiked by 1 person

I have been told by several builders to plan for$3000 per sqm to build in Auckland. This excludes the cost of land.

LikeLike

Michael, you have regularly claimed “freeing up land supply” as a significant solution to housing prices. I can understand the impact of bringing more serviced sections to market. Where I have difficulty is getting my head around who is going to do the investment and bear the costs of doing so. It’s not just a case of changing zone restrictions and moving a few lines on a map. I put myself in the shoes of a land-owner of a semi-rural property that is rezoned and the value goes up by 40%. I cant afford to subdivide and develop and put in roads and footpaths and power and drainage and waters. So I’m forced to sit on my hands and eat the increased costs of rates. Or I can sell the land to a developer. I then put my self into the shoes of a developer and offer to pay the land holder the going rate. Right at this moment, in the current climate, if I was in that business I think I would be contracting and mothballing back to bare-bones and trying to unload all stocks of unsold inventory. Battening down the hatches.

Can you please explain how you see “freeing up land supply” working

LikeLike

The fine details aren’t my area of expertise. But I’ve suggested before (focusing on Auckland), drawing a circle with a radius of 100 or 125 km centred on Queen St and allow any land in that area to be developed to a height of two storeys. One could add in refinements allowing greater height as of right in areas where that wouldn’t cast shadows on existing dwelling, or overwhelm exisitng urban roads, but I see little sign of much NZer appetite for height except (a) in central city areas, and (b as a third best to being able to afford the land for a detached house. One would of course have exceptions for land that was seriously geologically unstable, on a flood plain or the like.

Under that sort of regime, all empty land (and its owners) are competing with all other empty land as to where the next new suburbs and satellite towns will go. By removing the regulatory scarcity you create an incentive for the land to be used more quickly. Actual supply and expected supply would combine to materially lower urban and periphery land prices.

As to who would do the development, I’d assume mostly specialist development companies with the expertise and capital behind them.

There are of course some significant issues around transport and other infrastructure. I don’t lay claim to any great expertise there, but these issues appear to be managed in the vast swathes of the US with low and stable price to income ratios. Personally, I haven’t invested huge amounts of time in studying the options there because i think the population growth strategy is so deeply flawed. If we adopted a sensible immigration policy – eg 10-15K residence approvals – there wouldn’t be much trend growth even in Auckland’s population, and so a deregulated land use market would probably be sufficient to get house/land prices back to a reasonable level, without worrying about how to cope with another 40000 every year.

I should add the point I’d made in an earlier post but not in this one: construction costs seem to matter too, and I’m not confident of the answer there. I hope any new govt makes it a priorty to get to the bottom of that issue, and resolve it, even doing so involved direct government involvement in the market. Without doing something on the front, I’m sceptical that NZ house+land prices can be got all the way back to the 3x that. say, Demographia often tout.

Oh, finally, on your point about the current situation: yes, it is quite possible that some existing developers will be cautious, esp if the market were to go sideways for a year or two, and they had already paid up large for land. But that is different issue to how one would expect the market to develop with far-reaching land use liberalisation.

LikeLike

Re building costs.

Remember that in the last period of the two governments (1999 onward) we have seen added extra cost to building including front loading land services, insulation including double glazing, timber specs, geotech for nearly every site etc.

And do not forget the councils are trying to recover the leaky building costs.

We get better housing quality but it all costs

LikeLiked by 1 person

Yes, but I think is uncontroversial that building products are typically materially more expensive here than in Aus or the US. I do think eg making double glazing mandatory is regulatory overkill, but probably the political energy should go into identifying and eliminating the “rents” that someone is capturing in the products markets.

LikeLike

Auckland is already spread from Leigh up north to pukekohe down south a distance of 129km. Houston spreads from Woodlands up north to Texas city down south a distance of 118km with 6.2 million people. Auckland is a very long city due to the geography with water on 3 sides. It has hills and valleys, streams and rivers. Unfortunately we have put our largest city on the smallest piece of dirt in NZ. Auckland has unique features eg the waitakere ranges plenty of land but also full of kauri trees and native bush. No way the community would allow large scale building. There are 57 sacred mounts subject to a visual height limit which means that most of central Auckland will be subject to at most 5 level buildings.

The Unitary Plan zoning allows a 2nd dwelling concept that allows for 2 dwellings as you suggest already. But for most owner occupied households they do not want home and income unless they really need the extra income.

LikeLike

All true, but there is still a great deal of undeveloped land in and around Auckland, and no good reason – even given the “sacred mount protections” – why AKld land prices need be as high as they are.

LikeLike

Fletcher Building would be a great example how those sacred restrictions have hammered the companies profitability and shareprice as a result. It is encountering issues with 3 Kings where current zoning allows for 1600 properties but the community has protested and have got the backing of the environment court to consider the sacred hole called a quarry and therefore cut the number of units to 1200. When you remove 400 houses out of the development it does not change the basic infrastructure costs. All it has done is resulted in more expensive housing in 3 Kings development and costly for the developer after years of delays.

In Mangere a 480 housing project got cancelled after years of protesting due to sacred caves and Council removed the Special Housing Status after Fletcher had already spent millions on earthworks, planning and preliminaries.

Steven Joyce pointed out to Phil Tywford that Labour Party was fully involved in causing the delays in the RMA reform and in blocking the building of more housing that would have led to cheaper houses from economies of scale.

LikeLike

Of course development needs access to development finance. The high risk development finance industry got decimated when 61 finance companies collapsed between 2007 and 2011 with the loss of $6 billion in investor funds.

If banks are not lending to develop then no development takes place which results in scarcity. That scarcity leads to upward pressure on prices to cover the increased cost of borrowings.

LikeLike

Getgreatstuff, has the Oruarangi SHA development been cancelled? I thought Nick Smith had refused to agree/sign a revocation order?

http://www.stuff.co.nz/auckland/local-news/manukau-courier/71494315/Bid-to-stop-Mangere-Special-Housing-Area-fails

LikeLike

“A Fletchers project to build up to 480 homes on a Mangere site, including ancestral burial caves, may be the first Auckland Special Housing Area to be revoked after a revolt by local residents and a change of mind by some city councillors. Seven Auckland councillors, including both Manukau ward councillors Arthur Anae and Alf Filipaina, have signed a notice of motion to revoke support for a Special Housing Area (SHA) at the next full council meeting on August 27.”

Sorry. This article was dated 13 August 2015 so it is a ongoing saga of yay and nay. The latest is that Fletchers has approval, May 2016 article. But this is where the costs start to mount up with the yay and the nay creates uncertainty and ballooning costs.

“Locals are vowing to keep fighting a controversial special housing area after it received the go-ahead from commissioners. Fletcher Residential has received permission to build 480 homes next to the protected Otuataua Stonefields reserve in Ihumatao, Mangere. The Accord Territorial Authority, made up of four commissioners and Franklin Local Board member Murray Kay, made the decision after a series of hearings in February 2016.

http://www.stuff.co.nz/auckland/local-news/manukau-courier/80325008/fletcher-gets-goahead-for-ihumatao-special-housing-area

LikeLike

Couple of things here. Firstly I think we’re already in the zone of correcting house prices due to mortgage rates (refer earlier comment in reply to your earlier post on Shamubeel). Dominick Stephens from Westpac is saying as much: http://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=11906767

Will it be a crash? Probably not given continued immigration levels but reality is that a $ stretches only so far and with leverage decreasing people just can’t afford to pay asks, so asks have to move (so that people can…). So you end up in a weird situation of housing shortages but falling prices. I noticed homes.co.nz has reduced Ak price estimates by up to 10%; and yet I walked past 2 cars on beach access streets this weekend that were clearly being used as homes by their owners.

Secondly, to get down to 3-4x sooner than 35 years you can change the mix. Build higher density, smaller homes that sell at lower prices. But you need to fix planning and building costs for that. Good luck!

LikeLiked by 2 people

Yes, I agree with Dom that interest rates are probably playing a part. Which is one reason I’m not optimistic the pause is going to last – there is nothing in the wider economy suggesting that higher interest rates were required, and so I don’t rule out further OCR cuts to (in effect) neutralise the effect.

Re your second para, yes I agree, altho of course smaller/denser houses aren’t really what people would prefer. they get a roof over their heads, but they should have been able to have a market functioing that enables them to have so much more.

Re building costs,yes as I noted in a response to an earlier comment that is the other thing a new govt really needs to get to bottom of and do something about. But again, nothing from Labour. Which, in the end, is why I’m sceptical we’ll see much change at all. Whenever the next recession happens we’ll see another pullback, as in 08/09, but if nothing about structural policy changes it is hard to see why the next upswing shouldn’t just see prices go higher still.

LikeLike

Rather than being “excellent”, I’d suggest Twyford’s claim about an ideal price-income ratio reflects a fundamental misunderstanding. The price-income ratio is just one, incomplete, indicator of housing market conditions, and one that has no obviously ‘ideal’ value. For example, a ratio of 3 when mortgage rates are 5% is a very different beast to a ratio of 3 when mortgage rates are 20%. Ditto when tax rates are high compared to when they’re low.

What Twyford doesn’t seem to get is that these things are determined endogenously — you don’t just get to choose a desired value of one thing in isolation. So talking about an ‘ideal’ price-income ratio is Fairyland Economics.

LikeLiked by 1 person

“The price to income ratio in Auckland at 10 (possibly lower since recent drops) is horrendous ”

The problem here is that it is always compared to the National median income. what if it was compared to the incomes in the area the the houses are based. totally different picture I suggest.

” That nominal ‘price’ is probably currently a 200sqM house on a medium sized section and not on the outskirts.”

Yes and that is being compared with the old 110sq meters or less that was the house size many years back,including up into the 70’s. So not the same comparisons.

“Michael, you have regularly claimed “freeing up land supply” as a significant solution to housing prices. I can understand the impact of bringing more serviced sections to market. Where I have difficulty is getting my head around who is going to do the investment and bear the costs of doing so.”

Well if we are comparing apples with apples we would need to take into account that going back before Govt.’s gave local bodies (in many countries), the right to beat up the developers the councils themselves funded all the infrastructure on a long term basis. These days it is an up front cost that is paid (indeed prepaid by the section provider.

“I should add the point I’d made in an earlier post but not in this one: construction costs seem to matter too,”

“They are coming in with quite substantial deposits with the Kiwisaver First Home grants. It makes such a change to people’s lives.”

“The locals are buying because they can stay close to home and extended family, says Mark.

The older buyers wanted to move away from the bigger section and the younger buyers want to be able to buy into their first home.

The under $550,000 houses look the same as the over $500,000 houses. The same claddings, double glazing and internal fixtures and fittings, says Mark. The difference is in the size, and a few things like a different grade of the same brand flooring, plumbing a dishwasher but not fitting it.

“That saves $1000,”

Direct from todays Sunlive.http://www.sunlive.co.nz/news/160880-turning-complainers-into-customers.html

What he is pointing out is that yep you can build cheaper houses. They just do not have all the whiz bangs. And therein lies another difference. The basic 3 bed 100-120 sq meter house of the 60- and 70’s didn’t have garages already built in, they didn’t have media rooms and such, didn’t have wiring other than very basic 3 pin plugs one to a room. No wiring up for your TV or your computer. all these things are exoected today and simply drive up the price.

“I’m sceptical that NZ house+land prices can be got all the way back to the 3x that. say, Demographia often tout”

Hugh talks nonsense. He is comparing house price built by a population that is paid $7.50 an hour if they are lucky. That’s what importing Mexicans does along with no minimum hourly rate. why don’t you try asking a Kiwi or Aussie builder to work for that hourly rate? He also doesn’t talk much about the weather conditions and that funny little quirk we have called earthquakes. The houses demolish in a bit of breeze, they don’t do rain like we do and they don’t have earthquakes to bother their insurers. Different in California though.

“building products are typically materially more expensive here than in Aus or the US. I do think eg making double glazing mandatory is regulatory overkill, but probably the political energy should go into identifying and eliminating the “rents” that someone is capturing in the products markets.”

Some have tried of course but in the end they fall over or we finish up with product that doesn’t make the grade. e.g. steel, wallboard. every Kiwi has bought cheap stuff only to recycle it to the dump and make the importer fat.

‘Yes, I agree with Dom that interest rates are probably playing a part.”

Unlikely as they have barely moved and indeed are currently on the down, a down which I think will keep going for some while. There is just no reason why NZ should be the world leader in high interest rates other than the fact we spend more than we earn, mostly on trivia, cars and oversea’s trips.

The first 100k of a build is swallowed up by the councils. First on the section and all the details around them and their infrastructure, collecting for the nice to have reserves etc. etc. The next lot is taken once you look for a permit or worse if you need some departure from the norm and find yourself having to go to a hearing , fighting the rulings etc.

The next biggest determinant of the cost is the school. What school it is and how close.

Twyford convieniently fudges the numbers using aucklands figures and that and Christchurh are the two area’s where schools have a huge effect on the house prices. A study out a couple of weeks ago that I saw had rated the effect. In auckland some schools raised the house prices in their given area by 90%.

The answer to these of course in more schools in more area’s. If the Govt. were to build or dare I suggest allow Charter Schools to grow then that would have more effect on the house prices than any other single determinant.

“Buyers must pay price premiums of up to 90 per cent to get into the best school zones, new data shows.

Homes.co.nz has revealed that good school zones add significantly to the price that houses command, in many cities around the country.

The biggest difference is for Epsom Girls’ Grammar’s zone in Auckland, which adds a premium of 90.5 per cent to local house prices.”

https://www.stuff.co.nz/business/95390822/data-shows-school-zones-make-significant-difference-to-house-prices

Which makes a mockery of Twyfords ramblings and selective “facts”.

So the best answer is more schools with high standards so school customers (youknow the people who pay for the education) don’t have the need to compete for what they seem to think is the best education available and thus wouldn’t need to spend nearly twice as much to buy in the “in school zone”.

Now maybe a bit of serious study of that would encourage our lazy politicians to grow more schools instead of motorways so kids can get to school.

IMHO that simple study changes to game completely.

LikeLike

I’d disagree. I’m pretty sure he is aware that such a ratio is determined endogenously, and is drawing on the work of people like Demographia suggesting that a ratio of around 3 has been normal in a market that isn’t governed by tight land use restrictions.

In such a market, the unimproved land value is typically a small part of the price of a house+land (very much unlike the current NZ – or Sydney or SFO – situation. In such a world, only the unimproved value of land is, in principle, materially influenced by either interest rates or tax rates. As it happens, of course, in a cross-country comparison we have the highest real interest rates and some of the higher capital income tax rates.

LikeLike

Just wondering what would happen to the “Welcome Home” loans the Crown has underwritten / guaranteed. Probably small fry in the scheme of things but if borrowers were in line for some compensation, there could be a few howls (or whatever noise a kookaburra makes..) from lenders…

LikeLike

yes, presumably they would need to be excluded from any compensation scheme.

LikeLike

I watched an interview with Scott Morrison on SkyNews the other night and his answers to questions on the economy were much the same as when Joyce is tackled.

On land supply, it is interesting reading the debate in Australia following the new website set up by Dick Smith.

There are arguments that there is not enough land in Australia to support the current immigration levels.

It is worth reading dicksmithfairgo.com.au

LikeLike

I’d suggest that homeowners think of their home value the same as money in the bank, so any attempt to overtly lower house prices would get considerable blowback. Do you have any research on people’s attitude to this?

LikeLike

Jacinda is back onto the David Cunliffe mantra. Capital Gains tax under labour is now fully back on the active agenda. Capital Gains Tax is intended to be broad based and is not isolated to investment property. It is also a tax on business capital gains, on inherited property, on holiday homes on shares in unlisted entities and if sufficiently broadbased would also include unrealised capital gains based on valuations.

LikeLike

The unspoken variable is increased inflation. A slightly higher inflation target would bring wages up to 1/3rd of house prices much more quickly.

Also, think about the impact of decreasing income inequality. If incomes rise faster for the lowest paid, relative to the higher paid, then the median income will increase faster than GDP per person.

LikeLike

Yes, mechanically thst is right. A higher inflation rate would have costs of its own, and altho there is some argument for a higher inflation target anyway, I’d rather fix directly the things that lead people to argue for such an increase.

LikeLike

Of course, fixing the underlying issues is good, otherwise the problem reoccurs.

However there is an actually existing issue with house prices so far out of whack with incomes, which is going to cause big social problems if it can’t be corrected before another whole generation grows up and still can’t get reasonable cost housing.

LikeLike

Indeed, but changing the inflation target in isolation will make no beneficial difference to that problem. Indeed, it might even worsen it, because higher inflation rates mean higher nominal interest rates and thus higher servicing burdens in the early years of a mortgage.

But as part of a package of structural measures to fix the housing market, a higher inflation rate could help speed up removing the perceived debt overhang and risks of large numbers ending up with substantial negative equity. That was, in effect, how things worked in the late 70s.

LikeLike