Graeme Wheeler indicated yesterday that he will shortly be giving a speech offering some reflections on his time as Governor. It is a good idea, at least in principle. Wrapping up his 10 years as RBA Governor last year, Glenn Stevens gave a thoughtful speech along those lines (which I had intended to write about, but never got round to). Wrapping up his 10 years as Governor of the Reserve Bank, Alan Bollard did an interesting interview with one of the editors of the Bulletin – he even acknowledged having made a mistake early in his term.

It is hard to be very optimistic about the forthcoming Wheeler speech, but ….. perhaps……this time. Someone emailed me last night, after my comments on yesterday’s news conference, suggesting that

surely at heart you would have been more disappointed if Wheeler had finally answered questions in a meaningful way. Would have made the past 5 years of communication even more painful.

I’d have been astonished certainly, but I have a naively optimistic streak and I’d like to be pleasantly surprised, even this late in the game. When he was appointed, I had had high hopes for the Governor.

But the promise of a forthcoming review speech, and an exchange with someone yesterday about the relative performance of the three Governors who have operated in the inflation-targeting era (in which I found myself defending Graeme), got me reflecting on how one might do those comparisons, at least in respect of monetary policy.

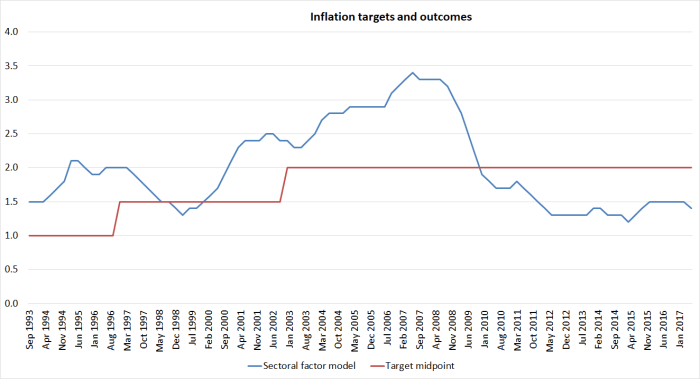

One could simply look at deviations of inflation from target. Using headline CPI inflation wouldn’t help much there – the CPI in the 1990s was constructed materially differently than it is now. And when Don Brash took office there wasn’t an inflation target at all. But the Bank is fond of its sectoral factor model measure of core inflation. That measure has only been around for the last five years or so, but the Bank has calculated the series back to September 1993. And as it happens, the first inflation target that last long enough for performance to be measured against it was the one adopted by the incoming National government in December 1990 – inflation was to be 0 to 2 per cent by December 1993.

So here is the sectoral factor model measure graphed against the midpoint of the successive target ranges.

There are several things to notice:

- this measure of core inflation has been much more stable in the Wheeler years than in any previous five year period,

- none of the three Governors kept sectoral core inflation (or any other measure) close to the midpoint of the target range, and

- the biggest deviations were in the last years of the previous boom, when this measure of core inflation was actually outside the target range.

In terms of average deviations

| Brash | 0.5 |

| Bollard | 0.5 |

| Wheeler | 0.6 |

But the Bollard decade was a tale of two halves: far above the target midpoint for his first six years or so, and then increasingly below the midpoint by the end of the period.

All this said, I wouldn’t want to put too much weight on those numbers, for various reasons including:

- monetary policy works with a lag. One can’t blame Graeme Wheeler for the first 12-18 months’ outcomes during his term. Then again, the last three or four years’ numbers aren’t much different from those early in his term,

- this measure didn’t exist, and certainly wasn’t being used, in the Brash or Bollard years (that said, no one disputes that inflation ran above the target midpoint during their terms, for various – different – reasons),

- only since Wheeler took office has the target midpoint had any formal status. In practice, Don Brash did aim for the midpoint, and often referred to it in public communications. Alan Bollard didn’t regard the midpoint as being particularly important, and thought (and talked) in terms only of being comfortably inside the target range (thus at times we published projections with inflation settling back to around 2.5 per cent).

The fact that inflation averaged well above the target midpoints during the Brash years often surprises people. Don had a reputation as an inflation-hating hardliner (an “inflation nutter”), which was – at least in some respects – well-warranted (he could also, at times, be a political pragmatist, to the dismay of the real hardliners). He took the targets, and the midpoints, seriously. So why was inflation averaging persistently above target? My story is that he – we – never quite realised how much higher than international interest rates New Zealand interest rates needed to be to keep inflation here in check. In today’s terms, we underestimated the neutral interest rate. In a way that wasn’t surprising. After the great disinflation, we expected our interest rates to converge to those of the rest of the world – and international visitors encouraged us in that view (I well recall the day a visiting senior Australian sat in my office trying to argue that we must have policy wrong because interest rates were still so much higher than those in Australia). That convergence has simply never proved possible – I argue because of the interaction of high immigration and low savings, but the “why” is a topic for another day. Everyone realises that now, but we didn’t in the 1990s. It led us to forecast lower inflation rates than we ended up achieving, and because – in effect – we believed our model we kept making what amounted to the same mistake.

Alan Bollard’s “mistake” was different. He came into office with a sense that Don – and those around him – had been too hardline, and that if only we “gave growth a chance” we could get better outcomes all round. I suspect he really did care about unemployment. He certainly cared a lot about the tradables sector, and the rising and high exchange rate quickly became quite a constraint on what he was willing to do with the OCR (it was something of a political constraint too). He was probably less willing to tighten than the median of the staff advice would have been, but actually staff advice also had something of the wrong model. People just didn’t realise how much momentum there was behind the boom, or how structural (to the interaction of population and land use regulation) the lift in house prices was. Because of the exchange rate, Alan was unwilling for too long to contemplate taking the OCR anywhere near the (real) peaks of the 1990s, even though by most measures – whether unemployment or capacity utilisation – the pressure on resources was much greater.

All three Governors made what would now be generally recognised as mistakes. Some lasted shorter than others. We held off adopting an OCR for years too long. In 1991 we made the now-incomprehensible mistake (I strongly supported it at the time) of trying to hold up interest rates even as the economy was falling away rapidly into a recession, on some misguided view around the interpretation of the yield curve slope. That lasted only a matter of months. Then there was the MCI debacle in 1997 and 1998. And scarred by that experience, we were too quick to cut the OCR in 2001 – responding to a US recession that never much affected us.

Alan Bollard later openly acknowledged that his interest rates cuts in 2003 had been a mistake (at the time I’d thought at least the first one was appropriate). And in 2010 the Bank was too quick to start raising interest rates, and had to reverse itself quite quickly.

As for the (single) Wheeler term, it was dominated by the mistake of promising to raise the OCR a lot, actually raising it by 100 basis points, and then the Bank only slowly and reluctantly having to more than fully reverse itself. Perhaps more seriously still, there has been no apparent effort to position New Zealand for the next recession, when the OCR won’t be starting at 8.25 per cent.

Some of the mistakes the Reserve Bank has made have been in company (other central banks doing similar things). Most haven’t. In some cases, it has been a clear example of the Governor imposing his will on the organisation – those 2003 OCR cuts were over the advice of a majority of OCRAG – but most haven’t. Then again, chief executives shape organisations, recruit people they are comfortable with, and sometimes don’t really welcome the airing of alternative views. I don’t think, with hindsight, the institution’s record has been particularly good – and I say that as someone who was heavily involved, at times at very senior levels, for a long time. Sadly, it doesn’t seem to be improving.

I’m reluctant to try to reach a view on whether, overall, Wheeler has been worse than his two predecessors. After all, the circumstances the three men faced were very different:

- Don Brash was in charge during what we liked to think of as the “heroic” phase, slaying the inflation beast that ravaged New Zealand for the previous 25 years. But, beyond that, he – and we – were learning what it meant to run monetary policy in a low inflation environment. We had few effective yardsticks – although we were probably more reluctant than we should have been to have consulted other countries’ practices and experiences.

- On the other hand, Don presided over monetary policy through probably the most stable period ever in New Zealand’s terms of trade.

- Alan Bollard presided during the most dramatic financial crisis the world had seen for decades – perhaps since 1914. I didn’t agree with all his stances in that time – some he himself changed quite quickly – but in many ways that 18 months or so was his finest hour: the willingness to improvise liquidity policies and to cut the OCR again and again, in large dollops.

- Recessions: Bollard and Brash had to cope with them (ie externally sourced ones – 1991, the Asian crisis, the dot-com bust, and 2008/09). and Wheeler simply hasn’t.

- Different shocks: Brash presided over the period of wrenching fiscal and structural adjustment, which made much of the data harder to read. Bollard presided during a whole new period of persistent and unexpected strength in the terms of trade (we hadn’t paid them much attention until to then) and the Canterbury earthquakes. All three Governors have had to grapple with the toxic mix of population growth and land use regulation spilling into rising trend house prices – but it was the Bollard years that saw the largest, and most widespread, increase in debt/GDP ratios and private sector lending more generally.

- In his early years, Brash had to deal with a severe domestic financial crisis and the aftermath of a very damaging credit, equity and commercial property boom. Neither Bollard (despite the finance companies) nor Wheeler had to face something similar.

But, in many ways, I’d argue that Graeme Wheeler, and the Bank he presides over, have had it relatively easy. Over his period there has been:

- no international recession,

- no major overseas financial crisis (the euro crisis transitioned into chronic state around the time Wheeler took office),

- no deeply dislocative domestic shocks,

- a stable backdrop of global inflation,

And unlike many of his international peers, he has always had total flexibility to adjust the OCR as required (the near-zero bound simply wasn’t an issue) and there were no looming fiscal crises in the background either.

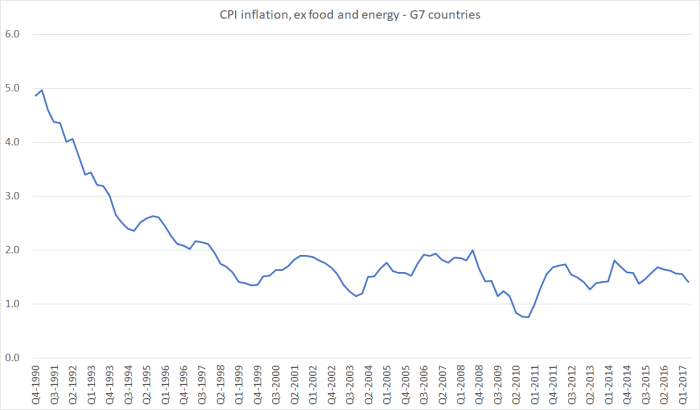

You might be surprised by the comment about stable global inflation. But here is the OECD’s measure of G7 core inflation (ie CPI ex food and energy).

Pretty stable for almost 20 years now. Of course, within that some countries have done better than others. And the interest rates that have been consistent with keeping inflation around these levels have fallen a long way. But there aren’t huge inflationary or deflationary shocks from other advanced economies. Contrast this chart with the New Zealand core inflation chart above. And recall that, unlike New Zealand, most of the G7 countries were pushed to the absolute limits of conventional monetary policy.

It is fair to acknowledge that the recent swings in the terms of trade have been quite large – so I’m not trying to suggest that getting monetary policy just right was easy (if it were that easy, we wouldn’t be paying a lot of people a lot of money to get it right). But broadly speaking, a lot of things have been working in the Reserve Bank’s favour in recent years, that their peers in other countries haven’t had:

- as already mentioned, the Reserve Bank had full OCR flexibility, and

- an unemployment rate persistently above their own estimates of the NAIRU (a basic pointer to a demand shortfall, something conventional monetary policy can remedy),

- high terms of trade (on average), supporting demand overall,

- the effects of Canterbury earthquakes were quite disruptive late in Bollard’s term, but ever since Wheeler took office, they’ve been a consistent source of demand growth [NB I’m not suggesting earthquakes make us richer, but the reconstruction is a significant source of demand – helpful if demand is otherwise scarce.] and

- really rapid population growth (hard to forecast, but persistently surprising on the upside throughout Wheeler’s term – the last quarter of net outflows, seasonally adjusted, ended a few days after he took office), and

- although fiscal policy was net contractionary at the start of his term, even that has swung round to neutral or mildly expansionary more recently.

There is no reason to think it has been any harder to get things right – forecasts and reality – than in the earlier years, and some reasons why it should have been easier to keep inflation up near target.

Non-tradables inflation, the bit the Reserve Bank has most medium-term influence over, should have been relatively easy to get up to levels more consistent with meeting the overall inflation target. And yet, the Bank’s sectoral factor model measure of non-tradables inflation is no higher now than it was when the Governor took office.

Arguments about technological change, structural changes in labour demand, or whatever simply aren’t relevant to this conclusion. They provide opportunities for faster growth without unduly fast inflation – surely, broadly speaking, the goal of economic policy? They provide the oppportunity to run the labour market a bit harder and get more people – often people who find life a bit difficult – into employment. In such a world, one does well – getting inflation back to target – by doing good. Instead, all too often it has come to seem as though the Wheeler Reserve Bank is more concerned about house prices – especially in Auckland – than it is about inflation or unemployment, even though – when pushed – they will acknowledge that monetary policy can’t do much about house prices. And all this with no good model of house prices, and the failures of land use regulation.

So, yes, we’ve had stable (core) inflation in the Wheeler years, but stable at too low a level – in his own words, an “unnecessarily” low levels. He agreed to deliver it higher, and had a lot of things working in his favour to get it higher. He wasn’t faced with rapid productivity growth – driving prices down – rather the contrary. And he was never faced with a fully employed labour market. He simply didn’t do his job, when he easily could have. He seemed to allow himself too readily to believe that somehow he faced the same challenges some of his peers bemoaned at BIS meetings – when the preconditions for rapid (per capita) demand growth, a strong labour market, and inflation around target were much different here.

Would another Governor faced with the same circumstances have done differently in recent years? We can’t really know. There have always been some economists and commentators running a different tack but (a) as far as we can tell, most of the rest of the Reserve Bank senior officials have supported the Governor’s approach, and (b) most domestic market economists have done so most of the time as well. It was the sort of defence we used in the Bollard and Brash years – few ever consistently argued for tougher policy. But it isn’t that persuasive an argument – we charge the Reserve Bank Governor, resource him, and pay him well, to do better.

Where I suspect we can conclude that a different Governor would have done better is in perhaps the more peripheral aspects of monetary policy:

- it is hard to believe that any other Governor would have been so reluctant to acknowledge a mistake. Even if reluctant to accept the fact, most would have found more effective, appealing, lines to use,

- Most possible Governors would have been much more willing to open themselves up to serious scrutiny, especially when questions around performance started arising. Good ones would prove their competence and capability in part by their ability to engage with and deal with alternative perspectives.

- Surely no other possible Governor would have taken the pursuit of Stephen Toplis to quite such lengths. We know other Governors have at times expressed irritation with particular views, but that is very different from deploying your entire senior management team to attempt to close a critic down, and then when that failed writing to Toplis’s employer – an institution the Bank actively regulates – to attempt to have him censored,

- (oh, and other possible Governors probably wouldn’t have attempted to tar publically, in the cool light of day, someone who highlighted a serious weakness in the Bank’s systems).

It is hard not to think that a different Governor wouldn’t have produced stronger speeches – more akin to the quality one finds from Governors in other advanced countries – or demanded, and received, more consistent depth and excellence in the quality of the analytical work underpinning the advice on monetary policy.

I’m not going to conclude that Wheeler did monetary policy worse than his predecessors – and I will be interested to see his own arguments in his forthcoming speech – but even considered in isolation it doesn’t look to have been a creditable record, whether on substance or on style. That is something the Bank’s Board – and whoever might shortly be Minister of Finance – need to reflect on seriously, not just in identifying a specific successor, but in strengthening the institution as a whole.

“…it was the Bollard years that saw the largest, and most widespread, increase in debt/GDP ratios and private sector lending more generally”. I think this might have played on his mind i.e. the BIS ‘financial cycle’ view; hence the LVR controls. Granted, borrowing is not the underlying cause of higher housing prices but the borrowing has added to the upward pressure on prices caused by the underlying supply constraint. And given household debt-to-disposable income ratios have been creeping up during his term, perhaps it became harder to argue this was adding to the resilience of financial system despite the low inflation outcomes. “Dancing between stimulus and stability..” as Mr Lowe just put it….

LikeLike

I updated my spatial economics article with Graeme Wheeler claiming credit for reducing housing inflation from 15% to 1.5% and with an addit at the end on the productivity recession analysis from investor broker -JBWere. Which seems in my mind consistent with the themes Michael informs us on.

View at Medium.com

LikeLike

Sorry but this blog post is amateur hour stuff. You’re poking the borax at Wheeler, rather than providing any cogent analysis. I’d be embarrassed and disappointed if one of my 7th form economic students couldn’t do better.

I don’t have time to write a full critique but here’s one example. You cherry pick a chart of the G7 CPI inflation rate (ex food and energy) and claim that global inflation has been stable. Hmm. Really? Conveniently leave out countries like China, whose export prices have been declining due to substantial over-capacity in manufacturing. And conveniently focus on an irrelevant measure of inflation anyhow. Any half way competent international economist knows that what matters for the transmission of global inflation is not the CPI, but prices for goods and services actually traded across countries. Here the trends look quite different as something like the World Economics Durable Goods Price Index shows (with prices falling since 2011). It is this kind of weakness that the RB is correctly citing, which has weighed heavily on tradables inflation and made its task harder.

Now, I’m not defending the Bank or Wheeler’s performance here – just arguing for robust, rigorous analysis of the sort you keep demanding from the Bank, but don’t seem capable of delivering yourself.

Pretty sloppy. 2/10 or D-.

Rob Ketteridge

LikeLike

I don’t agree with you. My point isn’t that goods prices from eg China haven’t been falling, but that each of those G7 countries have faced the same China shocks, and yet have managed to avoid their overall inflation rate slowing, even though they’ve had problems with interest rates getting to around the zero lower bound. NZ hasn’t, and that is the responsibility of the Reserve Bank – who has had other things a lot easier than most G7 countries’ central banks (the points I listed in the post).

But in your determination to dislike the post, you may not have noticed that in the course of my analysis in many respects I presented Wheeler’s mon pol performance as probably not worse than that of his predecessors – although I’m still reluctant to rank the three, partly because one of those former Governors is a friend. He is more culpable, in my view, on those other behavioural and supporting analyis points I listed (especially given the scale of resources the taxpayer puts at his disposal)/

LikeLike

If I had to rank the performance of the 3 governors.

1.Graeme Wheeler, best performer of the three

2. Don Brash

3. Allan Bollard

It is rather difficult to fault a RB governor that has allowed local companies to grow profitably, business confidence high and a growing economy and therefore as a result returned the governments tax coffers to a growing surplus even with the twin disaster events of Christchurch and Kaikoura. Wheeler has been more willing to reach for macro prudential tools rather than to push interest rates skywards and damaging local industries.

LikeLike