I was recording an interview earlier this afternoon, in which the focus of the questioning was the Real Estate Institute’s call for some easing in the Reserve Bank’s LVR restrictions.

Of course, I never favoured putting the successive waves of LVR restrictions on in the first place. They are discrimatory – across classes of borrowers, classes of borrowing, and classes of lending institutions – they aren’t based on any robust analysis, as a tool to protect the financial system they are inferior to higher capital requirements, they penalise the marginal in favour of the established (or lucky), and generally undermine an efficient and well-functioning housing finance market, for little evident end. Oh, and among types of housing lending, they deliberately carve-out an unrestricted space for the most risky class of housing lending – that on new builds.

That doesn’t mean I think it is remotely likely that the Reserve Bank will be easing the restrictions any time soon – apart from anything else, it would leave their consultation paper on debt to income ratio restrictions looking a little silly. Of course, it would be good if the Reserve Bank did lay out some specific criteria for lifting these ostensibly temporary restrictions, but with the toxic brew of rapid population growth and continuing land use restrictions in place, if I saw the world as they seem to, I wouldn’t be in a hurry to lift the restrictions either.

In any case, it isn’t that clear quite how large a role the LVR restrictions are playing in the reduction in sales volumes. They must be playing a part, but so too will higher interest rates, and the apparent increase in banks’ own lending standards, and pressure through the parents from APRA (on the lending standards across the whole of Australian banking groups). Which, of course, is also why it isn’t clear quite how much difference any easing back in the New Zealand LVR controls might make. Some presumably, but even the Reserve Bank has never claimed that LVR controls would have a very large impact on house prices, or housing market activity, for very long. And while I noticed an article this morning about negative equity, it is worth bearing in mind that, on the REINZ index (not using median prices), house prices have risen 65 per cent in the last five years, and are currently 0.6 per cent off their peak.

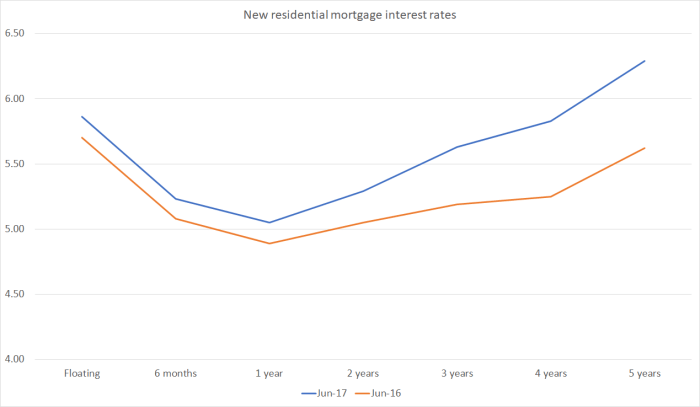

But what of interest rates? A year ago, the OCR was 2.25 per cent, and today it is 1.75 per cent. Thus, the Reserve Bank talks of having eased monetary policy. Here are mortgage rates though.

I don’t suppose anyone is taking out four or five year fixed rate mortgages, but across the entire curve, interest rates are higher not lower. Or we could go back another year or so, to just prior to when the Reserve Bank began cutting the OCR. The OCR has been cut by 175 basis points since then. Even at the shortish end of the mortgage curve, rates are down only 50-70 basis points.

I don’t suppose anyone is taking out four or five year fixed rate mortgages, but across the entire curve, interest rates are higher not lower. Or we could go back another year or so, to just prior to when the Reserve Bank began cutting the OCR. The OCR has been cut by 175 basis points since then. Even at the shortish end of the mortgage curve, rates are down only 50-70 basis points.

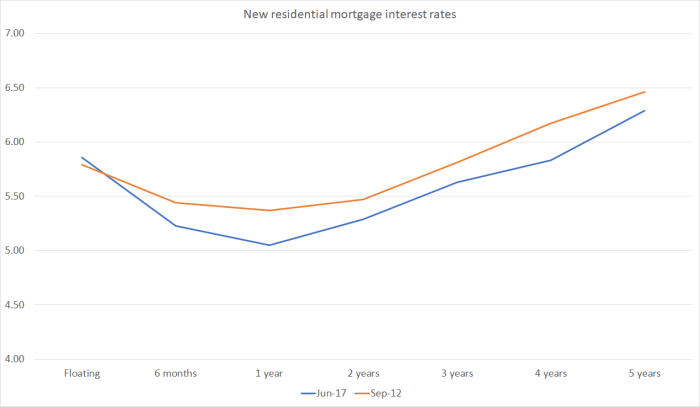

Having been reflecting this morning on Graeme Wheeler’s performance over his term, I had a look back at where interest rates were when Wheeler took office in September 2012.

Barely lower, even though core inflation – on their own favoured measure – is as low today as it was then (and has been consistently low throughout his term).

Barely lower, even though core inflation – on their own favoured measure – is as low today as it was then (and has been consistently low throughout his term).

I wondered if there were offsetting factors but:

- Two year ahead inflation expectations are about 25 basis points lower than they were then (largely offsetting any reductions in nominal mortgage rates, to leave real rates little changed)

- the TWI measure of the exchange rate is a bit higher than it was then,

- the ANZ commodity price index, in inflation-adjusted world price terms, is hardly changed from what it was then.

Of course, the unemployment rate has fallen since September 2012, but there hasn’t been any sign of a pick-up in the best indicator of labour scarcity – real wage inflation.

So, overall, it is a bit of a puzzle how the Governor expected to get core inflation back to fluctuating around the target midpoint without actually easing monetary conditions. I don’t happen to agree with him on this one, but he keeps talking about how the huge migration inflows have reduced net inflation pressures (supply effects outweighing the demand effects). If he really believes that it is even more puzzling that monetary conditions haven’t been eased.

I’m not sure how he’d respond. But perhaps he could explain that too in the forthcoming speech.

It will be interesting to see if we get a speech at all. where or who will he give it to?

Or will it be a press release telling us all we are ninkomputs?

Pleased he is about to leave.

Waiting for the next govt. to find someone who in not a depressed soul but one who see’s the world with brighter eyes.

LikeLike

A thought: can a financing market be efficient and well functioning if the asset it is funding is priced within an inefficient market?

LikeLike

“Australian taxpayers have been subsidising our five major banks since 2008 with government guarantees over bank deposits and a cheap $180 billon debt facility that has put them at a competitive advantage and boosted their earnings.

It was an unprecedented move that changed the nature of the relationship between the Commonwealth and the financial sector and one that would never be extended to any other industry. The guarantee lasted two years, but forever tied our banks to the Commonwealth. As a result, global ratings agencies now consider our banks government-backed.

There is the oligopoly or cartel-like behaviour of the major banks, which, between them, control about 80 per cent of the Australian mortgage market, the engine for their world-beating returns.”

http://www.abc.net.au/news/story-streams/federal-budget-2017/2017-05-15/why-scott-morrisons-bank-levy-doesnt-go-far-enough/8525620

Similarly, New Zealanders are being subjected to monopoly interest rates and fees. This monopoly behavious is costing New Zealanders and the RBNZ is aiding and abetting banks with the 40% equity LVR rtules making extremely difficult to change banks. HSBC is still offering 4.09% 18 months fixed but it is far too difficult to change banks to take advantage of these lower interest rates.

LikeLike

Interesting question, but on reflection “why not?”. From a bankers’ (and borrowers) perspective, the regulatory mess is what it is, and that is a risk that just has to be allowed for and priced. Perhaps it adds an extra layer of risk – but if so, it probably means less credit is voluntarily provided (perhaps relative to the value of the asset) than would be in a properly functioning urban land market. And banks (and borrowers) seem to have done a reasonable job over decades of distorted house prices – the US can be seen as an exception of course, but the US has a housing finance market where govts have been active players encouraging, and indeed compellling, lenders to take on more risk than they would have done themselves.

LikeLiked by 1 person

Agree with you again Mike.

I am sure we (New Zealanders ) used to be told by the banks ,that mortgage rates would be about 2 per cent above the OCR.

It is a crazy mix of financial issues around the globe and I don’t think anyone knows what to do.

LikeLike

Interest rates are currently 4% above the OCR on floating interest rates which is way beyond any New Zelanders expectations.

LikeLike

….might be of interest:

Click to access qb100301.pdf

LikeLike

Useful link on how to think about this issue.

At an even simpler level, consider the margin between the RB’s series of new floating mortgage interest rates and the six month term deposit rate. Over the last 25 years the average margin has been 227bps. The current margin is 254 bps, and the standard deviation in that series has been 40 bps. In other words, current mortgages rates are pretty much as one might expect given funding costs.

LikeLike