Or so it would seem from looking at the forecast tables accompanying today’s PREFU.

Recall that the government has long had a goal of materially increasing the share of New Zealand’s GDP accounted for by exports (with, presumably, a more or less matching increase in imports). As I’ve highlighted on various occasions – yesterday most recently – if anything the actual export share of GDP has been shrinking.

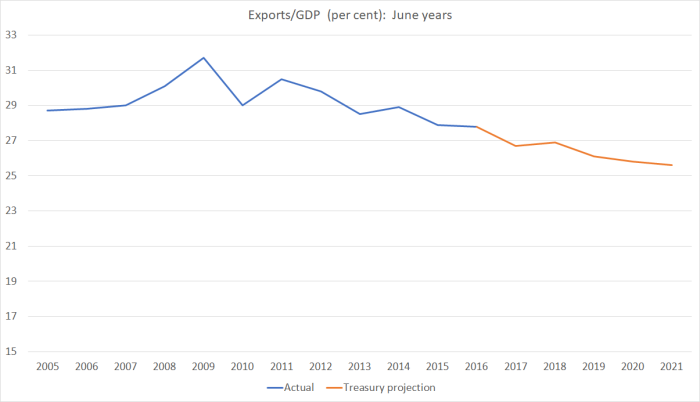

Here is the share of exports in GDP, showing actuals for the last decade or so, and Treasury’s projections for the next few years.

By the end of that forecast period, there will only be four more years until the goal of a much-increased export share of GDP was to be met. On these numbers, exports as a share of GDP would by then be at their lowest since 1989, 32 years earlier. So much for a more open globalising economy.

(The government actually specifies their target as the ratio of real exports to real GDP, while this chart is nominal exports to nominal GDP. Statisticians generally advise against using the real formulation. But on this occasion, it doesn’t make much difference either way. Over the five forecast years, the volume of exports is forecast to rise by 10.8 per cent, and real GDP is forecast to rise by 15.6 per cent. Whichever way you look at it, The Treasury expects the export share of the economy to carry on shrinking over the next few years.)

In many respects that isn’t very surprising. Treasury expects no fall in the exchange rate at all over the period, and they expect rapid increases in the OCR from around the end of next year. And they expect continued rapid population growth.

It is a non-tradables skewed economy, and while there is nothing intrinsically wrong with non-tradables, it isn’t usually a successful path for countries seeking to achieve higher productivity and sustained national prosperity. (Although Treasury does forecast that six years of zero productivity growth will finally come to an end, and we’ll have respectable productivity growth from 2019 onwards. What this is based on, who knows. We can hope I suppose.)

I think that Treasury has finally realised that the $15 billion Tourism and International Students as an export revenue is a very different animal from most industrial or manufacturing type export businesses. As I have pointed out several times already is that the Tourism and the International Student export revenue has almost a 100% flow on and conversion into the local domestic economy compared to most other types of export industries including the dairy milk industry is that only around 30% of that export revenue actually flows back to the local domestic economy.

Due to this almost 100% flow from export revenue to domestic revenue and the tourism and international export revenue continue to grow then we should expect the domestic economy to continue to grow as fast if not faster than the export economy. Its also called economics 101.

LikeLiked by 1 person

…..just wondering if the fixation on reducing net debt is the fiscal equivalent of being an “inflation nutter”; relatively speaking, NZ is in a decent debt position; are there any examples of counties that borrow to invest in projects which are assumed to underpin long term growth? e.g. some kind of ‘infrastructure council’; the assumed fall in residential investment growth is disheartening.

LikeLike

the operative word there might be “assumed”! democracies don;t have a great track record for doing govt capex well. my sense is that we are already doing projects that won’t pass any decent cost-benefit analysis – Transmission Gully is one example, but I suspect there are several in the list of roads the govt announced the otherday.

with proper net debt already below 10% of GDP, personally I’d have no real problem with the govt running modest deficits from here – not large, but just as the sort of level that stabilises net debt around here in future. I’d mainly use the freed-up money to lower business taxes, reinforced by acting on NZS which would free up money for other areas that look as tho they need more current spending.

LikeLike

“…and they expect rapid increases in the OCR from around the end of next year.”

Why? Is the CPI also forecast to be on the rise? Or are they assuming something else will change current trends/settings?

LikeLike

I’m not entirely sure, altho by then the unemployment rate is down to their estimate of the NAIRU (something like 4.25%). I suspect there is quite an element of “we think the neutral interest rate is around 4% and sooner or later we have to get back there”. Their answer would be more sophisticated, but probably boils down to much the same thing – they, in effect, think current interest rates are quite stimulatory.

LikeLike

Gosh, that’s a very big call on their part. My initial thought about TSYs general theme of ‘we’re slowing/going backwards from here on in’ might more have had to do with an attempt to cool the pork barrel prospects.

The description of the “one-off” better corporate results being the NZSF and the banks tax returns being up – but that was not to be repeated/expected in outyears is also a really interesting call. Point is, why might the banks profitability decline (given we’ve been having record after record recently) and are they predicting a dramatic stock market decline with respect to NZSF investments?

LikeLike

I think the prediction would be around the next 6 years that robots would start displacing humans on a much larger scale even in the service sector. Robots are relatively expensive for the service industry at the moment due to the abundance of cheap migrant labour. But increasing minimum wages would make robots more viable as an alternative and as adoption escalates the cost to manufacture robots starts falling then we would have a cascading effect where robots completely displace humans. Treasury predictions of increasing productivity after 6 years seem aligned with AI robot tech displacements forecasts.

LikeLike

But will automation result in “rapid increases in the OCR” by the end of next year, alongside bank profits eroding and an equities market downturn over the forecast period? As these all seem to be elements of their near term (4 year) forecast (from the news heading reporting of the document’s forecast findings, that is).

Which leaves me to suspect they were more erring on a political motivation to prevent a repeat of this sort of thing;

http://www.radionz.co.nz/national/programmes/afternoons/audio/201851773/the-history-of-election-bribes-in-nz

LikeLike

All the headlines including arguments between the RBNZ and banks economists indicate that the official view is that inflation continues to be below the 2% midpoint and would be headed back towards the 1% lower end of the mandated benchmark by the end of next year. With net migrant numbers still hovering around another record 72,400 and an abundance of low cost migrant workers, Oil prices still threatening falling further and there is clearly still a global oversupply production capacity it is difficult to see where inflation would come from at least over the next 2 to 5 years.

LikeLike

Yeah, well that would be my forecast as well – and the FIRE sector seems to do just fine based on those conditions.

LikeLike