It has been a quite remarkable rookie error by the Labour Party that allowed the mere possibility of specific tax increases to become such a major part of the election campaign, in a climate where the government’s debt is very low, and where official forecasts show surpluses projected for years to come. If government finances were showing large deficits, and there was a desperate need to close them, that political pressure might have been unavoidable. Closing big deficits involves governments taking money off people who currently have it – by whatever mix of spending cuts or tax increases – and doing so in large amounts. But the PREFU had growing surpluses, and Labour’s fiscal plan had almost identical surpluses for the next few years – without relying on any further tax changes that might have flowed from the recommendations of the proposed Tax Working Group.

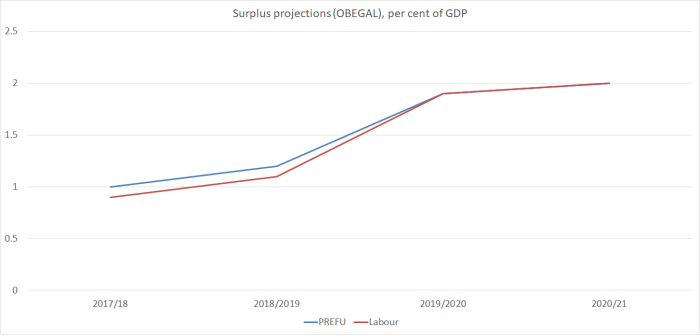

These are the surplus projections

Of course, Treasury GDP forecasts can’t always be counted on – and it is seven years now since the last recession – but there is quite a large buffer in those numbers even if the economic outlook changes. But the other side of politics wasn’t disputing the (Treasury) GDP assumptions. And it seems to have been lost sight of that in a growing economy, with low and stable debt levels, modest deficits (on average) are the steady-state outcome (consistent with low stable debt). That might involve decent surpluses in boom years, and perhaps quite big deficits in recession years (as the automatic stabilisers work on both sides) – but again the Treasury numbers, which both sides are basing their numbers on, say that at present we are in the middle (estimated output gap around zero, unemployment still a bit above a NAIRU, and on the other hand the terms of trade above average).

I guess it was always the sort of risk Labour faced in changing their leader so close to the election (things move fast and something – who knew what specifically – was almost bound to not work out well), but it was all so easily avoidable. They could have:

- stuck with the Andrew Little policy (now reverted to) of no changes flowing out of the TWG process to come into effect before the 2020 election,

- they could have reverted to the 2014 policy (a specific detailed capital gains tax proposal, perhaps including revenue estimates), or

- they could have committed to any package of TWG-inspired changes implemented before the next election being at least revenue neutral (if not revenue negative). This latter sort of commitment would have been easy to make precisely because of the large surpluses in the projections both sides are using (see chart above).

After weeks of contention and uncertainty – some reasonable, some just fear-mongering – they’ve finally adopted the first option.

But you have to wonder what the proposed Tax Working Group will be left to do? In practice, it looks as though it might most usefully be described as a capital gains tax advisory group – to advise on the practical options and details on how to make a capital gains tax work, as well perhaps as to review the evidence and arguments for (and against) such an extension to our tax system (my reflections on the CGT option are here).

They’ve ruled out increases in personal or company tax rates, they’ve ruled out GST increases, and they’ve ruled out a land tax affecting the land under “the family home” (which is most of the value of land in New Zealand). They apparently haven’t ruled out revenue-neutral packages that involve a reduction in income tax rates, but this looks like a pretty empty suggestion. Why?

The first reason is that they claim that their suite of policies are going to solve the housing crisis. I’m a bit sceptical about their claims (and those of the government), but if they are right, how much revenue do they suppose there is likely to be from a capital gains tax anytime in (say) the next 20 years? Treasury once produced some rather large revenue estimates, but (from memory) they involved some sort of muted extrapolation of the experience of the previous 20 years. Both sides of politics seem to think they can stabilise nominal house prices, and then let income growth and inflation reduce real prices and price to income ratios. If so, there are no systematic capital gains on housing – and idiosyncratic ones (particular cities or specific locations that do well) won’t add to much revenue at all. Of course, it might be different if the housing measures fail, but Grant Robertson yesterday seemed pretty adamant.

“What we are signalling is, the Labour Party’s policy is that our focus is on fixing the housing crisis. That is our focus.

A capital gains tax might (or might not) be a sensible addition to the tax system, but it shouldn’t raise much money.

What else is there? I’m sure tax experts have various small things they’d like the working group to look at, but it is hard to believe there is anything that could raise much revenue. For some, a land tax looked promising – my own scepticism is here. But Labour has now ruled out a tax on the land under “the family home”, which effectively nullifies any possibility of a sensible, credible, and enduring land tax.

It is one thing to rule the family home out of a capital gains tax net. Even for most of those left liable for capital gains tax (CGT), the effective liability can be deferred for many years (reducing the present value) simply by not realising the gain (not selling the asset). That is even more true with the sort of institutional holders than many seem keen to encourage into the rental market. And, of course, there is only a liability if prices actually go up. Those are among the reasons why the overseas literature tends to find little evidence that a CGT would make much useful difference to the housing market.

A land tax would be different. It is a liability year in, year out. Owner-occupiers (and associated trusts etc) wouldn’t pay it, but everyone else would. It would be a huge change in the effective cost of (say) providing rental services.

New Zealand real interest rates are the highest in the advanced world. A very long-term real government bond rate is around 2.5 per cent at present (the real OCR is currently zero or slightly negative). So suppose a government imposed a 1 per cent per annum land tax on land not under owner-occupied dwellings. Relative to a risk-free rate of, at most, 2.5 per cent that would be a huge impost (40 per cent of the implied safe earnings of the asset – the appropriate benchmark since the tax itself isn’t risk-dependent.) It would dramatically lower how much any bidder who wasn’t planning to live on the land could afford to pay for the land – by perhaps as much as 40 per cent.

That might sound quite appealing. Rental property owners (actual and potential) drop out of the market and land (and house+land) prices plummet. But wait. Wasn’t the political promise that they weren’t trying to cut existing house prices? And what about the people who – because of youth, or desire for mobility – don’t want to own a house and positively prefer, for time being at least, to rent. And what about farmers? Lifestyle blocks (presumably exempt from the land tax) instantly become much more affordable than farming (which presumably does face the tax). To what social or economic end?

Attempt to impose such a land tax and my prediction would be (a) that it would never pass, since it would represent such a heavy impost on a large number of people (and yet on not enough to raise enough revenue to allow meaningful income tax cuts to offset the effect), and (b) if it did pass, exemptions and carve-outs would quite quickly reduce it to the sort of land tax we actually had in New Zealand only 30 years ago – which only affected city commercial property.

Now perhaps there is a limited middle ground. There is a plausible case that can be made for use of land value rating by local councils rather than the capital value rating system that most councils now use. I’m not aware that we have good studies suggesting better (empirical) outcomes in places that still use land value rating, but the theory is good. The problem, of course, is that by ruling out a land tax on the family home, Labour would appear to have ruled out (say) using legislation to encourage or compel councils to rely more heavily on land value rating. Perhaps that might leave undeveloped land within existing urban areas as potentially subject to land value rating? There might be some merit in that, but the potential seems quite limited.

So, as I say, it looks as though the proposed tax working group should really just be a CGT advisory group.

And that would be a shame because, whatever you think of the merits of a CGT, it isn’t the only issue that would have been worth addressing in a proper review of the design of our tax system. For 30 years now – since what was a fairly cynical revenue grab (recognised at the time by those involved) in 1988/89 – our tax system has systematically penalised returns to savings (both relative to how we treated those returns previously, and relative to how other countries typically treat such returns). The prevailing mantra – broad base low rate – which holds the commanding heights in Wellington sounds good, until one stops to think about it. We have modest rates of national savings, and consistently low rates of business investment – and our productivity languishes – and yet the relevant elites continue to think it makes sense to tax capital income as heavily as labour income. It doesn’t, whether in theory or in practice. They don’t, for example, in social democratic Scandinavia. They don’t – when it comes to returns to financial savings – almost anywhere else in the advanced world. We should be looking carefully at options like a Nordic system, a progressive consumption tax, at inflation-indexing the tax treatment of interest, and at whether interest should be taxed (or deductible) at all.

Plenty of people are worrying about the potentially radical nature of some aspects of a possible new left-wing government. I come from the market-oriented right on matters economic, but I worry that in these areas they won’t be radical enough – won’t even be willing to open up the serious issues that might be contributing to our sustained economic underperformance. And frankly, when the debt levels are as low as they now, and sustained surpluses appear to be in prospect, if ever there is a time to look at more serious structural reforms it is now. It is a great deal easier to do tax reform when any changes can be revenue-negative (actually the approach taken by the current government in 2010 – see table of static estimates here) or (depending on your orientation) used to increase public spending. But it looks as though another opportunity is going to be let go by. That would be a shame.

(Having mentioned the 2010 package in passing, I am a little surprised that the increase in the effective rate of business taxation in that package doesn’t get more attention. It often passes unnoticed because the headline company tax rate was reduced, but as the published Treasury assessment at the time put it

While the tax package lowers the company tax rate, changes to thin capitalisation rules and depreciation allowances mean that, on average, firms will pay more tax as the reduction in the company tax rate does not fully offset the impact of higher taxable income owing to the base-broadening measures. As a result combined company and dividend tax revenues are estimated to be about 3-4% higher than in the absence of the package. In the case where all investment is financed by equity, this could increase the user cost of capital by about 0.6%.

Using the New Zealand Treasury Model (NZTM) we estimate that the increase in the user cost of capital leads to the private business capital stock reducing by 0.45% compared to what would have been the case in the absence of the package.

Not obviously a desirable outcome for an economy that had, for decades, had low levels of business investment.)

And finally, a chart showing in just what good shape New Zealand public finances are relative to those in the rest of the advanced world. New Zealand government debt has increased relative to GDP under the term of the current government (mostly some mix of a recession and earthquakes), but government debt as a share of GDP has increased in most other countries too. Here is the gap between New Zealand and the median OECD country, using the OECD’s series of general government net financial liabilities. Our net financial liabilities last year were around 5 per cent of GDP on this measure (seven OECD countries have less net debt, or have net assets). The median OECD country has net financial liabilities of 40 per cent of GDP. But here is the gap, going back to 1993 when the data commence for New Zealand.

It is quite a striking chart – and took me a little by surprise frankly. If you didn’t know when the two changes of government had occurred, there would be no hint in this chart. For almost 25 years now we’ve kept on lowering our net debt relative to that of other OECD countries, through good times (for them and us) and for tougher times, under National governments and Labour ones. There just isn’t any obvious break in the series. And as we have a lot fewer off-balance sheet liabilities (eg public service pension commitments) the actual position is even more favourable than suggested here.

I’m not a big fan of increasing government debt as a share of GDP – and low as current interest rates are (a) productivity growth is lower still, and (b) our interest rates are still the highest around. But you do have to wonder quite what analysis backs up the drive for still lower rates of government debt to GDP, absolutely and relative to the rest of the advanced world. And persisting with the “big New Zealand” strategy of rapid population growth makes the emphasis on very low levels of government debt even more difficult to make much rational sense of.