The possible new fiscal institution first, and them some comments on some of the numbers.

It was interesting to see the joint statement from James Shaw and Grant Robertson that the government is looking to move ahead with some sort of independent fiscal institution. This had been a Greens cause more than a Labour one – former leader Metiria Turei had openly called for a new body – and although the pledge had formed part of the pre-election Budget Responsibility Rules, I’d been beginning to wonder whether the government would follow through. After all, Treasury has never been keen on a potential alternative source of fiscal advice/analysis, even though the independent review of their fiscal advice and analysis a few years ago by the former head of the IMF Fiscal Affairs Department had been positive on the idea that New Zealand establish a Fiscal Council (and the OECD had also recommended it).

There were few specifics in yesterday’s statement

Public consultation will be launched in August on establishing an independent body to better inform public debate in our democracy, Associate Finance Minister James Shaw announced today.

“We are pleased to take forward a Green Party idea developed before the last election to see a body formed which could provide all political parties with independent, non-partisan costings on their policies,” says James Shaw.

“That way we can reduce political point-scoring and attempts to create unreasonable doubt about a party’s policy figures. That will mean better debate about the ideas being put forward.

“We are proposing a new institution independent of Ministers that would provide the public with an assessment of government forecasts and cost political parties’ policies,” says Grant Robertson.

“This independent fiscal institution (IFI) would crunch the numbers on political parties’ election policies in a credible and consistent way,” says James Shaw.

Indeed, the statement is a reminder that there are two very different roles being discussed here:

- costing political parties’ election promises, and

- monitoring and assessing government (Treasury surely?) fiscal forecasts, and perhaps government fiscal strategy.

As I’ve written previously, I am generally positive on the second of those roles, but am sceptical of the former. Notwithstanding last year’s debates about “fiscal holes”, I don’t see a gap in the market (after all, surely “pointscoring” is part of the point of election campaigns?), and I suspect any such costings office would tend to become an additional research service for small parties (the Australian office seems to have been used mainly by the Greens), and not much used either by the main parties (with more resources, including in the form of supporters’ own expertise), or by any right-wing parties (given the social democratic leanings of those likely to be doing this sort of work, probably on rotation or secondment from The Treasury).

Of the second leg, these were some of my earlier comments

A Fiscal Council seems more likely to add value if it is positioned (normally) at one remove from the detailed forecasting business, offering advice and analysis on the fiscal rules themselves (design and implementation) and how best to think about the appropriate fiscal policy rules. The Council might also, for example, be able to provide some useful advice on what material might usefully be included in the PREFU (before the election, I noted that routine publication of a baseline scenario that projected expenditure using the inflation and population pressures used in the Treasury economic forecasts would be a helpful step forward).

There is unlikely to be a simple-to-replicate off-the-shelf model that can quickly be adopted here, and some work will be needed on devising a cost-effective sustainable model, relevant to New Zealand’s specific circumstances. That is partly about the details of the legislation (mandate, resourcing etc), but also partly about identifying the right sort of mix of people – some mix of specific professional expertise, an independent cast of mind, communications skills, and so on. A useful Fiscal Council won’t be constantly disagreeing with Treasury or the Minister of Finance (but won’t be afraid to do so when required), but will be bringing different perspectives to bear on the issues, to inform a better quality independent debate on fiscal issues.

I hope to offer some more-detailed thoughts when the public consultation phase of the policy development occurs. In the meantime, I’d continue to urge ministers (and Treasury) to think about broadening the ambit of any new council, to include external monitoring analysis of monetary policy and perhaps the other responsibilities of the Reserve Bank.

…it wouldn’t be about second-guessing individual OCR decisions or specific sets of forecasts, but offering perspectives on the framework and rules, and some periodic ex-post assessment. In a small country, it would also have the appeal of offering some critical mass to any new Council.

What of this year’s numbers?

I’m not someone who champions big government. In fact, I think we could do the things the state should be doing, and do them well – better than they are being done now – with a smaller share of GDP devoted to government spending.

But as outside observer of left-wing politics in government, I continue to find charts like this a bit surprising.

Not only is government spending over the next four fiscal years planned/projected to be a smaller share of GDP than in the last four years under the previous government, but that government spending share averages less than in every single year of the Clark/Cullen government. In the interim, nothing has been done to raise the NZS eligibility age, so that that particular fiscal outlay is becoming more burdensome every year. And all the campaign rhetoric – and actually the rhetoric in government – is about rebuilds, past underfunding etc etc. Something doesn’t seem to add up. I suspect, as I’ve argued previously, that the aggregate spending line can’t, and won’t, be held over the next few years.

And you will recall that the Labour-Greens pledge around government spending was (as it first appeared last May)

4. The Government will take a prudent approach to ensure expenditure is phased, controlled, and directed to maximise its benefits. The Government will maintain its expenditure to within the recent historical range of spending to GDP ratio.

During the global financial crisis Core Crown spending rose to 34% of GDP. However, for the last 20 years, Core Crown spending has been around 30% of GDP and we will manage our expenditure carefully to continue this trend.

In the separate release on the rules yesterday, that second paragraph now reads

Core Crown spending has averaged around 30% of GDP for the past 20 years. The Treasury forecasts show we are staying below this – peaking at 28.5% of GDP in 2018/19.

It is as if 30 per cent has become a ceiling – staying below it a badge of honour for the government – rather than something to fluctuate around.

Perhaps the Minister would defend himself by noting that over the forecast period the economy is running at capacity, and he needs to allow for the inevitable next recession at some point. But with planned spending averaging 28.5 per cent of forecast GDP, it would take an unexpected 8 per cent fall in nominal GDP (relative to the current forecast path), with no change at all in government spending (say, wage settlements being lower etc) for government spending to equal 31 per cent of GDP, even in a single year in the depths of such a recession. And even 31 per cent wouldn’t be out of the recent historical range of the spending to GDP ratio. Again, relative to the political rhetoric, something doesn’t compute.

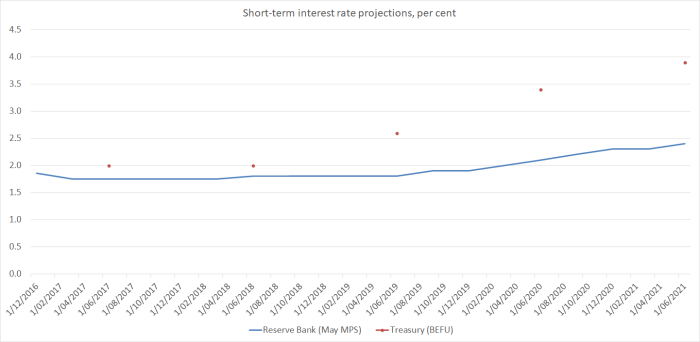

There are also some puzzling things in the Treasury macro forecasts – which are Treasury’s responsibility, not that of the Minister of Finance. Here is the difference in the interest rate projections of the Reserve Bank and The Treasury. The Bank forecasts the OCR directly, while The Treasury forecasts the 90 day bill rate, but you can easily see the difference.

Only last week, the new Governor (over)confidently told us that official interest rates “will” remain on hold for some time to come. The Treasury clearly doesn’t believe him, reckoning that by this time next year we’ll already have had 50 to 75 basis points on OCR increases, with lots more increases in the following two years.

Even though I think the Governor was expressing himself too strongly, I just don’t believe the Treasury numbers at all. They imply a lot of pent-up inflation pressures building up now that can only be nipped in the bud if the Bank gets on with the job and tightens policy. And yet, on Treasury’s own numbers, the output gap has increased from around -1.5 per cent of GDP (for several years) to around zero now, and there has been only a very modest increase in core inflation. It is hard to see how the quite small projected increase in capacity pressures will now finally get core inflation back to 2 per cent – requiring quite a lift in the inflation rate from here – and how those pressures are likely to appear if people really thought such a significant tightening of the OCR was in prospect. As it is, on these Treasury numbers, it is another three years until inflation gts back to 2 per cent. That is even slower than in the Reserve Bank projections.

Also a bit sobering were the Treasury export forecasts. From time to time the government talks – as its predecessor did – about lifting exports (and imports presumably) as part of a successful reorientation of the economy. Treasury clearly doesn’t believe that any such reorientation is underway.

Just some more of the same dismal picture. But I guess that is what one would expect when the two parties just keep on with much the same policies that got us where we are today, with the economy less open (as measured by trade shares) than it was averaging 25 years ago).

I mentioned earlier the uncertain timing of the next recession. If the Treasury projections come to pass we’ll have gone 12 years (since the 2010 double-dip recession) without a recession. That is possible, but it probably isn’t an outcome people should be planning on. I noticed last night this chart from a recent survey of US fund managers.

Quite possibly, like economists, fund managers picked six of the last three recessions. Nonetheless, it is a salutary reminder of where things can go wrong. For example:

- The Fed could end up overtightening (often a contributor to past downturns),

- Emerging market stresses (eg Turkey and Argentina) could foreshadow something more widespreads,

- Economic data in the euro-area seems to be weakening, and the likely new Italian government doesn’t look like a force to increase confidence and resilience in the euro,

- and of the course there are risks around China, and in the Middle East – trade wars and other aspects of geopolitics.

Nearer to home, some straws in the wind are also starting to pile up.

I don’t do medium-term economic forecasts – nor does any wise person – but with the terms of trade assumed to hold at near-record highs, there is a sense that the macro picture the government is using, and selling, is a little too good to last. In that respect – but probably only – it is eerily reminiscent of the start of 2008 when The Treasury revised its advice and confirmed to the then government of the day that it thought the higher revenue levels were likely to be permanent. Little did they realise…….

Of course, our government debt levels are very low – net debt is only 7.3 per cent of GDP – so these risks aren’t some sort of existential threat (although any new global downturn will greatly exacerbate fiscal problems elsewhere, and further constrain policy freedom of action and limit the ability of the advanced world to bounce back quickly). But our authorities do need to be more actively planning for the next downturn: it will come, and when it does it appears that the government and the Reserve Bank have not yet done anything much to assure that they have anything the freedom of monetary policy action we can usually count on. (Perhaps instead of offering his unsolicited thoughts on all and sundry political issues, the Governor could substantively address that issue, which is core to his remit.)

Jacinda Ardern is a liar. She said No New Taxes in her election slogan and we get all these new taxes.

4 new taxes in 6 months of office.

1. Government Fuel Tax

2. Regional Fuel Tax

3. Extension of the Bright Line Test to 5 years

4. On line shopping tax

Under consultation to be implemented.

5. Ring fencing property tax losses

6. Targetted property infrastructure tax

Labour Party slogan should be “Lets Lie to the dumb NZ public and not call a tax a tax.”

LikeLike

Reflecting on your excellent blogs over many months, I wonder whether the low productivity growth but high immigration state of the economy is largely a Ponzi scheme? Successive governments have used total real GDP as the key economic indicator, but as you’ve pointed out on numerous occasions, net population growth (in our case largely from immigration) pretty much inevitably means GDP growth as more people make and use more stuff. Immigration driving this “success” then makes changing immigration policy an approach that places our prosperity at risk, so the government of the day can always look good, and reduce the risk of looking bad, by continuing immigration. In fact the more the better!!

LikeLike

Given that successive RB governors with hawkish interest rates have decimated NZ industries and manufacturing, and NZ economists wrongly identifying primary industries as highly productive industries forgetting to count the 10 million cows, 30 million sheep and 1 million deer and goats we have ended up heavily subsidising primary industries at the expense of not providing incubation subsidies for new manufacturing in new technologies. Relegating to a quick fix, John Key as tourism minister led the charge on tourism to drag a languishing economy in recession to 3% surpluses. Tourism is a service industry which require low skilled labour and as a.result boosting the need to feed, house and provide entertainment driving the need for higher and higher immigration as kiwis highly qualified prefer larger economies and shift to Australia, US and Canada that actually still do make things.

The current government has revived research tax credits but these are tiny sums of millions rather than the billions that will go towards subsidies on roading, irrigation and transportation. Even the the rail network is mainly intended to move tourists around Auckland, mainly trying to get the 19 million inbound and outbound passengers out of Auckland airport.

LikeLike