When Parliament legislated to require the Reserve Bank to publish six-monthly Financial Stability Reports this is what they said in the two relevant clauses

162AA Purpose of accountability documents

The purpose of the 3 accountability documents required under this Part is as follows:…..

(c)financial stability report: to—

(i) report on matters relating to the soundness and efficiency of the financial system and other matters associated with the Bank’s statutory prudential purposes; and

(ii) allow assessments to be made of the effectiveness of the Bank’s use of its powers to achieve its statutory prudential purposes.

165A Financial stability reports

……(2) A financial stability report must—

(a) report on the soundness and efficiency of the financial system and other matters associated with the Bank’s statutory prudential purposes; and

(b) contain the information necessary to allow an assessment to be made of the activities undertaken by the Bank to achieve its statutory prudential purposes under this Act and any other enactment.

Financial Stability Reports over the years seem to do a passable job of reportage – a collection of sometimes-interesting charts and some text recounting (although only rarely analysing, or putting in context) what has been going on on the financing side of the New Zealand economy. There are usually some fairly perfunctory updates on policy issues the Bank is considering.

But what is very rarely there is the sort of information that would enable us to really assess the Bank’s use of its powers and the conduct of policy under the various relevant acts. There is never any critical self-scrutiny; it is as if the Bank thought itself beyond error.

Of course, supply tends to respond to demand. There is little searching scrutiny of the Reserve Bank at the Finance and Expenditure Committee, and not much more from the media (the level of questioning at the Governor’s press conference this morning seemed weaker than usual).

What do I have in mind about weaknesses in today’s document?

Remarkably, there is no substantive discussion in today’s Financial Stability Report of CBL, the insurance company, regulated by the Reserve Bank, that the Bank petitioned to have put into interim liquidation earlier in the year. I’m not aware of any reason to think the Reserve Bank acted inappropriately in this matter, but it is a fairly significant institutional failure (on the Bank’s watch), and a fairly significant set of regulatory actions, including the (at least somewhat questionable) use of gagging orders to prevent the company telling its own shareholders and customers about regulatory interventions. Then again, remarkably no journalist asked a single question on this topic.

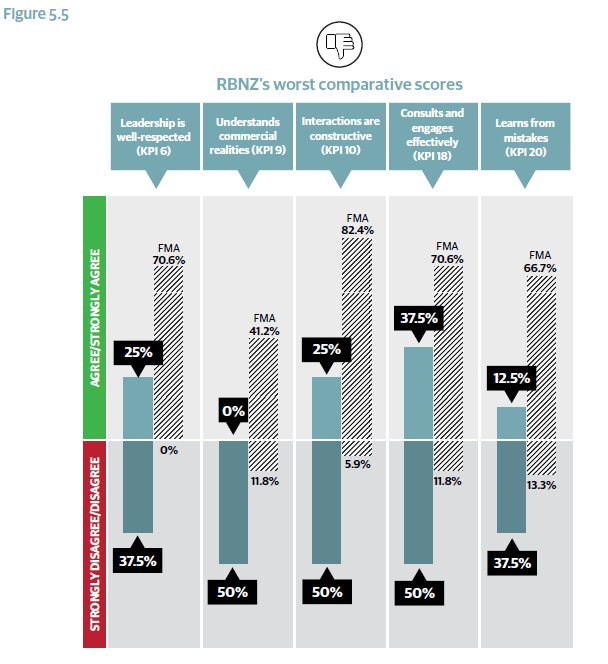

Readers will also recall the scathing feedback on the Bank’s prudential regulatory side in the recent New Zealand Initiative report, and survey of regulated entities. There was, for example, this chart, comparing Reserve Bank and FMA results for the KPIs where the Reserve Bank scores worst in the survey.

This report had come out since the last FSR. In a newspaper interview a while ago, the Governor had appeared to indicate that he was going to take it seriously, with comments like these

“This place is a diamond, but it needs significant polishing in places,” Orr said in an interview in the Reserve Bank headquarters.

“We need to think much harder about how we behave, how we roll, how we explain, how we do things. That’s a cultural challenge for the bank.”

and

As well as posting the comments of the report on the Reserve Bank’s internal intranet, Orr had written to bank bosses with the message that: “Hey, this doesn’t print well. We hear you. We need to do something about it.”

Interestingly, he actually talked then of problems in the Bank’s own culture. But in his main accountability document for the financial regulatory functions, there was no reference to the survey, no comment on cultural issues at the Bank (all while continuing to bash banks), no comment on improving the Bank’s own performance, no nothing.

And, remarkably, the Governor faced no questions on the matter, even though the survey had almost handed them the data with which to grill the Governor. Perhaps the journalists have forgotten, but the counterpart to the delegation of extensive powers to unelected officials has to be serious scrutiny and accountability. There appears to be almost none here.

Similarly – and somewhat remarkably – the Governor managed to avoid any questions about his “culture war” by noting that he and the FMA would be appearing before a select committee this afternoon, and suggesting deferrring questions. But I don’t suppose he will be holding a press conference after that appearance, and questions from MPs are likely to be as weak as ever, more interested in associating with the Governor than in holding him to account.

And this failure to ask questions was perhaps more remarkable given that the press release the Governor put out with the FSR bears the heading “Banking culture in the spotlight”. Reading that headline one might have expected a substantive treatment, but in the press release there was just the unsubstantiated claim that “an ongoing driver of financial soundness is the conduct and culture of banks”. To which one can only respond, well yes loans that turn bad tend, in sufficient volume, to be what brings down banks, but misjudgements about big picture credit quality, and the overoptimism that takes hold (of bankers and regulators) in boomtimes, aren’t the sort of stuff the Australian Royal Commission – which the Governor always tries to associate with – is about. Here is what he had to say about that (cutesy picture and all)

Quite how evidence in an inquiry which has not yet reported can really illustrate anything conclusive – let alone the connection to the soundness of the financial system – is a bit beyond me. The Governor seems more keen on his populism, and on associating himself with a highly political Australian inquiry, than on actually identifying specific reasons for concern here. Perhaps he will explain himself this afternoon?

Reverting to other stuff, there was this extraordinary line in the Governor’s press release

The high dairy-farm indebtedness, and the fact that LVRs were necessary, reflects that banks’ allocative efficiency – eg deciding how much to lend to whom – can be impaired due to the pursuit of short-term, rather than longer-term, profits.

It is an almost incoherent sentence. For a start, New Zealand bank loan losses have remained consistently low for several decades now – even the farm losses in the last recession were pretty modest in the scheme of things. Secondly, you can’t argue – as a regulator – that the fact you acted (in this case imposing LVRs) is evidence of a problem. There might – as I would argue – have been no need for LVR controls in the first place – after all, the Bank’s stress test results have consistently highlighted the resilience of New Zealand banks, and of the system as a whole. And thirdly, if even there were to be a large stock of troubled lending that would not, of itself, suggest some systematic flaw n the way banks were allocating credit. None of us – not banks, not central banks – operate in a full information world. Sometimes, events will turn out differently than either lenders or borrowers expected. That isn’t an indication of any sort of structural failing. We might reasonably expect rather more substantive analysis before the Governor starts impugning the business decisions of private companies. but……there was nothing else in the report to back up his claims. (And no cognisance of regulator failure either.)

Somewhat related to this was the pretty unsatisfactory discussion of the housing market, both in the document and the press conference. The Bank consistently fails to recognise that land use regulation is the key factor explaining the high level of house and urban land prices: against that backdrop, bank lending practices are likely to be of little more than marginal importance. Thus, they talk like this

But they never once recognise that if the mix of regulatory and population pressures keeps making land artificially scarce, high levels of bank credit are just necessary to accommodate people getting into the increasingly high-priced market. In that case, credit is at worst a lubricant, a facilitator, but not either the cause or the real problem. (The Bank might want to argue differently, but if so surely they owe us rather better and deeper analysis.)

There were a couple of interesting snippets in the report. The smaller one was this comment on the next stage of the review of the Reserve Bank Act

Both the Reserve Bank and the Treasury have provided advice to the Minister of Finance on the scope for Phase 2. The terms of reference for Phase 2 will be published by the Government in June. Phase 2 will be a significant undertaking and could take a number of years to complete.

That suggests the untrammelled rule of the Governor alone – in the financial stability area – could continue for some considerable time. That is unfortunate, especially as there is less effective accountability for the Governor around these functions than around monetary policy (where accountability is weak enough). Nonetheless, I will look forward to seeing the announcement in June.

The other interesting snippet was Box C, a report on a benchmarking exercise undertaken in respect of a sample portfolio of dairy loans.

The exercise required the banks to measure the risk of the same portfolio of loans to 20 hypothetical dairy farms. These farms represented a range of characteristics and varying degrees of risk. Banks were then provided with financial data and descriptive information for each farm, as well as the details of the hypothetical loans.

The preliminary results of the exercise indicate significant differences in estimates across banks. The highest and lowest average risk weight for the whole hypothetical portfolio differed by 40 percentage points, leading to differences in the hypothetical capital requirement.

Variation in both PD [probability of default] and LGD [loss given default] was was significant. Figure C1 shows the range of average PD estimates across five groups, each containing four loans, ranging from the group of loans with the lowest estimated PDs to the group with the highest estimated PDs. Each line represents the estimates of one bank, before overrides. Absolute variation was largest at the mid- to high-risk end of the spectrum, but proportionate variation was large across all levels of risk. The model overrides applied by banks tended to reduce the variation across banks, but it remained significant.

These are big differences. The Bank reports that

The provisional results show significant variation in model outcomes, even for the same level of underlying risk. The Reserve Bank is conducting further analysis of banks’ farm lending portfolios to see if patterns in actual risk estimates are consistent with the results of the hypothetical exercise. This work will help inform the Reserve Bank’s review of bank capital requirements.

There are at least two quite different ways of looking at such results. One could treat them as evidence that “banks can’t be trusted” to get these things right, and that the Reserve Bank should just be setting all the key parameters that feed into calculations of capital requirements. But one could also see them as a reminder of the uncertainty of the world in which we live, and that equally intelligent people can at times assess the risks of a particular type of loan quite differently. There is – or should be – information in that difference. That information would be lost if the Reserve Bank was simply imposing its estimates, the more so as there is no particular reason to suppose that Reserve Bank staff are better able to assess risk than employees of an institution that has its own money on the line.

Without consistent evidence that one bank has been better than the others at assessing risks on particular types of loans, the Bank should be hesitant about what it does with the results of such benchmarking exercises. As I’ve argued previously for stress tests, perhaps transparency is the best way forward. Our Reserve Bank – unlike say the Bank of England – doesn’t publish stress test results for individual banks. As the chart above illustrates, it also doesn’t publish information from benchmarking exercises by bank. Perhaps they should.

Overall, it was another Financial Stability Report that – for all the cutesy pictures – fell well short of the level of self-scrutiny and openness that citizens should expect from such a powerful agency (and individual). And the way the Bank completely passed over the very negative detailed feedback it had received only recently on its own performance, suggests that the cultural failures that dogged the Bank during the Wheeler years might be less likely to be seriously addressed under the new Governor than I’d hoped.

For example, if culture and conduct issues really worry the Governor, perhaps he should start closer to home, and demonstrate consistent excellence, transparency, and accountability as a regulator. There is plenty of scope to clean up his own house. Physician heal thyself, and all that (here and here).