A couple of weeks ago I wrote about the government’s consultative document on its proposal to target net-zero emissions by 2050, and particularly the commissioned modelling NZIER had undertaken on the likely consequences of each of several options for future real GDP. As the consultative document itself put it

The analysis by NZIER suggests that GDP will continue to grow but will be in the range of 10 per cent to 22 per cent less in 2050, compared with taking no further action on climate change.

Those are breathtakingly large numbers (future GDP gains) for a government to simply propose walking away from. As one comparison, high end estimates of the GDP gains from preferential trade agreements (such as CPTPP or the proposed new one with the EU) tend to be about 1 per cent each.

A couple of days ago NZIER’s final report itself was released, making it a bit easier to make sense of the reported modelling results. There is a great deal of detail (the report is 90 pages), a considerable number of (necessary and inevitable) caveats, as well as quite a bit of editorial advocacy for their client’s wishes.

The centrepiece remains this table which I ran in the earlier post.

From reading the final report, and a few exchanges with NZIER, they would encourage people to focus on the final three columns. In those scenarios, relative to the baseline (the first column, which is built from The Treasury’s longer-term economic projections/assumptions), the net-zero target sees productivity growth fall quite substantially, such that average annual GDP growth falls by 0.3 percentage points. Over 33 years, that cumulates to a sacrifice of about 10 per cent of GDP (real GDP – per capita, since the population assumptions don’t change – in 2050 is about 10 per cent lower than it otherwise would be). These are serious numbers: 10 per cent of today’s GDP is about $28 billion. And the loss isn’t just for one year. Depending on various possible assumptions, the cumulative loss the next generation would experience could easily be a couple of hundred billion dollars (in today’s dollars).

(Perhaps encouraged by their client) NZIER try to play down these numbers a bit by encouraging people to focus only on the difference between the third to last and last columns. They argue that the 50 per cent net reduction is already government policy, and so the relevant metric is the marginal additional losses from moving to net zero. But, of course, actual policies to deliver the previous government’s own vapourware objective (the 50 per cent reduction by 2050) aren’t in place, and that target itself is not binding in any real sense.

Some readers might think that a 10 per cent loss of future GDP isn’t too bad – big as it is. it certainly isn’t as large as the 22 per cent loss referred to in that quote above.

But the 10 per cent of GDP annual cost by 2050 (the final scenario in the final column of the table) relies on some really rather optimistic assumptions (and assumptions they all are, as is clearly identified in the NZIER report).

First, they assume quite a lot of technological innovation in some sectors that might be most exposed to a higher carbon price. For example, it is assumed that by 2030 methane vaccine is readily available, commercially viable, and widely used, which would reduce methane emissions by 30 per cent. It is also assumed that global demand for dairy and sheep/beef products falls quite substantially (even though, all else equal, this would make New Zealand poorer, it would make farmers more ready to shift away from emitting-animals). It is also assumed that much faster improvements in energy efficiency are achieved and that (without subsidies or regulation) electric vehicles make up 95 per cent all light vehicles on the road in 2050 and 50 per cent of all heavy vehicles.

No doubt a much higher carbon price (globally) would encourage additional R&D in affected sectors, and so some of these innovations may well occur. But in my earlier post, I described these assumptions as assistance from the “magic fairy”, because while it is probably fine to assume that big changes in relative prices, imposed by governments, will foster innovation to economise on what is being taxed more heavily, it is unreasonable to assume – as is done here – no offset in the rest of the economy. On these assumptions (presumably developed jointly by MfE and NZIER) a government-driven huge change in the structure of the economy (driven away from the market baseline) is a net positive source of new economic innovation. It doesn’t seem very likely. It isn’t at all obvious what precedents could be cited in support of such an assumption. On that basis, for example, putting on import licensing and exchange controls after 1938 might have been hugely positive for business innovation in New Zealand. Enthusiasts at the time probably hoped so, but the typical reading of the evidence would suggest not.

In the consultation document these “assume innovation” scenarios were all described solely as technological innovations (as described above – and the text is reproduced in my earlier posts). But what becomes clear, and quite explicit, in the full NZIER report is that much of what is going on in these “assume innovation” scenarios is in fact different assumptions about increased sequestration of emissions by a permanent increase in land used for forestry. The model can’t cope with generating increased afforestation endogenously, and so assumptions have simply had to be imposed.

In the net-zero scenario (far right column), so much additional sequestration is assumed that the authors state that it would require a 140 per cent increase in the land area devoted to forestry (a really big increase, and the baseline presumably includes not just plantation forest but forests in, eg, national parks). The big step up in the assumed forestation between the 75% and net-zero columns is the reason why the GDP growth rates are the same in the two scenarios.

It does seem reasonable to suppose that a much higher carbon price (and in the NZIER modelling, the carbon prices goes very high on some scenarios) there will be changes in land use in favour of forestry. But here again, the magic fairy is at work.

We assume that additional forestry planting does not materially reduce the amount of productive land available for other uses. This could be seen as assuming that additional planting occurs on scrub land, rather than substituting for sheep and beef or dairy land.

If afforestation occurs on productive land, the economic costs of imposing emissions targets will increase, as the productive capacity of the agricultural and horticultural industries will decrease, which will also have negative flow-on effects for downstream primary processing industries.

In other words, NZIER is assuming that a big change in relative prices (the carbon price) makes economic a whole lot of resource that has not hitherto been used for anything much. I’m sure there is such land – a considerable portion probably Maori land, with all the issues around title/collateral that make it difficult to use – but is it reasonable to assume that all, or even most, of the land newly devoted to forests will be land that wasn’t previously being used for anything? Why, for example, wouldn’t one assume that land that has been converted from forestry to dairying in recent decades (eg much between Taupo and Tokoroa, and Taupo and Rotorua) be among the first that would be converted back to forestry? If so, as NZIER acknowledges, there will be additional real economic losses.

As in the Productivity Commission’s draft report, this NZIER modelling makes no allowance for the possibility of a lower population growth rate (by lowering our annual immigration approvals targets). It is quite an extraordinary omission, given the cross-country data I’ve shown previously illustrating (the rather obvious point) that more people tends to mean more emissions. If they are your own people, there isn’t much governments can do about it, but in New Zealand a large (and increasing) part of trend population increase is about discretionary immigration policy.

One would need to have NZIER rerun their models to get really good estimates (and since they ran and published sensitivities on a variety of other alternative assumptions, there is no good reason not to have done so as regards population growth – although no doubt to have done so would have been unwelcome at MfE and in the Minister’s office). But since the increased afforestation assumptions are a bit like a free lunch (raise the carbon price, and a whole lot of previously unused land is brought into play, sequestering carbon emissions), one can get a sense of what a difference a similar free lunch assumption might make. Lowering the projected population growth by 0.7 per cent per annum (the difference lowering residence approvals from 45000 to 15000 per annum would make) would reduce expected future emissions enormously, without needing the see the carbon price driven sky-high. Perhaps then a net-zero target – on this definition – might really be feasible with a 10 per cent sacrifice of annual GDP per capita, or perhaps even something a bit smaller.

However, even then there are areas where the NZIER numbers are underdone if the government is really serious about a true net-zero goal. I checked the Labour Party’s and Green Party’s climate change policies, and the net-zero goal is there in a pretty stark and unqualified way. There is no suggestion that they are only interested in net-zero emissions on some UN definition – and fair enough, for them this is a moral cause, not a bureaucratic one.

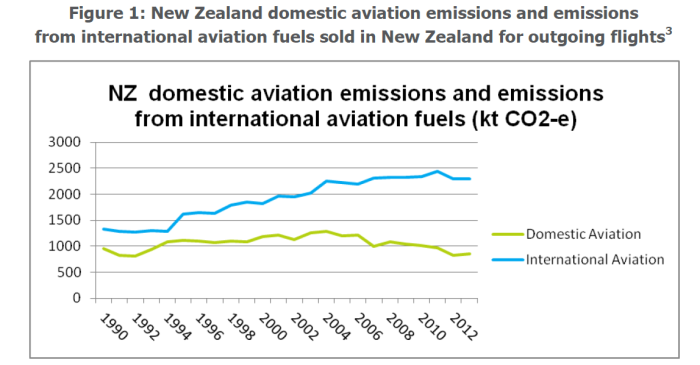

But what isn’t always appreciated among the wider public is that emissions associated with international aviation, real and substantial as they are, are not included in the UNFCCC (UN framework convention on climate change) definitions (neither is international shipping). This wasn’t because of any high science.

The international aviation and shipping sectors are not included in the recent Paris Agreement, which was negotiated under the United Nations Framework Convention on Climate Change (UNFCCC). The precedent for excluding these sectors from global climate agreements was set in 1998, when both sectors were excluded from national targets established under the Kyoto Protocol. This was largely due to a lack of agreement on how emissions should be attributed to particular States.

From the planet’s perspective, it doesn’t appear to matter whether the emissions comes from your car, or from Air New Zealand’s aeroplane. In the UNFCCC numbers – the base NZIER uses for their modelling – it does. But if you “care about the planet”, and want to give a strong “moral lead”, in the way the governing parties claim to, surely you need to offset international aviations as well. Domestic aviation is included in the ETS – so I learned, New Zealand was among the first to do so – but not international aviation.

There was a government document published on this issue a couple of years ago. As it points out, at present the numbers aren’t unduly large

Domestic aviation accounts for 1.1 percent of New Zealand’s total emissions.

and international emissions are about 2.5 times domestic

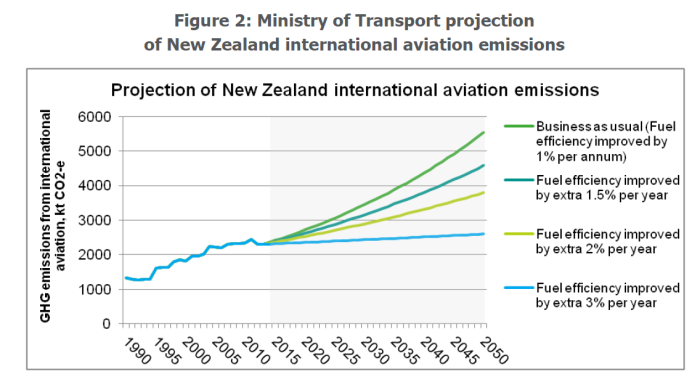

International tourism has been booming since then. And here are Ministry of Transport projections.

Even if we take the middle two lines, international aviation emissions would almost double by 2050.

Remember too that fuel costs are a very large proportion of airline operating costs (especially for long-haul operations) and that tourism spending is quite price-sensitive (you might be determined to take a holiday, but price affects location choice). If the government is really serious about a moral crusade for net-zero they can’t but include international aviation in the framework (and in the goal) – and if others were to follow their moral lead, the industry will have to have been included globally by 2050. And what will that do to the viability of our international tourism industry – almost everywhere is closer for almost everyone than New Zealand is, and we don’t have many unique offerings? Given a choice between taking your electric vehicle to the Croatian coast or flying to New Zealand, the economics won’t favour New Zealand.

In other words, if the government is serious about a genuine net-zero target, they really need to start factoring in international aviation emissions, especially as these are set to rise absolutely and (especially) as a share of total emissions. Perhaps they can just assume into existence some more forests, at no cost to other production, but it would seem highly risky to just do so.

For all these reasons, the 10 per cent sacrifice (a deliberately chosen act) of annual GDP estimated by NZIER seems to be very much at the low end of the plausible range, especially if they are serious about offsetting all emissions, not just ones that international convention negotiators happened to agree on. The 22 per cent number comes from MfE and NZIER and doesn’t seem implausible. Of course, any modelling, and any estimates, are inevitably highly imprecise. Something could turn up to set all these costs at naught, but it would seem rash – to say the very least – to set out upon such a journey in the idle hope that something will turn up, and if not well – never mind – our children will simply be up to a quarter worse off than otherwise. Productivity growth in New Zealand hasn’t been rapid in recent decades, but lopping a quarter off future incomes would be the equivalent today of simply giving up all the economic gains (in real GDP per hour worked) of the last 20 years. Simply breathtaking. And meanwhile people lament child poverty concerns, constraints on the health system, and so on. Productivity is about new possibilities. Are we really happy to give up such possibilities for the next few decades?

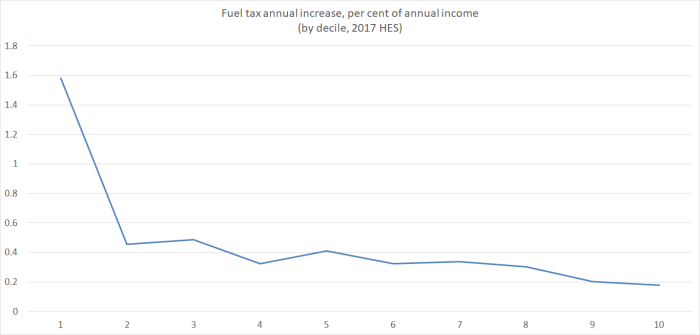

There is a lot of other interesting stuff in the NZIER report, but I wanted to end with the chart on the estimated distributional impact. In my previous post, I quoted the MfE text

Our modelling suggests the households that are in the lowest 20 per cent bracket for income may be more than twice as affected, on a relative basis, than those households with an average income.

Which is quite bad enough. But it is all the more stark when you see the chart in the NZIER report, drawn from some work done for them by Infometrics (in this chart they are looking only at the additional estimated losses from moving from the 50 per cent target to a net-zero target).

Specifically, people in the bottom two income quintiles will be hit six times as hard as people in the top quintile. Like MfE in the consultation document, NZIER rush to the client’s defence and suggest that redistribution policies could alleviate this. You wouldn’t thought that sort of advocacy was their role – having been commissioned to do modelling – but more importantly, they should know as well as anyone that when governments adopt policies to materially shrink the economy, it is even harder than usual to persuade voters in the upper quintiles to agree to give up even more to mitigate the losses the worst off are exposed to. Redistribution tends to win more favour when everyone is getting better off.

Has any government anywhere ever consulted on policy objectives that, if seriously pursued could cut future GDP per capita by anything from – on their own numbers – 10 to 22 per cent? If so, I can’t imagine when. It is a huge price to propose for what seems to be mostly a moral crusade – hence the title about pricing the hair shirt. If you doubt that interpretation, check out Labour climate change policy.

New Zealand must do its part, along with the rest of the world, in reducing climate pollution. It is not good enough to say we are too small to matter – most countries individually could claim the same. We must take our share in the effort however small, just as we did when dealing with CFCs, or opposing apartheid, or fighting fascism. Kiwis are not shirkers.

Opposing apartheid will have cost almost nothing to New Zealand GDP (albeit some utility losses for some rugby supporters) – same goes no doubt for opposing French nuclear testing in the Pacific. And I’ve never seen any large estimates for the cost of dealing with CFCs.

What of the World War Two comparison? I alluded to it in the my earlier post observing

Wars, of course, come at a very considerable cost – and sometimes are worth fighting – but again, I doubt any democracy (or perhaps even any tyranny) ever entered a war thinking that as a result of doing so they would be so much poorer 30 years on.

Awful as wars are – and with staggering losses of life in some countries – there is simply no way that any of the Anglo countries, that voluntarily entered the war to resist Hitler, were 10 per cent poorer, let alone 22 per cent poorer, thirty years on as a result.

Perhaps there is a legitimate moral cause at work here, but the government is inviting citizens to offer up a fearsome price – in lost incomes and opportunities – all while refusing to even consider the lowest cost option for substantially reducing the volume of emissions in New Zealand. For a country that has done so badly as regard productivity, under successive governments over many decades, it seems breathtakingly reckless. It seems all the weirder to be proposing to take some global moral lead in a country where, as even the IPCC reports have noted, there are both gains (eg better crop yields in many areas) and losses apparently on offer from rising global temperatures.