It was confirmed yesterday that the new government’s immigration policy will be the policy the Labour Party campaigned on (albeit very quietly). And so we learned that the new government will remain a fully signed-up adherent of the same flawed, increasingly misguided, “big New Zealand” approach that has guided immigration policy for at least the last 25 years.

If that is disappointing, it shouldn’t really be any surprise. The Green Party approach to immigration is pretty open – the “globalist” strand in their thought apparently outweighing either concern for New Zealand’s natural environment or any sort of hard-headed analysis of the economic costs and benefits to New Zealanders. Only a few months ago, they were at one with the New Zealand Initiative, tarring as “xenophobic” any serious debate around the appropriate rate of immigration to New Zealand. Never mind that population growth is driving up carbon and methane emissions, in a country where marginal abatement costs are larger than in other advanced economies, and yet where the same party is determined that New Zealand should reach net zero emissions only 33 years hence.

As for New Zealand First, they talk a good talk. But that’s it. As I noted a few months ago, reading the New Zealand First immigration policy (itself very light on specifics)

If one took this page of policy seriously, one could vote for NZ First safe in the expectation that nothing very much would change at all about the broad direction, or scale, of our immigration policy. Of course, there would be precedent for that. The last times New Zealand First was part of a government, nothing happened about immigration either.

Even so, I was just slightly surprised that there wasn’t even a token departure from the Labour Party’s immigration policy that New Zealand First could claim credit for. The New Zealand Initiative’s report on immigration policy earlier in the year was largely (and explicitly) motivated by concerns about what New Zealand First might mean for immigration policy.

Six months ago, when we started scoping the Initiative’s immigration report, we had a very specific audience in mind: Winston Peters. Our aim was to assemble all the available research and have a fact-based conversation with New Zealand’s most prominent immigration sceptic.

Turns out that, perhaps not surprisingly based on the past track record, that they needn’t have bothered.

And so Labour’s election policy will be the immigration policy of the new government. The policy documents themselves are here and here. I wrote about the policy here at the time it was released in June, before the Ardern ascendancy. It was notable how little attention Labour gave to immigration policy during the campaign – perhaps it didn’t fit easily with the “relentlessly positive” theme – and I understand there was a conscious decision by the new leadership to downplay the subject. It will be interesting to see now whether they follow through on their manifesto, but very little about immigration policy requires legislative change so, in principle, the changes should be able to be done quite quickly. In fact, as the biggest proposed changes affect international students one would assume they will be wanting to have those measures in places in time for the new academic year.

What also remains quite remarkable is the extent to which Labour’s policy has been taken as a substantial change. Serious overseas media and intelligent commentators have presented Labour’s proposals as some sort of major sustained change in New Zealand approach to immigration, and thus to expected immigrant numbers. To read some of the Australian and American commentary you might have supposed, say, that in future New Zealand’s immigration approvals might be cut towards, say, the sorts of levels (per capita) that prevailed in the United States under Bush and Obama.

Labour’s policy is, of course, nothing of the sort. Under the proposed policy, New Zealand will remain – by international standards – extraordinarily open to non-citizen migrants, with expected inflows three times (per capita) those of the United States, and exceeded only (among OECD countries) by Israel in a good year (for them).

What determines how many people from abroad get to settle permanently in New Zealand is the residence approvals programme. Under that programme, at present the aim is to grant around 45000 approvals to non-citizens each year (Australians aren’t subject to visa requirements, but in most years the net inflow of Australians is very small). The outgoing government reduced that target (from 47500) last year. Labour’s immigration policy document does not, even once, mention the residence approvals programme. That was, no doubt, a conscious choice. They are quite happy with the baseline rate of non-citizen immigration we’ve had for the last 20 years; quite happy to have the highest planned rate of non-citizen immigration anywhere in the OECD. Medium-term forecasts of the net non-citizen immigration inflow will not change, one iota, if Labour proceeds with their policy. For some of course, that will be a desirable feature. For others it is a serious flaw, that results from failing to come to grips with the damage large scale immigration is doing to the economic fortunes of New Zealanders.

Of course, there are planned policy changes. There are various small things:

- an increased refugee quota,

- steps to increase the utilisation of the existing Pacific quotas,

- more onerous requirements for investor visas (including requiring investment in new “government-issued infrastructure bonds”),

- a new Exceptional Skills visa,

- a KiwiBuild visa

Taken together, these won’t affect total numbers to any material extent.

There is also a (welcome) change under which they will

Remove the Skilled Migrant Category bonus points currently gained by studying or working in New Zealand and standardise the age points to 30 for everyone under 45.

All else equal, these changes won’t affect the number of people getting residence, or materially affect the average quality (skill level) of those getting residence. That is a shame: at present, too many migrants aren’t that skilled at all, and maintaining such a large approvals target (in such a remote, not very prosperous, country) makes it hard to lift the average quality.

The bigger changes are under two headings. The first is around temporary work visas. Here is what they say they will do.

Labour will:

• Actively manage the essential skills in demand lists with a view to reducing the number of occupations included on those lists

• Develop regional skill shortage lists in consultation with regional councils and issue visas that require the visa holder to live and work within a region that is relevant to their identified skill

• For jobs outside of skills shortages lists, Labour will ensure visas are only issued when a genuine effort has been made to find Kiwi workers

• Strengthen the labour market test for Essential Skills Work Visas to require employers to have offered rates of pay and working conditions that are at least the market rate

• Require industries with occupations on the Essential Skills in Demand lists to have a plan for training people to have the skills they require developed together with Industry Training Organisations

• Review the accredited employers system to make sure it is operating properly.

The broad direction seems sensible enough – after all, the rhetoric has been about lifting the average skill level of the people we take. But as I noted in my comments in June, the policy is notable for its touching faith in the ability of bureaucrats to get things right, juggling and managing skills lists, and now extending that to a regional differentiation. There is no suggestion, for example, of letting markets work, whether by (as I’ve proposed) imposing a flat (quite high) fee for work visas and then letting the market work out which jobs need temporary immigrant labour, or by requiring evidence that market wages for the skill concerned have already risen quite a lot. The latter would have seemed an obvious consideration for a party with trade union affiliates.

On Labour’s own estimates, these changes won’t have a large effect on the number of people here on work visas at any one time, although in the year or so after any changes are implemented, the net inflows that year will be lower than they otherwise would have been.

Much the same goes for the biggest area of change Labour is proposing, around international students.

Labour will:

• Continue to issue student visas and associated work rights to international students studying at Level 7 or higher – usually university levels and higher

• Stop issuing student visas for courses below a bachelor’s degree which are not independently assessed by the TEC and NZQA to be of high quality

• Limit the ability to work while studying to international students studying at Bachelor-level or higher. For those below that level, their course will have to have the ability to work approved as part of the course

• Limit the “Post Study Work Visa – Open” after graduating from a course of study in New Zealand to those who have studied at Bachelor-level or higher.

In general, I think these are changes in the right direction. Here were some of the comments I made earlier

I’m a little uneasy about the line drawn between bachelor’s degree and other lines of study. It seems to prioritise more academic courses of study over more vocational ones, and while the former will often require a higher level of skill, the potential for the system to be gamed, and for smart tertiary operators to further degrade some of the quality of their (very numerous) bachelor’s degree offerings can’t be ignored. …… I’d probably have been happier if the right to work while studying had been withdrawn, or more tightly limited, for all courses. And if open post-study work visas had been restricted to those completing post-graduate qualifications.

The proposals are some mix of protecting foreign students themselves, protecting the reputation of the better bits of our export education industry, and changes in the temporary work visas rules themselves. In Labour’s telling – and it seems a plausible story – the changes are not designed to produce a particular numerical outcome, but to realign the rules in ways that better balance various interests. The numbers will adjust of course, but that isn’t the primary goal.

Labour estimates that these changes will lower the number of visas granted annually by around 20000. That is presented, in their documents, as a reduction in annual net migration of around that amount. But that is true only in a transition, immediately after the changes are introduced. The stock of people here on such student and related visas will fall, but after the initial transitional period there will be little or no expected change in the net inflow over time (which is as one would expect, since the residence approvals target is the key consideration there).

To see this consider a scenario in which 100000 new short-term visas are issued each year, and all those people stay for a year and a day (just long enough to get into the PLT numbers). In a typical year, there will then be 100000 new arrivals and 100000 departures.

Now change the rules so that in future only 75000 short-term visas are issued each year. In the first year, there will be 75000 arrivals and (still) 100000 departures (people whose visas were issued under the old rules and who were already here). But in the next year, there will be 75000 arrivals and 75000 departures. Measured net PLT migration will have been 25000 lower than otherwise in the first year, but is not different than otherwise in the years beyond that.

That doesn’t mean the policy changes have no effect. They will lower the stock of short-term non-citizens working and studying in New Zealand. They will ease, a little, demand for housing. In some specific sectors, with lots of short-term immigrant labour, they may ease downward pressures on wages (although in general, immigrants add more to demand than to supply, and that applies to students too). But it won’t change the expected medium-term migration inflow.

Oh, and the student visa changes will, all else equal, reduce exports

Selling education to foreign students is an export industry, and tighter rules will (on Labour’s own numbers) mean a reduction in the total sales of that industry. Does that bother me? No, not really. When you subsidise an activity you tend to get more of it. We saw that with subsidies to manufacturing exporters in the 1970s and 80s, and with subsidies to farmers at around the same time. We see it with film subsidies today. Export incentives simply distort the economy, and leave us with lower levels of productivity, and wealth/income, than we would otherwise have. In export education, we haven’t been giving out government cash with the export sales, but the work rights (during study and post-study) and the preferential access to points in applying for residence are subsidies nonetheless. If the industry can stand on its own feet, with good quality educational offerings pitched at a price the market can stand, then good luck to it. If not, we shouldn’t be wanting it here any more than we want car assembly plants or TV manufacturing operations here.

I participated in a panel discussion on Radio New Zealand this morning on Labour’s proposed changes. In that discussion I was surprised to hear Eric Crampton suggest that the changes would put material additional pressure on the finances of universities. Perhaps, although (a) the changes are explicitly aimed at sub-degree level courses, and (b) to the extent that universities are getting students partly because of the residence points that have been on offer, it is just another form of “corporate welfare” or subsidy that one would typically expect the New Zealand Initiative to oppose. Whether hidden or explicit, industry subsidies aren’t a desirable feature of economic policy.

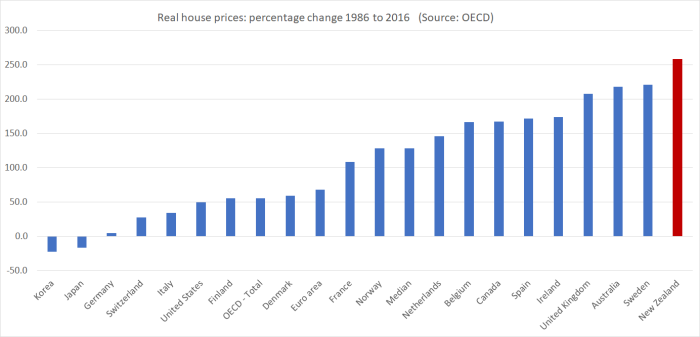

Standing back, Labour’s proposal look as though they might make a big difference in only a small number of sectors, notably the lower end of the export education market. If implemented, they will be likely to temporarily demand housing demand – perhaps reinforcing the current weakness in the Auckland housing market, along with some of their other proposed legislation (eg the extension of the brightline test and the “healthy homes” bill). But they aren’t any sort of solution to the house price problem either: after the single year adjustment, population growth projections will be as strong as ever, and in the face of those pressures only fixing the urban land market will solve that problem. Time will tell what Labour’s policy proposals in that area, which have sounded promising, will come to.

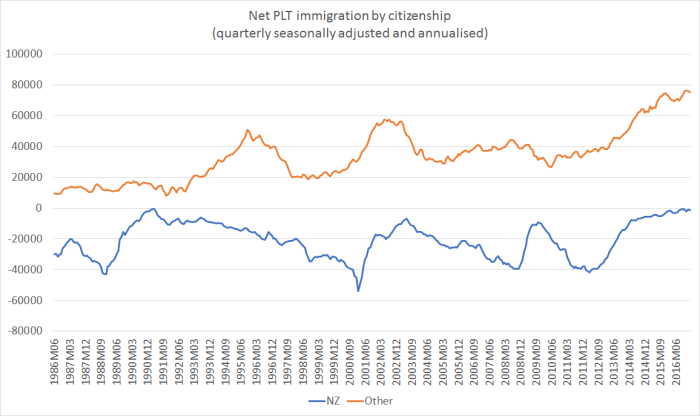

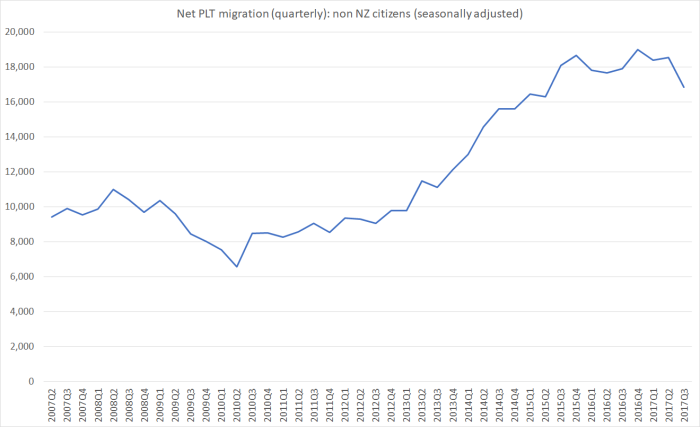

Two final thoughts. One wonders if whatever heat there has been in the immigration issue – and it didn’t figure hugely in the election – will fade if the headline numbers start to turn down again anyway. The net flow of New Zealanders to Australia has not yet shown signs of picking up – but it will resume as the Australian labour market recovers. But in the latest numbers, there has been some sign of a downturn in the net inflow of non-citizens.

There is a long way to go to get back to the 11250 a quarter that is roughly consistent with the 45000 residence approvals planned for each year. But, if sustained, this correction would provide at least some temporary relief on the housing and transport fronts. As above, Labour’s changes will have a one-off effect on further reducing this net inflow in the next 12 or 18 months, but nothing material beyond that.

And in case this post is seen by the new Minister of Immigration, or that person’s advisers, could I make a case for two things:

- first, better and more accessible data. The readily useable migration approvals is published only once a year, with a lag even then of four or five months. The latest Migration Trends and Outlook was released in November 2016, covering the year to June 2016. It is inexcusably poor that we do not have this data readily, and easily useable, available monthly, within a few days of the end of the relevant month, and included (for example) as part of Statistics New Zealand’s Infoshare platform. The monthly PLT data are useful for some things, but if you want a good quality discussion and debate around immigration policy, make the immigration approvals data more easily available. As a comparison, building permits data is quickly and easily available, reported by SNZ. Why not migration approvals?

- second, considering referring the issue of the economics of New Zealand immigration to the Productivity Commission for an inquiry. Perhaps the current policy, as Labour proposes to amend it, has all the net gains the advocates say it does. If so, the Productivity Commission could helpfully, and in a non-partisan way, demonstrate that. But there are still serious issues around New Zealand’s unusually liberal immigration policy, in a country so remote and with such a poor track record in increasing its international trade share. Whatever the economic merits of immigration in some places, it is by no means sure that large scale immigration here is doing anything to improve the fortunes of most New Zealanders. It may, in fact, be holding us back, being one part of the story as to why we’ve failed to make any progress in closing the productivity gaps with other advanced economies. It would seem an obvious topic for the Productivity Commission, and a good way of lifting the quality of the policy debate around this really substantial policy intervention.