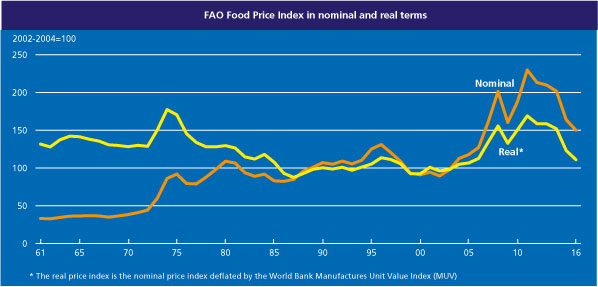

I stumbled on this chart yesterday.

It shows the FAO’s food price index, all the way back to 1961, including a real series in which the nominal FAO index is deflated by the World Bank’s Manufactures Unit Value Index, “a composite index of prices for manufactured exports from the fifteen major developed and emerging economies to low- and middle-income economies”. The FAO index itself is a weighted average of the international prices for cereals, vegetable oil, dairy, meat, and sugar.

Never knowingly optimistic, I was still a little surprised by the picture. After all, a dominant story of the last 25 years has been one of falling prices of manufactures, driven in large part by the industrialisation of China, and reflected in (for example) sharp falls in the terms of trade for Japan and Taiwan. And optimists around New Zealand have told stories about the growing global scarcity of water, rising Asian demand for high quality protein, and so on. And yet on this measure real food prices – the amount of manufactures a given amount of food commodities would purchase – have been no better than flat. If anything, at present prices seem to be moving back towards the lows of the 20 years from the mid 80s to the mid 00s. And the dairy component doesn’t appear to have been behaving much differently than the other components of the index.

Of course New Zealand isn’t a low or middle income country, so perhaps this World Bank index isn’t representative of our purchases over time. The WTO also has an index for prices of imports and exports of manufactures: it has only been running since 2005, and over that period prices of manufactures have increased less than those of food (as reflected in the FAO index). Our own overall terms of trade – for a wider range of exports than food, and imports than manufactures – have still been quite good by historical standards (although even in the 1950s and 60s our incomes were drifting down relative to the rest of the advanced world).

There appears to plenty of scope for productivity growth in agriculture (although there hasn’t been much in New Zealand in recent years), but there isn’t any more land being made here, and environmental/water concerns are limiting just how much more intensively existing land can be used. For a country with a fairly rapidly growing population, that is still heavily dependent on its food exports, the prospects for sustained high incomes seems to rest on some combination of high productivity and high prices. Or, of course, the rapid growth in other exports – but over decades now that latter just hasn’t been happening.

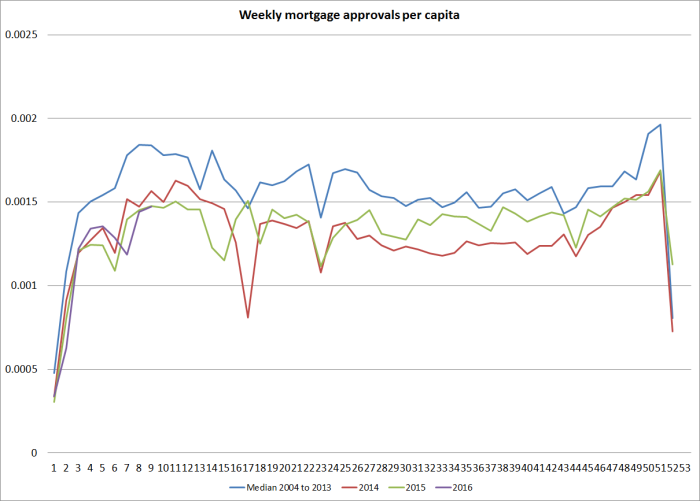

On completely different topic, this is one of favourite housing charts.

It shows the number of weekly mortgage approvals (with a rough adjustment to turn it into a per capita measure) for each week of the year, numbering 1 to 52/53. That deals with (a) the rising trend in the population over time (material over a decade), and (b) the fact that the data aren’t seasonally adjusted.

I haven’t shown a (hard to read) version with lines for each year for which the Reserve Bank has data. But you can see how much more active the mortgage market was on average over the first decade of the data than it has been over the last few. In fact, in 2007, the peak year of the previous boom the line was around .0025 at this time of year – in other words, more than 60 per cent more mortgages were being approved per capita at this time of year in 2007 than was happening this year (or last year).

The housing finance is now, unfortunately, quite badly distorted by the Reserve Bank’s increasing range of direct controls, but there is just nothing in this data to suggest a frenzied speculative boom. In such booms, volumes tend to be very strong – not just new loans, but turnover per capita too. There was a plausible story like that, backed by the data, in the previous boom from 2002 to 2007. There hasn’t been, and isn’t, in the last few years. Individual potential buyers have no doubt been very worried about missing out, perhaps permanently, but the main factors behind what strength there has been in house prices – considerable in Auckland- was the government. It encourages rapid population growth through a liberal immigration policy, and at the same time is responsible for the legislative framework that makes urban land scarce and impedes the physical expansion of the city. That seems that like a crazy policy mix to me, but it isn’t a frenzied credit boom – and isn’t obviously any sort of “bubble” either. The definition of a bubble is rather elusive, but suggests something completely detached from fundamentals. But government policy parameters are fundamentals. They could change, but there is little or no sign of them doing so.

Why harp on the point? In the lead-up to next week Monetary Policy Statement some of those opposing OCR cuts do so on the basis of house price concerns. House prices aren’t in the Reserve Bank’s monetary policy remit, but in any case there is no sign of irrational exuberance – whether by buyers or financiers – driving what is going on. Rising (and absurdly high) real house prices in some areas appears to be largely a relative price change, attributable to pretty easily identifiable structural factors. Orienting monetary policy around the price of a good, itself largely shaped by government structural policy choices, would be even odder than orienting it around, say, the price of gold – a product which, at least, governments did not directly influence the supply.

The other relevant consideration is the question of just how much difference monetary policy shocks, and adjustments to the OCR, actually make to house prices. In support of its LVR policies, the Reserve Bank used their model a couple of years ago to argue that achieving the same impact on house prices as they expected to achieve using LVR restrictions, they would have to lift interest rates (relative to baseline) by around 200 basis points. The LVR restrictions were expected to lower house price inflation by around 1-4 percentage points in the first year (the effect fading away thereafter). Modelling house prices well isn’t easy, but if this Reserve Bank analysis is even remotely right it seems unlikely that further cuts to the OCR over the next few quarters of even 50 to 100 basis points, offsetting falling external incomes, falling inflation expectations and rising offshore funding costs, would materially affect the level of national house prices.

The law of supply and demand: simple, yet, so complex – especially when it comes to housing! Supply appears an issue (though, just over 10k properties for rent on Trade Me) but I’ve been pondering the ‘structure’ of demand and especially the role of investors – particularly those that have accumulated a portfolio during the last 20 years. To my mind, capital gains on legacy investment properties – aided initially by financial liberalization and more recently by falling (global) interest rates combined with a recovery in credit supply – has enabled those with assets to accumulate more assets: an investor with a good lawyer, accountant, and bank relationship has, arguably, been in a superior position to bid on properties during the past few years especially as rental demand remains high as future homeowners save for a (growing) deposit. Perhaps this is an issue mainly in Auckland – Figure 4.7 within the November 2015 FSR would provide some supporting evidence (nb: I guess as gross rental yields get closer to one year deposit rates, there is a limit to further investor demand unless capital gain expectations remain strong?). In short, is housing demand a two tier market? Any thoughts (ggs!) appreciated.

Re (food) commodities, supply seems eventually to react to prices that are generating above average returns for existing producers so perhaps our terms of trade reflect this aspect of fundamental economics. Recent trends would indicate there is scope for tourism to kick on and I guess it is less of a commodity product (??) so fingers crossed we can keep the waterways clean if this is deemed part of the New Zealand experience.

LikeLike

The average property investor is a mum and dad who have equity in their homes and are looking towards some form of retirement income in their retirement. That is why Labour does not make any headway when they propose a Capital Gains Tax, they are basically decimating their own voter base.

Auckland property under the Unitary Plan would allow a second dwelling with a separate kitchen attached to the main dwelling. Auckland Council planners have provision for higher density without having to go highrise by allowing practically most existing houses a opportunity for a home and income or for a property investor, 2 incomes for every property. Minimum build requirement is 40sqm for the extended property. No carparking requirement and no additional living space requirement.

It does mean more expensive houses but it may mean cheaper rents.

LikeLike

(distracted by the Republican debate)

Re exports, I’m prob more skeptical about the tourist potential than you would be. It has been a good year, but a bad decade – so another couple of really good years might still only take us back to a middling sort of trend. I know there are lots of Chinese, but is there really that much to see/do in NZ? Perhaps I’m just a Europhile, but given the choice between the UK or France, and NZ, I know which I’d go back to again and again.

Housing: I’m more skeptical about their having been an autonomous role for investors in driving up prices – after all, they haven’t risen in those US places with the supply obstacles. Smart people (not me) either realized the implications of the population and supply constraints issue, or simply extrapolated good returns in some parts of the country (mostly those with supply/popn constraints) and also emerged as the purchasers of second-resort when the prices of houses started getting beyond the ability of younger people to buy (someone had to own). There is no doubt that having collateral has assisted in getting more – but is it an independent force, or just a responsive one, an effect of the chokehold of population and supply squeezing out the new generation of owner-occupiers?

LikeLike

No idea! Still trying to join the dots. But I guess it partly reflects the fact that real estate/land is, from the banking system perspective, a superior form of collateral the appreciation of which – for whatever reason(s) – enables easier access to credit/capital. Further, rising rents on legacy debt funded assets refinanced at record low rates seems to distort the demand side somewhat but unpicking the linkages/causation is a nightmare….

LikeLike

Michael I have written a series of articles for the layman on the economics of housing intensification. So far the layman haven’t been interested -I think it was a mistake to use a geeky word like contiguity in the title. Some economist types though have given me some positive feedback.

https://makingchristchurch.com/why-land-contiguity-is-causing-market-failure-in-new-zealand-s-cities-eb00577c8d91#.ubrll026c

https://makingchristchurch.com/leave-it-to-the-market-to-find-a-solution-98ecd8669648#.qxvql93xr

https://makingchristchurch.com/use-compulsory-acquisition-of-land-for-housing-52ad0ffc700d#.5ffsqusfx

https://makingchristchurch.com/voluntary-land-reallocation-and-adjustment-881311e995af#.8r6zhmou9

LikeLike

THanks Brendon. I’ll look forward to reading them.

LikeLike

Eminent Domain is not a US thing. It exists under English law and is common throughout the former colonies of the British Empire. The Public Works Act is derived from this Eminent Domain doctrine ie all land is ultimately owned by the crown. Singapore uses this doctrine in compulsory acquisition of land for its social housing developments.

The Public Works Act can certainly be expanded to be able to compulsorily acquire land for social good. Certainly the main provisions are already in place. It is extremely unlikely the government or any NZ government would risk it.

Large plots of land are available however there are certain problems which no one wants to recognise,

1. the Waitakere Ranges. Lots of large plots, all we need to do is chop down a few hundred kauri trees. Ooooops not going to happen. It is a community issue not a legislature issue.

2. Height limits over vast vast tracts of land surrounding 57 sacred mounts. Remove that viewshaft visual limits and you can build massive highrise buildings. Oooops that is a maori heritage and community issue, not a legislature issue.

3. Drop the 25 metre road frontage requirement then you do not need contiguity of land

4. Lack of infrastructure, due to lack of funding. Ooooops that is a budget constraint issue and not a legislature issue.

Until you fix these 4 main issues you still cannot build even with large tracts of land.

LikeLike