Since the Governor’s speech a couple of weeks ago (building on the January OCR review announcement), I’ve been reflecting again on how best to think about what is going on with inflation in New Zealand.

The Governor cited a single measure of core inflation, the sectoral factor model measure of core inflation, to assert his comfort with the current headline inflation rate. As I noted at the time, it is very rare for any specific measure of core inflation to be cited in official Bank announcements. The typical story has been along these lines

There is no agreed upon ‘best’ approach to measuring core inflation, and each approach has various advantages and limitations. Some work best in some circumstances; some in others.

That line is taken from the abstract to a nice Reserve Bank Bulletin article reviewing core inflation issues and measure, published a little earlier in the current Governor’s term).

The same year they published a nice Analytical Note on the sectoral core measure itself. The non-technical summary at the start of that paper notes

There are many ways to measure core inflation. Statistics New Zealand publishes a range of measures that involve removing volatile price movements before inflation is calculated, or excluding certain groups of items from the calculation. As well, the Reserve Bank of New Zealand has a set of models that produce core inflation estimates. Every model is different, and the Reserve Bank uses the full suite of measures when forming an assessment of what is going on with inflation.

(For the record, I edited both these publications, but both were widely circulated in draft, and were approved by the Assistant Governor – Chief Economist – and the Bank’s Communications Committee, on which all four governors sit and actively participate. I don’t recall such lines ever being contentious.)

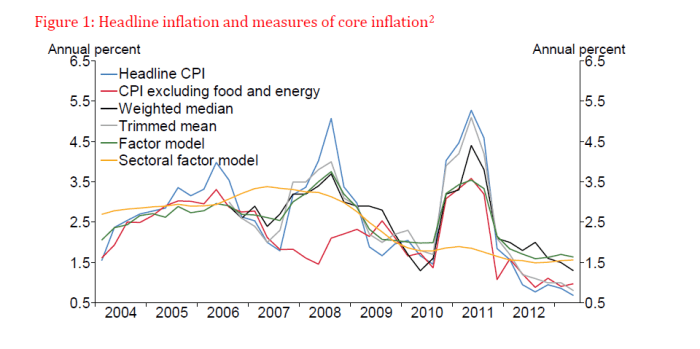

The Analytical Note went as far as to publish this chart, illustrating the variety of measures the Bank looked at.

Incidentally, note the nice longer-term time series for the weighted median and trimmed mean series. The Bank no longer publishes these (linked) series on its website, just reporting the very short official series published by Statistics New Zealand. This is something that should be remedied – as, for example, the Reserve Bank of Australia does.

But now, apparently, the Governor favours the sectoral factor model to the exclusion of all other core inflation indicators. It is certainly convenient that it is, at present, the highest of any of the range of core inflation measures, and that the inflation rate, on this measure, has increased over the last year.

Here is a table I ran a couple of weeks ago:

| Annual inflation, year to Dec 2015 | |

| Trimmed mean | 0.4 |

| Weighted median | 1.5 |

| Factor model | 1.3 |

| Sectoral factor model | 1.6 |

| CPI ex petrol | 0.5 |

| CPI ex food and vehicle fuel | 0.9 |

| CPI ex food, household energy and vehicle fuel | 0.9 |

| CPI ex cigarettes and tobacco | -0.3 |

| Non-tradables ex govt charges and alcohol and tobacco | 1.8 |

But neither the Governor, nor his officials, have given us any reasoning as to why they think that on this occasion this indicator is the single best representation of what is going on – so much so that the other measures aren’t even worth mentioning. I suppose one could lodge a request but (a) I doubt there would be anything to support the Governor’s preference, and (b) no doubt, we’d be told it was none of our business and that information had to remain secret to, for example, “prevent damaging the economy of New Zealand“. For an institution that likes to hold itself out as being transparent about its economic reasoning and analysis – and which has more (taxpayer-funded) macro analysts and researchers than any other agency – it really isn’t good enough.

Relatedly, if the sectoral core model is really providing much the best steer, what has changed since the start of 2014? Recall that sectoral core inflation then had been almost dead-flat at around 1.4 per cent for a couple of years – and yet the Governor began an aggressive tightening cycle. Perhaps it was a misleading measure then, but the best measure now? It is possible, but surely we are owed an explanation?

Why might we be a little sceptical that some “true” notion of core inflation is (a) rising, and (b) as high as 1.6 per cent (itself still materially below the midpoint)?

First, the sectoral factor measure is the product of a model, and that model has error bands around it. Even the historical period numbers are midpoint estimates of a range which the Bank tells us is around 0.6 percentage points wide.

And, as with all of these sorts of models, the problems are particularly acute for the most recent observations. The model is, in effect, trying to discern the common trends in the various component price series, but it can do that increasingly reliably with the benefit of more time and more data. That makes tools like this most valuable for identifying the underlying inflation processes in periods of history (eg looking back now on the pre 2008 boom) and relatively less useful for “spot” reads on what is happening right now. In that sense, it is a little like filter-based estimates of the output gap, and it is similarly unwise to put too much weight on real-time estimates of any one model of the output gap.

And, as with all of these sorts of models, the problems are particularly acute for the most recent observations. The model is, in effect, trying to discern the common trends in the various component price series, but it can do that increasingly reliably with the benefit of more time and more data. That makes tools like this most valuable for identifying the underlying inflation processes in periods of history (eg looking back now on the pre 2008 boom) and relatively less useful for “spot” reads on what is happening right now. In that sense, it is a little like filter-based estimates of the output gap, and it is similarly unwise to put too much weight on real-time estimates of any one model of the output gap.

Second, there is no sign of any pick-up in wage inflation, or in measure of inflation expectations.

Third, the measures that are easier to disentangle mostly aren’t suggesting core inflation is rising, or that it is as high as 1.6 per cent. Take, for example, the internationally quite commonly used approach: CPI inflation rate excluding food, household energy and vehicle fuels is only 0.9 per cent. It isn’t always reliable – in 2007 it ran below most other measures of core inflation because of some large changes in government charges (childcare subsidies). But we know (SNZ tells us) this time round that taxes and government charges are not, overall, affecting the inflation rate. It is a good example of why one needs to look at all the measures, and use them to develop an overall story. Focusing on a single indicator is often likely to be quite dangerous – especially when it is something of a black-box, prone to endpoint problems.

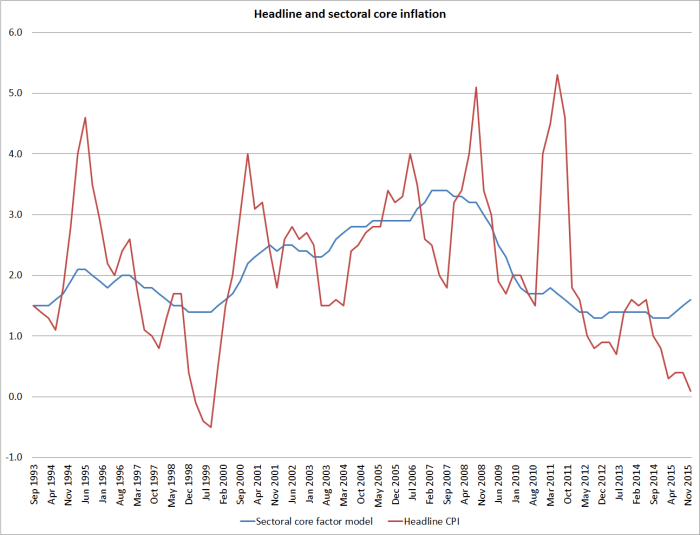

And here is a concrete illustration of something that bothers me about the sectoral factor model results at present.

We know that the repeated increases in tobacco excise has been having a big impact of overall non-tradables inflation in recent years (and the overall CPI). More recently, cuts to ACC motor vehicle registration charges have worked the other way. Statistics New Zealand do not give us a series of overall CPI inflation excluding tobacco and government charges, but they do provide one for non-tradables inflation (at least from 2007). And the Reserve Bank helpfully publishes separately the non-tradables component of the sectoral factor model. The chart shows overall non-tradables inflation as well. (The 2010 surge is the increase in GST, administratively excluded from the sectoral factor measures.)

Over the period since 2007, the combined effects of tobacco tax increases and central and local government charges have substantially boosted non-tradables inflation (the red line has been well above the blue line). So it is troubling that the non-tradables sectoral factor model component looks so like the overall non-tradables series over the period since 2009, even though it is substantially boosted by factors that no one would regard as core inflation – they are administered (by governments) prices. I’m less bothered by the idea that sectoral core inflation in the non-tradables sector might have been flat – a lot of the inflation in recent years looks to have been in the construction sector (think Christchurch) and the model will tend to look past that as not representative of the whole economy.

But if the Bank is going to drive policy – its assessment of the current inflation situation relative to target – off a measure that has looked more like a series that includes lots of administered taxes and prices, than it does the series that excludes those effects, they need to give us a lot more explanation than they have done to date. It is possible that there is a good and convincing story, and that the sectoral factor model is really capturing something important that has been going on in non-tradables inflation that simply isn’t visible to the naked eye (or in other price series), but we need to see that story. and the other supporting evidence for it. What is it, for example, that is leading to the sectoral measure holding up, and even rising, just as the overall non-tradables inflation rate converges (downwards) on the series excluding those government-determined prices?

Personally, I think it would be safer for the Bank to work on provisional basis that core inflation is around 1 per cent at present. That is around where the exclusion measures would suggest, and well above the trimmed mean – the approach to core inflation approach that, for example, tends to get most coverage among analysts in Australia.

[UPDATE: And don’t lose sight of the fact that the average of the blue line – excluding the GST spike – has been below 2 per cent since 2009. No one I know of would expect non-tradables inflation to be at or below 2 per cent if core or underlying inflation in total were anywhere near the 2 per cent target midpoint.]

This whole episode is pretty unsatisfactory, and a poor reflection on the Bank. Reasonable people might differ on the appropriate stance of monetary policy. But the attempt to justify the stance on a single (complex) core measure, without substantive elaboration or explanation, when that same core measure would appear to have warranted policy easings when the Bank began aggressively tightening two years ago, looks disconcertingly like a Governor fixing for a time on the highest convenient measure of inflation. That isn’t good policy or good governance. And I suspect it makes many of the Bank’s own economists quite uncomfortable.

As a reminder of the Deputy Governor’s 2013 report of the Bank’s aspirations

The Reserve Bank is deeply committed to transparency – of policy objectives, policy proposals, economic reasoning, and of our understanding of the economy, and of course of our policy actions and intent. Clear communication and strong public understanding make our policy actions more effective.

We are working to enhance the openness and effectiveness of our communications

It just isn’t happening.

And note that all these quotes are from 2013, early in the Governor’s term, before things started going really wrong. And before they responded to those mistakes – which any humans will at times make – by turning inward, pretending that nothing is wrong, and avoiding serious scrutiny and debate. Digging deeper holes doesn’t usually solve such problems.

It was wryly amusing to note the other day that the Governor of the People’s Bank of China – central bank of a brutal repressive state not know for any sort of transparency – had given an extensive interview (not necessarily revealing a great deal) to a publication not historically known as a party mouthpiece. Our Governor has, I’m told, not given a single substantive interview in his three and half years in the job.

Our RBA love the Trimmed mean and median series and people are taking notice of the US series courtesy of the cleveland Fed.

I would have thought they are the best two but to include all both historically and up to date to show us all what the picture actually is.

LikeLiked by 1 person

I do not have a issue with the Governor not fronting to explain. He does come across as a shy book worm type. But I do expect working papers and justification of decisions and forecasts that are open to scrutiny and debate. With 250 economists twiddling their thumbs in the RBNZ I would expect some paperwork justification available.

LikeLike

In their defence (momentarily….) most of the 250 aren’t economists, but there are a lot……

Communications inevitably involves a mix of products. But in the modern era, especially with all the considerable powers formally vested in a single individual, I don’t really think it is any more acceptable for the Governor to do no interviews than, say, for the MOF not to. “shy book worms” don’t usually become Ministers of Finance…

LikeLiked by 1 person

Interesting stuff. It does seem inflation/the inflation process is a much more complex beast these days and perhaps this is one area where a lot more research and/or public debate is warranted. Demographics, technology, globalisation, confidence etc. are often cited as reasons why (global) inflation is low, yet, it seems difficult to quantify the impact of these relatively recent trends using prior ‘workhorse’ models. “We are looking into it” would be a welcome phrase but maybe there is the thought that this could prompt questions about the ability of central banks to control inflation? Or would an open review further enhance credibility? (e.g. your post on the Bank of Canada renewal process). Not sure but sometimes I think lower prices driven by innovation, fair labour relations, and effective competition should be considered a welcomed development….

ps. does this article count as substantive? Sleeves rolled up, looking relaxed – seems ready for a pint rather than another book!!

http://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=11511736

LikeLike

I guess my problem with the supply-driven story of low inflation (which I would largely welcome if true) is that no one really doubts that productivity growth has slowed rather than accelerated, and as far as I can see the regulatory state and size of govt haven’t been skrinking either. So to the extent that there is abundant supply of some stuff, it mostly feels like a consequence of unexpectedly weak demand. Commodities – and labour – were really cheap in the 1930s too.

I’m relying on a senior journalist (who has requested several) for the “no interviews” line, but I inserted “substantive” because I was conscious of that rather soft Dann piece.

LikeLike

…..not my area of expertise (like most topics in economics!!) but there has been some research of late into the issue of service sector output / productivity measurement. It is interesting that employment is rising in the UK/US for example but productivity remains stagnant which begs the question – why are the jobs being created? I often think it is a macro v micro issue as the service sector, while high on labour input, is typically quite low in terms ‘physical capital’. Lower physical capital typically requires less financial capital which provides scope for higher returns on the latter even though productivity in aggregate looks quite low…..??

LikeLike

One would have to come to the conclusion that the Gov. is simply a procrastinator.

Can’t make up his mind, beats about the bush, hides from his peers and those his decisions must affect.

Typical poor quality Public Servant.

Not what we need.

LikeLike

This National government has done alot.

1. Dropped depreciation on building which I disagree with as we are pretty much the only country in the world that does not allow building depreciation.

2. Introduced a form of Capital Gains tax on property by stealth and called it a 2 year Bright Line Test for speculators and IRD registration of overseas buyers.

3. Got a $500 million Sky City convention and hotel complex approved and across the line

4. Put on a fabulous Rugby World finale in a brand new MT Eden Stadium after being stymied on a $400 million Rugby stadium on the Auckland Harbour, which Aucklanders were rather dumb to reject.

5. Dropped Labour Michael Cullen’s 4% company contribution on Kiwisaver and allowed loopholes in Kiwisaver legislation that allows Employers to draw both Employer and Employee contribution from the Employee.

6. Increased spending on Roading of National significance and extensive bicycle lanes

7. Tourists hit a record 3 million and $11 billion contribution to the economy

8. International fee paying students hit a record 110,000 with $2.85 billion contribution to the economy

9. The NZ economy has still been fairly resilient even with a 50% drop in dairy prices.

10. Demonstrated that the Unitary Plan would fail in densification by bringing forward 91 Special Housing Areas which is essentially the Unitary Plan brought forward.

11. Dropped Helen Clark’s Foreshore and Seabed Act that was in contravention to UN Tribal Land rights charter and introduced Customary Title and gave recognition to Maori traditional land use rights.

12. Gave significant tax relief to Lord of the Rings, Hobbit and other movie enterprises to film and showcase the beauty of NZ.

13. China Free Trade Agreement signed, Korea Free Trade Agreement signed. TPP Free Trade Agreement with 12 countries signed involving New Zealand, Australia, Brunei Darussalam, Canada, Chile, Japan, Malaysia, Mexico, Peru, Singapore, the United States and Viet Nam subject to Parliament approval.

14. Decimated Labour by offering Shane Jones a job.

15. Disappointed Dr Russell Norman at the last election with the Green Party votes dropping to 10% when he was hoping for 15% and therefore resigning from the Green Party.

16. Put up GST to 15% and dropped the top tax rate from 38% to 33%.

17. New Space station in Gisborne launching satellites into space without any fuss from the US, quite a different reaction from the US from North Koreas similar launch into space.

etc etc etc

LikeLike

One could agree and disagree with various items on that list, but I’m not sure what it has to do with either the post or earlier comments on it?

LikeLike

Oh ok we are not talking about the government but of Wheeler being a poor public servant. Off topic. Wheeler, I must give some credit does move things fairly quickly. Mostly I think we has done a great job. Where he has bombed out was when he moved interest rates up too fast in anticipation of a non existent inflation and when the big drivers were Dairy, a commodity product subject to high risk price fluctuations and a Christchurch rebuild which is disaster recovery. Both industries highly susceptible to interest rate rises and almost 100% dependent on debt to generate activity. Talk about trying hard to kill the golden goose.

LikeLike