On average, over time, one would expect the real exchange rate of a more poorly-performing country to depreciate against that of a better-performing country.

There is a whole variety of strands to a possible story about why one might expect to see such a relationship, and for why it would be helpful for the more poorly-performing country for such a depreciation to occur. A less well-performing country will typically have found its firms less well able to compete in international markets (than those of the better performing country). That, in turn might reflect a less attractive tax and regulatory environment, less real productivity growth, or changing demand patterns so that the world wants more of what the more successful country produces and less of what the less successful country produces. Or it might even be about natural resource discoveries – a country that discovers major new resources (eg oil and gas) just has more stuff that the rest of the world wants, and with good institutions such a country will tend to outperform other countries for a (perhaps quite prolonged) period. And the citizens of a faster-growing country will rationally anticipate strong future income gains, increasing their consumption demand relative to the trajectory of consumption demand in the less well-performing economy.

I’ve illustrated previously that one of the striking stylized facts about New Zealand is that although our economic performance over the last 60 or even 100 years has been pretty disappointing by global standards, there has been no depreciation in our real exchange rate relative to those of other advanced economies. No wonder our tradables sector has struggled.

This post is really just about illustrating the point by reference to one other particular small commodity exporting country, Norway.

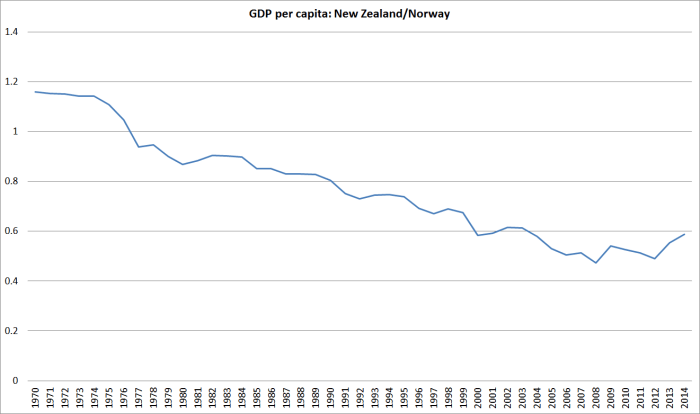

For the first 100 years or more of modern New Zealand, no one doubted that per capita incomes in New Zealand were much higher than those in Norway. New Zealand was one of the great economic success stories, while Norway struggled, and exported a lot of people, especially to the United States. On the Maddison numbers, GDP per capita in New Zealand in 1870 was more than twice that in Norway. By 1910, when New Zealand GDP per capita is estimated to have been the highest in the world, the margin was even more in our favour.

These days, GDP per capita in New Zealand is not much more than half that in Norway (and the NNI per capita gap is even larger). New Zealanders work long hours per capita, and our real GDP per hour worked is estimated to be only about 45 per cent of that in Norway. Over the last few years, we’ve done a bit better than Norway, but the multi-decade trend has been strongly downwards.

Here, using the OECD database which has estimates back to 1970, is New Zealand GDP per capita relative to Norway’s (in current prices, using current PPP exchange rates). These are really large declines. Back in the early 1970s we had incomes about the same as those of Norwegians.

Norway began to pull away from other OECD countries when its large oil and reserves began to move into production in the 1970s. We, on the other hand, suffered in the 1970s from a deep decline in the terms of trade, and new access restrictions on our major export products.

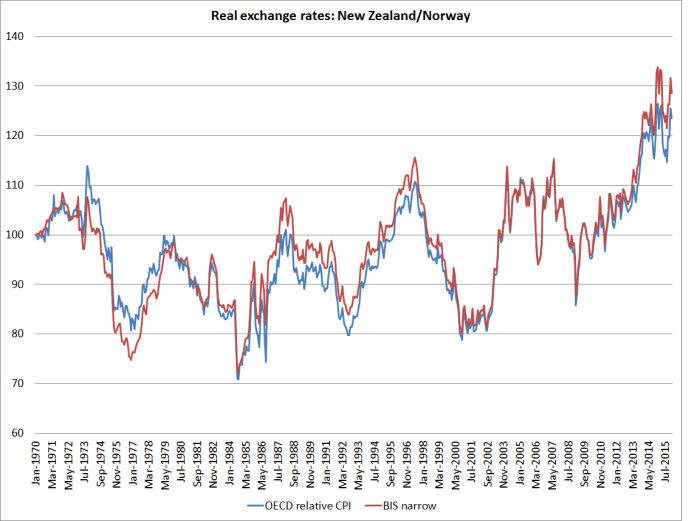

And yet here is a chart showing New Zealand’s real exchange rate relative to that of Norway since 1970. I’ve shown two, very similar, series – one is the OECD’s relative consumer prices index, and the other is the BIS’s narrow real exchange rate measure.

Our real exchange rate (in particular) has been quite variable – Norway’s has mostly been materially more stable – but over the whole period there has been no trend whatever in the ratio of our real exchange rate to theirs (and in the last few years, New Zealand’s real exchange rate has risen a lot relative to Norway’s).

Using the OECD’s relative unit labour cost measure produces a slightly more encouraging picture for New Zealand – but if there has been a trend decline at all, it has been quite small, compared with the magnitude of the deterioration in New Zealand’s economic performance (productivity, GDP per capita, usuable natural resource endowments).

Why has it happened? Well, it is Saturday and I’m not planning to write an extended essay. But my thesis is that it is a combination of things Norway has done, and things we have done.

On the Norwegian side, wisely or otherwise, much of the oil and gas revenues – mostly accruing to the Crown – were diverted into the Petroleum Fund, and saved for a later day. Norway has net government financial assets of around 250 per cent of GDP – a figure that was less than 50 per cent only 20 years ago. And there hasn’t been a large private sector offset Norway’s positive net international investment position is now some 200 per cent of GDP.

What that has meant is that quite a large proportion of the new income earned in recent decades has not been spent. And income not spent does not put upward pressure on the prices of non-tradables goods and services relative to those of tradables (another definition of the real exchange rate). Norway has experienced some of that pressure – Oslo is an expensive city – but a lot less than they would have without the huge savings rates.

Since the early 1970s, our government debt position hasn’t changed much – it has gone up and down – but was pretty low at the start of the period, and is pretty low now. Our NIIP position has gone in the opposite direction of Norway’s, even though they were earning lots of (initially unexpected) income, and we were experiencing repeated disappointment. On best estimates, our NIIP position was around -10 per cent of GDP in the early 1970s, and has been fluctuating around -70 to -80 per cent of GDP for the last couple of decades.

The Norwegians haven’t spent a larger share of their income even as their growth prospects improved, and we haven’t saved a larger share of ours even as our growth prospects deteriorated. Neither choice is necessarily better than the other, but their choice tended to weaken their real exchange rate (all else equal) keeping more non-oil tradables firms competitive, and our choices tended to strengthen our real exchange rate, making it hard for the tradables sector to grow much. For us, it tends to reinforce our decline.

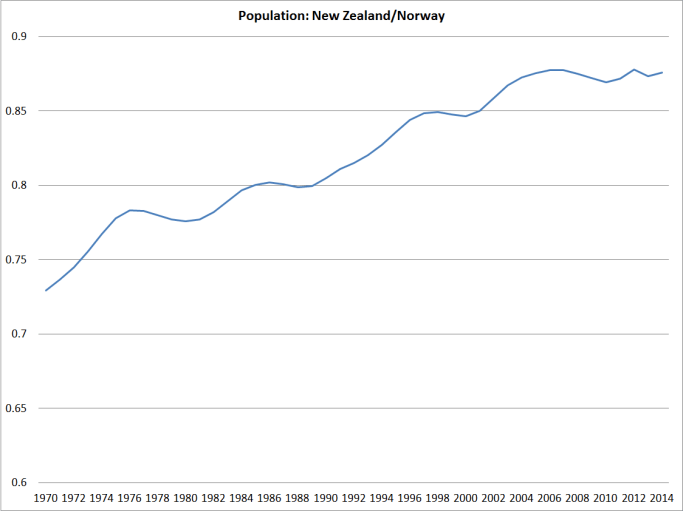

And then there are population choices. When migration works well, it usually complements economic success that was already underway. Rapid population growth, all else equal, tends to put upward pressure on a country’s real exchange rate – it involves a high demand for non-tradables, putting upward pressure on non-tradables prices relative to those of tradables (set globally). Norway’s population growth rate has increased quite a bit in the last decade, but over the full period since 1970, here is the chart showing the ratio of New Zealand’s population to that of Norway.

Our population – in a country that has had one of the worst performances of any advanced country – has grown materially faster than that of Norway, one of the most successful countries in the advanced world. Not usually a recipe for success – in a family, or at a national level.

I don’t believe in population policy – people should be free to have as many, or as few, kids as they can afford, and it should be no concern of governments – but immigration policy is a different matter. Our population has grown faster than that of Norway almost entirely because successive National and Labour governments have chosen to bring so many non-New Zealanders into the country (more than offsetting the upsurge in those leaving, mainly for Australia). Doing so has helped impede the sort of the sustained downward adjustment in the real exchange rate one would have expected if governments had simply stayed out of the way. It has made even harder for New Zealand to turn around the decades of economic decline.

It just looks like a wrongheaded policy, foisted on us – at our expense, without seeking our endorsement – by a succession of bureaucratic and political elites (different party labels or none, but similar ideologies and mindsets) who can offer barely a shred of evidence in support of the success of their strategy.

We can’t change the fact that Norway got oil or gas, and nor would we wish to, or begrudge them their good fortune. But it is pretty extraordinary that over 35 years when they’ve done so well and we’ve done so badly, there has been no change in our real exchange rate relative to theirs. At our end of that relationship, it is as if governments have set out to stop the adjustment happening. It wasn’t their conscious intent, but after this long lack of conscious intent makes them no less culpable.