The Reserve Bank’s quarterly survey of expectations results were released the other day. As a reminder, it is a survey of business people, sector leaders, and quite a few economists. The vision has always been that the survey should capture some mix of informed people and people who might influence actual behavior – whether through their own business transactions, or through their commentary or advice to others. There is a sample pool of about 100 potential respondents, and they typically seem to get about 65 or 70 replies each quarter. Some criticize the survey for its small sample, but for what it is trying to do, in a small country, it has never seemed too bad to me. It is, after all, asking for numerical answers to quite a bunch of macroeconomic questions. I know that when I fill it in, I sometimes have to go back to the data to check what the latest reported numbers were – not carrying QES wage inflation data in my head.

For inflation expectations specifically there are other surveys with larger samples. ANZ provide their long-running Business Outlook survey, and their newer survey of household expectations, and the Reserve Bank will release its latest survey of household expectations next week. At the other extreme is the (inaccessible to the general public) AON survey, designed primarily to provide inputs for actuaries evaluating pension funds. They ask about, inter alia, longer-term inflation expectations, but they ask only a handful (perhaps 7) economists.

I’ve never been quite sure what to make of inflation expectations measures. Inflation expectations play a significant, and quite plausible, role in conventional macroeconomic models. The difficulties come with mapping the data we have available with the concepts in the models. For a start, what horizon matters? In principle, 10 or 20 year ahead expectations sounds interesting, abstracting from all the short-term noise, whether around taxes and government charges, petrol prices, or even swings in the exchange rate. Then again, how many people sign up to 10 year nominal contracts? No one sets wages or selling prices that far ahead. And while plenty of bonds are issued with long maturities, when corporates issue them they typically seem to swap back to floating rates. So 10 year ahead expectations probably provide some useful information about how confident people are that, say, the framework will hold or be delivered on, over 10 years, but I doubt they make very much difference at all to this year’s inflation rate, or the challenges a central bank faces in meeting its inflation target over the next couple of years. I don’t know much about the politics of the next 20 years, but if forced to write down a number for average inflation over the next 20 years I might still write down 2 per cent. But with huge error bounds….and grateful that nothing rests on it and that my pension is inflation indexed.

Shorter-term expectations matter more. But not too short. Quarter or year-ahead expectations are influenced by specific stuff people know about – relative price changes and administered taxes and charges. In trying to make sense of inflation expectations, analysts are typically trying to look through those effects, to get a sense of the “norms” people have in mind when they set selling prices, negotiate wages, and make decisions to borrow or save. If firms have in mind a benchmark inflation rate of, say, 1 per cent, then when they come to review their pricing schedules – perhaps every six or twelve months – pricing adjustments are likely to be different (lower) than if firms had in mind a benchmark or normal inflation rate of 2.5 per cent. Same goes for wage negotiations. And for how potential borrowers react to any particular nominal interest rate. When those norms are above the inflation target, it can be hard to get actual inflation down to target – more interest rate pressure is needed, than otherwise, to deliver the desired inflation rate. And vice versa. Two year ahead expectations have often been seen as a reasonable horizon to focus on for these purposes – far enough that it gets beyond most (but not all) of the immediate noise, but close enough that it is more or less within the planning horizons of many. In the latest RB survey, for example, the actual question asked in early February 2016 was about the annual inflation rate for the year to December 2017. Halfway through that year respondents are asked to focus on is only 16 months away. (Similarly, it was pleasing that when the ANZ launched a household expectations survey they asked about two year ahead expectations).

If, in principle, measures of two year ahead inflation might usually give one a steer on the “pricing norms” that firms and households are operating on (at least implicitly), there is still the matter of whether the answers to survey questions actually give us the information we really need. As I’ve noted before, for example, the ANZBO survey and the Reserve Bank household survey measures have consistently, over decades, been materially above actual average inflation. In the 20 years the RB household survey has been running, mean expectations have been just over 1 per cent higher than the average inflation outcome. Does it mean households really didn’t believe the Reserve Bank would do it job? Does it mean those are the inflation rates people implicitly contract on? We simply don’t know (at least without a lot more formal research). There is no incentive for people to invest any time or effort in responding to one question in a substantial telephone survey – whereas they might well be when they ponder taking out a mortgage, or negotiating a pay increase.

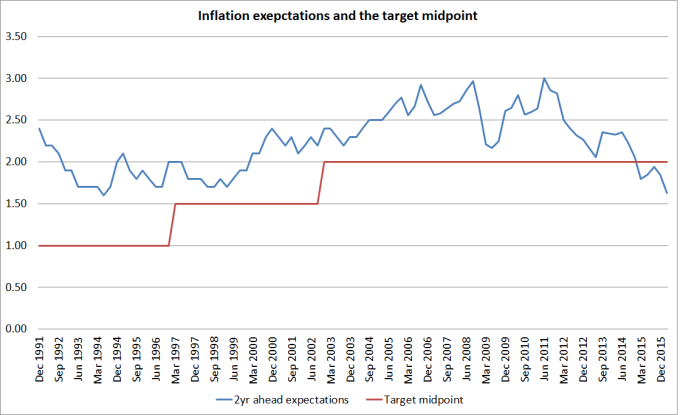

All of which is a roundabout way of getting to the point that historically the Reserve Bank has put most weight on the two year ahead inflation expectations measure from the Survey of Expectations. And it has done so because (a) there is now a good long time series (back to 1987), (b) it fits the prior that, typically, it will be horizons just beyond the immediate noise that matter, given that most contracts reprice at least every year or two, and (c) because historically it had a mean which seemed to align quite well over time with actual inflation. One way to see this is to compare the two year ahead expectation with the Bank’s preferred sectoral factor model indicator of core inflation (remember what I said yesterday – whatever the potential problems, for historical periods it is probably as reasonable as any measure, effectively smoothing through the noise in headline inflation).

So what actually happened in the most recent survey? Two year ahead expectations fell by 0.22 percentage points to 1.63 per cent [1]. Relative to the midpoint of the inflation target, that is the lowest in the history of the survey. That isn’t all a bad thing – despite the rhetoric suggesting we were crazed mechanistic inflation zealots, actually under both Don Brash and Alan Bollard inflation had averaged higher than the successive target midpoints, and expectations (in this survey) seemed more or less consistent with that. But we don’t have a price level target, and if expectations start undershooting the target that is pretty undesirable as well.

The size of the fall in inflation expectations wasn’t unprecedented, but it was pretty large for this (not overly noisy) series. In the period since low inflation became the norm (say since 1992) the only materially larger quarterly falls were (a) in the depths of the 2008/09 recession, and (b) in March 2012, when (post GST) the headline inflation rate had just fallen, in a single quarter, from 4.6 per cent to 1.8 per cent.

So this fall will have got the attention of the Reserve Bank, its analysts and forecasters. It can’t really have been expected – only 2 weeks ago the Governor told us explicitly that “survey measures of inflation…are now consistent with inflation settling at 2 per cent in the medium term”. That was arguable, at best, previously. It doesn’t really wash at 1.63 per cent – and the prospect of further falls from here.

In the internal debate in the Bank, some will try to dismiss the latest fall as “just about petrol prices”. Inflation expectations measures do respond, to some extent, to headline inflation, some seem “excessively” responsive to petrol prices, and even this two year measure (of informed respondents) is a bit sensitive to headline movements. But, as I have pointed out on several occasions, the latest annual CPI inflation rate excluding petrol was only 0.5 per cent. The more internationally conventional ex food and energy measure of inflation was only 0.9 per cent. So if headline inflation is influencing two year ahead expectations (a) that seems quite reasonable – it looks as though there is some information in trends in the headline rate, and (b) nobody much seems to expect headline inflation (including or excluding petrol) to pick up soon. It looks as though respondents are just gradually giving up on the Reserve Bank’s story that inflation is heading back to 2 per cent any time soon. It should be doubly sobering for the Bank that this comes in a survey in which responses to the other questions are not uniformly bleak: large falls in inflation expectations have usually gone hand in hand with more pessimistic GDP growth expectations, but in this survey those expectations have actually risen a little.

If people more generally – not just these respondents – are giving up on the Reserve Bank story, that will make it materially harder to get inflation back to target.

In one sense, it often seems wrong and excessively “mechanistic” to put too much weight on a single survey, and of 65 people – it often did to me, when I sat around contemplating the survey results and wondering what OCR advice to offer successive Governors. And in isolation that would be fine. But it isn’t the only information we have – rather, if anything, it is somewhat belated confirmation that the persistent undershoots of the inflation target have changed how people are thinking about prospects for inflation in New Zealand. I suspect the Reserve Bank, perhaps rather grudgingly, will come to the same conclusion.

Recall what Mario Draghi, head of the ECB, said in the speech I discussed the other day

… in a context of prolonged low inflation, monetary policy cannot be relaxed about a succession of supply shocks. Adopting a wait-and-see attitude and extending the policy horizon brings with it risks: namely a lasting de-anchoring of expectations leading to persistently weaker inflation. And if that were to happen, we would need a much more accommodative monetary policy to reverse it. Seen from that perspective, the risks of acting too late outweigh the risks of acting too early.

And it is not as if New Zealand monetary policy has somehow already got ahead of the problem. If the two year ahead measure is a reasonable proxy for the inflation norms now abroad in New Zealand – and it may yet prove too high – real interest rates have actually risen over the last couple of years.

The Reserve Bank lists three lending rates on its main retail rates page: a business lending rate, an SME rate, and new customer floating mortgage rate. In nominal terms, all are almost exactly now where they were at the start of 2014 (just before the OCR tightening cycle began). Inflation expectations, by contrast, are 70 points lower than they were then. With an unemployment rate above any measure of NAIRU, and inflation persistently below target, rising real interest rates have not obviously been something this economy needed. Retail deposit rates are lower than they were two years ago – by even they are no lower in real terms. And as funding spreads are rising – as they appear to have been recently, reflecting market unease about banks internationally – all else equal, the pressure on retail rates over the period ahead will be upwards not downwards.

And all this is before we focus on the continuing high exchange rate, the continuing weak commodity prices, and the growing stress persistently weak dairy returns are going to be placing on demand and activity (even if they aren’t necessarily a threat to the soundness of our banks). Let alone the worsening global situation.

And, of course, there are market measures of implicit inflation expectations (from the difference between indexed and conventional bond yields). These are weakening everywhere, but a chart someone sent me yesterday highlighted that the fall has been particularly sharp in New Zealand. As of yesterday, a 10 year conventional bond had a yield of 3.06 per cent, and a 2025 inflation indexed bond was yielding 2.12 per cent. That gap is now less than 1 per cent (and look how far it has fallen this year so far).

These aren’t perfect proxies, and bond investors’ expectations don’t directly affect (CPI goods and services) pricing now, but I don’t think central banks – ours in particular – can afford to be indifferent to message from bond markets: people with money on the line are no longer acting as if they think inflation is going to be near target on average over the next decade. They might be wrong, but why would central banks be so confident that those investors are wrong – especially when central banks, ours foremost among them, have themselves been persistently surprised by how weak inflation has been. In part, in turn, that has been because central banks – ours among them – have been persistently focused not on doing “whatever it takes” to create confidence that inflation targets will be delivered, but on doing as little as they can away with, perennially focused on “normalization” and some long-term benchmarks of where, surely, interest rates have to get back to one day.

There is a story abroad – I saw it in a commentary from one of the local banks yesterday – that low inflation is good and inevitable. It certainly isn’t inevitable here – looser monetary policy would, for example, lower our exchange rate generating additional resource pressure over time. And it isn’t good either. The story seems to go that structural features are driving price levels down. But remember that productivity growth rates globally have been falling, not rising. And stories about global overcapacity tell you mostly about demand having failed to keep up with supply capacity: discretionary monetary policy exists to influence demand. The indifference to what is going on is hauntingly reminiscent of some of the discussion and debate during the Great Depression – when there was excess supply capacity (reflecting, eg, past heavy investment in agriculture), even amid rapid ongoing productivity gains – and a sense in too many circles, for too long, that nothing very much should be done about monetary policy and the monetary system.

[1] For what it is worth, when I completed the survey I did not lower my two year ahead expectation from the one I recorded in the November survey. On both occasions, I wrote down 1.4 per cent.