Some of the discussion around New Zealand’s low inflation rate, and the question of what the Reserve Bank should do (or have done) about it, has a strong element of “it has been awfully hard to keep inflation up near target, not just here but everywhere in the advanced world”. In other words, we shouldn’t be too critical of the Reserve Bank because they have just been struggling with the same problems everyone else has faced. Everyone, perhaps, except Norway?

Inflation is, ultimately, a monetary phenomenon. But monetary policy works and responds within a wider economic climate, where there can be all sort of other pressures at any one time. Sometimes those other pressures work in the same direction as monetary policy, and sometimes in the opposite direction – in those cases we might say it is (respectively) a bit easier or a bit harder than usual to deliver on inflation goals. People have advanced various stories about these sorts of pressures to help explain both the rise in inflation in the advanced world in the 1960s and 70s, and the subsequent sharp decline. Changed attitudes of monetary policy decision-makers contributed in both cases, but those attitudes weren’t the only factors.

Today I don’t want to try to illustrate that point over history, but rather to look at the pressure/shocks/pre-conditions that might have made it a little easier, or a little harder, for monetary policymakers in OECD countries over the period since just prior to the 2008/09 recession.

What about the pre-conditions?

Many advanced countries have been, or felt they were, constrained in doing more with monetary policy by the near-zero lower bound on nominal interest rates. Thus, going into a period with lots of downward pressure on the inflation rate it helped, all else equal, to have high nominal interest rates. High nominal interest rates leave plenty of room to cut. Going into the 2008/09 recession and aftermath, New Zealand had the third highest interest rates in the OECD – only Iceland and Turkey had rates higher than New Zealand. That wasn’t just a reflection of some last minute RBNZ madness in driving interest rates sky high. Our interest rates have been above those in most of the rest of the OECD for a long time.

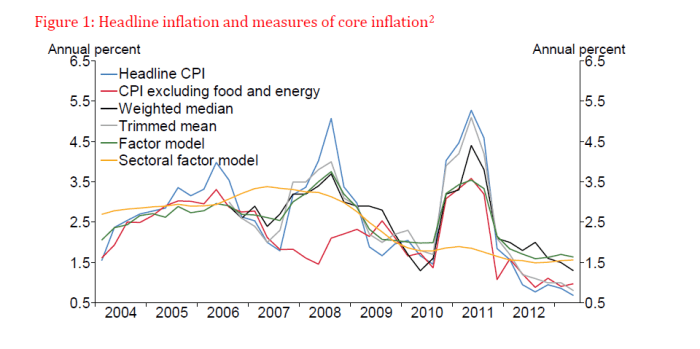

And going into the period of the recession and beyond, we had also had quite high inflation. I’m not going to attempt to reconstruct the chart here, but work done at the Reserve Bank showed that among inflation targeting countries New Zealand was quite unusual in that our inflation outcomes had typically run above the midpoint of our (successive) target ranges. Other countries had historically averaged nearer the midpoint. Going into the recession, the Reserve Bank’s favoured measure of core inflation was actually above the 3 per cent top of the target range, and as this Reserve Bank chart I reproduced the other day illustrates, core measures had all typically been well above the target midpoint in the years leading up to 2008.

So we had higher inflation to start with (and inflation expectations fairly consistent with that high inflation) and more room to cut policy rates should that be required. Oh, and unlike half the OECD countries – members of, or pegged to, the euro – we had a floating exchange rate. Floating exchange rates increase a country’s ability to achieve its own inflation target whatever is going on elsewhere.

What about the fiscal pre-conditions? If government finances are in such bad shape that there is little effective choice but to run severely contractionary fiscal policy, it can make it a little harder for monetary authorities if those authorities are trying to keep inflation up, especially if the near-zero lower bound is in view.

One way of looking at the fiscal situation is to look at the cyclically-adjusted balances prior to the recession. Using the OECD’s measure, New Zealand’s average surplus over the years 2006 to 2008 was higher than those in almost every other OECD country.

Using data on the general government sector’s net debt, New Zealand’s position wasn’t quite as strong. But in 2007, we were one of the 12 countries where the government sector has less debt than financial assets, still one of the stronger positions among OECD countries.

Using data on the general government sector’s net debt, New Zealand’s position wasn’t quite as strong. But in 2007, we were one of the 12 countries where the government sector has less debt than financial assets, still one of the stronger positions among OECD countries.

So the pre-conditions looked pretty favourable for New Zealand to be able to keep inflation near target. If anyone was going to be able to do so, in a strongly disinflationary environment, our high starting inflation, high starting interest rates, and strong fiscal position meant New Zealand was well-positioned to do so.

Pre-conditions are one thing. But what about the shocks that each country faced?

Financial sector crises didn’t occur to same extent in all countries. I’ve shown this table before, classifying advanced countries by the extent of the increase in non-performing loans since 2007. Real wealth losses – whether borne by the government in bailouts, or by private creditors – make it harder to keep inflation up, all else equal. New Zealand is among the group of countries to the left of the table with the smallest increase in losses.

&Non-performing loans since 2007

Source: World Bank.

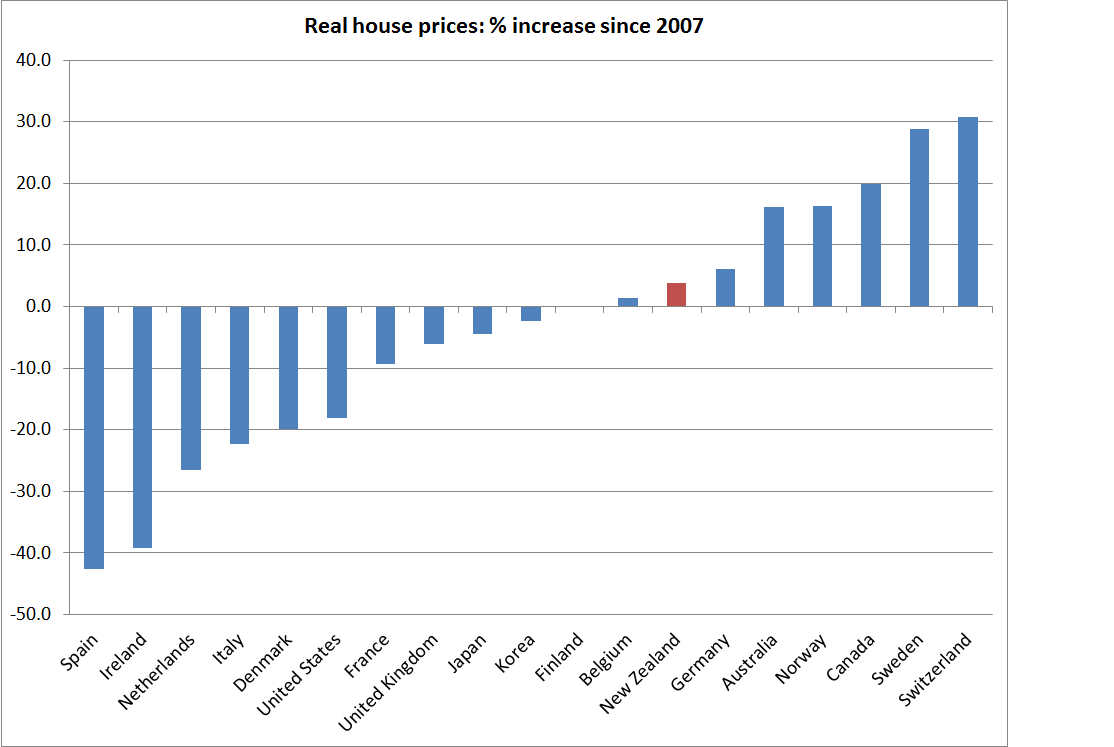

It is never clear how to think about the impact of house price falls – how much of it is a real wealth loss, given that we go on living in the same house and consuming the same flow of housing services? New Zealand did experience falling house prices during the recession, but as this chart I ran a few months ago illustrates, those aggregate losses have been fully recovered and, if anything, real house prices here have been a little stronger than those in the median OECD country.

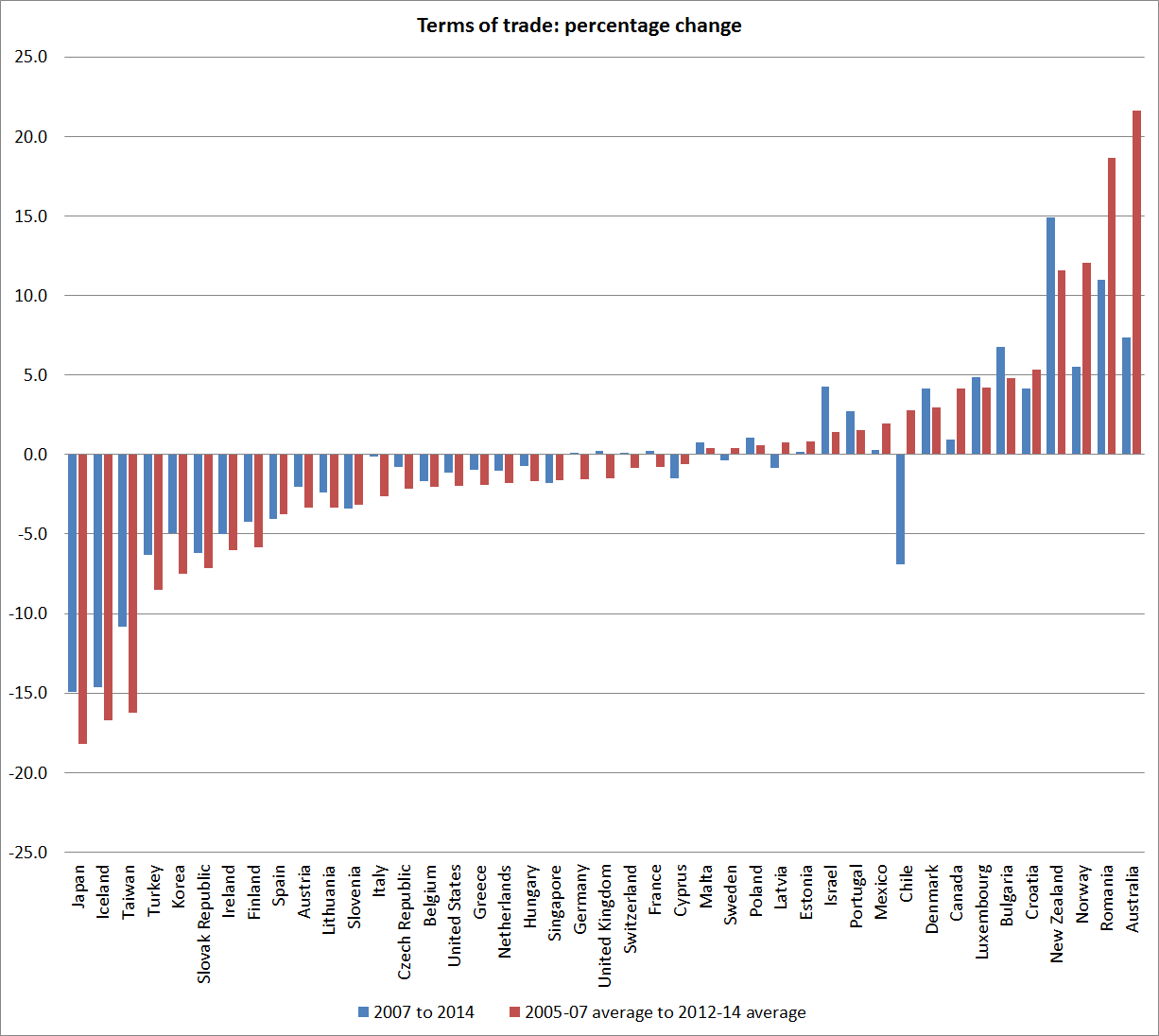

How about the terms of trade? For a country like New Zealand, the terms of trade are largely exogenous. A strong terms of trade boosts national incomes, supporting domestic demand (consumption and investment) whatever else is going on in the rest of the world. All else equal, if central banks are struggling to keep inflation up near target, they would prefer strong income gains, rather than the alternative, to support the efforts of monetary policy.

As this chart shows, New Zealand was among the handful of countries with the strongest terms of trade. Even now the terms of trade are around 10 per cent higher than they were over the years prior to the recession. That gave us an edge, all else equal, in keeping inflation up.

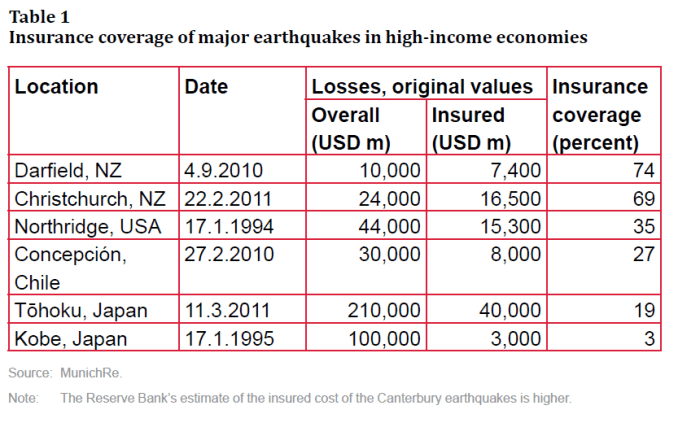

What about exogenous demand shocks? It is often hard to think of examples of these, but the repair and rebuild process associated with the Canterbury earthquakes is one. Other OECD countries have had to repair and rebuild after natural disasters – Chile and Japan both suffered from serious earthquakes. But the damage in Japan, as a share of GDP, was much smaller than the damage in New Zealand and Chile (in both cases up towards 20 per cent of annual GDP). And, as this table in recent Reserve Bank article highlighted again, what really marked New Zealand out was the extent of the insurance coverage of the losses – most of that, in turn, covered by foreign reinsurers, rather than by domestic institutions.

Earthquakes are awful, and often expensive, phenomena. But the activity associated with the repair and rebuild processes can be a substantial near-term boost to demand and activity. That is so even if all the losses are borne domestically – since people need a new house (or functioning water pipes) now, and might pay for it through higher savings over 40 years – but it is much more obviously so when foreign reinsurers bear the bulk of the cost. Activity needs to occur now, and someone external is paying for it. That provides a lot of support for demand. It could be quite troublesome if there was already a lot of inflation pressure, but – much as one would wish the earthquakes never occurred – it provides a lot of potentially helpful support for demand (reinforcing monetary policy) when other inflation pressures are weak.

Looking through the list of OECD countries, I can’t see any countries that have had anything like that sort of large exogenous demand shock in the last decade or so. Perhaps I’m missing some, and if so please feel to mention those case in the comments.

In general, declining population growth rates tend to be associated with relatively weak demand pressures. That can be helpful when other demand and inflation pressures are strong, but more troublesome if other inflation pressures are weak – as they have been, across the advanced world, in recent years. But as it happens, New Zealand has had one of the faster population growth rates among OECD countries in the last decade or so, and in the last couple of years has had the fastest population growth we’ve experienced for 40 years.

Bringing it all together, thinking about things that have made it easier or harder for monetary policy to do its job and keep inflation up around target in recent years, relative to the situation in other advanced countries, we’ve had:

Favourable pre-conditions (things already in place in 2008):

- high starting inflation (relative to target)

- high starting interest rates

- a floating exchange rate

- low net public debt

- a strong flow fiscal position

And favourable idiosyncratic shocks (or shocks avoided that others faced):

- few direct financial crisis costs

- no large sustained fall in house prices

- a strong terms of trade

- a large exogenous demand shock (earthquake repair process) largely externally-financed

- continued strong population growth

None of this is to deny that the global environment – eg the declining productivity and population growth I highlighted yesterday, and global oversupply in various markets reflecting past excess investment associated with China – might have made it more difficult, perhaps materially more difficult, generally for central banks to keep inflation up to around their respective targets.

But among advanced countries, it is difficult to think of any where it should have been easier to have kept inflation up near target than New Zealand. Almost everything was going our way, and yet the Reserve Bank has consistently failed.

In any reasonable evaluation of the performance of an independent agency pursuing a target it does not control directly, one has to look at all the circumstances, not just at the bottom line, important as that bottom line often is. One could easily envisage an alternative New Zealand in which many of the factors in the list above might have been reversed. In such an environment, whatever else was going on in the rest of the world, one might not have been inclined to be very harsh in evaluating our own Governor had he persistently failed to keep inflation around the target. But in the environment the Governor and his advisers have actually faced in the last few years, it is difficult to acquit the Reserve Bank of responsibility for failing to achieve its primary goal. It was easier for them than for almost all their overseas peers, and yet they’ve failed. And no forecast I’ve seen suggests that situation is about to reverse rapidly.

The Reserve Bank published an article late last year on “Evaluating Monetary Policy”. I discussed it here, and included a link to another earlier article they had published on a similar topic. From the earlier article I highlighted a list of things the Reserve Bank’s Board (or the Minister) might want to take into account in evaluating the Governor’s performance, and perhaps considering any reappointment.

Some of the items the Reserve Bank’s Board might be expected to concern themselves with in fulfilling the monetary policy monitoring role include:

- The processes the Governor uses to gather and interpret economic information.

- The choices the Governor makes in allocating resources areas of the organisation relevant to monetary policy (including judgements he makes on whether to seek more, or fewer, resources, when the five-yearly funding agreement is negotiated)

- The means the Governor uses to ensure that he is exposed to alternative perspectives.

- The quality of the people the Governor appoints to advise him on policy choices.

- The way in which the Governor applies section 3 and 4 of the PTA (dealing with deviations from the target range, and the avoidance of unnecessary instability).

- The way in which the Governor thinks about and responds to the uncertainties around monetary policy.

- The ability of the Governor to articulate the reasons for his policy choices, and his ability to convince others of his case.

- The processes the Governor uses to assess past policy and learn from experience.

- The stability through time in the Governor’s policy choices.

I’d now add to the list “the shocks and pre-conditions” the Governor faced over his or her term. On this occasion, it doesn’t really seem to help his case.