On average, over time, one would expect the real exchange rate of a more poorly-performing country to depreciate against that of a better-performing country.

There is a whole variety of strands to a possible story about why one might expect to see such a relationship, and for why it would be helpful for the more poorly-performing country for such a depreciation to occur. A less well-performing country will typically have found its firms less well able to compete in international markets (than those of the better performing country). That, in turn might reflect a less attractive tax and regulatory environment, less real productivity growth, or changing demand patterns so that the world wants more of what the more successful country produces and less of what the less successful country produces. Or it might even be about natural resource discoveries – a country that discovers major new resources (eg oil and gas) just has more stuff that the rest of the world wants, and with good institutions such a country will tend to outperform other countries for a (perhaps quite prolonged) period. And the citizens of a faster-growing country will rationally anticipate strong future income gains, increasing their consumption demand relative to the trajectory of consumption demand in the less well-performing economy.

I’ve illustrated previously that one of the striking stylized facts about New Zealand is that although our economic performance over the last 60 or even 100 years has been pretty disappointing by global standards, there has been no depreciation in our real exchange rate relative to those of other advanced economies. No wonder our tradables sector has struggled.

This post is really just about illustrating the point by reference to one other particular small commodity exporting country, Norway.

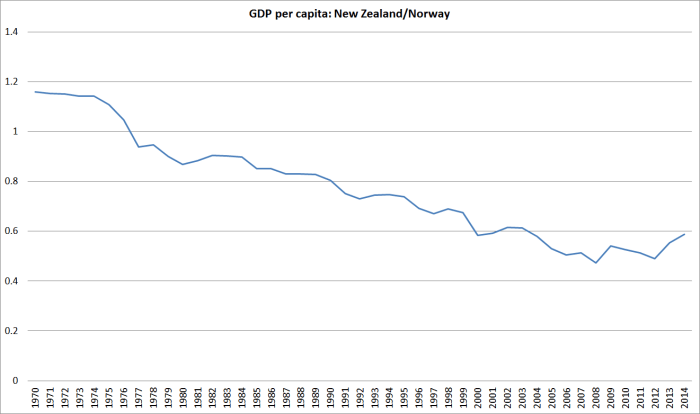

For the first 100 years or more of modern New Zealand, no one doubted that per capita incomes in New Zealand were much higher than those in Norway. New Zealand was one of the great economic success stories, while Norway struggled, and exported a lot of people, especially to the United States. On the Maddison numbers, GDP per capita in New Zealand in 1870 was more than twice that in Norway. By 1910, when New Zealand GDP per capita is estimated to have been the highest in the world, the margin was even more in our favour.

These days, GDP per capita in New Zealand is not much more than half that in Norway (and the NNI per capita gap is even larger). New Zealanders work long hours per capita, and our real GDP per hour worked is estimated to be only about 45 per cent of that in Norway. Over the last few years, we’ve done a bit better than Norway, but the multi-decade trend has been strongly downwards.

Here, using the OECD database which has estimates back to 1970, is New Zealand GDP per capita relative to Norway’s (in current prices, using current PPP exchange rates). These are really large declines. Back in the early 1970s we had incomes about the same as those of Norwegians.

Norway began to pull away from other OECD countries when its large oil and reserves began to move into production in the 1970s. We, on the other hand, suffered in the 1970s from a deep decline in the terms of trade, and new access restrictions on our major export products.

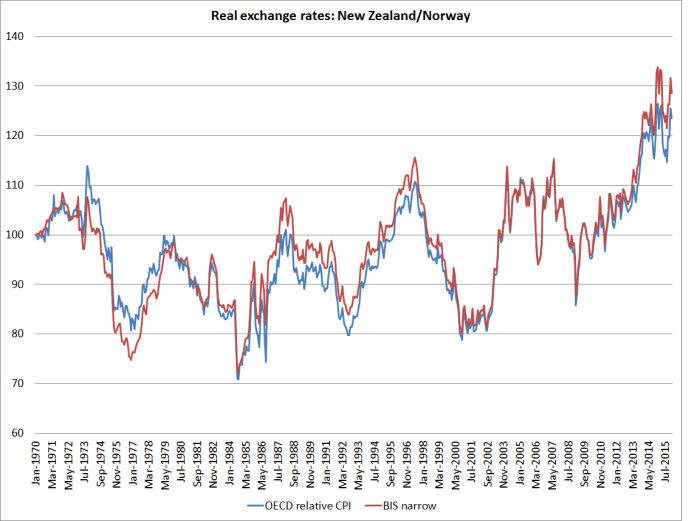

And yet here is a chart showing New Zealand’s real exchange rate relative to that of Norway since 1970. I’ve shown two, very similar, series – one is the OECD’s relative consumer prices index, and the other is the BIS’s narrow real exchange rate measure.

Our real exchange rate (in particular) has been quite variable – Norway’s has mostly been materially more stable – but over the whole period there has been no trend whatever in the ratio of our real exchange rate to theirs (and in the last few years, New Zealand’s real exchange rate has risen a lot relative to Norway’s).

Using the OECD’s relative unit labour cost measure produces a slightly more encouraging picture for New Zealand – but if there has been a trend decline at all, it has been quite small, compared with the magnitude of the deterioration in New Zealand’s economic performance (productivity, GDP per capita, usuable natural resource endowments).

Why has it happened? Well, it is Saturday and I’m not planning to write an extended essay. But my thesis is that it is a combination of things Norway has done, and things we have done.

On the Norwegian side, wisely or otherwise, much of the oil and gas revenues – mostly accruing to the Crown – were diverted into the Petroleum Fund, and saved for a later day. Norway has net government financial assets of around 250 per cent of GDP – a figure that was less than 50 per cent only 20 years ago. And there hasn’t been a large private sector offset Norway’s positive net international investment position is now some 200 per cent of GDP.

What that has meant is that quite a large proportion of the new income earned in recent decades has not been spent. And income not spent does not put upward pressure on the prices of non-tradables goods and services relative to those of tradables (another definition of the real exchange rate). Norway has experienced some of that pressure – Oslo is an expensive city – but a lot less than they would have without the huge savings rates.

Since the early 1970s, our government debt position hasn’t changed much – it has gone up and down – but was pretty low at the start of the period, and is pretty low now. Our NIIP position has gone in the opposite direction of Norway’s, even though they were earning lots of (initially unexpected) income, and we were experiencing repeated disappointment. On best estimates, our NIIP position was around -10 per cent of GDP in the early 1970s, and has been fluctuating around -70 to -80 per cent of GDP for the last couple of decades.

The Norwegians haven’t spent a larger share of their income even as their growth prospects improved, and we haven’t saved a larger share of ours even as our growth prospects deteriorated. Neither choice is necessarily better than the other, but their choice tended to weaken their real exchange rate (all else equal) keeping more non-oil tradables firms competitive, and our choices tended to strengthen our real exchange rate, making it hard for the tradables sector to grow much. For us, it tends to reinforce our decline.

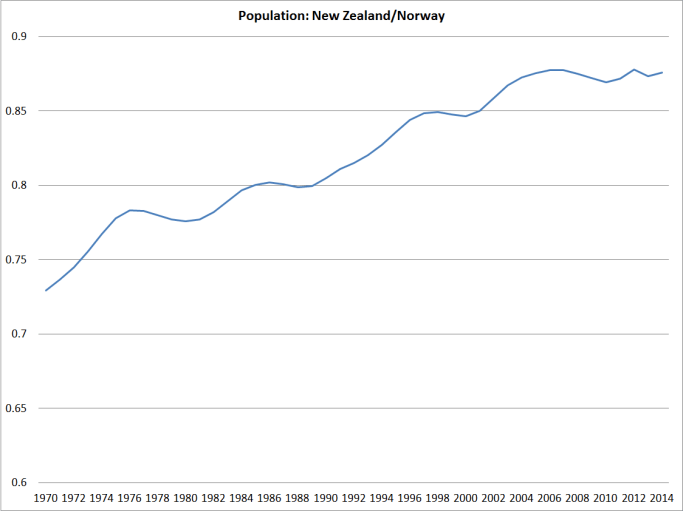

And then there are population choices. When migration works well, it usually complements economic success that was already underway. Rapid population growth, all else equal, tends to put upward pressure on a country’s real exchange rate – it involves a high demand for non-tradables, putting upward pressure on non-tradables prices relative to those of tradables (set globally). Norway’s population growth rate has increased quite a bit in the last decade, but over the full period since 1970, here is the chart showing the ratio of New Zealand’s population to that of Norway.

Our population – in a country that has had one of the worst performances of any advanced country – has grown materially faster than that of Norway, one of the most successful countries in the advanced world. Not usually a recipe for success – in a family, or at a national level.

I don’t believe in population policy – people should be free to have as many, or as few, kids as they can afford, and it should be no concern of governments – but immigration policy is a different matter. Our population has grown faster than that of Norway almost entirely because successive National and Labour governments have chosen to bring so many non-New Zealanders into the country (more than offsetting the upsurge in those leaving, mainly for Australia). Doing so has helped impede the sort of the sustained downward adjustment in the real exchange rate one would have expected if governments had simply stayed out of the way. It has made even harder for New Zealand to turn around the decades of economic decline.

It just looks like a wrongheaded policy, foisted on us – at our expense, without seeking our endorsement – by a succession of bureaucratic and political elites (different party labels or none, but similar ideologies and mindsets) who can offer barely a shred of evidence in support of the success of their strategy.

We can’t change the fact that Norway got oil or gas, and nor would we wish to, or begrudge them their good fortune. But it is pretty extraordinary that over 35 years when they’ve done so well and we’ve done so badly, there has been no change in our real exchange rate relative to theirs. At our end of that relationship, it is as if governments have set out to stop the adjustment happening. It wasn’t their conscious intent, but after this long lack of conscious intent makes them no less culpable.

Interesting, so the GDP per capita and population graphs have a good negative correlation? Would be very interesting if you could demonstrate similar results for other countries had the same relation and that immigration really was bad.

A couple of additions to your comments. 1) I assume the Petroleum fund is mainly invested outside Norway, so that money hasn’t even gone into Norway, reducing pressure on their exchange rate. 2) When dairying/farming has done well, not only do we bring the earnings into the country, but farmers bid up the value of farms and bring in more money from overseas as borrowings to fund farm purchases and put upward pressure on the exchange rate.

LikeLike

Yes, the Petroleum Fund is mostly invested internationally.

On your first para, remember that my claim isn’t that immigration is generally bad. When it complements economic success it is a clear win for the migrants, and at little or no economic costs to the “natives”, and for those who value “diversity” for its own sake there may be other benefits too. Immigration to NZ pre WW1 wasn’t inconsistent with us having the highest per capita incomes on earth – so strong were the gains from the new dairy and refrigerated shipping technologies – and probably even had economc benefits for Maori (although against that some of them might cite sovereignty/cultural dominance concerns). My argument is simply that a country that is in relative decline (a) is unlikely to be able to reverse that decline through immigration (unless it managed to find truly exceptional people, who didn’t have better opportunities elsewhere, and (b) that such a country persisting with a large scale immigration programme, when it otherwise has pretty good policies, probably does come at the expense of the natives. In NZ specifically, the argument is reinforced by the distance/location arguments, that mean that a largish population is never likely to be sensible here in a way that it might be in Singapore or Belgium (say).

LikeLike

It is not large scale immigration when it is replacement. Lets stick to facts rather than innuendo please.

LikeLike

The immigration programme – the ability of non-citizens to move to NZ – is large. That isn’t in contest – Treasury and MBIE accept the description. The debate should turn on the implications of that policy choice. You think it is benign because to some extent the newcomers “replace” those NZers who left. I think that just compounds the problem – govts foisting onto us an outcome quite different from what private choices were in the process of producing.

LikeLike

IMPRESSIVE GAINS

Yesterday’s strong growth in international visitor numbers has enabled officials to value the benefit to the New Zealand economy. Data released today shows that international visitor spending has increased by +31% to NZ$9.7 bln in 2015. That is an impressive NZ$2.3 bln increase. Australia, China and the USA were the main drivers of the rise, in that order.

http://www.interest.co.nz/news/80315/review-things-you-need-know-you-go-home-friday-fixed-rate-cuts-good-trade-data-visitor#comment-844458

Perhaps your focus should be on the record 3 million plus international visitors and growing each and every year as a larger and more credible culprit that is keeping the NZD on the up and putting pressure on resources. Your pre-occupation on net migration gains of 67k made up of mainly international students and returning kiwis is close to perpetuating rumour mongering rather than a professional rendering of facts.

LikeLike

MIchael, you have not demonstrated the link between actual real migration and NZ productivity poverty. The high NZD is not due to migration but due to international speculation off a back of a RBNZ governor that have taken a hawkish interest rate policy based on some imagined values over the last 30 years.

Census statistics have indicated that NZ Stats tend to over exaggerate population growth numbers eg we celebrated Auckland population at 1.5m and census night proved that Auckland population was well down from 1.5m in 2013. We do know that international students and international tourist add to the record net migration numbers. It is this contribution by International fee paying students and international tourists that have provided some resilience in the diary price collapse. We do know that many international students eventually do apply to live in NZ to work and take on permanent residency. But most do eventually depart. Over the years I have met many many foreign students, have had many many migrant friends. I am very often at the airport bidding them farewell. They are less likely to stay permanently. There is only a 1 in 20 chance that they would stay. Perhaps a few short years but our city is far too small for career development with more a branch office setup rather than a city for large corporates that allow for career development.

The numbers indicate that population growth is largely by natural birth and therefore immigration is a replacement policy. Replacement means zero growth from migration and therefore immigration is not a NZ problem. It is a Auckland problem due largely to a single international entry point.

We also managed to build our largest city on the smallest piece of dirt in NZ and then we put up 4 level height limits due to 57 sacred mounts and pretty picture visual impact and no one builds 4 level buildings. It is not cost effective to build 4 level buildings ie no profit margin.

LikeLike

I won’t respond to your whole comment, as we part company in the first para. There is no – repeat, no – evidence that the RB has had monetary policy too tight for the last 30 years. Apart from anything else, until recently inflation had typically been above a quite internationally conventional target. The RB has dealt with this issue repeatedly over the years in documents that are on the website.

LikeLike

Economists at country’s biggest bank do u-turn; now see Official Cash Rate hitting 2%

1. a moderation in economic momentum now looks to be around the corner at a time when inflation is already low;

2. global unease – China has problems and they will be exported; and

3. structural shift in funding costs, which, if not compensated for by monetary policy, will accentuate decelerating economic momentum.

http://www.interest.co.nz/bonds/80331/economists-countrys-biggest-bank-do-u-turn-now-see-official-cash-rate-hitting-2

Note the 3rd reason which is the real reason, ie structural shift in funding costs, which means “oooops I have too much savings and I need interest rates to fall”

There was a failure by Bollard to recognise when he had pushed interest rate rises too far. The same mistake is being repeated by Wheeler. Failure to understand the global variables at play and we saw that with Brash, Bollard and now Wheeler and thus failure to adjust to those conditions. Just because economists do not understand and are blind does not mean there is no evidence.

LikeLike

I don’t know if you’ve read any of the novels of Karl Ove Knausgaard (they are excellent). Growing up in a small town in Norway in the 1970s was a lot like growing up in NZ. Of course they are now very different.

I take your point about immigration. But I also think Norway’s story illustrates that when a country expands its welfare state, removing much of the financial risk from everyday life, it makes sense for its leaders to think about how they will replace the lost precautionary savings. If New Zealand had an oil fund, people may well have declared it a giant hedge fund and distributed the proceeds to citizens. But I support the Oil Fund because I think it makes sense in the national context of Norway. Unlike you I also support the NZ Superannuation Fund.

LikeLike

Actually, I also largely support the Petroleum Fund in those unique circumstances. That said, I was once press-ganged at short notice into being a discussant at conference where a Norwegian senior official was speaking. I somewhat rashly asserted that in the long run Norway might regret ever having had oil. I was more under the thrall of the “resource curse” literature then than I am now, but I still think it is something of an open – if purely hypothetical – question.

LikeLike

The NZD is the 10th most traded currency in the world. It is ridiculous to think that Net migration gain of 67,000 which includes a whole lot of international students and returning kiwis that buy a lot of Warehouse cheapies is going to affect the NZD?? It is international speculation that drives the NZD. Nothing to do with migration.

LikeLike

The real exchange rate – emphasis “real” – is not (on average over time) determined in the fx market: it is the relative price of non-tradables goods to the prices of tradable goods. Tradable goods prices are determined in the international markets, where we have very little influence, but non-tradables goods prices are the outcome of domestic supply and demand pressures, of which population pressures are just one form (government spending is another key influence).

LikeLike

I would have thought that the $10billion spent by the 3 million plus, tourists would have a more credible impact than the net migration gain of 67k, made up largely of poverty stricken international students and redundant NZ mining workers? Your preoccupation with natural birth population growth rates as the reason for NZ productivity poverty really comes across as nonsense. If the RB abd the MBIE share this nonsense thinking then no wonder our interest setting is also nonsense. Garbage in you get garbage out.

LikeLike

Did I say anywhere that the RB, Tsy, or MBIE share my analysis of the economic impact of immigration in NZ? No, I didn’t.

As for the rest, I’m astonished that you can take from anything I’ve written that I have a “preoccupation with natural birth rates”.

No one compels you to read my material, or to comment, but if you do it might be more constructive and useful to actually engage with the substance of my arguments.

LikeLike

When immigration is replacement and population growth in NZ is by natural birth then your persistent argument that we have economic problems due to high immigration falls over on the first hurdle because population growth in and NZ is pretty much equal to the natural birth numbers and therefore if you look at the same argument in a different direction you are persistently arguing that population growth in NZ by natural birth is the cause of NZ productivity problems.

This then boils down to why would our top economists be so blindsided as you appear to be with what is a simple mathematical construct? ie x + y = a, therefore that equates to a – x = y. Hey don’t shoot the messenger.

LikeLike

No. Based on New Zealanders’ individual choices – partly a response to economic opportunities here – New Zealand would now have little or no population growth. We’d have a rate of natural increase a bit higher than those of most advanced countries, and a large (in the average year) outflow of NZers. The government undermines that adjustment by running a liberal immigration policy.

LikeLike

China which has a billion plus people and the Yuan is the 9th most traded currency compared to NZ’s, 10th placing with only 4.2 million people and our net migration of 67k made up of poor international students and poverty driven kiwis returning after having been made redundant in the mining sector in Australia is driving the NZD upwards does not add any credibility to your thesis. It is scary that Treasury and the MBIE would share your view.

LikeLike

Replacement is not high under any mathematical construct no matter how many equations you throw up in defense of your claim of imagined high migration numbers. Replacement equate to zero contribution from migration especially if your base assumption that a new migrant is the same as a kiwi that leaves NZ.

LikeLike

When I said they shared the view, my point was the description “we have one of the largest immigration programmes of any advanced country”. Much as I wish it otherwise, the don’t share my view of the econ implications of our immigration programme,

I’m not quite sure how the rest of the comment relates. If you are uneasy about how much NZD is traded, I’m happy to deal with that in another post one day (personally, i’m not partiucularly uneasy, although I suspect the volume of NZD trade would drop if our real interest rates were typically more similar to those in the rest of the advanced world).

LikeLike

I guess an interesting question is whether the exchange rate should be considered a variable that causes economic outcomes or reflects economic outcomes? Given NZ relies on the market to determine the price of its currecy, it is even more extraordinary that those in this market seemingly have had little concern about relative ‘fundamental’ economic performance in this case. Higher real rates but weaker underlying economic developments is a contradiction which cannot last forever so fingers crossed the market doesn’t rapidly change its mind on the NZD as that could cause some undesirable economic outcomes.. …

LikeLike

Simultaneous processes at work of course in an general equilibrium system, but remember that “the market” has no interest (or need to be interested in) NZ’s long-term economic success or failure. All investors presumably care about is maximizing risk-adjusted returns, a process that should generate expected risk-adjusted returns (interest rate plus expected change in exchange rate) across countries that are pretty similar. My argument is that government policy has repeatedly prevented the sort of real adjustment that would be in NZers’ long-term interests. That would set up nasty future crisis risks if the intervention took the form of huge govt offshore borrowing (as at times in the past), but in the form of the last 25 years it mostly seems to expose us to slow continued relative decline. Some will argue that the housing market is the source of major vulnerability, but I’m skeptical of that – unless perhaps there was a huge reversal of immigration policy at much the same time as a big land use liberalization. In my view, that combination of measures would still be desirable in the long run……but transitions could be be nasty.

LikeLike

Thanks Michael. A bit of a head scratch as I would have thought those risk adjusted returns should – in the ‘long run’ – reflect relative real economic outcomes/trends. But I have always found the FX market a mystery so I’ll dust off some books to clear part of the fog…..!!

LikeLike

The UIP bit is set out in my 2013 paper (altho words not algebra). from a fixed income investor perspective, you can treat our interest rates as a given – whether it is excess demand for underlying productivity driving it – and then it is just a matter of the spot exchange rate adjusting to allow ex ante equalization of returns (ex post never happens, and doesn’t matter that much). For decades, the received expectation has been for the NZ exchange rate to fall.

LikeLike

….hmmm – capital flowing into NZ isn’t just invested in fixed income assets? (i.e. presumably not under conditions reflecting UIP): agricultural land, real estate, equity all have uncertain payoffs which requires expected return and risk guesswork. But I’ll reread your paper and think on……!

LikeLike

yes, agree not all capital is in fixed interest (tho equity pricing will include a risk-free rate). much of it, of course, is in the non-tradables sector, in which required/expected rates of return probably pan out. A skewed economy – not seeing growth in tradables – might not be v good for NZers in the long haul, but it doesn’t obviously lose investors money in any sort of crisis-prone way.

LikeLike

You describe net immigration as the result of “governments foisting onto us an outcome quite different from what private choices were in the process of producing” – but isn’t immigration just as much the result of private choice as is emigration? You make it sound as though the Government is deliberately dragging people here against their wills whereas in fact every immigrant comes and stays here because they want to come and stay here (and are prepared to go through a demanding and sometimes expensive process to do so).

Migration-driven population increase may not be an outcome you desire, but I’m not seeing that it can reasonably be portrayed as the result of Government’s interfering in private choices.

LikeLike

Yes, from the immigrants’ own perspective what you say is perfectly true. The perspective I’m talking about tho is that of resident NZers. In large numbers they have been choosing to leave for better opportunities abroad, which history and economics suggests tends to benefit those who leave and those who stay. The govt interferes with that adjustment process by actively seeking large numbers of other people to come to NZ.

LikeLike

[…] reiterated on Saturday that the exchange rate of the yuan, also known as the renminbi, would be kept basically stable this year, while Beijing […]

LikeLike

One may wonder how successful Norway really is. The prices of housing in Norway have grown to a level where it is impossible to buy a home without establishing a dept that is impossible to get rid of in a lifetime. Generally the price of food and fuel is also the highest in the world. Norwegians look like they have a high living standard, but in the recent years this has been maintained for most citizens by accumulating a steadily higher dept. The result is that the Norwegian population has the highest dept burden in the world. Right now, and probably in many years to come the oil prices has got below the cost of the Norwegian oil production, which means that Norway will lack funding for the daily costs of public and private sector. Norway is probably heading towards a chronic crisis, given the economical facts.

LikeLike

Thanks for those comments. Of course, in a very rich country one would expect things to be expensive (the US has always been a bit of an outlier) as – eg – rents and wages will be high. It will be interesting to watch how Norway copes with a period of persistently weak oil prices, but of course there is a huge buffer in the Provident Fund – and a very long way to drift down before Norway was recording GDP per capita anywhere near as low as NZ’s.

LikeLike