[Here is the link to the coverage of my paper on governance in the Sunday Star Times]

This post had its origins in an earlier OIA stoush – not mine, but that of one of the Green Party’s parliamentary staff.

For at least 15 years, I’ve thought that the way the Reserve Bank was governed should be changed and that we should move away from the situation (unusual internationally and anywhere else in the New Zealand public sector) where a single unelected official makes all the policy decisions (in the Reserve Bank case, on monetary policy and financial regulatory matters). Other countries don’t do it that way. New Zealand doesn’t do it in any other field of policy.

In late 2011, I was filling in time in the office between Christmas and New Year. Alan Bollard’s second term was coming to an end, and while he hadn’t confirmed he was going it was widely (and correctly) expected. I’d been saying to people for some time that a change of Governor was the best time to try to trigger discussion on the issue. So I decided to write a brief internal discussion note making, in writing, the case I’d been making in conversation for years. I didn’t propose a detailed alternative model, and simply urged that change be considered, and that the Bank think about getting in front of the issue. I wrote the note, and sent it round to only perhaps 10-12 of the Governor’s senior advisers on monetary policy. I went on holiday, and when I got back word came down that the Governor was not all happy that the discussion note had been written.

Some months later, I took the opportunity to revise the note, and to take on board some useful comments I had received. By this time, it was confirmed that Alan Bollard was going, but no decision had quite yet been announced as to who would be the new Governor. Since no one could then think the paper was in any way a criticism of any individual, I sent it around a wider group of the Bank’s policy and analytical staff. When Graeme Wheeler joined the Bank I sent him a copy, and had an appreciative response.

At some stage in 2013, the Green Party became aware that the paper existed (because the Bank had released another paper under the OIA, and my note was included in the list of references). Their staffer asked for the paper, and was turned down. He pursued the matter to the Ombudsman, who accepted the Governor’s argument that if this paper were released he would not be able to allow free and frank debate among staff. I didn’t have a strong view on whether it should be released – internal debate is important, and my note had been intended only as a contribution to that. But it wasn’t a very recent paper, hadn’t even been written when the current Governor was in office, was not on a topic that was under active review, and the Governor’s argumentation was perhaps a little chilling.

Anyway, had the 2012 paper been released a couple of years ago, I probably wouldn’t have done anything more on the issue. But I had continued to think about the issues, and particularly to think about them in the context of the much wider ranges of responsibilities and powers the Bank now exercises. The result is this paper.

time for Parliament to reform the governance of the Reserve Bank online version

My preamble is partly to make clear that this is an issue that I have been thinking about for a very long time. As people occasionally remind me, some of my comments on this blog could be seen as (but are not) motivated by grudges against current Bank management. As Don Brash will confirm, I was running (less-developed forms of) the argument fifteen years ago. The best Governor in the world simply should not have the extent of power any Reserve Bank Governor now has.

As important are two things:

- The Reserve Bank does not write its legislation, Parliament does. The Bank, and its Governor, operate within laws that Parliament has passed. The responsibility for legislation in this area rests with the Minister of Finance and Parliament.

- To his credit, Graeme Wheeler seems to have recognised some of the weaknesses of the current system. I suspect he and I would not agree on the solution (I don’t think staff should make the sorts of decisions the Reserve Bank is responsible for), but what matters at this stage is to get a good discussion and debate going, and to have a careful examination of the pros and cons of various possible models.

As it happens, I’m not sure if anyone is now particularly wedded to the current model. The Treasury favoured a review in 2012, and they reported that many or most of the market economists then favoured change. The Governor appears to recognise the risks and deficiencies of the single decision-maker model, and several political parties have also at times talked of proposing change.

This isn’t an issue that should divide people on any sort of ideological lines. I’ve taken as given the current powers and objectives of the Bank. Perhaps some of them should be looked at again, but this paper is just an attempt to prompt some discussion about how best to organise and govern a powerful New Zealand public agency, carrying out the wide range of functions that Parliament has assigned to it.

As ever, I’d welcome thoughtful comments and alternative perspectives.

The first page of the paper, an introduction and summary, is here:

Introduction and summary

When Parliament passed the new Reserve Bank of New Zealand Act in December 1989 a key, and innovative, feature of the Act was that the powers of the Reserve Bank were to be exercised by the Governor, and the Governor alone. The legislation provided substantial operating autonomy to the Reserve Bank, and the establishment of a single decision-maker was seen as a way of providing effective accountability. If things went wrong, the Governor would have been responsible for any decisions, and the Governor could be dismissed, for cause, by the Minister of Finance.

But the model is out of step and out of date. It is out of step with international practice in respect of monetary policy and of financial system supervisory and regulatory policy. As importantly, it is out of step with approaches to governance used in the New Zealand public sector more generally.

The Reserve Bank governance model was developed, in part, to parallel reforms to core government departments that were going on at much the same time. Those reforms themselves have since been considerably modified. But even if that were not so, the conception of the Reserve Bank that the 1989 legislation reflected has not been borne out by reality.

The 1989 governance model might have been thought appropriate (if still unusual) for a very simple and uncontroversial most-monetary-policy agency. Today’s Reserve Bank is a complex, multi-functional, organisation, exercising much more policy discretion in a range of areas, that are all characterised by considerable risk and uncertainty, than was envisaged in the 1980s. Vesting all that power in a single unelected person is too risky, and is inappropriate. It is not the way we do things in New Zealand.

In this note I will take as given both the range of functions the Reserve Bank has, and the allocation of powers between the Minister of Finance and the Bank. Aspects of both issues should probably be revisited, but here I focus simply on the weaknesses in the governance model given the responsibilities that Parliament has assigned to the Reserve Bank.

The rest of this note outlines the key aspects of Reserve Bank governance and explains the background to the governance choices made in the 1989 Act. It then focuses on how different things are today and why, even if it was a suitable model in 1989, it no longer is today. I outline some alternative options and conclude by outlining my own preferred option. Key aspects of any reforms should be (a) a move away from having policy decisions made by a single unelected official, and (b) the establishment of collective decision-making bodies which clearly distinguish among the main functions the Reserve Bank undertakes.

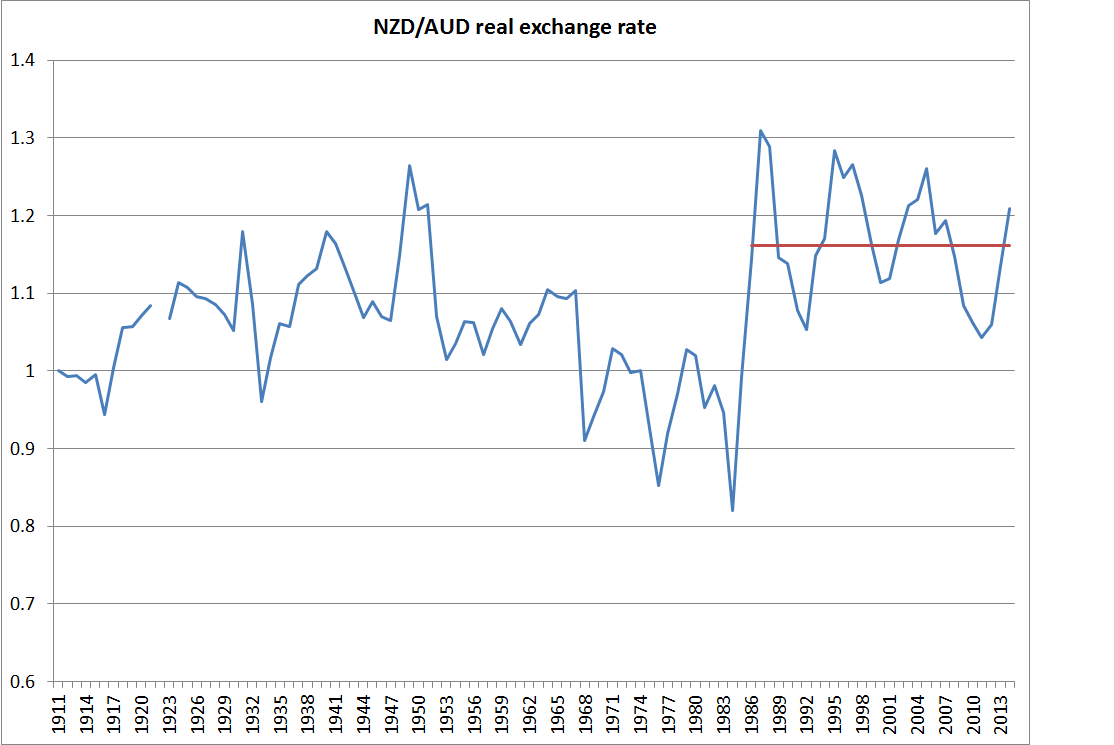

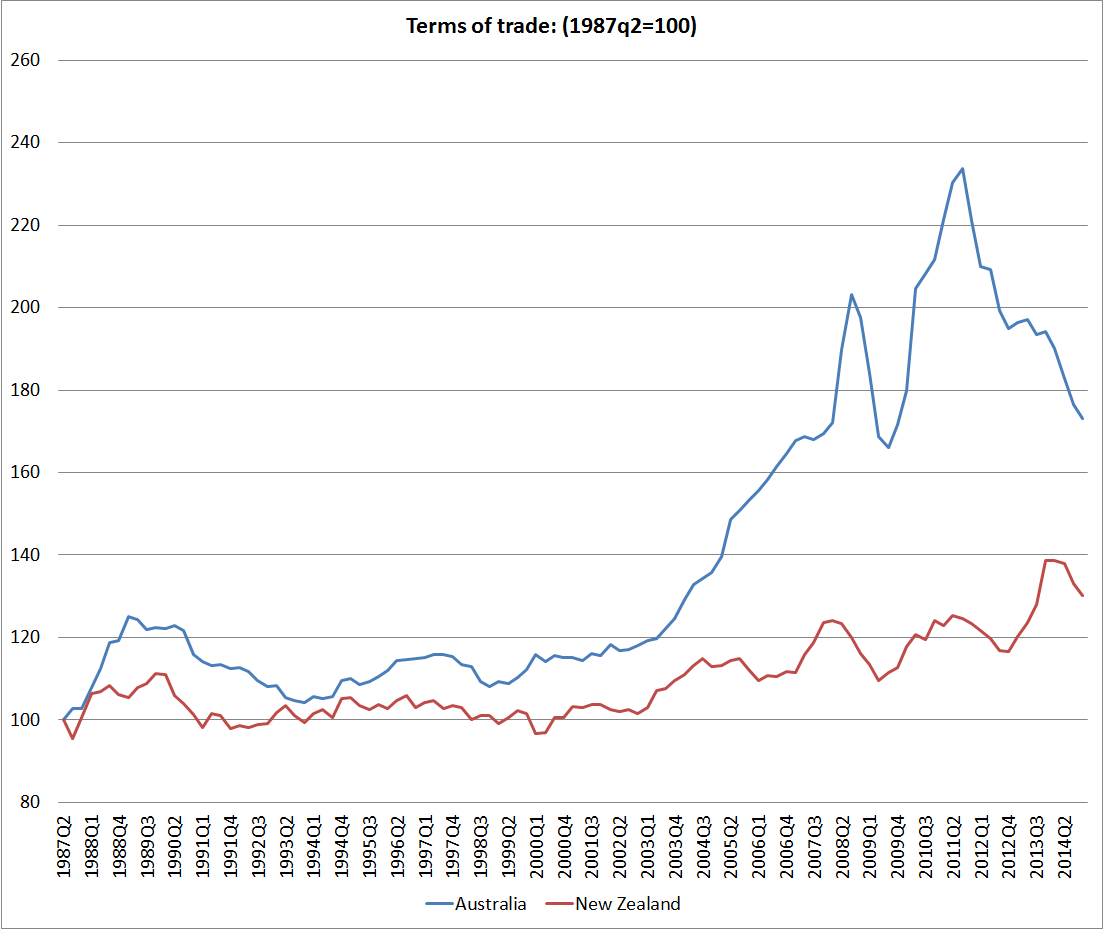

I think the second sentence is a little unfair, although it does depend what people mean by “overvalued”. Most prominently, Graeme Wheeler routinely highlights that the exchange rate appears out of line with long-term fundamentals.

On the question the commenter poses, I do have view and the answer is “typically not”. At present, I think the Reserve Bank has the OCR set too high, and will need to lower it. At the margin, the overly tight monetary policy in recent years has left the exchange rate a little higher than otherwise.

The other instrument the Reserve Bank has at its disposal is foreign exchange intervention. I have come and gone over the years on whether the Bank should be able to do such intervention, but no one believes it can make any material or sustained difference to the sorts of real exchange rate misalignment I was talking about in the earlier post.

Central banks can do things that make a difference to the real exchange rate for short periods of time. Monetary policy makes more difference than intervention. But sustained misalignments, over decades, are real phenomena, not monetary ones. To understand those sorts of sustained pressures, one needs to look to what drives differences in real interest rates over long periods. And, again, the answer isn’t monetary policy (as the Bank explained here). Regulatory policy doesn’t make much sustained difference either, although there are some intriguing suggestions to the contrary here.