I wrote the other day about the way that New Zealand’s real exchange rate had become (not just recently, but in the last 20-30 years) out of line with changes in our terms of trade and in our relative productivity performance. In that post I suggested that the large gap between New Zealand’s real interest rates and those in other advanced countries was a big part of the explanation. Not, of course, that interest rates are an independent factor just imposed on us, but that if we could understand what had driven such a wedge between our interest rates and those of the rest of the advanced world, we would be on the way to understanding what was resulting in such a persistent (albeit rational) misalignment of the real exchange rate. In that post, I simply noted the current very large gap between the real yields on inflation-indexed bonds issued by the New Zealand and US governments respectively. That gap is around 1.5 percentage points. Over 20 years, that looks like a huge difference in expected returns.

Interest rate differentials can move around quite a lot. Even for long-term bonds, cyclical differences in the health of the respective economies can make quite a difference[1]. Risk factors can matter too – at times of heightened global risk, for example, US Treasury bonds still tend to be an asset of choice. My focus is not really on short-term movements in those differentials, but on what has happened on average over time, and that is the focus of this post.

The OECD publishes data on long-term bond yields for each of its member countries. “Long-term” here generally means something close to 10 years, the usual benchmark for such comparisons. The data are nominal, and of course over time differences in inflation rates should explain quite a lot about differences in nominal interest rates across countries. So I restricted myself to the period from the end of 1991. For New Zealand, that was the first quarter in which inflation had fallen inside the new inflation target range, and most other of the older advanced countries had also broken the back of the high inflation of the 1970s and 1980s by then. But I’ll come back and look at trends in inflation a bit later.

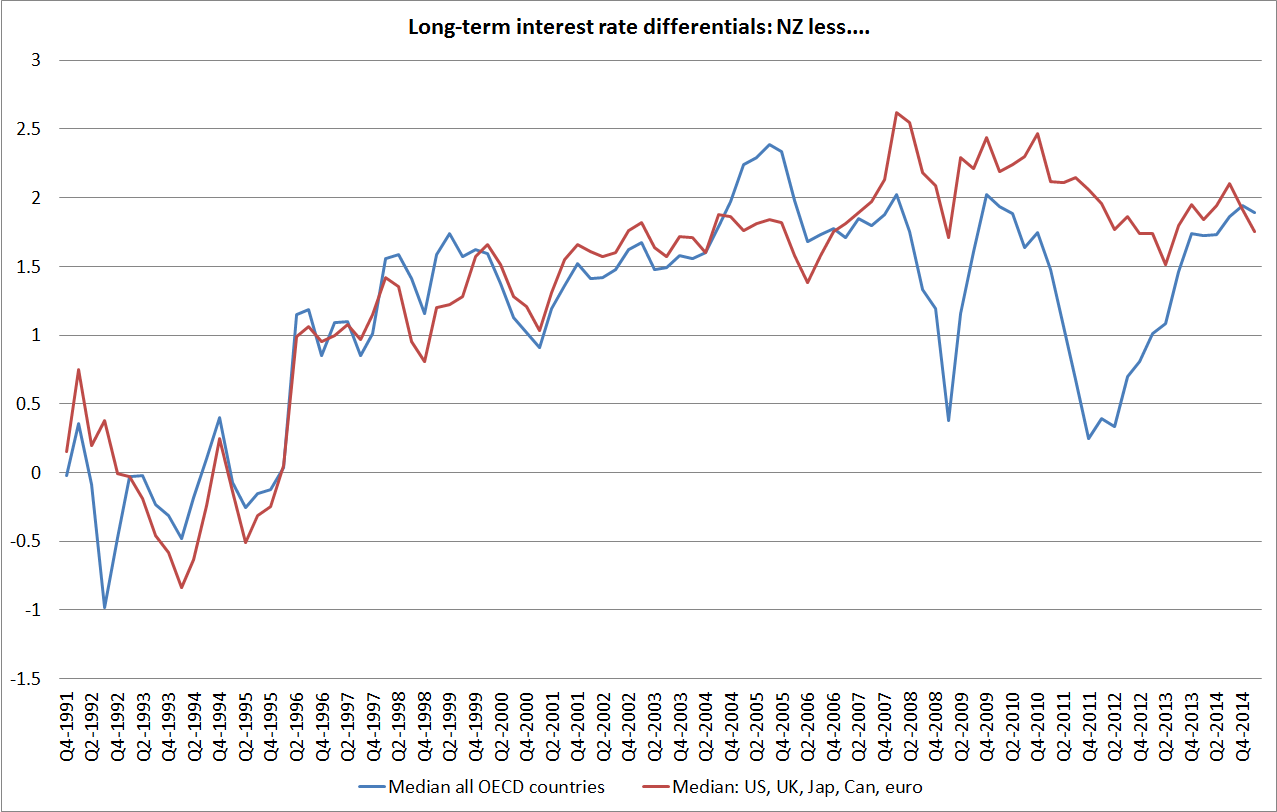

In this first chart, I’ve shown long-term bond yields for New Zealand, for the US and for the medians of several groups of countries. I’ve looked at the median of all OECD countries (but at the start of the period there is no data for many of the former communist countries, and by the end of the period, half of all the countries were in the euro), of the G7 countries individually, and of a grouping of G7 currency areas (Canada, the US, the UK, Japan, and the euro-area). Most of the time it does not much make difference which measure one looks at. I’ve included them all so that you can see that I haven’t been cherry-picking. My preferred series to compare New Zealand against is probably the G7 currency areas one.

Of course, the dominant story of the last 25 years is the dramatic fall in the level of interest rates everywhere. Part of that is the fall in actual and expected inflation – even in the G7 countries, inflation still averaged 4 per cent at the end of 1991 – but real interest rates have also fallen markedly.

But my main interest is in the differentials: how have New Zealand bond yields behaved relative to those of these other advanced countries. It was notable in the first chart how the gap between New Zealand and other countries emerged over time.

Well, here is the chart of the differentials. This time, to make the chart easier to read, I’ve shown only two series: New Zealand less the median of all OECD countries, and NZ less the median of the G7 currency areas. It is easy to forget how low New Zealand interest rates were at the start of the period, relative to those abroad (I was running teams at the Reserve Bank advising on monetary policy and doing the Bank’s macro forecasts, and I had forgotten). At the start of the period, we were just emerging from two decades of very high inflation, and were only a few months on from the much-publicised threat by rating agencies of a double-downgrade to New Zealand’s sovereign credit rating. We did, however, at the time have a very low inflation target – even if political support for that target was fragile at best.

But I’m really interested in more recent periods. Again, I partly started back in 1991 just to provide context.

Throughout the 1990s, there was a very strong expectation that New Zealand short-term and long-term interest rates would converge to those of the rest of the world[2] Once we had low and stable inflation, much stronger fiscal accounts, and people were confident those things would last, then having become integrated with global capital markets, it seemed a reasonable story. Sure, there might be small differences – small New Zealand markets might always be less liquid – but the differences weren’t thought likely to amount to much, especially when comparing us against other small advanced economies.

But that convergence has just never happened, and the fact that it has not happened – that the interest gaps have been so large, through booms and busts – is one of the most striking features of what has happened in New Zealand in the last 20-25 years. Day-to-day what happens internationally is a key influence on changes in New Zealand bond yields, and there is clearly a common factor at work in the long-term decline in real yields, but the levels remain completely different.

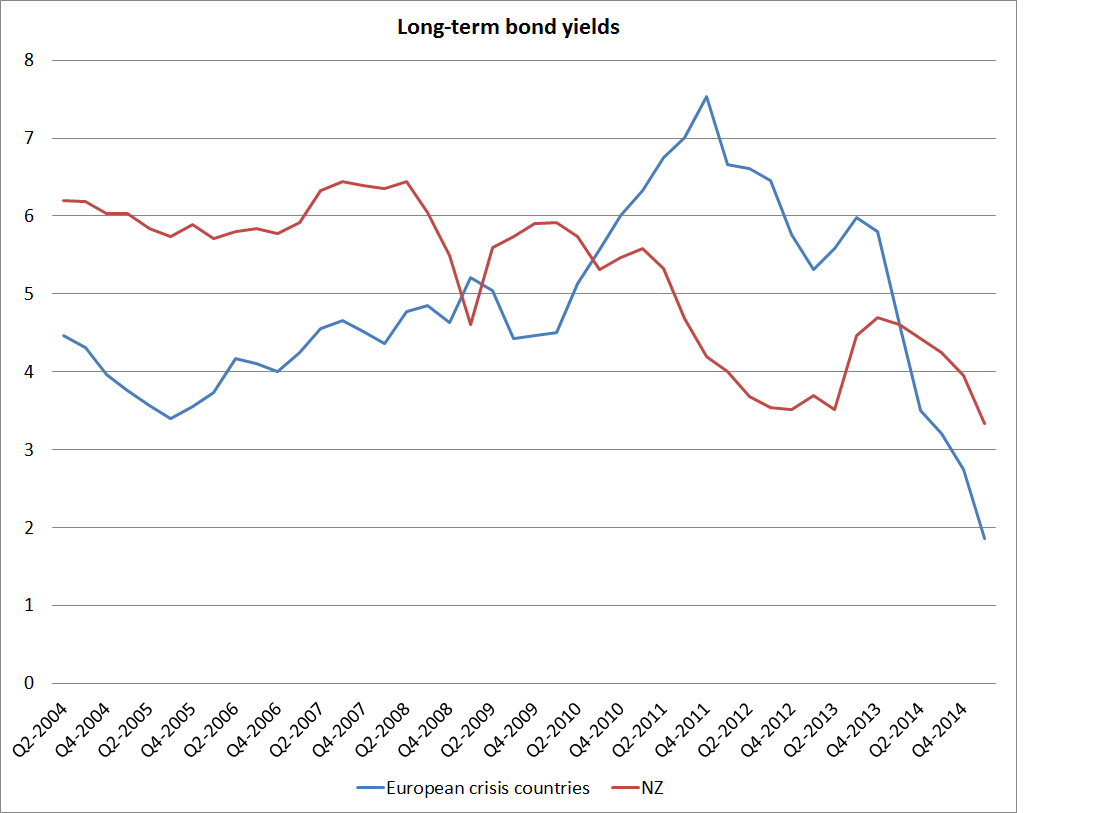

It is interesting to note where the two lines diverge materially, both in the period since 2007. Nothing very interesting happens in the differential between New Zealand and G7 bond yields since 2007, but both during the 2008/09 recession, and again – more starkly – at the height of the 2011/12 euro-crisis, New Zealand bond yield differentials fall sharply relative to the median OECD country. It is easy to see that effect in this chart, simply comparing New Zealand against a group of eight crisis countries (Iceland, Ireland, Greece, Spain, Portugal, Italy, Slovenia and Hungary).

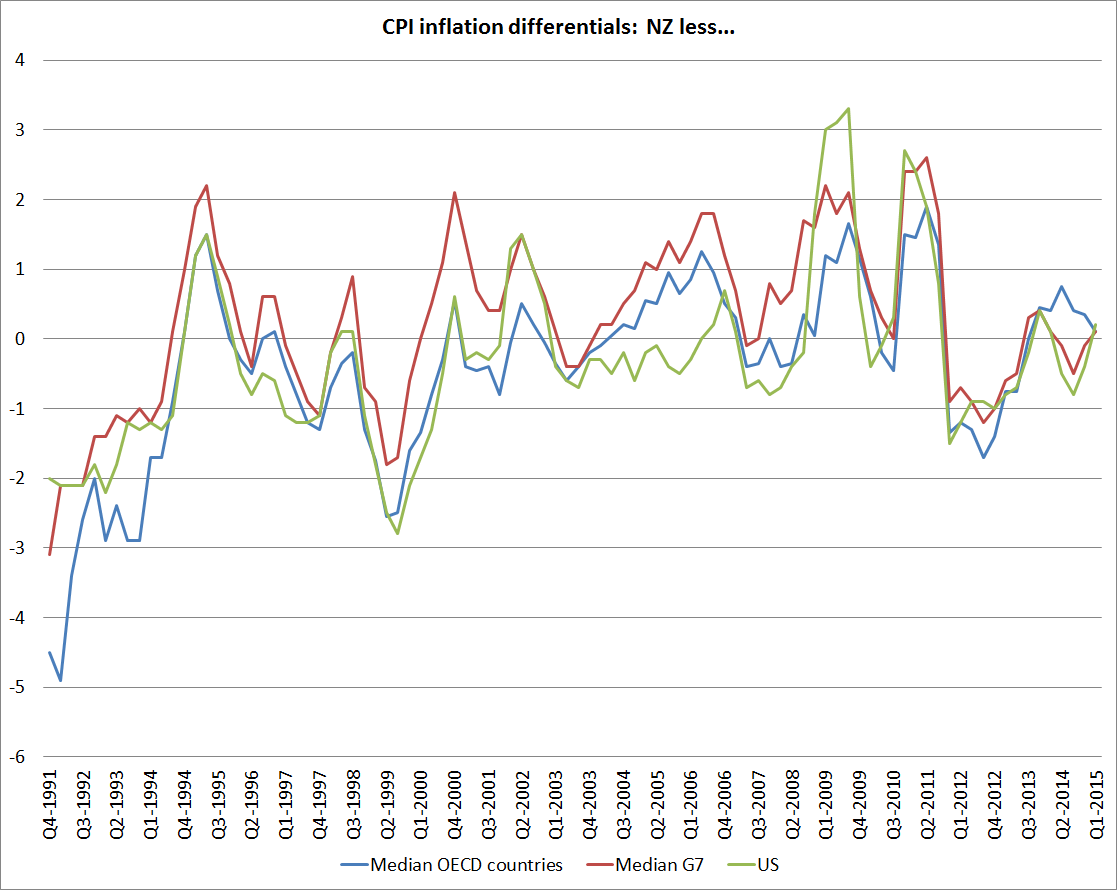

As I noted earlier, differences in actual and expected inflation can affect the interpretation of nominal bond yield differentials. We don’t have consistently-compiled cross-country measures of inflation expectations (and in most countries, indexed bonds are too recent or too patchy – the NZ story – to provide much of a time series). And so people tend to fall back on comparing actual inflation rates over time. It has to do, since it is all we have, but it is worth remembering that even CPIs are compiled differently across countries, and across time even within individual countries. In New Zealand, for example, until 1999 CPI inflation rates included the direct effects of interest rates, and section prices.

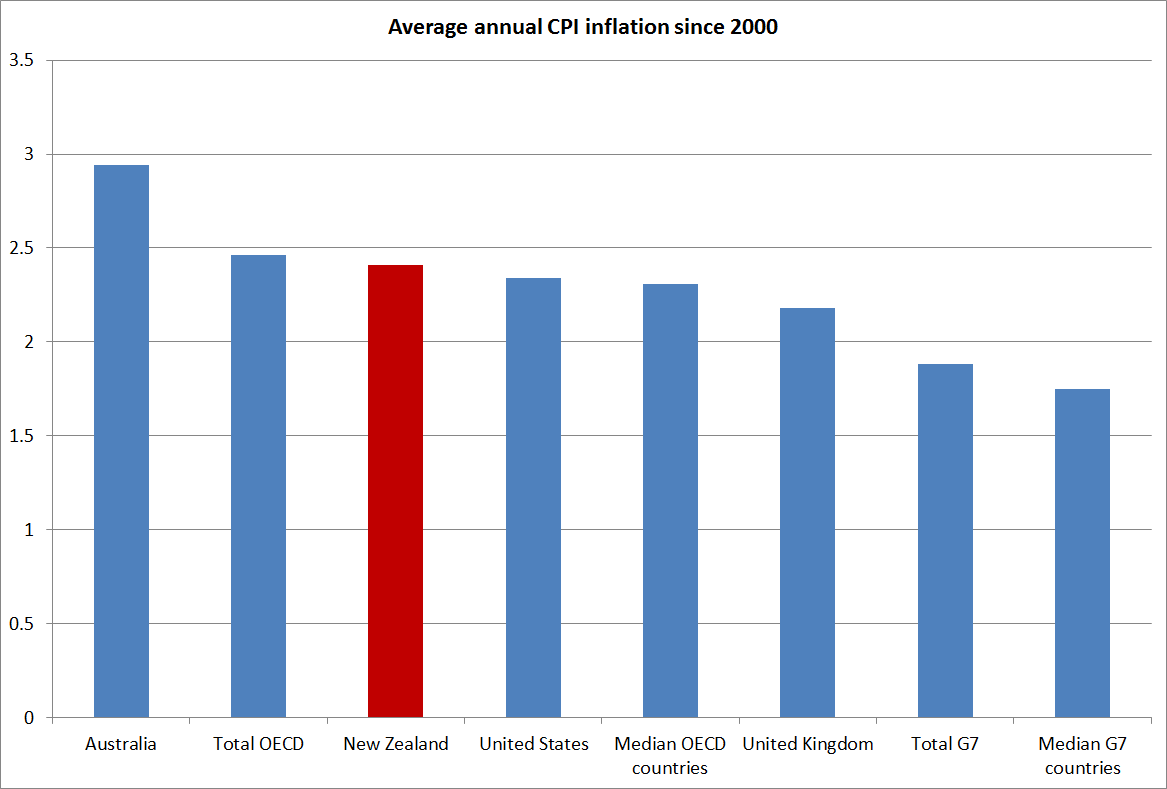

This chart just shows the average inflation rates for New Zealand, for a couple of individual countries, and for various country groupings since 2000. New Zealand’s inflation rate has averaged a bit higher than inflation in the G7 countries, by around 0.6 percentage points, but has been very similar to that among OECD countries as a whole, and that in the United States. At least since the mid 1990s, it doesn’t look as if there has been any particular change in the relativities, and at present New Zealand’s inflation rate is almost identical to that in the rest of the advanced world.

Historical differences in inflation outcomes might be thought to have warranted nominal bond yields in New Zealand perhaps 0.5 percentage points higher than those in the rest of the advanced world. Looking ahead, however, New Zealand’s inflation target is very similar to those in the rest of the advanced world: our target is centred on 2 per cent, and while Australia’s in a touch higher, and the euro-area’s is a touch lower, taken as a group there isn’t much difference. And yet our nominal bond yields have still been averaging 2 percentage points higher than those abroad.

What does explain it? A common story is risk around the high level of net international indebtedness of New Zealand entities. I don’t find that story persuasive at all, and will explain why in my next post.

[1] Using implied forward rates (the yield implicit in the second five years of a ten year bond) is a good way around this, but such data are less readily accessible).

[2] I documented this in a paper I wrote a few years ago for a Reserve Bank and Treasury workshop. I would quite like to post it, but it would no doubt take at least 20 working days to extract it from the Bank.

[…] week I illustrated how much higher our long-term interest rates have been (and are) than those in other advanced […]

LikeLike