Reading the Herald over lunch I found Audrey Young’s interview with Labour’s finance spokesperson Grant Robertson.

I was interested in his praise of the former Minister of Finance, Michael Cullen. No doubt he has to say some positive things about his predecessor, but his comments seem quite genuine – Cullen is his “finance hero”. It isn’t an overly partisan interview – he describes both Michael Cullen and Bill English as people “who are seen to be good Finance Ministers”.

There is no single way to evaluate the success of a Minister of Finance; it is such a multi-faceted job. Labour ran large surpluses for much of its term, but then left a Budget – with Treasury’s explicit imprimatur – that meant large deficits when the unexpectedly severe recession hit. The current government has run deficits, despite record terms of trade, but then they had a tough starting point. The economy was buoyant in the years up to 2008, and has shown little (per capita) growth since then, but neither Minister of Finance had much hand in those outcomes.

One the most disappointing aspects of my adult life has been the failure of any government (two Labour-led, two National-led) to make any real progress in turning round the gaps in living standards between New Zealand and other advanced economies.

People can debate how to measure living standards , but perhaps the best test is what choice New Zealanders are making. Are they coming, going, or staying?

A successful economy isn’t one in which no New Zealander ever leaves. Individuals will come and go at different stages of their lives, for professional opportunities, for adventure, or just to see the world. And a few will always go permanently – whether it is marriage to someone overseas, or a particular professional niche. I’ve been in and out three times in thirty years, and we actually produced a PLT inflow by having two kids abroad. But a reasonable benchmark for the success of a country is likely to be whether, on average over time, the net outflows of its own citizens roughly match the net inflows of people returning. If so, it suggests that people, on average, reckon they can have just as good a life here – near home and family, in the culture they know – as in other advanced economies.

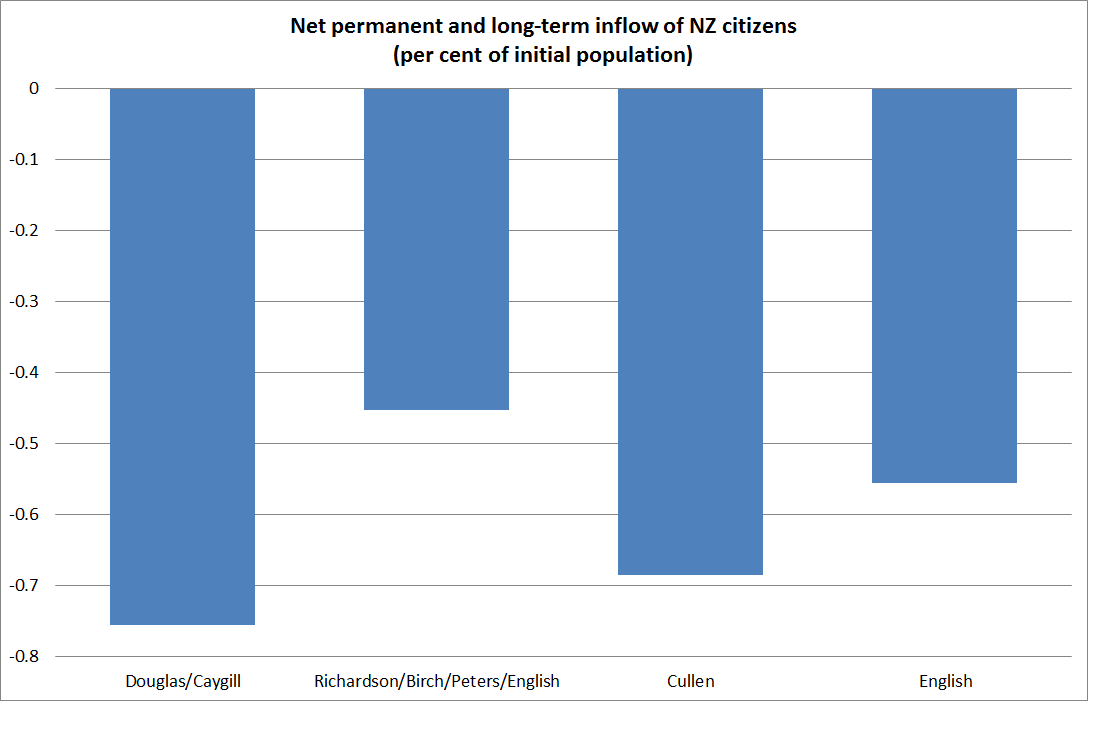

How have the different governments, and Ministers of Finance, done since 1984?

These data are based on what people say on their arrival/departure cards. They aren’t perfect: some people say they are going short-term and end up staying away for good. Others go planning never to return and are back a few months later. But the general picture in the multi-year averages isn’t likely to be that far off.

There just isn’t much sign of the net outflow slowing down much. It ebbs and flows with the differences between the cyclical health of Australia’s economy and ours. And when the world is in a particularly bad way people tend to stay close to home too. Perhaps the 1990s period stands out as better than most, but I wouldn’t make very much of that. Right now the net outflow is quite small, but the series is very volatile, and this trough is no shallower than others we’ve seen over the years. It is unlikely to last, let alone turn into a net inflow.

I’ve shown the average annual net outflow as a percentage of the population. Those can look small – year by year they don’t make much difference. But over the 31 years, a net 676000 people have left New Zealand, from a country that had only 3.3m people in 1984. And many of them will have had children and grandchildren who are also now not growing up as New Zealanders.

Does it matter? Perhaps not to some – each individual is making his or her own best choices – but it has changed New Zealand, and if nations mean anything then it matters. To me, it marks the failure of our governments.

John Key certainly thought so[1]. This extract was from a speech he delivered just before the 2008 election. I had a copy pinned above my desk for several years; first in (perhaps rather naïve) hope, and then, if not in despair, at least in resignation. What changes?

I came into politics because I believed New Zealand was underperforming economically as a country. I don’t think it’s good enough that so many New Zealanders feel forced to leave our country each year to seek higher wages in Australia. I don’t think it’s good enough that our average incomes lag so far behind the rest of the world. And I think it’s unforgivable that the Labour Party has done so little to address these fundamental challenges. I believe that a very big step change is needed in our economic performance to ensure New Zealand can make the most of its considerable potential.

[1] And I’m sure his predecessors of both parties did too. This isn’t intended as a particularly partisan comment.