Some further, slightly scattered, thoughts prompted by the Budget.

I can’t get excited about the question of which year a surplus is finally recorded. Apart from anything else, the government’s interest costs include an inflation-adjustment component (medium-term inflation expectations are still around 1.85 per cent per annum). That is effectively a repayment of principal, not an operating cost. A modest deficit is consistent with inflation-adjusted balance or surplus. And if one is content to have a positive target level of debt – as those on both sides of politics seem to be – then a small deficit each year is still consistent with a stable or falling ratio of debt to GDP. We probably should be a little more worried about the continuing structural deficits, especially once an adjustment is made for the above-average terms of trade New Zealand has been experiencing. High terms of trade should have made it easier than otherwise to get back to balance. Then again, the Treasury appears to be quite optimistic about the future path of the terms of trade – let’s hope they are right.

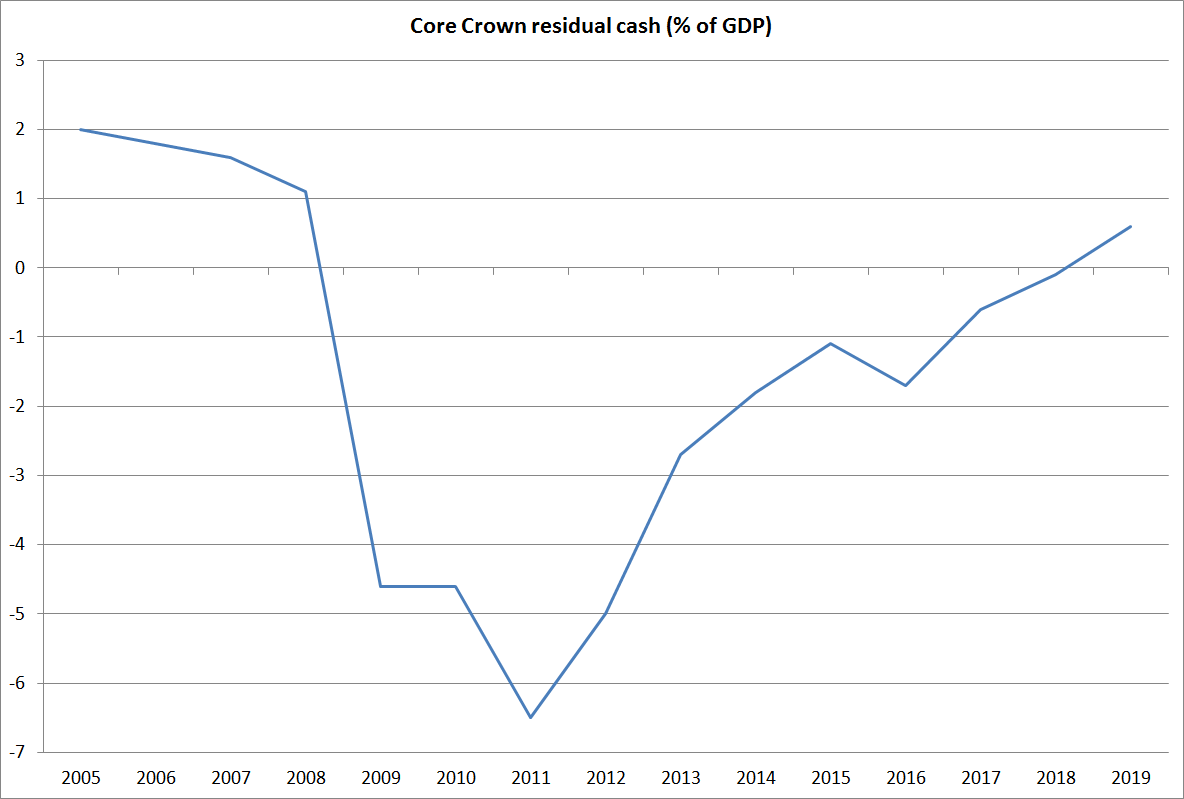

When I went to Treasury for a couple of years, one of their more sage observers counselled me to focus on the core Crown residual cash balance (just like analysing a set of corporate accounts – look for the cash). That measure includes all the gains from the buoyant terms of trade, and the cycle peaks, and still doesn’t get to balance for another three years.

Perhaps the more important question is how much debt should governments aim to have. We like to think of New Zealand government debt as quite low. Debt is often quoted as a ratio to GDP, but if we take government gross debt as a percentage of government revenue, that ratio is now around 130 per cent – not so different from the ratio of household debt to disposable incomes that often seems to trouble observers. Net debt is certainly lower, but a considerable chunk of the financial assets are in the highly volatile New Zealand Superannuation Fund (which I have been meaning to write about).

Looking at the tables in the last OECD Economic Outlook, six OECD countries currently have positive net government financial liabilities (Estonia, Finland, Korea, Luxembourg, Norway and Sweden). Some argue for the government to run net assets, to counter the effects of the welfare system in deterring private savings. Others could construct a case for a positive net debt, because of the significant real assets governments own (some of which are, arguably, productive). Those effects go in opposite directions. Personally, I’m not convinced there is a case for governments holding large net assets, but perhaps we should be looking at reframing the local debate, and aiming to see net government debt at least fluctuate around zero. Shakespeare’s “neither a borrower nor a lender be” has some appeal as a medium fiscal strategy. It won’t be a textbook public finance strategy, but those particular textbooks don’t give much weight to the failures, and weaknesses, of governments. Aiming for something around zero would also mean citizens just didn’t have to worry about government debt, one way or the other.

As a strategy for normal times, I also quite like the longstanding Swedish fiscal rule, of aiming for a 1 per cent of GDP structural surplus (although I see that the current Swedish government is looking at scrapping it). No one can do structural adjustments particularly accurately in real time, but a 1 per cent structural surplus target is a cautious pragmatic second best approach. If you get it right, debt will be low when crises hit – and they eventually will. But often enough you will misjudge your how structural your surplus is. But if you think you are running a 1 per cent surplus, and it later turns out that it was in fact a structural deficit (if, say, potential GDP turns out to have been lower than was thought) you are most unlikely to be in major fiscal problems. Getting back to balance from a 2 per cent structural deficit isn’t likely to be that hard, or that urgent.

And, on the other hand, aiming for no more than a 1 per cent structural surplus deliberately foreswears the over-optimism of those who believe that very large swings in structural fiscal balances can act as effective macro-stabilisers in boom times (ZLB periods might be different). In fact, running up large surpluses in boom times – when no one knows how long booms will last – just tends to set up an electoral auction.

The previous government in many ways deserves a lot of credit for keeping spending in check for their first six years, but the structural surplus in 2006 peaked at 4.7 per cent of GDP (OECD estimate). Those huge surpluses just set up an electoral auction in the 2005 election campaign. No political party will ever want to be in the position of allowing their opposition to spend the surplus their way – those choices, about priorities, are a large part of what politics is about. And the large surpluses built up in the early 2000s didn’t even do much to ease pressure on monetary policy, because they were run up well before the peak pressures on resources (2005 to 2008). Quite possibly, overall macroeconomic management in New Zealand over the last 15 years would have been a little better if piecemeal adjustments had been made throughout. We’d never have got into a position where we had highly stimulatory discretionary fiscal policy in the period (2005-2007) of greatest pressure on resources (and on the exchange rate). And it would also have avoided a situation where Treasury, applying its best professional judgement, finally determined only just before the great recession of 2008/09 that the revenue increases looked permanent. A high stakes judgement that turned out to be quite wrong. Fiscal institutions, and ambitions, need to take more serious account of the severe limits of anyone’s knowledge. A Fiscal Council, as the New Zealand Initiative and the former director of the IMF’s Fiscal Affairs Department have recently called for, might explore some of these issues. Or a Macroeconomic Council might? Then again, our academics and think tanks might lead such debates,

In passing, it is worth noting that the Reserve Bank is always curiously reluctant to analyse sovereign debt risk in their FSRs, even though the New Zealand government would be by far the largest single-name credit exposure of any of the banks. And the New Zealand government last defaulted on its debts some decades more recently than the last time a New Zealand bank defaulted on any of its debts. In a through the cycle sense, how robust are the risk weights on domestic sovereign debt exposures? I’m not suggesting that the New Zealand government is in any near-term danger of defaulting, but then neither are the banks – apart from anything else, the Bank’s stress tests told us so. The Reserve Bank tends to assume that governments can always just increase taxes to pay their debts, or inflate it away, but the historical track record is that they don’t always do so. Sovereign debt defaults are simply not that uncommon. We’ve done it. The US and UK have, and Reinhart and Rogoff reminded us of the rather long list of others.

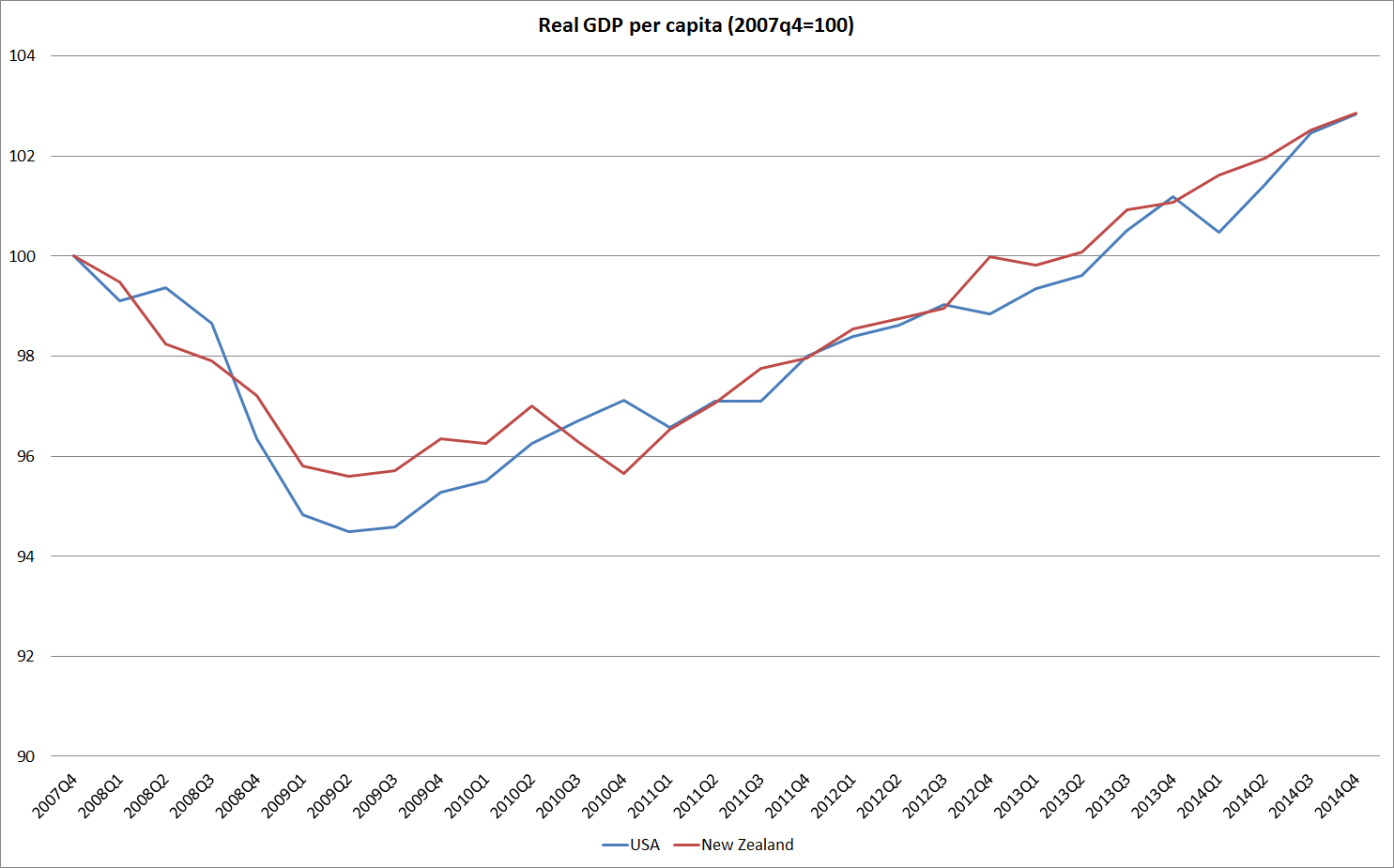

But to return to the Budget, perhaps the saddest aspect is that there is no sign of any serious effort to turn around New Zealand’s decades of relative economic decline, or indeed to materially alter the state of affairs that sees 10 per cent of the working age population on welfare benefits. Another year, another wasted opportunity. There is a line in the Bible, “to whom much is given, from much shall be required”. I doubt history will look that kindly on Key, Joyce and English, or Clark, Anderton, and Cullen – stewards of our country’s affairs for the last 16 years between them. . It is not that the macroeconomic stewardship has been that bad, under either government, but both seem to have been content to preside over whatever direction the ship is taking, rather than exercising effective and persuasive leadership to make of this country what it once was, and again could be. The common line is ‘ah, but at least we avoided a financial crisis”, but to what advantage when our overall economic performance in recent years has been as bad as that of the United States, the country at the heart of the crisis, despite having had the best terms of trade in decades.