Gideon Rachman’s column in today’s FT suggests (if he doesn’t quite directly say) that for Greece to leave the euro would now be the best way forward for everyone. He uses the analogy of a struggling marriage in which both parties might be happiest apart, however traumatic the breaking up might be. Where I come from marriage is “until death alone parts us” and my reading of the literature suggests that many unhappy couples who chose to stay together end up happier than those who separate. But the euro isn’t a lifelong covenant. It is an act of foreign economic policy among a group of sovereign states. While it serves the interests of their respective peoples it should last, and when it doesn’t it should be dissolved or slimmed down.

Rachman’s line is similar to ones I’ve run in a couple of recent posts (here and here), although my focus has been more on the idea that there is no politically saleable path (saleable in Greece, and in the other eurogroup countries) that offers both a robust Greek recovery and the whole euro group of countries remaining together. There is no guarantee that exit would be in the long-term best interests of Greece, but the status quo looks pretty awful.

Everyone knows how large the fall in real GDP has been, and how high the unemployment rate now is, years on from the start of this crisis. With no scope for discretionary monetary policy, and limited fiscal room even if the sovereign debt is mostly defaulted on (since the near-term appetite of new lenders is surely going to be limited), the source of any sustained boost to demand must either domestic innovation and productivity, or external demand.

Those wanting to put an optimistic gloss on the data can certainly produce real exchange rate measures that seem to show some gains in competitiveness. Perhaps, but it is difficult to adjust for compositional effects (the least productive people will have lost their jobs, but presumably want to be employed again one day).

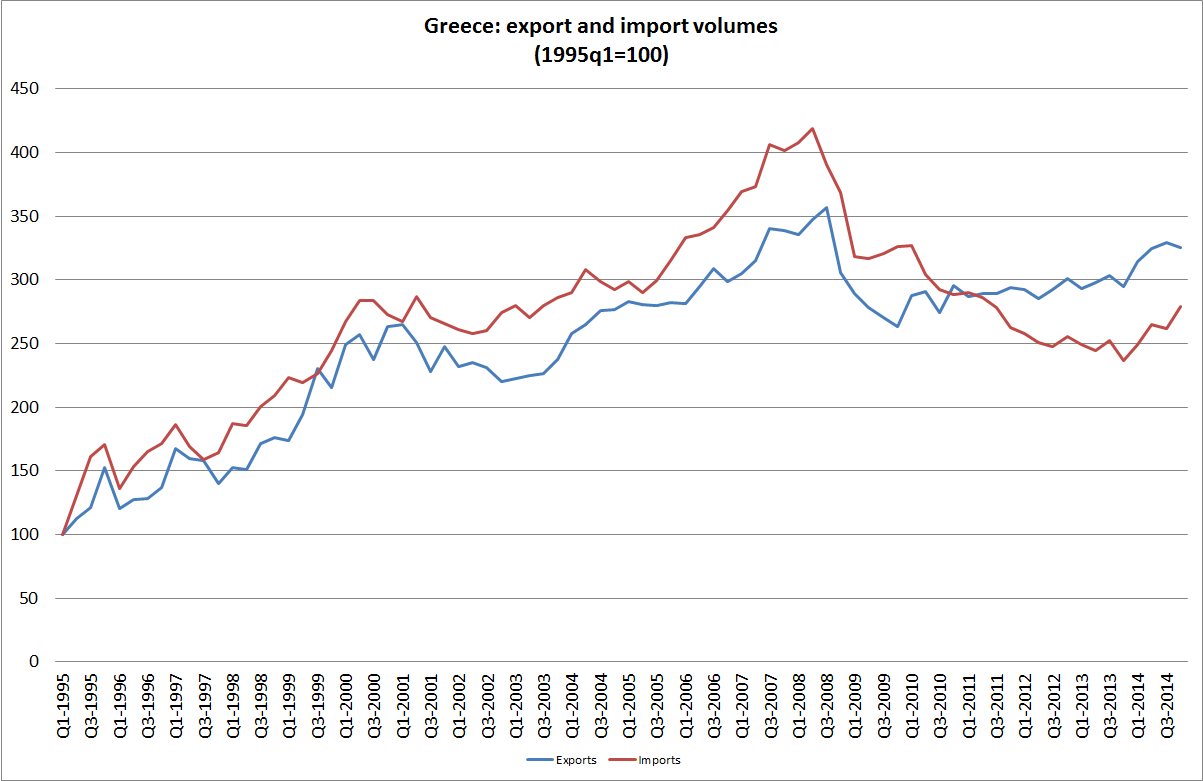

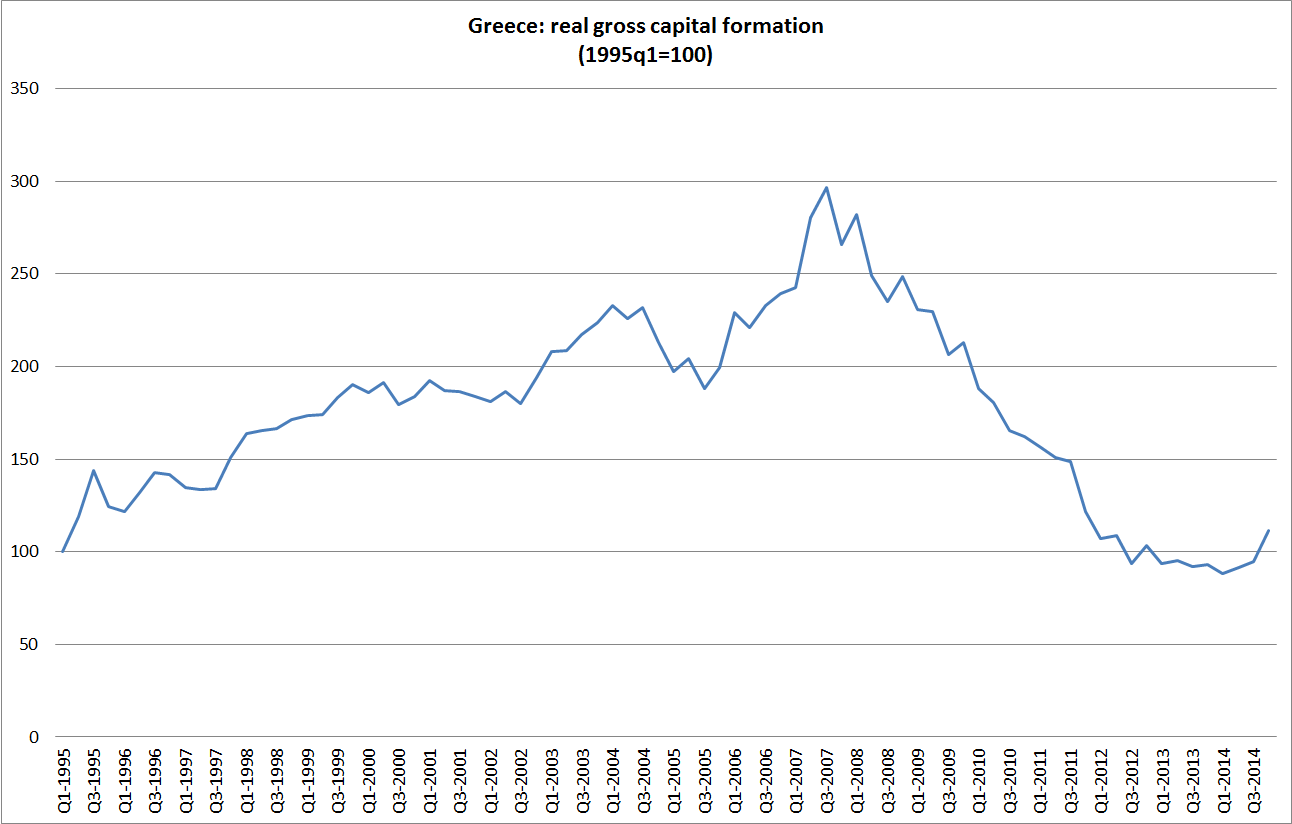

These two charts just look at some of the key aggregates, drawing from the OECD’s quarterly national accounts database.

Exports have been recovering somewhat since the trough after the global recession of 2008/09, but the volume of exports is only now back to 2007 levels. In an economy with unemployment in excess of 25 per cent, there is no crowding out of the export sector.

Import volumes have certainly fallen, very substantially. That might reflect competitiveness gains, and greater opportunities for domestic import-competing tradables producers. But it looks a lot more likely to mostly reflect a severe compression in demand. The collapse in real investment is particularly telling.

It is not quite all bad news. Greece has experienced an improved terms of trade over the last few years. But there is no sign of it translating into the sort of robust export growth, or business sector investment, that might enable the external sector to begin to pick up the huge slack in Greece’s economy. Whether that is because firms just aren’t competitive or because of rising uncertainty (or some combination of the two, as seems more likely) isn’t immediately clear. But note that these data go up only to 2014q4 – this was what things were looking like under the previous government and the old programme (for all its limitations). Any uncertainty has only become greater since then.

WIth almost nothing going well in Greek economy, and limited tolerance in the rest of Europe, the status quo surely can’t go on much longer. One piece of good news today is reports that the IMF is no longer willing to extend and pretend, in this case at least.