Wolfgang Munchau writes a very stimulating weekly column for the Financial Times, on aspects of the euro crisis. Yesterday’s column was no exception. It is behind the FT’s paywall, so not everyone will be able to read it, but the gist of his argument is that Greece’s public debt is unsustainable and hence that far-reaching default is necessary and desirable, but that Greek exit from the euro is not. I’m not sure that he expects Greece to stay in, but he clearly wishes that it would. And I think that is the nub of the issue: Greek exit is now likely to be in the medium-term best interests of Greece, but is also likely to be the first step towards the total dissolution of the euro area, and perhaps the EU itself. For many, that would be the end of a dream. The words hubris and nemesis spring to mind.

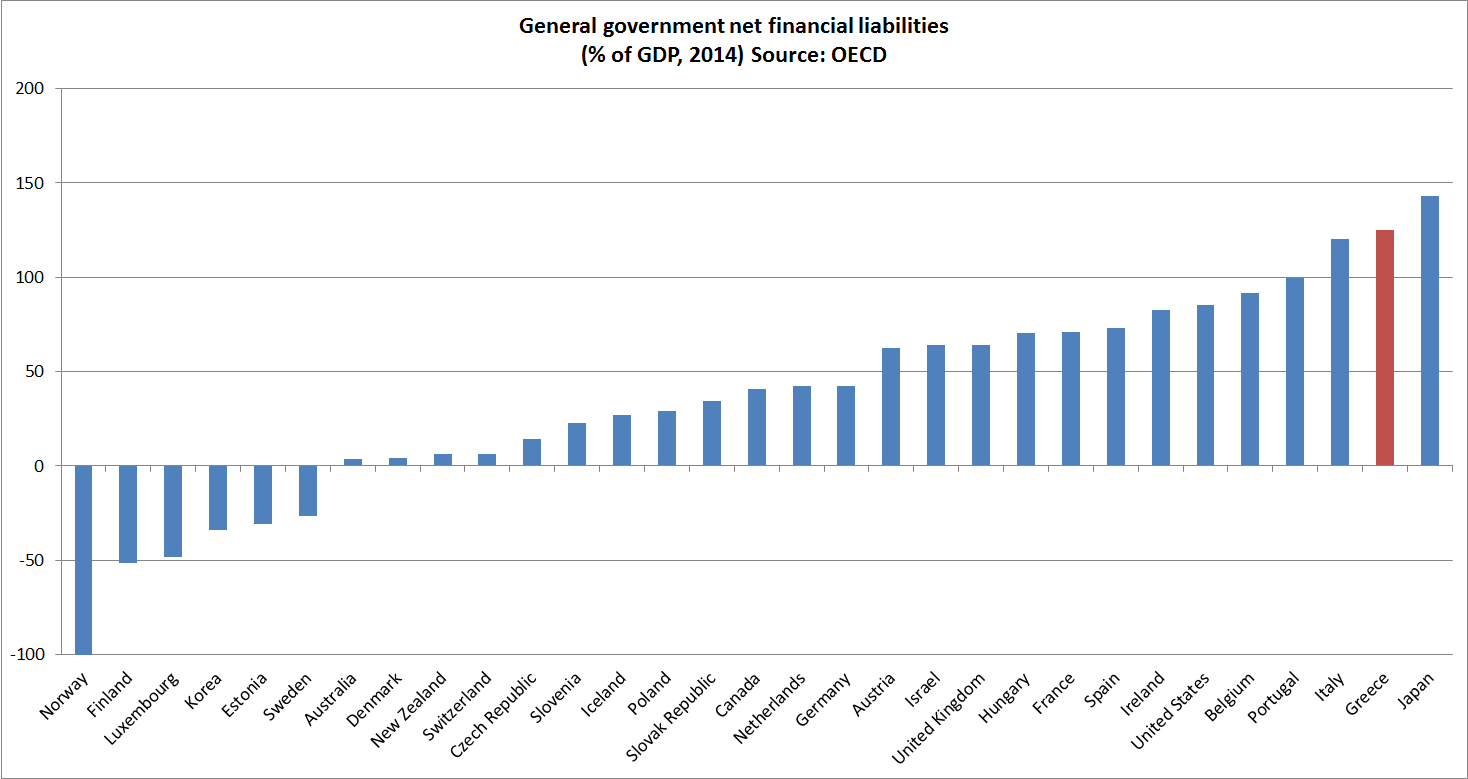

What about the Greek debt? Yes, it is certainly high. On the broadest measure I could find – the OECD’s series of general government net financial liabilities – Greece had debt of around 125 per cent of (vastly reduced, and surely not permanently lower) GDP last year. That was less debt than Japan had, and only slightly more than Italy. Portugal is not that far behind, with net financial liabilities of around 100 per cent of GDP. Belgium had a debt level similar to Greece’s for much of the 1990s, when world real interest rates were much higher than they are now. Historically, the UK and the US emerged from wars with much higher debt levels. But, nearer to home, New Zealand and Australia spent the 50 years prior to World War Two with far higher levels of public (and external) debt. There were modest defaults and creditor remissions during the Great Depression, but the bulk of the debt was successfully serviced by the citizens of our two countries.

And Greece has already achieved substantial reductions, and deferrals, in its debt servicing burden. Interest payments on its government debt (mostly non-market debt now) are less than those facing Italy and Portugal, and not much above those of Ireland. Sovereign debt service is largely a sovereign choice. Markets haven’t been willing to lend much, and for term, to Greece for the last five years, no doubt taking a view on the choices Greece was likely (again) to make.

I’m not suggesting that Greece shouldn’t default[1], but the much more important issue is competitiveness – the ability to achieve growth in the real and nominal economy. With nominal GDP at 2008 levels, all else equal, Greece, would have debt ratios not much higher than those of the United States. For decades, the ability to devalue one’s currency has been seen as the least costly (there are no no-cost options) way to put an economy back on a path to export-oriented growth in demand. That option was given up by countries adopting the euro, without seriously considering their ability to cope with severe shocks. The political imperatives of European unity – and in Greece’s case of being fully part of modern democratic Europe, only 25 years on from a brutal military dictatorship – seemed to override all other considerations, and the little-considered tail risks.

But now, contemplate the horror of Greece. Output losses match those seen in the worst-performing countries of the Great Depression. The unemployment rate is ruinous. And even before the election of SYRIZA, there was little or no sign of any sort of rapid recovery. Some competitiveness indicators were looking better, but the bottom line was the willingness of firms to invest and there was little sign last year of the private sector champing at the bit to invest heavily in tradable sectors. Greece’s difficulties were only compounded by the troubles (and falling currency) of its largest trading partner, Russia. No doubt many of the micro reforms being proposed by the Troika were sensible, and even necessary, but they didn’t address the more immediate issue, of a catastrophic failure of demand. Greece cannot adjust its nominal exchange rate, and it cannot adjust its nominal interest rate, even though much lower real interest rates and real exchange rates would have been a standard prescription for any other country in such a difficult position. Further debt relief – even if it were politically feasible for the rest of Europe – doesn’t materially improve Greece’s competitiveness position or ability to materially boost demand.

Exit from the euro area will be difficult for Greece. Greek public opinion has wanted to stay in the euro. But Greek public opinion also recoils at the output and employment losses. The latter are only worsening as the degree of confidence around Greece’s position in the euro deteriorates. Only a very brave person would invest in Greece now, with such extreme uncertainty about the transitions over the next year or two. But experience suggests that after a rocky period over the first year or so out of the euro, and perhaps many long-running law suits, a substantial real depreciation would be likely to put Greece on a much stronger path.

What of the rest of the euro area? Relative to 2010, Europe is much better placed to deal with the short-term ramifications of a Greek default and exit. Very little of the Greek debt is held by private banking institutions in the rest of Europe, and the connections between the Greek banking system and the private banking systems and those of the rest of Europe are also much weaker.

But that is about the very short-term. What seems somewhat underplayed is the risk – the likelihood in my view – that a Greek exit would be like punching the first hole in the dike. Before long, the pressures that would build up – political pressures and then market pressures would become increasingly irresistible. The poorer members of the EU are the ones most resisting concessions to Greece. Why? Because concessions to Greece will only feed domestic sentiment along the lines of “and why not us too”. Tyler Cowen highlighted little Slovenia yesterday. But what of Spain, where the radical Podemos party has already been leading the polls. Or France, where Martine Le Pen’s Eurosceptic National Front looms. And that is before anyone has broken out. What if, a year down the track, signs of recovery were becoming apparent in Greece? Why not us, populist movements in countries with severe unemployment such as Spain or Portugal might ask? And what of German citizens, many of whom never regarded the euro as offering anything much to them. A comprehensive Greek default will mean default on Greece’s huge debts to the ECB, through the TARGET clearing and settlement system. Germany is the largest European economy, and holds the largest claims on the ECB, and will face very large losses. The backlash is unlikely to be pretty, or easy for the government to manage.

There was a strong “end of history” sense to narratives around the creation of the euro: time’s winged arrow going only in one direction, to a union indissoluble and irrevocable. Despite the rhetoric, that was never very likely. The euro has been in place for 16 years – a reasonable run by the standards of modern currency regimes. Bretton Woods didn’t last much longer, in its various forms. Successor regimes – and those in the decades prior to World War Two – lasted for much shorter periods. The euro was an ambitious vision, but time has proved it to be deeply flawed. The growth record been almost inconceivably bad – far worse in the euro area than in the rest of the advanced world. Of course, not all of those poor outcomes can be put down to the euro, but in many countries the chaos of the last decade is a direct result of that choice. The increasing risk is that the backlash to this grand experiment will jeopardise much that was relatively good in the wider EU project – opening and integrating (even if over-regulating) goods and services and factor markets. No wonder the euro-area and EU elites are so desperate now. They are looking into the abyss.

UPDATE: I largely agree with this piece by Ashoka Mody, who suggests the IMF should write off its Greek debt. Perhaps, but it won’t happen. Preferred creditor status doesn’t exist in law, but in practice it is very strong. Perhaps France and Germany should pay the IMF debt for Greece – since they were the main beneficiaries of the 2010 package – but that is not going to happen either. Outcomes would be very difficult if there were some deus ex machina. pulling strings and coordinating all the moving pieces. But God doesn’t typically do macroeconomic management/

[1] Although my prediction is that in the end the debt to the IMF will be paid in full, even if arrears build up for a time.

What amazes me is that the ECB thinks this outcome is preferable to even a little bit of reflation.

LikeLike

I doubt they do. I think Draghi is serious about the “whatever it takes” rhetoric, but without dealing with the zero lower bound issue – which is harder in a union like that, than in a single country, and no one has even started doing so in a single country – there are pretty severe limits to what monetary policy can now do.

Recall, that if the bad outcome happens the ECB itself will disappear, amid huge and bitter recriminations,and those on the bridge when it happens aren’t likely to be that well-remembered/regarded by history.

LikeLike

(I agree it’s a bit late now. But the ECB has many sins to atone for, like raising rates in 2011.)

Very good essay, Michael. I hope it gets widely read.

LikeLike

The anglo saxon world continues to underestimate that 80 pct of Greeks want to stay in Euro currency.

LikeLike

I’m sure 100% of Greeks want a stronger economy. But I guess my real question is whether there is any politically feasible way for Greece to stay in – politically feasible across the other euro area countries, and Greece.

LikeLike

[…] understating the severity of the risks if Greece were to leave the euro. Earlier in the week, I argued that Greek exit may well set off a chain of events that, in time, leads to the complete dissolution […]

LikeLike

[…] line is similar to ones I’ve run in a couple of recent posts (here and here), although my focus has been more on the idea that there is no politically saleable path […]

LikeLike