Patrick Honohan, Governor of the Central Bank of Ireland, gave a fascinating presentation earlier this week on Currency Choices in Ireland Past and Present. There was even something for geeky history buffs ( I didn’t realise, for example, that for the first 25 years after the Act of Union, Ireland and Britain had had separate currencies, with a variable exchange rate between them). But the more immediate interest was in Honohan’s attempt to put Ireland’s choice of, and experience with, the euro in historical context. From 1826 to 1979 Ireland had either used sterling, or had an exchange rate firmly pegged to sterling. Effective monetary independence lasted for less than 20 years.

Honohan’s goal is to hose down a narrative that says the entering the euro was a mistake for Ireland. As he notes “poor economic choices and bad luck are more reliable determinants of episodes of poor economic performance than choice of exchange rate regime”.

Serving Governors can’t exactly go round publically bagging their own country’s exchange rate regime. But the claim that adopting the euro is just another currency choice, of second order importance, seems a step too far. The Irish Famine aside, the recent post-crisis shakeout has been the worst sustained period of (no) economic growth in Ireland’s modern economic history. Ireland actually got through the Great Depression relatively well. And while Angus Maddison’s estimates don’t cover the few years leading up to independence and the civil war following it, even if that period was worse economically the benchmark for good modern exchange rate regime choices has to be set a little higher than “well, out-turns weren’t quite as bad as those in the civil war”.

In fairness to Honohan, he isn’t indifferent to the dislocations and huge cost of the last few years. But he argues that the fault “lies not so much in the system’s design as in the inadequacy of national economic and financial policies to take account of the risks that were still associated with the euro”. Oh, and he notes that in non-euro countries there were crises too.

In principle, so it is argued, very stringent fiscal policies and very conservative bank supervision and regulation – neither of which featured in Ireland – might have made all the difference. But this looks like some sort of counsel of perfection – and perfection isn’t a standard we can expect from our politicians and policymakers. Would a central bank that tried to impose consistently very tough prudential standards have been allowed to get away with it? Would the Governor of such a robust institution have been reappointed? And while Ireland no doubt should have run bigger fiscal surpluses, and (in particular) made its tax system less dependent on sources that would dry up when property turnover did, large surpluses invite electoral auctions. We saw it here in 2005. Institutional choices – including exchange rate regimes – need to take account of how democracies actually work.

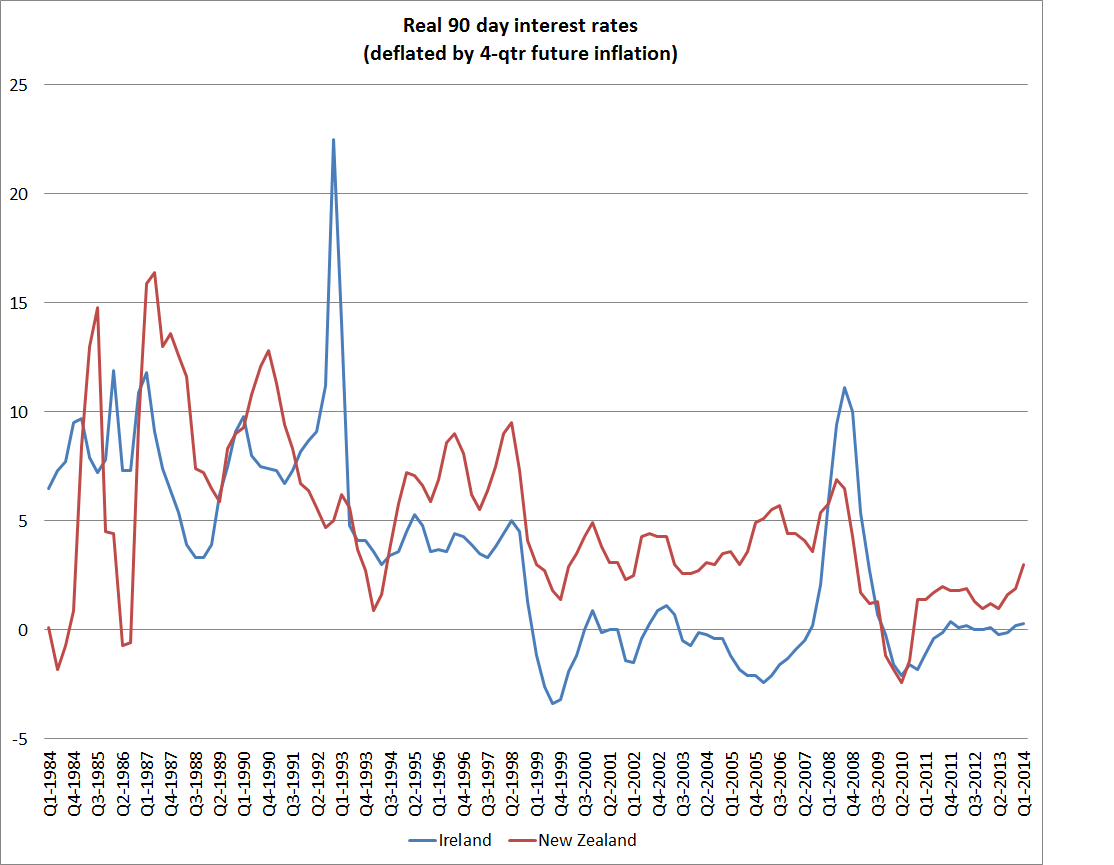

The Irish could, and no doubt should, have managed the boom years better. But what they got looks a lot like what one would expect if one takes an economy with a neutral interest rate that might have been similar to New Zealand’s and gives it an actual interest rate set mainly for Germany and France. If New Zealand nominal interest rates had been set at German, or US, levels since the late 1990s we would have ended up with a pretty spectacular bust as well. Honohan runs the Irish version of this chart in his speech.

Ireland will survive, and in time will prosper again. Exchange rate regimes don’t shape long-term prosperity. But with hindsight, it is difficult not to think that Ireland would have been a lot better off with a floating exchange rate, like New Zealand, with interest rates set for its own domestic economic conditions, than in the euro. Floating exchange rates are no panacea – and the last decade hasn’t seen great economic performance here either – but it is hard to escape the point that the worst performing advanced countries since 2007 have almost all been members of the euro.

But read it yourself, and see how persuasive you find Honohan’s story.