Today’s CPI numbers must surely kick one of the last few remaining supports out from under the Reserve Bank’s view of inflation and monetary policy. Yes, the headline number was slightly less low than they had forecast. But the real issue here isn’t about actual inflation vs the projections of a few weeks ago, but about the underlying picture of inflation.

Ever since the end of the 2008/09 recession, the Bank has been telling us that inflation was going to pick up again. And it did briefly, as in quite a few other advanced countries. New Zealand’s non-tradables inflation (ex GST) got up to around 3 per cent in 2011. Like New Zealand, a wide range of other OECD countries (although not the US or UK) actually raised policy interest rates in 2010/11. With hindsight it was unnecessary, but on the evidence to hand they were probably reasonable calls at the time.

But our Reserve Bank has gone on picking that inflation would rise. For a time it still seemed plausible, as the scale of the repair process in Christchurch after the 2010/11 earthquakes became apparent. In fairness to the Reserve Bank, most of the local market economists have been even more convinced that inflation would rise (and more “hawkish” on policy).

But it just has not happened. There have been isolated pockets of inflation. Some of it was just taxes – Tariana Turia’s gift to closing the deficit in the form of repeated increases in tobacco taxes. And construction costs did rise, especially in Christchurch. Big real shocks typically induce relative price changes. And there was no widespread spillover of Christchurch construction cost inflation to the rest of the economy.

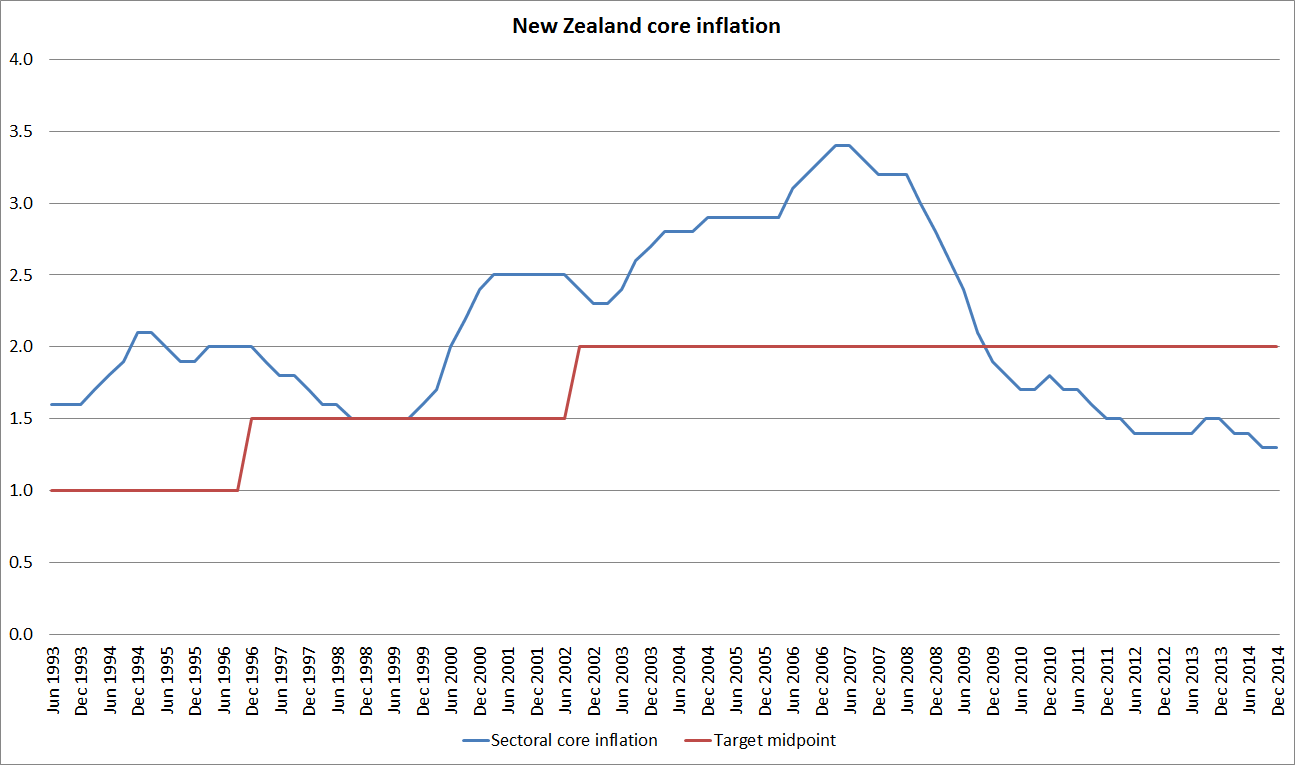

Where do we stand now? I’m not mentioning headline inflation – it didn’t matter much when it was nearly 5 per cent, and it doesn’t matter that much that it is currently nearly zero. But the Reserve Bank’s best estimate of core inflation – the sectoral factor model – was last above 2 per cent in the year to December 2009. It hung around 1.5 per cent for some time, and in the last couple of quarters has fallen again, and it is now around 1.3 per cent. This is a very slow-moving series, and being that close to the bottom of the target range should be of serious concern to the Reserve Bank.

Concern should be mounting because other core measures, while perhaps less informative (noisier), are at least as weak. Trimmed mean inflation – the best of the rest in my view – was 0.6 per cent in the year to March. That measure is constructed in a way that will have given no weight to falling petrol prices or rising cigarette prices. I could go on. Non-tradables should probably be around 3 per cent when overall CPI inflation is on target at 2 per cent. Non-tradables inflation got as high as 3 per cent in the year to last March as construction cost inflation picked up, but was only 2.3 per cent in the year to March 2015 – barely above the lows reached in the depths of the recession.

Is there comfort anywhere else? I don’t think so. Wage inflation is showing no sign of picking up, inflation expectations are likely to keep falling, and a high exchange rate can’t even really be blamed for low headline inflation – the exchange rate in recent months has been lower than (certainly no higher than) it was early last year.

Inflation globally is weak. Commodity prices are falling. Growth in China – the largest component in global growth in recent years – is weakening. And although there is still a lot of building activity going on in Christchurch there is little sign of pressure on resources (or inflation) getting more intense there. It is very difficult to see core inflation rising from here, on anything like current policy.

The case for OCR increases last year was always weak, but it was within a range of plausible outcomes. But time showed that those increases were unnecessary, and the Bank has gradually abandoned the plans the Governor had talked about of raising the OCR by 200 basis points. What isn’t clear is why the Bank won’t now reverse the unnecessary OCR increases. Inflation is well below target, and has repeatedly surprised on the low side. Unemployment is still above any reasonable sense of a NAIRU, the recovery has not been strong by historical standards, and the Bank repeatedly anguishes in its policy statements about an overvalued exchange rate.

No one knows the future, and even forecasts of the near-future should be held rather lightly. But when (Bank and market economist) forecasts have been consistently wrong, there is a strong case for looking out the window and reacting to what we see now. And what we see is low and falling inflation, subdued credit growth, quite-high unemployment, and a troublingly high exchange rate. House price inflation is certainly higher than most would like, but the Governor told us at the March Monetary Policy Statement that house prices were not a particular factor in his recent interest rate decisions.

Most other advanced and emerging countries have been cutting policy rates in the last year. Today’s inflation number is further evidence that New Zealand should join them. A strict inflation targeter would (if there were any such) but a flexible one certainly now should be.