The Dominion-Post reported yesterday on the results of the latest Westpac (in association with the Productivity Commission) Grow New Zealand survey of “nearly 1200 small and medium businesses” with turnover ranging from $250000 to $5 million. The results were interesting – data almost always are – including the comparisons with the earlier 2011 report, taken when the economy was only just beginning to emerge from the recession. But the interpretations placed on the results were what caught my eye.

In the 2015 survey many fewer respondents saw the “current state of the market” and “lack of funds” as the main obstacle to growth in their own business. As those obstacles had been removed, more cited a desire to “maintain my work/life balance” and “want to retire/leave the business” soon. These results shouldn’t surprise us. After all, in 2011 the recession had only just ended – times were tougher, on average, for businesses. In 2015, many business owners reasonably enough feel that they have more choices.

There has been a popular line running round the New Zealand debate for some years that what ails New Zealand is lifestyle – the people who run New Zealand small and medium businesses don’t have the hunger they perhaps “should” or could have, and are instead content to get to a certain scale and then settle for a very comfortable lifestyle, characterised as “bach, boat, and BMW”. The Dom-Post journalist uses the Westpac survey results to give this line another run. The chair of the Productivity Commission is reporting as suggesting that “in the more competitive United States market, the concept of taking it easy for the purposes of leisure time was unheard of.”

But how seriously should we take the “bach, boat and BMW” syndrome as an obstacle to growth? New Zealanders work longer hours per capita than their peers in most Western advanced economies, and it isn’t obvious why we should assume that our business owners are particularly different. And are US small and medium business owners really so different? The US is a very big and diverse country, and perhaps there is a risk of forgetting that for every Microsoft or Oracle there are thousands of small businesses in small towns and medium-sized cities, often protected by occupational licensing and entry restrictions that make New Zealand look intensely competitive. Many owners will be keen on a round of golf on Wednesday afternoon, or just the flexibility that comes with being one’s own boss. The range of factors that motivate people to set up a business is likely to be as diverse there as here.

In preparing its first report in 2009, the 2025 Taskforce – charged with understanding why New Zealand GDP per capita lagged so far behind Australia’s (and other advanced countries) – went through some of the common arguments. Here is what they said (and if the prose style feels familiar, I drafted it for the Taskforce):

Sometimes it is also claimed that successful New Zealand business people are too willing to cash up too soon, and enjoy the fruits of success (the boat, bach, and BMW) rather than continuing to build their businesses up. We have not encountered any systematic evidence to support this claim. Everywhere in the world, some people build businesses, and then cash up to enjoy the fruits – from successful merchants or industrialists retiring from Manchester to build elegant country houses in the 19th century, to businessmen selling up to go into politics. Some will be talented creators, but not natural managers of large enterprises. Some will have owed their success as much to good fortune as to innate skill: for them, selling up and crystallizing the gains is likely to be a very prudent step. Others will simply put a higher value on other things in life than making more money. In any society – especially one New Zealand’s size – there are likely to be only a relatively few highly successful highly-driven entrepreneurs.

Tastes and preferences vary, but I reckon that in a country that was once among the very richest in the world, peopled with those whose ancestors made the costly effort to come to uttermost parts of the earth to build a better life, we would be better off looking for the pitfalls in government policy for the answers than in suggesting that our business owners are somehow letting us down by through their own lifestyle preferences

Incidentally, in the same article I noticed Murray Sherwin quoted as suggesting that the survey results “reflect that New Zealand has had a very good global financial crisis compared to most”. I was a bit puzzled, and emailed Murray, who tells me that what he had in mind was GDP per hour worked. Growth in GDP per hour worked has slowed a lot since 2007 when compared with the previous decade, but the slowing has certainly been less marked here than in many advanced countries.

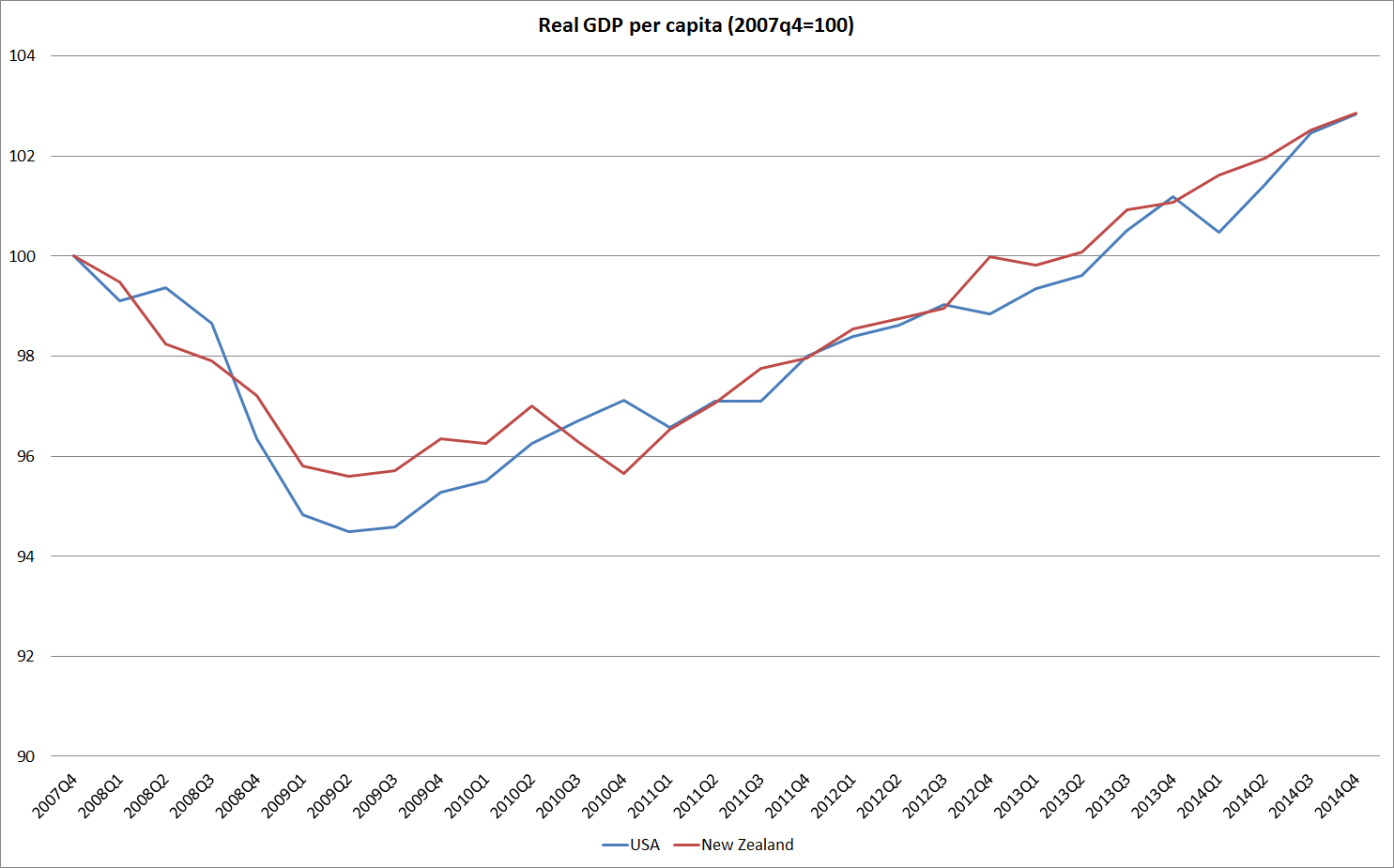

But our overall economic performance since 2007 – just before the global crisis hit – has been mediocre at best. We’ve had lots of advantages – high terms of trade, no domestic financial crisis, and no major external constraints on using macro policy (not in the euro, avoided the near-zero lower bound) – and yet in GDP per capita terms we’ve tracked very similarly to the United States, the country at the epicentre of the initial crisis. Even that picture flatters us: US productivity has been better than New Zealand’s, but we’ve made up for it with more people working. It could have been worse – and in most euro-area countries it has been – but the years since 2007 haven’t been good ones for New Zealand.