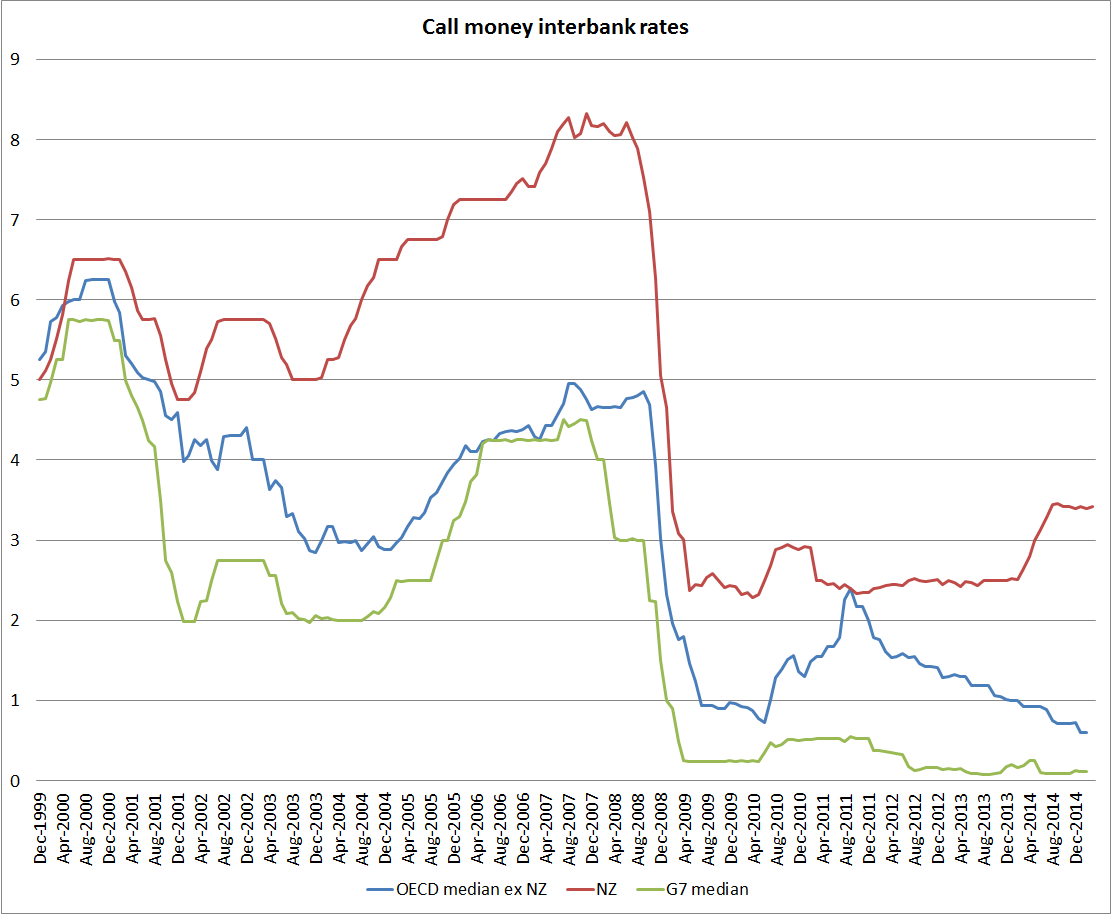

This is one of my favourite troubling charts of the last year or two. It uses OECD data to proxy policy interest rates (they describe them as “call money interbank rates”. I’ve shown three lines: New Zealand, a median for the G7 countries (in this case the US, the UK, the euro area (for Germany, Italy, and France), Japan, and Canada) and a median for all 20 countries/regions in the OECD with the ability to set their own policy rates. I’ve gone back 15 years, to the end of 1999 – a point where the gap between NZ and foreign rates was unusually low.

Two things have troubled me about the chart:

- the growing divergence between New Zealand and foreign rates over the last couple of years. New Zealand and foreign short-term interest rates won’t always move together, but when they diverge we should be able to identify specific developments in inflation (as almost all these countries are now inflation targeters) to warrant the divergence. Forecasts of inflation may have diverged in ways that suggested higher New Zealand interest rates, but actual inflation (headline or core) has been at least as weak, relative to target, as we’ve seen in the typical advanced economy.

- perhaps more important, is that near-flat line for the G7 countries (and one could add several others to that list of countries) for now six years or so. It would be some sort of miracle if appropriate interest rates had been so stable for so long. In fact, what we have seen is countries reacting to the perception of a lower bound on nominal interest rates at or very near zero.

The idea of the zero lower bound has been around for a long time, When Japan got there most of us still treated it as an idiosyncratic curiosity. And no country has yet taken policy interest rates as low as they can effectively go. We know this because in no country has there been a large scale switch into physical cash holdings (the option that makes the near-zero bound troublesome). But when policy rates have been at or very near the practical bound for so long, it suggests they would appropriately have gone materially lower had that been possible. Combined with lingering high unemployment (or low participation in the US case) and weak inflation, they continue to point to a shortage of demand as a problem in most advanced countries.

As concerning is that, six years on, it appears that no central bank (of finance ministry) has taken a lead to reduce the risk that the zero bound will be an even more major problem in the next recession. We don’t know when that will be, and hope it will be years away, but that can’t be guaranteed, especially as emerging market growth slows and recessionary risks rise in those countries. And next time, most advanced countries might go into a recession from a cyclical high in policy rates of perhaps 0.25 per cent. And New Zealand, which cut by 575 points last time, could well peak this cycle at a 3.5 per cent OCR.

One problem has been the constant belief – in markets and central banks – that a sustained upturn is just around the corner, and with it the basis for higher policy rates. Both markets and central banks have been repeatedly wrong. But we should hope that in the backrooms of major central banks serious practical work is underway to alleviate the (actual or felt) constraint of the ZLB before the next significant downturn.

I have a few ideas, and will discuss some of them in a future post.