First, welcome to those readers who’ve come here today as a result of Tyler Cowen’s brief mention on Marginal Revolution. I’ve set out something of my background, and what I’m trying to do, here. My focus tends to be on New Zealand issues – macro and micro – but I’ll also be offering some perspectives on international issues, especially around inflation targeting, financial regulation, and the euro.

Last week, my old boss Grant Spencer, Deputy Governor of the Reserve Bank, gave a speech outlining his view of what needed to be done about the New Zealand housing market. National house prices are high, and rising, but the house price inflation is now mostly a phenomenon of our largest city, Auckland . I was quite critical of a number of aspects of the speech, and commented here, here, and outlined my own perspective on New Zealand policy here. My main criticism of the speech was the absence of any serious analysis on the scale and nature of the financial stability risks it is asserted that New Zealand faces.

New Zealand’s biggest-circulation daily newspaper, the Auckland-based New Zealand Herald has given Spencer’s speech considerable, and almost entirely favourable, coverage, with both an editorial and political and business columnists weighing in in support. The Reserve Bank might be a little embarrassed by some of the support.

The Herald’s political correspondent John Armstrong began his Saturday column asserting that “the overheated Auckland property market makes the South Seas Bubble of the 1700s look like an exercise in financial probity”. As Charles Kindleberger wrote in his classic account of Manias, Panics, and Crashes, “Some bubbles are swindles, some are not. … The South Seas Bubble was a swindle”. In a more litigious society, the local banks might this morning be consulting their lawyers on this preposterous claim, and the associated slur on the banks’ lending practices and standards. As a reminder, the stock of loans to households is growing at around 5 per cent per annum (as it total Private Sector Credit), while nominal GDP can be expected to grow at around 4.5 per cent. There has been no growth in household debt/disposable income, or in private sector credit/GDP since 2007. There is simply no evidence of widespread poor quality lending practices – and neither Armstrong, nor the Reserve Bank, has provided evidence to the contrary. That is a very different than the US position towards the end of its housing boom, which I discussed last week.

Fran O’Sullivan has been writing about New Zealand business, economics and politics for decades. In her weekend column on Spencer’s speech (under the sub-heading “Failure to heed Reserve Bank’s words on possible crisis plain irresponsible”) she reaches back into New Zealand history, and the lead-up to the large exchange rate devaluation in 1984, which acted as the trigger for the wave of reforms adopted in New Zealand over the following decade. O’Sullivan adopts unquestioningly the Bank’s talk of potential crisis and threats to financial and economic stability, and draws parallels with the advice provided by the Reserve Bank and Treasury to the then Minister of Finance in the early 1980s to devalue the exchange rate.

The Bank’s then Deputy Governor, Rod Deane, had been at the forefront of the analysis and advice provided to Robert Muldoon, then Minister of Finance and Prime Minister. Deane was probably the greatest figure in the history of the Reserve Bank of New Zealand, building up its policy and research capabilities and giving it voice and influence within Wellington official circles. His legacy at the Bank lasted for many years.

In the early 1980s Deane paid a high price for the courageous analysis and advice that he was primarily responsible for: Muldoon refused to appoint him as Governor. The Bank at the time generated a lot of practically-oriented research and analysis, and had done a lot of work not just about how to end New Zealand’s lamentable inflation record, but also about how to restructure and reform the New Zealand economy, with a focus on the macroeconomic dimensions of those issues. There was a generally shared view among the economic elites at the time that a much lower real exchange rate was likely to be an essential part of rebalancing the New Zealand economy, and putting it on a path in which the growing external debt and the decline in New Zealand’s relative living standards could begin to be reversed.

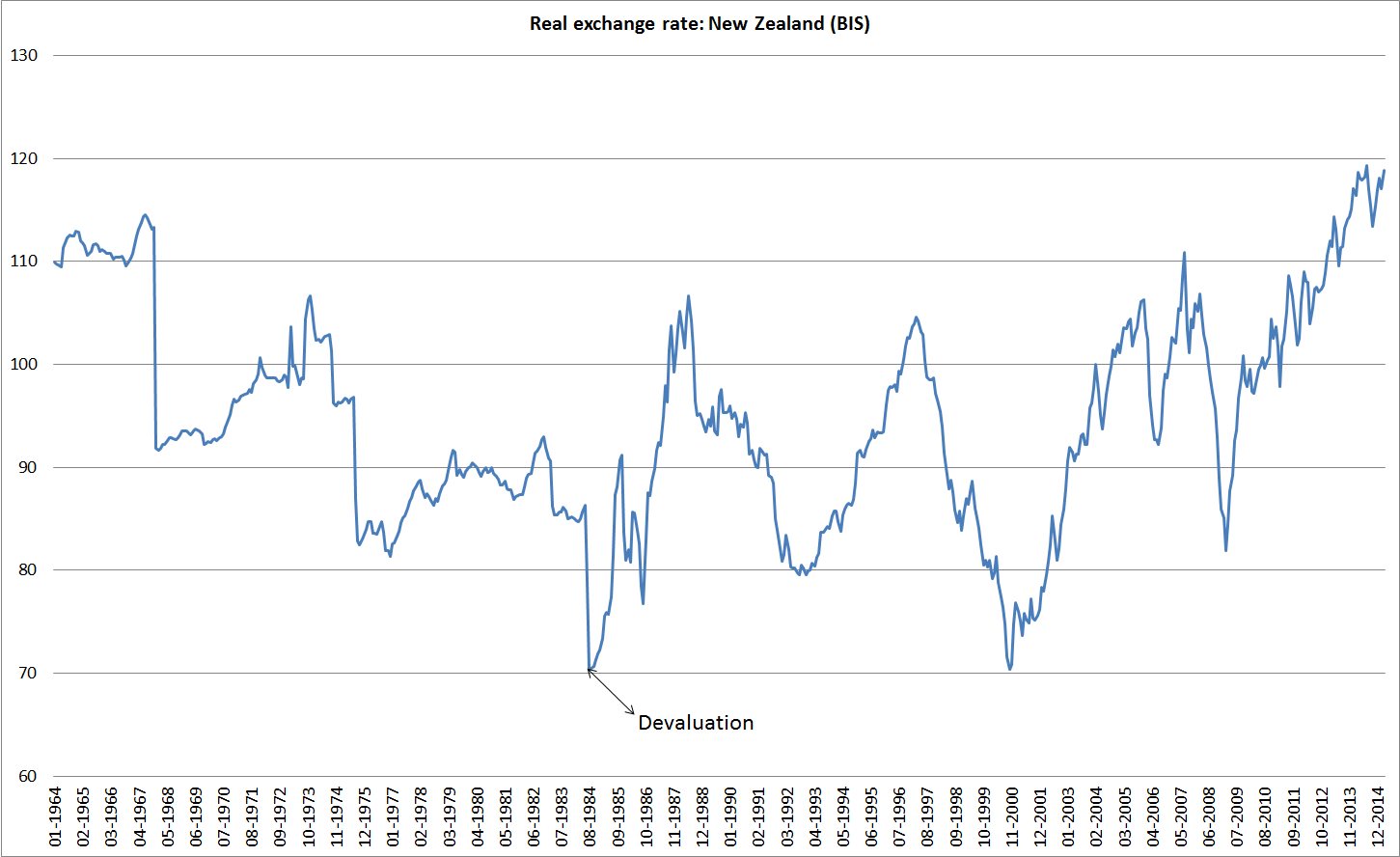

As New Zealand readers know, New Zealand was forced into a 20 per cent devaluation in July 1984 – the timing was “forced” by a combination of interest rate controls and a growing conviction that the likely new government wanted to devalue anyway. Among elite bureaucratic circles there was a strong sense that the devaluation was a first step to rebalancing the economy and re-stimulating the tradables sectors. I was a first year graduate at the time, sent along on occasion to take minutes of meetings of key figures in the Reserve Bank and Treasury: there was a very strong sense that the biggest macroeconomic policy challenge was to “cement in” the new lower real exchange rate. There was no discussion around the possibility that the new lower real exchange rate might not prove to be sustainable.

And yet here is the chart of the New Zealand’s real exchange rate (using the BIS measure, as the RB has not yet backdated their measure far enough). The 1984 devaluation certainly stands out, but not as some turning point in New Zealand’s competitiveness. Rather it stands out as a level only once reached again – and then very briefly – in the subsequent 30 years.

In short, they were wrong. Not wrong, in my view, about the longer-term challenges. I’ve argued that the failure of the real exchange rate to move sustainably lower, to reflect long-term adverse productivity growth differentials, is a key proximate marker (please note that I did not use “cause”) of what has gone wrong with New Zealand’s economy over the long term. But real exchange rate can’t be adjusted, by ministers and senior officials, in a vacuum. I have the utmost regard for people like Rod Deane, and some of his Treasury counterparts. But on this issue – where Fran O’Sullivan lauds them as heroically correct – they were simply wrong, or incomplete in their analysis of what achieving a sustainably lower real exchange rate would require. And that despite a lot of expert analysis and research, laid out in books, and discussion papers, and Bulletin articles. The limitations of knowledge we all face – great figures like Rod Deane not much less than the rest of us – seems to get continually swept under the carpet.

As I pointed out the other day, I’m not remotely relaxed about Auckland property prices. They are a social and political scandal. But they look like the rational outcome of a misguided set of central and local government policies (supply and land use restrictions, combined with high trend target levels of non-citizen immigration). No one knows when, or even if, such policies will be changed.

But the weight that should be given to the Reserve Bank’s arguments around housing depends on its claim that financial stability is being materially jeopardised. New Zealand banks have high levels of capital, and are subject to high minimum risk weights on housing loans. The Reserve Bank’s own stress tests suggest a high degree of resilience at present, even if house prices were to fall sharply in Auckland (they have been falling in various other places in the country). If the Reserve Bank really believes there is a growing risk of financial crisis, they should set out their analysis and evidence. A good start might be to answer the question as to whether there has ever been a systemic financial crisis in a system where the stock of credit has been growing at only around 5 per cent per annum, and at growth rates than haven’t exceeded average nominal GDP growth for a number of years. Perhaps there are such cases – the Reserve Bank has more resources than I do, and should be able to lay them out for us. In the meantime, John Key and Bill English might usefully set the Bank’s warnings to one side (while still thinking hard about housing supply and immigration issues) and perhaps have a quiet word with the Bank’s Board about their performance monitoring of the Governor and his team.

UPDATE: A nice piece from Oliver Hartwich on the importance of expectations. Of course, this is true not just of possible housing supply responsiveness reforms such as those he (and I for that matter) would favour, but of any changes in migration targets, or (indeed) complex tax regime changes as well.

An interesting article, up until the last sentence – which lacks any sort of grace or charm, at all.

LikeLike

Martin

Thanks for the feedback. The final sentence certainly wasn’t intended that way, so I’m sorry if that is the way it came across. But if the head of a government department, or one of his/her deputies, gave such a speech on highly contentious political issues, with so little supporting analysis, I’d expect the relevant ministers to raise questions, both with the CEO and with the SSC (as employing and performance monitoring agent for public service CEOs). The Reserve Bank’s Board plays essentially the SSC’s role in respect of the Bank’s Governor.

LikeLike

Given we have a central bank that is undershooting its inflation target pretty badly and our two leading columnists seem intent on egging it on, I would tend to class this as a case of speaking truth to power rather than as a failure of decorum. The Bank has been dealing with uninformed criticism for years, so a small dose of informed criticism should be a blessed relief.

LikeLike