Last week I posted the brief submission I had made to the Reserve Bank on its consultation document on residential mortgage loans for investment purposes. I suggested that the case for a separate risk class for investor property loans had not yet been convincingly made.

I noted then that the Reserve Bank had not set out convincing evidence on the loan loss experience on investment property loans. In particular, although investor property default rates in the UK and Ireland had been higher than those on owner occupier loans, the Reserve Bank had made no attempt to show whether this difference reflected the purpose for which the loan was being take (ie investor property vs owner-occupier), or the characteristics of the respective borrowers. I hypothesised, for example, that many of the UK and Irish buy-to-let loans may have been taken out very late in the boom, and – if so – the typical borrower was likely to have had a higher loan-to-value ratio and more stressed income servicing requirements than the average owner-occupier borrower. If so, actual loan losses on investor property loans would be higher than those on owner occupier loans. But the factors behind those differences (higher LVRs, higher debt service requirements) should already be picked up in the risk-modelling and they would not warrant separate capital requirements for investment property loans.

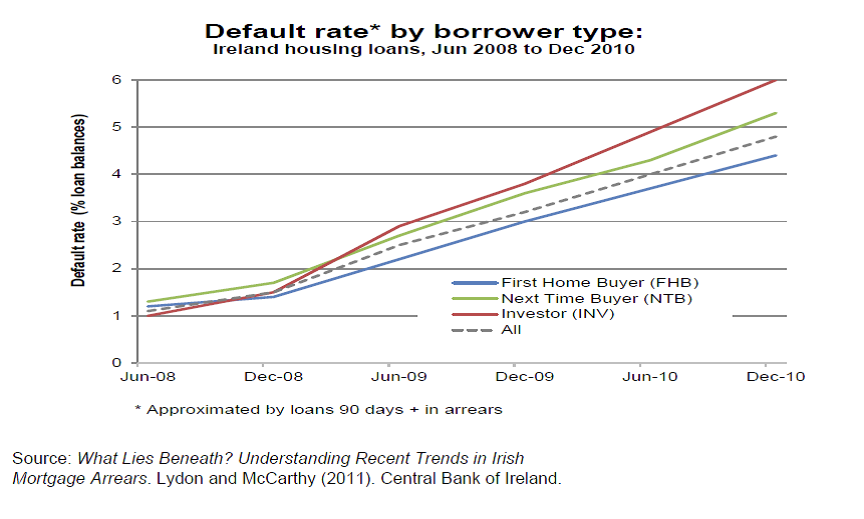

The Reserve Bank included this chart, from a 2011 Irish research paper, in their consultation document.

A reader has pointed out that the conclusions of this paper explicitly state that differences between the arrears rates for buy-to-let borrowers and owner-occupiers is reduced once allowance is made for these characteristics. And the remaining increase in buy to let default rates seems to have been largely due to the buy-to let loans being disproportionately made towards the very end of the boom when (among other things) lending standards were at their most lax). That particular paper is several years old now, no doubt there is now more data on actual loan loss experiences (not just arrears) and one should be hesitant to put too much weight on any single paper. But this was a paper the Bank itself cited. Surely the Bank needs to document more fully their claim that investment property loans, per se, are typically more risky than other types of residential mortgage loans. It is an empirical issue, and only really resolvable with good empirical evidence.

This chart, from another paper on the UK experience, illustrates how late in the cycle most British buy-to-let loans were made. Newly-minted loans tend to have higher default rates than older loans, no matter who they are made to or for what purpose

It has also been pointed out that the Reserve Bank has been a little selective in how it quoted from the Basle definitions and guidelines. As I noted, I don’t think the New Zealand authorities should be guided too much by international guidelines, but it was the Reserve Bank who cited this material in support of their position.

In paragraph 21 of their consultation document we find the following from the Basle IRB material.

Residential mortgage loans (including first and subsequent liens, term loans and revolving home equity lines of credit) are eligible for retail treatment regardless of exposure size so long as the credit is extended to an individual that is an owner occupier of the property

But they omit the rest of the paragraph (paragraph 231 of this document)

…with the understanding that supervisors exercise reasonable flexibility regarding buildings containing only a few rental units ─otherwise they are treated as corporate). Loans secured by a single or small number of condominium or co-operative residential housing units in a single building or complex also fall within the scope of the residential mortgage category. National supervisors may set limits on the maximum number of housing units per exposure.

Not only is it clear that the Basle guidelines have in mind apartment buildings (rather than the typical New Zealand rental properties) but that the Basle guidelines envisage that small investors will be treated as retail borrowers (“with the understanding that supervisors exercise reasonable flexibility regardin g buildings containing only a few rental units”).

Presumably there was no intention to mislead in putting together the consultation document, but that is likely to have been the effect. No doubt the Reserve Bank would have stern words to any bank whose disclosure documents were inadvertently misleading. Perhaps it might even require the document to be reissued.

Whatever the Basle guidelines might say, in full or in part, what matters is the evidence on the riskiness of investment property loans. At present, it remains “case not proven”. As I noted in another post the other day, it would be interesting to know what the loan loss experience has been in those regions of New Zealand where nominal house prices have fallen since 2007. Is there evidence that losses on investment property loans have been higher, all else equal (ie similar vintage, similar LVR, similar debt service ratios), than those on owner-occupier loans? If so, that would certainly make the Bank’s case for the separate classification of all investor property loans more persuasive. If not, it might reasonably lead to a rethink. If the Bank has not yet gathered such data from the registered banks (or if the banks have not supplied it with their own submissions) it might be wise to do so before implementing policy on what appears, at present, to be a rather thin base of evidence.

Hi, I do think tjis is a greatt blog. I stumbledupon it 😉

I will come back yet aagain since I bookmarked it.

May and freedom is the greatest way to change, may you be rich and

continue to help other people.

LikeLike