Last month I wrote about Peter Wallinson’s book Hidden in Plain Sight, about the role that Federal government interventions, and mandates, in the US housing finance market had played in the US housing credit boom of the late 90s and early 2000s. Wallison argued, pretty persuasively to me, that it was these interventions that drove down credit quality and which meant that when house prices in the US fell, the losses to lenders were large – much larger than has typically been seen when house prices have fallen sharply in other countries. Those losses in turn – and the uncertainty around them – was the catalyst for the US-centred financial crisis of 2007-09.

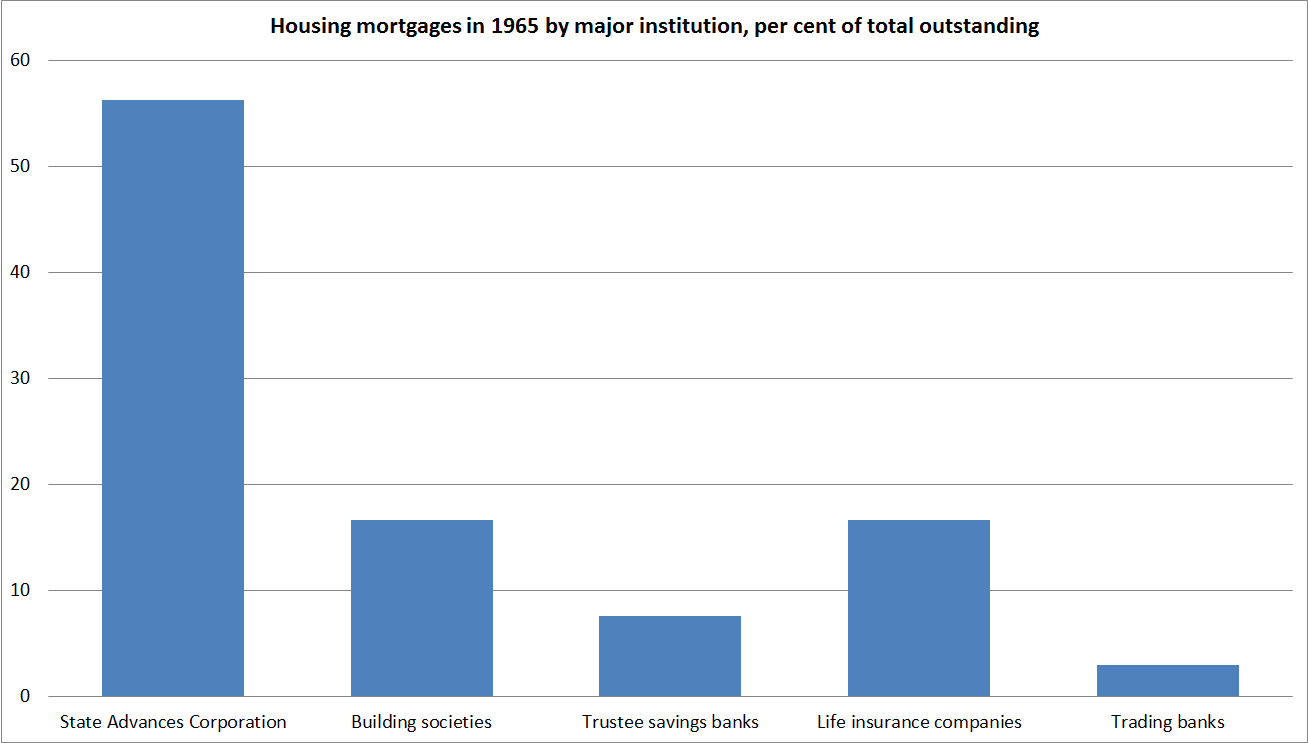

The US government has had a very large role in the housing finance market for decades now. That has become quite unusual by the standards of advanced market economies. Take New Zealand, by comparison. In the early post-war decades, most first home buyers got a mortgage from the State Advances Corporation. Indeed, the Monetary and Economic Council in their 1972 report on Monetary Policy and the Financial System reported that in 1965 just over 50 per cent of all outstanding mortgage debt advanced by financial institutions was held by the State Advances Corporation.

That lending didn’t go bad for a variety of reasons – overall debt levels were low (relative to GDP or household income), inflation increased, and credit rationing was pervasive (SAC dominated the market, but government policy was focused on administrative measures to restrain excess demand and so even SAC lending standards were not overly liberal). By contrast, any government-provided or government-guaranteed mortgages in New Zealand now make up a derisory share of the market. That has been the trend in most advanced economies in recent decades. Housing debt is now initiated by private lenders, and while those lenders have at times made mistakes, or got over-exuberant, the losses on housing loans have not typically been large enough to threaten the health of the system.

The United States was different. Not only did the government stay actively involved, but possibly in the worst possible way: mandating greater access to credit in a system where the private rewards from complying (and private costs from failing to comply) were very high. State Advances Corporation managers did not have the sorts of bonuses and options at stake – let alone the potential for merger approvals to be withheld – that characterised the US.

But I’m not writing about this today simply to rake over history, but because in some respects the US government involvement in the housing finance market has just got worse since last decade’s crisis. Around 80 per cent of all new residential mortgages initiated in the US now have a federal government guarantee.

This new short piece from Stephen Oliner, a former senior Fed official and now a fellow at the UCLA Ziman Center for Real Estate, outlines some of the facts and some of the risks. (The FHA is the Federal Housing Administration, which accounts for a quarter of all government guaranteed mortgages.) Oliner writes:

A few statistics about FHA loans are sufficient to dispel the myth that only pristine borrowers can get a mortgage. In recent months, the median credit score for borrowers who took out an FHA-guaranteed home purchase loan was 673. About two-thirds of all individuals in the U.S. have a higher credit score than that. FHA’s credit standards are loose as well for two other primary determinants of loan risk: the size of the down payment and the monthly payment burden. The median FHA borrower makes a down payment of less than five percent. If the borrower were to turn around and sell the home, the agent’s commission and other costs would exceed five percent. Hence, the median borrower is effectively underwater on day one. Second, many FHA-guaranteed loans have onerous monthly payments relative to the borrowers’ income. In fact, the payment-to-income ratio for more than four in ten FHA borrowers exceeds the ability-to-repay limit that was set in the recent Qualified Mortgage rule. This is a not a picture of tight credit.

The default rate on these FHA loans, while relatively low in today’s benign environment of solid job growth and rising home prices, would increase substantially in an ordinary recession and would skyrocket if we have another financial meltdown. To gauge the vulnerability of recently originated mortgage loans, AEI’s International Center on Housing Risk publishes every month the results of a rigorous stress test, the National Mortgage Risk Index (NMRI). The NMRI uses the default experience of loans originated in 2007 to estimate how recent loans would perform if hit with a shock akin to the 2008-09 financial crisis. The index shows that nearly 25 percent of recent FHA loan borrowers would default in that scenario. This would be exceptionally harmful, not just to the borrowers, but also to the neighborhoods in which they live and to the taxpayers who would have to make good on the FHA’s loan guarantees.

Note that well: the median FHA borrower – and typical FHA borrowers have low credit scores – has a down payment of less than 5 per cent.

The US systemic risks are not nearly as great as those in 2007. The total stock of mortgage debt is growing much less rapidly, and so far most US housing markets seem less overheated. But it is a reminder both of how hugely distorted the US housing finance market is, and a contrast to the sorts of housing finance markets we see in New Zealand, Australia, or the UK. In those latter countries, private lenders make their own assessment of the riskiness of the loans they are making, and of the wider market. And those private lenders have their own shareholders’ money primarily at stake. The risks here are simply very different from those in the United States – both pre-crisis, and now. For that, we should be very grateful. But we also need to recognise that it is not primarily a matter of grace, but of superior policy. When governments stay out of markets things are – generally – much less likely to go spectacularly wrong.