I wasn’t really intending to post anything today, but this morning I was sitting in the sun watching my daughter’s soccer and reading last week’s Spectator, where I found Nigel Lawson – former Conservative Chancellor of the Exchequer – suggesting that:

It is widely accepted overseas that the UK economic recovery since the 2008 banking meltdown is a significant success story, certainly compared with all other major economies except that of the US

That hadn’t been my impression, but (even allowing for the political motivation behind the comments) I thought it was worth having another quick look at the data. I wasn’t sure which countries Lawson might have had in mind, but I took the G7 countries, and added Spain and Korea (both bigger than Canada) and the Netherlands. That made 10 countries in total.

Not wanting to attempt anything very ambitious I downloaded some series from the latest WEO database and looked at a few charts.

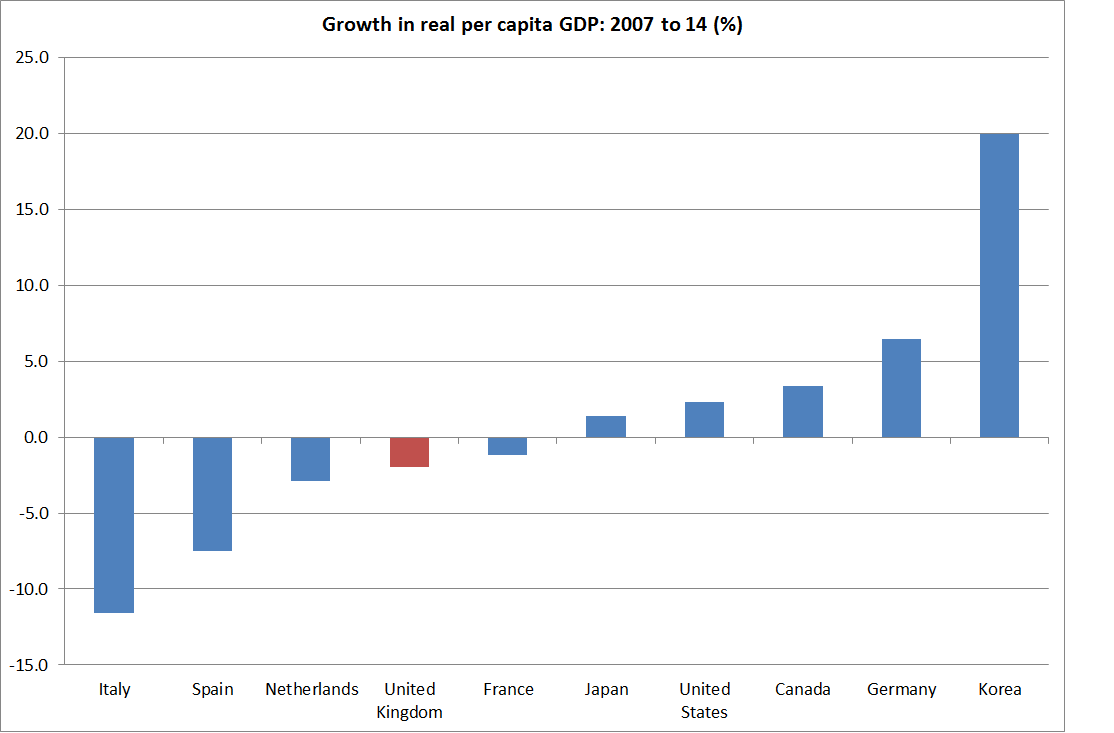

The first was per capita real GDP growth from 2007 to 20014. The median country had had around zero growth over 7 years, while per capita GDP fell 2 per cent in the UK.

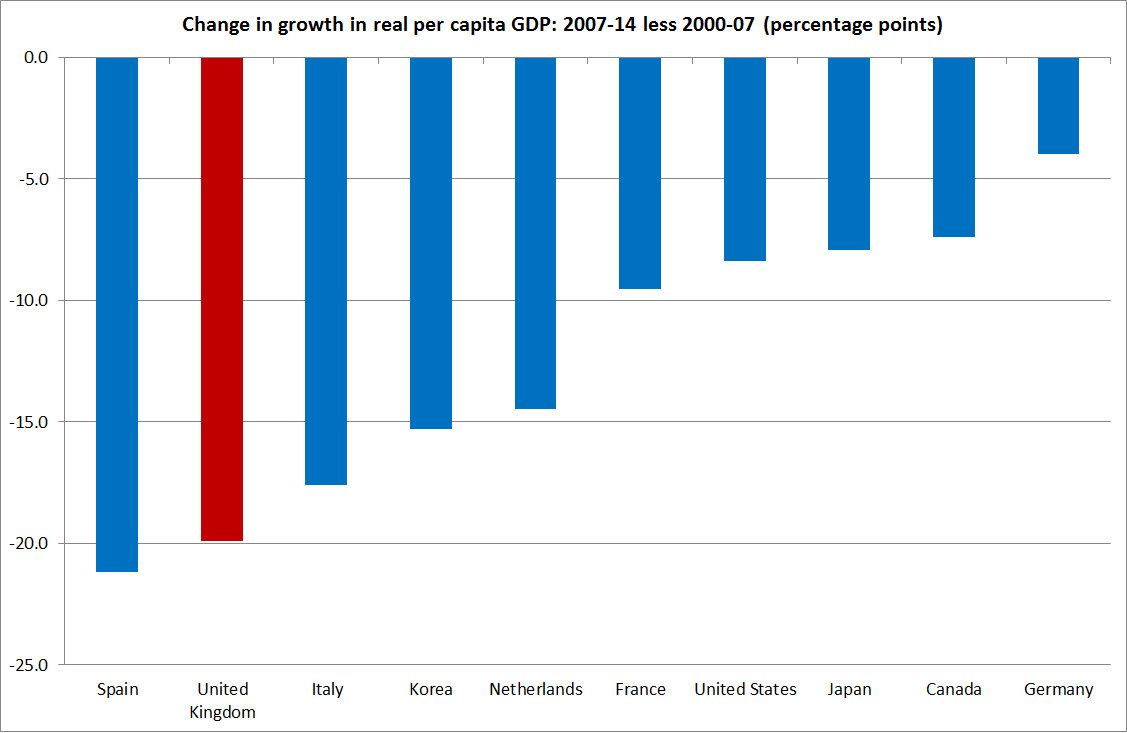

The second was the change in per capita growth, comparing 2007 to 2014 against the previous seven years, 2000 to 2007. As the UK had had the second fastest growth of this group of countries from 2000 to 2007, the slowdown subsequently was huge – almost as bad as that in Spain. The IMF reckons that the UK had (just) the largest output gap of any of these countries in 2007. One might be a little sceptical of that – more pressure on resources than in Spain? – but the differences aren’t going to redeem the UK picture.

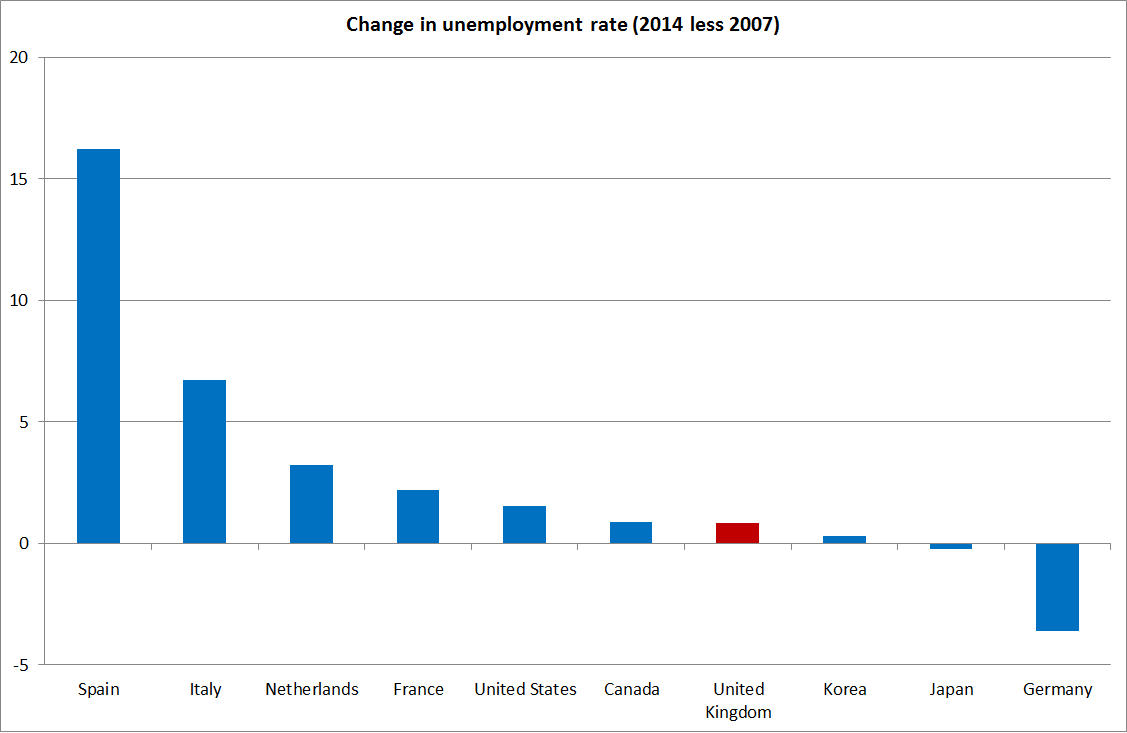

Unemployment rates in 2014 were higher than those in 2007 in eight of these ten countries. Here the UK scores relatively well, with an increase less than one percentage point.

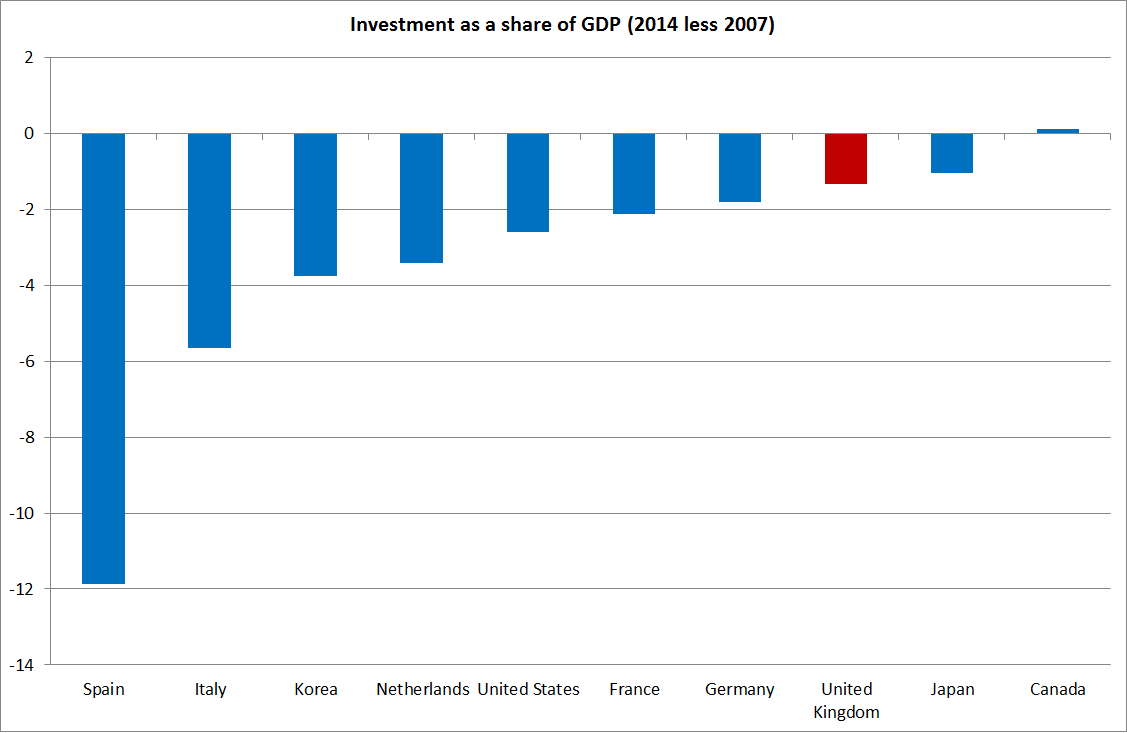

Investment as a share of GDP differs widely across countries, but in all but one of our countries, the investment share was lower in 2014 than in 2007. The UK doesn’t do too badly on this measure either.

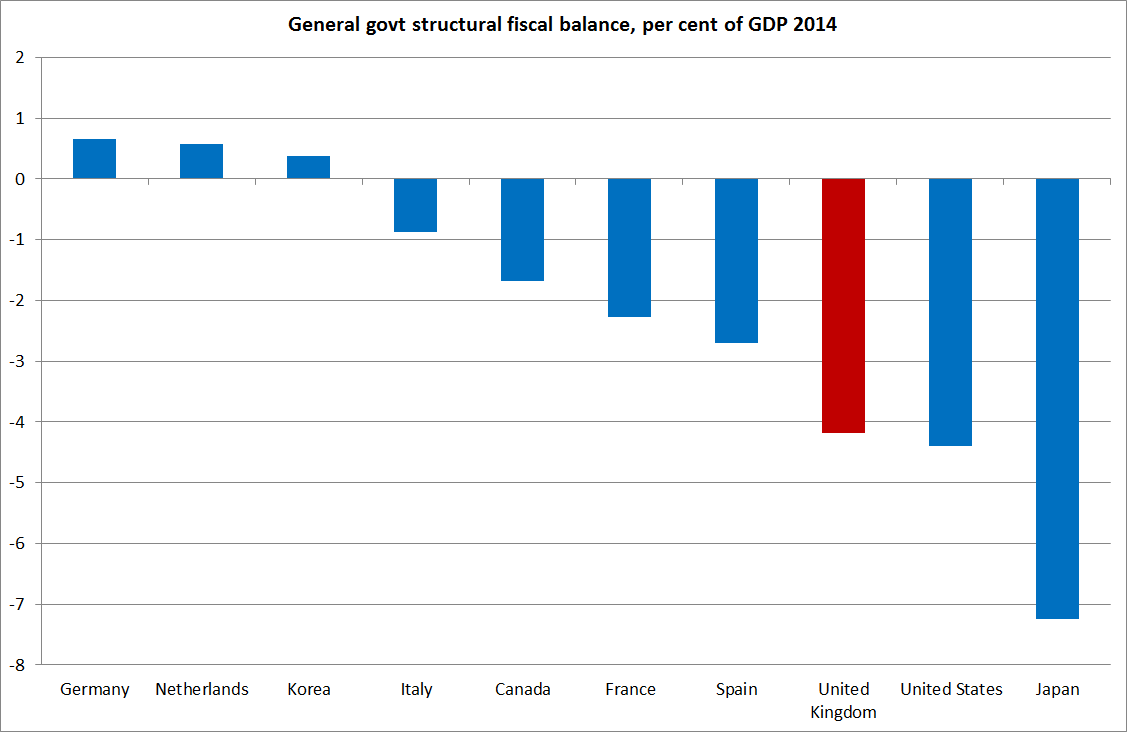

Much of the political-economic debate around the UK in recent years seems to have been around fiscal “austerity”. The IMF estimates that the UK’s structural fiscal deficit, as a share of GDP, was a bit smaller than it had been in 2007. But…..the imbalance in the UK’s fiscal accounts, on this measure, last year was still third largest of these 10 countries.

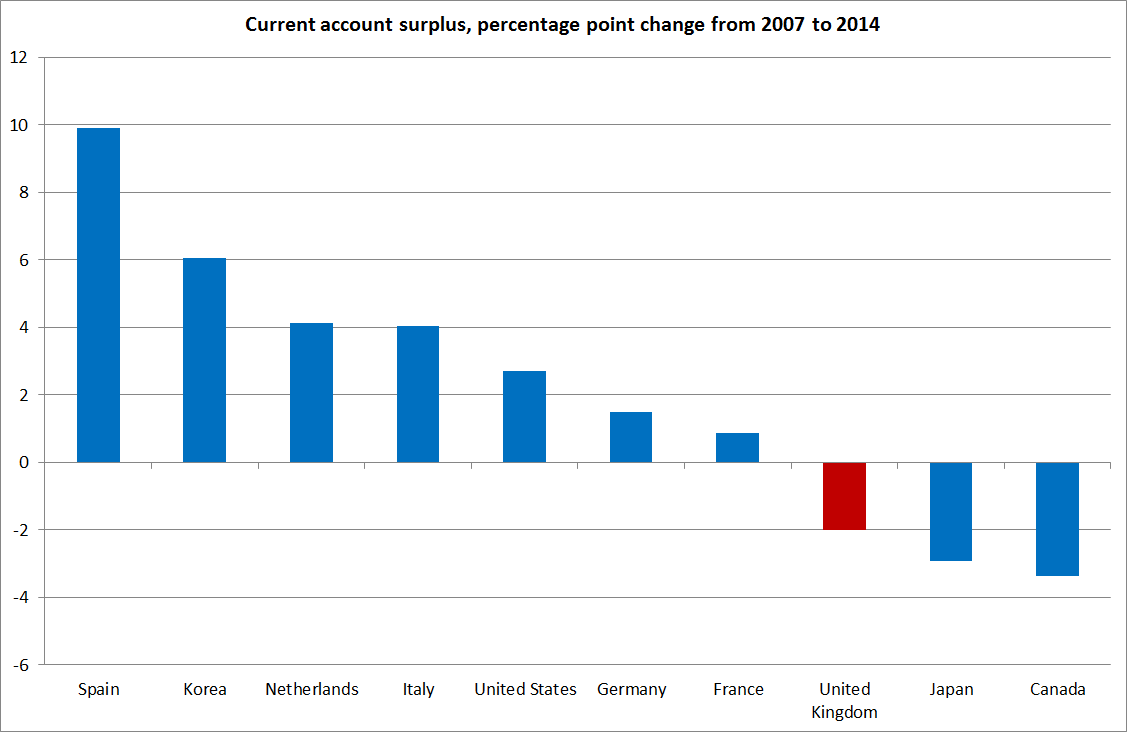

And finally, the current account balance. At 4.8 per cent of GDP, the UK had the largest current account deficit of any of these countries. If we look at the change in the current account balance from 2007 to 2014, the UK has had the third largest reduction in the current account surplus (or increase in the deficit). There is no simple way to interpret whether this is a good or bad thing, but I imagine the UK authorities would be feeling a touch nervous if the deficit were to get much larger than it is now.

So what to make of Lord Lawson’s story? The advanced world has done very badly since 2007, and that UK hasn’t been exempt. It is by no means the worst of this group of countries, but I probably wouldn’t score it as even second best either. But then the UK had a pretty stellar couple of decades prior to the recession.

If the IMF is to be believed, there is still a lot of fiscal adjustment to do at some point. When it might be prudent to do that is not going to be an easy call for the reappointed Chancellor, with a increasingly fragile eurogroup just across the Channel.