Paul Glass, of Devon Funds, had an article in the Herald yesterday, containing his agenda for action for New Zealand economic policymakers. I was sympathetic to quite a bit of his analysis, but this section caught my eye:

It’s a technical area, but the amount of regulatory capital held against residential mortgages should be increased substantially, not just tinkered with around the edges as is currently happening. This would limit the amount of debt available for mortgages.

It is a common view, but I think it is wrong. I’m not sure what reasoning Glass has behind his recommendation, but Gareth Morgan has argued along similar lines for years. Morgan argues that the bank regulatory capital regime (whether Basle I, II, or III) artificially favours lending secured on housing, because the risk weights used in calculating the amount of capital that needs to held in respect of such loans are less than those used in many other types of commercial bank assets.

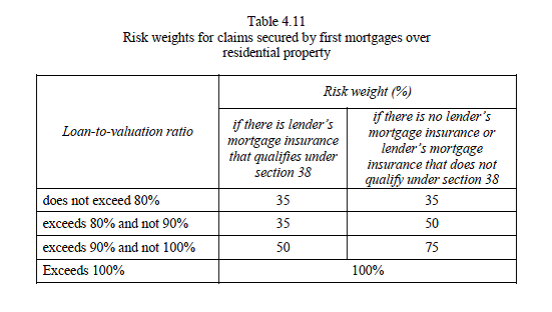

Calculation of risk weights for banks using internal ratings based model (the big 4 banks) is far from transparent, but the easiest way to see the difference is in the rules for other (“standardised”) banks. Risk weights for residential mortgages are as follows:

For loans with an LVR of less than 80 per cent, the risk weight is 35 per cent

By contrast, exposures to unrated corporate borrowers generally have a risk weight of 100 per cent.

But that is because the risks to banks from typical housing loans have been found to be less than those on many other bank assets. This is not just an observation about boom times, or about New Zealand and Australia in recent decades, it is a result across many countries and many different circumstances. Housing mortgages initiated by banks themselves, not under regulatory mandates to take on dubious risks, have rarely if ever played a major role in financial crises. A recent Reserve Bank Bulletin reported on some of the international literature in this area. A good example was Finland in the 1990s, where after a major credit boom and rapid growth in asset prices in the late 1980s, house prices fell by about 50 per cent in nominal terms, real GDP fell away sharply and unemployment rose substantially. Banks took losses on their mortgage portfolios, but those losses were modest and not remotely enough to have threatened the health of banks. The experience in the US since 2007 superficially looks like a counter-example, but binding federal government and congressional mandates played a key role in driving down the quality of new mortgage originations (and hence driving up subsequent loan losses).

It is not surprising that housing loan portfolios are not overly risky. Lenders have a lot at stake, but they also have solid collateral. Borrowers also have a lot at stake, especially in countries (like New Zealand and Australia with with-recourse mortgages). You can escape your debts if you go bankrupt but fortunately (in my view) we don’t have a culture that is overly welcoming to bankruptcy. And a owner-occupied home is not just a roof over the head, it is often also about a place in a community – the local school, or sports club, or church. So most residential mortgage borrowers do everything they can to avoid defaulting on their mortgage, and losing their house, even in very tough times. There will always be a minority of bad borrowers, and other people who are just overwhelmed by events and the size of a shock. Recent loans tend to be riskier than older loans – most of us probably borrowed about as much as we could afford to get into a first house, but mortgage portfolios age and typically get safer as they do. And it portfolios of loans – not individual loans – that need to be evaluated in thinking about the risk to banks.

By contrast, the typical unrated business loans will have no collateral, revenue streams that depend quite strongly on the economic cycle (profits are more volatile than wages) and limited liability. The nature of business is taking risk, and sometimes risks pay off and other times they go spectacularly wrong. Empirical evidence is that a portfolio of unrated business loans is materially risker than a portfolio of unrated residential mortgages. To be more specific, even in respect of property-based exposures, the evidence is that commercial property, and especially property development exposures, are far riskier (and more likely to lead threaten the health of banks and the financial system) than residential loan books. Markets will, and regulators should, reflect that in their expectations around capital.

Actual risk-weighting for our big banks is more sophisticated than this description and, as mentioned, much less transparent. Reasonable people can differ on whether anything is gained by having the IRB approach, or whether it would be better to simply use the standardised approach for all our banks – all of which are relatively simple.

But not only is there good reason for residential mortgage risk weights to be lower than those on many/most commercial exposures, but New Zealand’s risk weights on residential loans are high by international standards. This IMF piece, done a couple of years ago, contrasted effective risk weights on residential mortgages with those then in the UK, Australia and Canada

Sweden recently raised the minimum risk weights used by their banks on residential mortgages. As part of the preparation for that move they produced this document, which includes this chart. Again New Zealand risk weights on residential mortgage loans are higher than any of the banks in this chart – and are higher than the newly increased Swedish risk weights.

Residential risk weights, or overall required capital ratios, might still in some sense be too low in New Zealand. But the onus should be on those calling for such increases to make the case that the threat to financial stability is greater than what is already allowed for in the bank capital framework. The Reserve Bank did stress tests last year looking at the impact of a really quite severe adverse shock, in which nominal house prices fell a long way and unemployment rose substantially (it usually takes both to cause real trouble). Not one of the banks, let alone the system as a whole, had its capital materially impaired in that scenario. Those tests may well have been flawed, they may have missed something important, and they certainly won’t have captured everything that mattered, but on the information we have actually available the New Zealand banking system currently looks pretty well-placed to cope with a severe shock affecting the residential mortgage book. With the stock of credit growing at only around 5 per cent per annum, that also should not be a great surprise.

And since housing seems to be one of those areas where to cast doubt on one possible explanation/solution is to risk being accused of thinking there is no issue or problem at all, I refer anyone inclined to react that way back to my take on housing.