Paul Glass, of Devon Funds, had an article in the Herald yesterday, containing his agenda for action for New Zealand economic policymakers. I was sympathetic to quite a bit of his analysis, but this section caught my eye:

It’s a technical area, but the amount of regulatory capital held against residential mortgages should be increased substantially, not just tinkered with around the edges as is currently happening. This would limit the amount of debt available for mortgages.

It is a common view, but I think it is wrong. I’m not sure what reasoning Glass has behind his recommendation, but Gareth Morgan has argued along similar lines for years. Morgan argues that the bank regulatory capital regime (whether Basle I, II, or III) artificially favours lending secured on housing, because the risk weights used in calculating the amount of capital that needs to held in respect of such loans are less than those used in many other types of commercial bank assets.

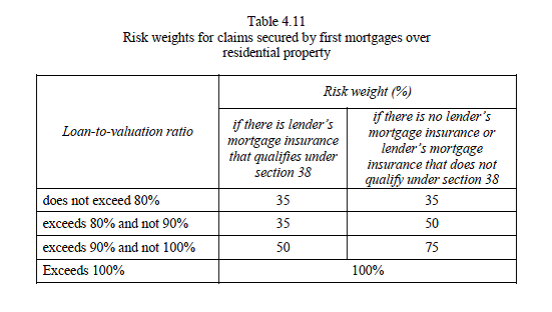

Calculation of risk weights for banks using internal ratings based model (the big 4 banks) is far from transparent, but the easiest way to see the difference is in the rules for other (“standardised”) banks. Risk weights for residential mortgages are as follows:

For loans with an LVR of less than 80 per cent, the risk weight is 35 per cent

By contrast, exposures to unrated corporate borrowers generally have a risk weight of 100 per cent.

But that is because the risks to banks from typical housing loans have been found to be less than those on many other bank assets. This is not just an observation about boom times, or about New Zealand and Australia in recent decades, it is a result across many countries and many different circumstances. Housing mortgages initiated by banks themselves, not under regulatory mandates to take on dubious risks, have rarely if ever played a major role in financial crises. A recent Reserve Bank Bulletin reported on some of the international literature in this area. A good example was Finland in the 1990s, where after a major credit boom and rapid growth in asset prices in the late 1980s, house prices fell by about 50 per cent in nominal terms, real GDP fell away sharply and unemployment rose substantially. Banks took losses on their mortgage portfolios, but those losses were modest and not remotely enough to have threatened the health of banks. The experience in the US since 2007 superficially looks like a counter-example, but binding federal government and congressional mandates played a key role in driving down the quality of new mortgage originations (and hence driving up subsequent loan losses).

It is not surprising that housing loan portfolios are not overly risky. Lenders have a lot at stake, but they also have solid collateral. Borrowers also have a lot at stake, especially in countries (like New Zealand and Australia with with-recourse mortgages). You can escape your debts if you go bankrupt but fortunately (in my view) we don’t have a culture that is overly welcoming to bankruptcy. And a owner-occupied home is not just a roof over the head, it is often also about a place in a community – the local school, or sports club, or church. So most residential mortgage borrowers do everything they can to avoid defaulting on their mortgage, and losing their house, even in very tough times. There will always be a minority of bad borrowers, and other people who are just overwhelmed by events and the size of a shock. Recent loans tend to be riskier than older loans – most of us probably borrowed about as much as we could afford to get into a first house, but mortgage portfolios age and typically get safer as they do. And it portfolios of loans – not individual loans – that need to be evaluated in thinking about the risk to banks.

By contrast, the typical unrated business loans will have no collateral, revenue streams that depend quite strongly on the economic cycle (profits are more volatile than wages) and limited liability. The nature of business is taking risk, and sometimes risks pay off and other times they go spectacularly wrong. Empirical evidence is that a portfolio of unrated business loans is materially risker than a portfolio of unrated residential mortgages. To be more specific, even in respect of property-based exposures, the evidence is that commercial property, and especially property development exposures, are far riskier (and more likely to lead threaten the health of banks and the financial system) than residential loan books. Markets will, and regulators should, reflect that in their expectations around capital.

Actual risk-weighting for our big banks is more sophisticated than this description and, as mentioned, much less transparent. Reasonable people can differ on whether anything is gained by having the IRB approach, or whether it would be better to simply use the standardised approach for all our banks – all of which are relatively simple.

But not only is there good reason for residential mortgage risk weights to be lower than those on many/most commercial exposures, but New Zealand’s risk weights on residential loans are high by international standards. This IMF piece, done a couple of years ago, contrasted effective risk weights on residential mortgages with those then in the UK, Australia and Canada

Sweden recently raised the minimum risk weights used by their banks on residential mortgages. As part of the preparation for that move they produced this document, which includes this chart. Again New Zealand risk weights on residential mortgage loans are higher than any of the banks in this chart – and are higher than the newly increased Swedish risk weights.

Residential risk weights, or overall required capital ratios, might still in some sense be too low in New Zealand. But the onus should be on those calling for such increases to make the case that the threat to financial stability is greater than what is already allowed for in the bank capital framework. The Reserve Bank did stress tests last year looking at the impact of a really quite severe adverse shock, in which nominal house prices fell a long way and unemployment rose substantially (it usually takes both to cause real trouble). Not one of the banks, let alone the system as a whole, had its capital materially impaired in that scenario. Those tests may well have been flawed, they may have missed something important, and they certainly won’t have captured everything that mattered, but on the information we have actually available the New Zealand banking system currently looks pretty well-placed to cope with a severe shock affecting the residential mortgage book. With the stock of credit growing at only around 5 per cent per annum, that also should not be a great surprise.

And since housing seems to be one of those areas where to cast doubt on one possible explanation/solution is to risk being accused of thinking there is no issue or problem at all, I refer anyone inclined to react that way back to my take on housing.

Michael, I think this is a very interesting topic that needs further discussion. It is relevant not only for the current frenzied debate about housing but also for firms’ access to finance and overall efficiency of our credit creation system. I found this recent paper interesting: http://www.nber.org/papers/w1054.pdf (Jorda, Schularick and Taylor ).

LikeLike

Thanks. I find anything by those guys well worth reading.

LikeLike

All very well if you live in an alter reality, one where banks are regulated( haha), where the big banksters take risks(haha) where the US was not bankrupt in 1933.

Housing loans: big profits and no risk( as the big bankster just do whatever they like with their books, create money from nowhere and self audit) .

“During the past two centuries when the peoples of the world were gradually winning their political freedom from the dynastic monarchies, the major banking families of Europe and America were actually reversing the trend by setting up new dynasties of political control through the formation of international financial combines. These banking dynasties had learned that all governments must have sources of revenue from which to borrow in times of emergency. They had also learned that by providing such funds from their own private resources, they could make both kings and democratic leaders tremendously subservient to their will.”

Carroll Quigley in his book “Tragedy and Hope”

“There is a special breed of international financiers whose success typically is built upon certain character traits. Those include cold objectivity, immunity to patriotism, and indifference to the human condition. That profile is the basis for proposing a theoretical strategy, called the Rothschild Formula, which motivates such men to propel governments into war for the profits they yield… As long as the mechanism of central banking exists, it will be to such men an irresistible temptation to convert debt into perpetual war and war into perpetual debt.”

G. Edward Griffin in his book “The Creature from Jekyll Island”

“By the end of the 1890’s [J.P.] Morgan and [John D.] Rockefeller had become the giants of an increasingly powerful Money Trust controlling American industry and government policy… Some 60 families – names like Rockefeller, Morgan, Dodge, Mellon, Pratt, Harkness, Whitney, Duke, Harriman, Carnegie, Vanderbilt, DuPont, Guggenheim, Astor, Lehman, Warburg, Taft, Huntington, Baruch and Rosenwald formed a close network of plutocratic wealth that manipulated, bribed, and bullied its way to control the destiny of the United States. At the dawn of the 20th Century, some sixty ultra-rich families, through dynastic intermarriage and corporate, interconnected shareholdings, had gained control of American industry and banking institutions.”

F. William Engdahl in his book “Gods of Money: Wall Street and the Death of the American Century”

“The House of Morgan financed half the US [World War II] war effort. Morgan had also financed the British Boer War in South Africa and the Franco-Prussian War.”

Dean Henderson in his book “Big Oil & Their Bankers in the Persian Gulf”

“In the latter half of the 1800s European financiers were in favor of an American Civil War that would return the United States to its colonial status.

The Civil War, lasted from 1861 until 1865 … during which, Congress also set up a national bank, putting the government into partnership with the banking interests, guaranteeing their profits.”

Andrew Gavin Marshall, Global Research

“International bankers make money by extending credit to governments. The greater the debt of the political state, the larger the interest returned to lenders. The national banks of Europe are also owned and controlled by private interests. We recognize in a hazy sort of way that the Rothschilds and the Warburgs of Europe and the houses of JP Morgan, Kuhn Loeb & Co., Schff, Lehman and Rockefeller possess and control vast wealth. How they acquire this vast financial power and employ it is a mystery to most of us.”

Senator Barry M. Goldwater in his memoirs “With No Apologies”

“The substantive financial powers of the world were in the hands of investment bankers (also called “international” or “merchant” bankers) who remained largely behind the scenes in their own unincorporated private banks. These formed a system of international cooperation and national dominance which was more private, more powerful, and more secret than that of their agents in the central banks. This dominance of investment bankers was based on their control over the flows of credit and investment funds in their own countries and throughout the world. They could dominate the financial and industrial systems of their own countries by their influence over the flow of current funds through bank loans, the discount rate, and the re-discounting of commercial debts; they could dominate governments by their control over current government loans and the play of the international exchanges. Almost all of this power was exercised by the personal influence and prestige of men who had demonstrated their ability in the past to bring off successful financial coupes to keep their word, to remain cool in a crisis, and to share their winning opportunities with their associates. In this system the Rothschilds had been preeminent during much of the nineteenth century, but, at the end of that century, they were being replaced by J. P. Morgan whose central office was in New York, although it was always operated as if it were in London.”

Carroll Quigley, in his book “Tragedy and Hope”

“The Depression [1929] was not accidental. It was a carefully contrived occurrence. The international bankers sought to bring about a condition of despair here [United States] so that they might emerge as rulers of us all.”

Louis T. McFadden, Chairman of the U.S. House of Representatives’ Banking and Currency Committee, 1932

“Our global banking system is a global cartel, a “super-entity” in which the world’s major banks all own each other and own the controlling shares in the world’s largest multinational corporations.

… This is the real “free market,” a highly profitable global banking cartel, functioning as a worldwide financial Mafia.”

Andrew Gavin Marshall

“John D. Rockefeller J. P. Morgan, and other kingpins of the Money Trust were powerful monopolists. A monopolist seeks to eliminate competition. In fact, Rockefeller once said: “Competition is a sin.” These men were not free enterprise advocates.”

James Perloff in his book “The Shadows of Power: The Council on Foreign Relations and the American Decline”

“In 1899, J. Pierpont Morgan and Anthony Drexel went to England to attend the International Bankers Convention. When they returned, J.P. Morgan had been appointed head representative of the Rothschild interests in the United States.

As the result of the London Conference, J.P. Morgan and Company of New York, Drexel and Company of Philadelphia, Grenfell and Company of London, Morgan Harjes Cie of Paris, M.M. Warburg Company of Germany and America, and the House of Rothschild, were all affiliated.”

William Guy Carr in his book “Pawns In The Game”

“The European Bankers favor the end of slavery… the European Plan is that capital money lenders shall control labor by controlling wages. The great debt that capitalists will see is made out of the war and must be used to control the valve of money. To accomplish this government bonds must be used as a banking basis. We are now awaiting Secretary of Treasury Salmon Chase to make that recommendation. It will not allow Greenbacks to circulate as money as we cannot control that. We control bonds and through them banking issues.”

European bankers “Hazard Circular”, 1962 – from Dean Henderson’s book “Big Oil & Their Bankers In The Persian Gulf”

“The bankers control the world’s major corporations, media, intelligence agencies, think tanks, foundations and universities.”

Henry Makow

“The structure of financial controls created by the tycoons of ‘Big Banking’ and ‘Big Business’ was of extraordinary complexity, one business fief being built on another, both being allied with semi-independent associates, the whole rearing upward into two pinnacles of economic and political power, of which one, centered in New York, was headed by J. P. Morgan and Company and the other, in Ohio, was headed by the Rockefeller family. When the two cooperated, as they generally did, they could influence the economic life of the country to a large degree and could almost control its political life, at least at the Federal level. They caused the “panic of 1907″ and the collapse of two railroads, one in 1914 and the other in 1929.”

Carroll Quigley in his book “Tragedy and Hope”

“The reason why the British abolished the right of the American Colonies to create and issue their own money is simple: the bankers did not want the Colonists to be able to trade among themselves without paying tribute to them… The objective was clear: by forcing Americans to pay interest, the European money changers wanted to enslave the Colonies in a mountain of debt.

… We are paying the International Bankers hundreds of millions of dollars each year in interest on our National Debt. This money (or credit) was created by the bankers out of nothing – and loaned to us at a high rate of interest.”

Des Griffin in his book “Fourth Reich of the Rich

“Hundreds of years ago, bankers began to specialize, with the richer and more influential ones associated increasingly with foreign trade and foreign-exchange transactions. Since these were richer and more cosmopolitan and increasingly concerned with questions of political significance, such as stability and debasement of currencies, war and peace, dynastic marriages, and worldwide trading monopolies, they became the financiers and financial advisers of governments.

Moreover, since their relationships with governments were always in monetary terms and not real terms, and since they were always obsessed with the stability of monetary exchanges between one country’s money and another, they used their power and influence to do two things: (1) to get all money and debts expressed in terms of a strictly limited commodity-ultimately gold; and (2) to get all monetary matters out of the control of governments and political authority, on the ground that they would be handled better by private banking interests.”

Carroll Quigley, in his book “Tragedy and Hope”

“In the Bolshevik Revolution we have some of the world’s richest and most powerful men financing a movement which claims its very existence is based on the concept of stripping of their wealth, men like the Rothschids, Rockefellers, Schiffs, Warburgs, Morgans, Harrimans, and Milners. But obviously these men have no fear of international Communism. It is only logical to assume that if they financed it and do not fear it, it must be because they control it.”

Gary Allen in his book “None Dare Call It Conspiracy”

“We shall have World Government, whether or not we like it. The only question is whether World Government will be achieved by conquest or consent.”

international banker James Warburg testifying before the United States Senate on Feb. 7, 1950

LikeLike

Some strong arguments here, but I’m not completely convinced that variable risk weighted assets are the way to go. Risk weightings are subject to interpretation and can be and are gamed to some extents. Second, the weights are set on the basis of historic data which can be a poor guide to historic events – especially when the data itself adds a positive feedback loop (by encouraging higher leverage late in long booms, and by encouraging investors to take on more debt). Finally, we can question the efficiency of regulators imposing these weightings on banks, who have better knowledge.

Regarding the overall level of bank capital (ordinary equity), it is welcome to see this has improved. However it remains low relative to historic norms. Further, I understand that there remains an element of implicit subsidy in the form of assuming government assistance (from memory, credit ratings are a notch higher across the Board). We know that financial crises can lead to huge output and employment losses (as in the US) or very negative consequences if the sovereign feels compelled to take on the obligations of private sector banks (as it did in Ireland). My preference is that the chance of this happening should be reduced as close to zero as possible (i.e. less than once per 70 years).

My personal view is that bank equity requirements can be increased gradually without harm to the economy or the banks themselves – although ROEs may fall, the banks become lower beta stocks and will be able to borrow at lower risk premiums (and/or the implied government subsidy disappears). I don’t accept the argument that business or residential lending will be curtailed – these are profitable lines, and the banks will raise more equity to fund them if required. Some marginal in-house trading activities might be constrained, without loss to the broader economy. But there would be benefits to the banks as well. With higher equity, they would not have to worry so much about the regulator second guessing their LVR policies.

LikeLike

Blair

Personally I would have considerable sympathy with moving back to the standardised model for risk-weighting, rather than relying on internal bank models with (not very transparent) regulatory overlays.

My bias would probably also be towards generally higher required bank capital ratios, and I agree that it would be unlikely to be costly to the economy if that happened (Admati et al), but…..I’m less sure than I used to be that historical norms are that enlightening. It isn’t that banks are smarter, just that books stuffed full of conventional residential mortgages, diversified across a whole country, are much less risky than many of the things banks might have had on their books 100 years or more ago. The current regulatory minima are already calibrated to supposedly allow crises much less frequently than one in 70 years – and perhaps reflecting that NZ either hasn’t had a systemic crisis since the 1890s or if you want to count the late 1980s one can put that down to a deregulatory transition and the dominant role of a govt owned bank

I’d be wary of the idea that financial crises are hugely economically costly. Recall that NZ didn’t have a crisis in 2008/09 and yet our economy has performed no better than the US’s since 2007. Crises are very disruptive at the time, and can be fiscally costly as you say, but needn’t have long term large real costs

Oh, on capital requirements you might have a look at this piece, which was the Bank’s regulatory impact statement for Basle III. It is only as good as the assumption that went into it, but it makes a reasonable case for current levels being enough. http://www.rbnz.govt.nz/regulation_and_supervision/banks/policy/4932427.pdf

Michael

LikeLike

[…] that has encouraged many to put more weight on stress tests in recent years. But in any case recall that New Zealand banks have high capital ratios by international standards, and that is so even […]

LikeLike