Last week I illustrated how much higher our long-term interest rates have been (and are) than those in other advanced countries, and set out my argument that investor concerns about the large New Zealand negative NIIP position (loosely, “the large external debt”) don’t look to have been the culprit.

In this post, I’m going to show another couple of charts, and then briefly respond to a commenter’s question.

One possible reason why New Zealand’s interest rates might sensibly have been higher than those abroad would have been if New Zealand’s rate of productivity growth had been so strong that returns to large amounts of new investment in New Zealand were very high. Profitable business opportunities might have abounded, and businesses had been rushing to invest to take advantage of those opportunities, while households might have been rationally anticipating future much higher incomes.

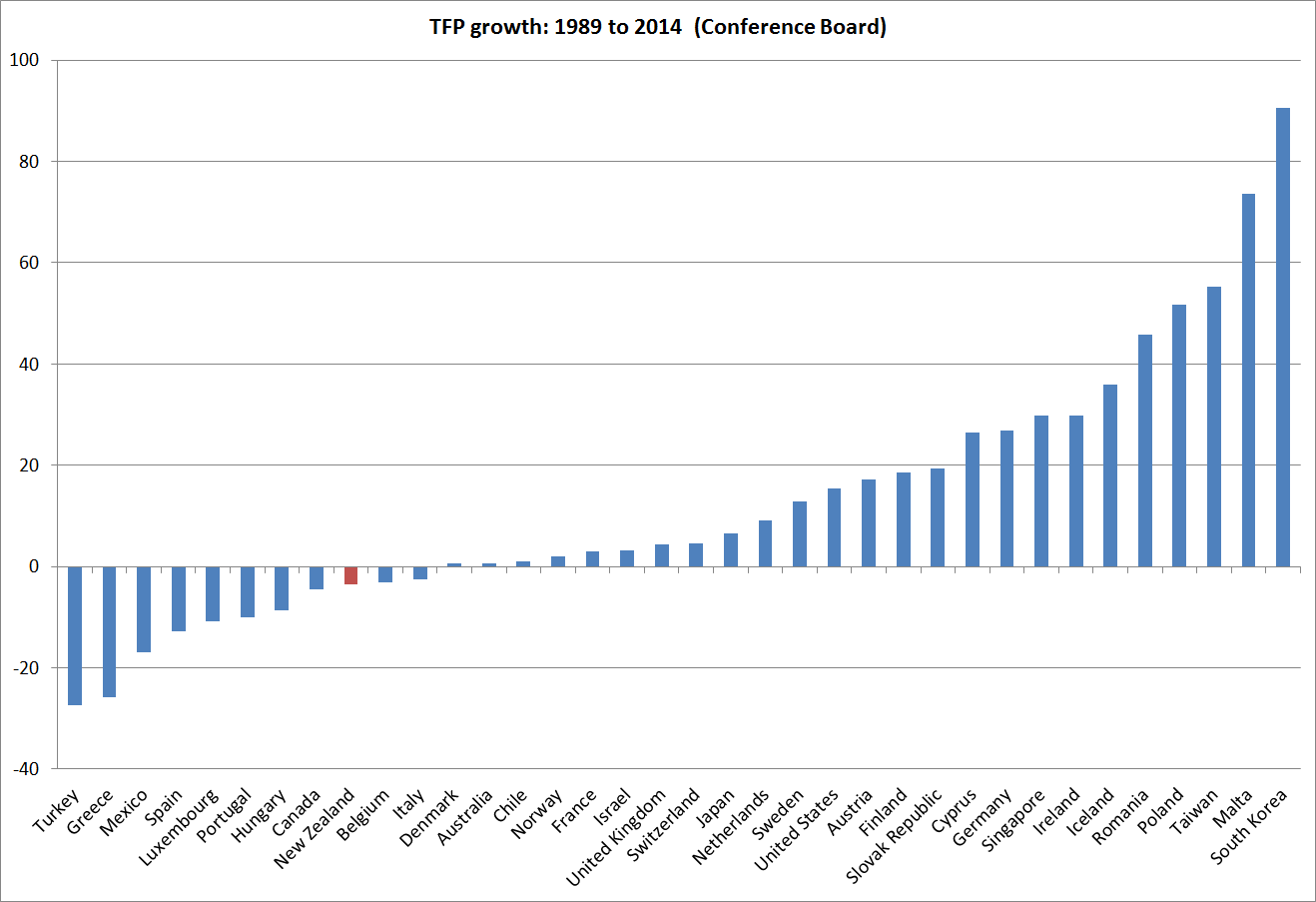

That doesn’t sound like New Zealand over the last 25 years. In fact, our rate of business investment (as a share of GDP) has been one of the lower among OECD countries. In recent days, I’ve shown a couple of charts drawn from the Conference Board’s TFP data. Here is another. For the advanced countries for which the Conference Board has estimates all the way back, it shows total estimated growth in TFP since 1989 (when the public data start). New Zealand hasn’t been the worst of these countries, but the record is pretty underwhelming. And Greece, Spain and Portugal each look a bit worse than they deserve because there is so much excess capacity in those economies right now.

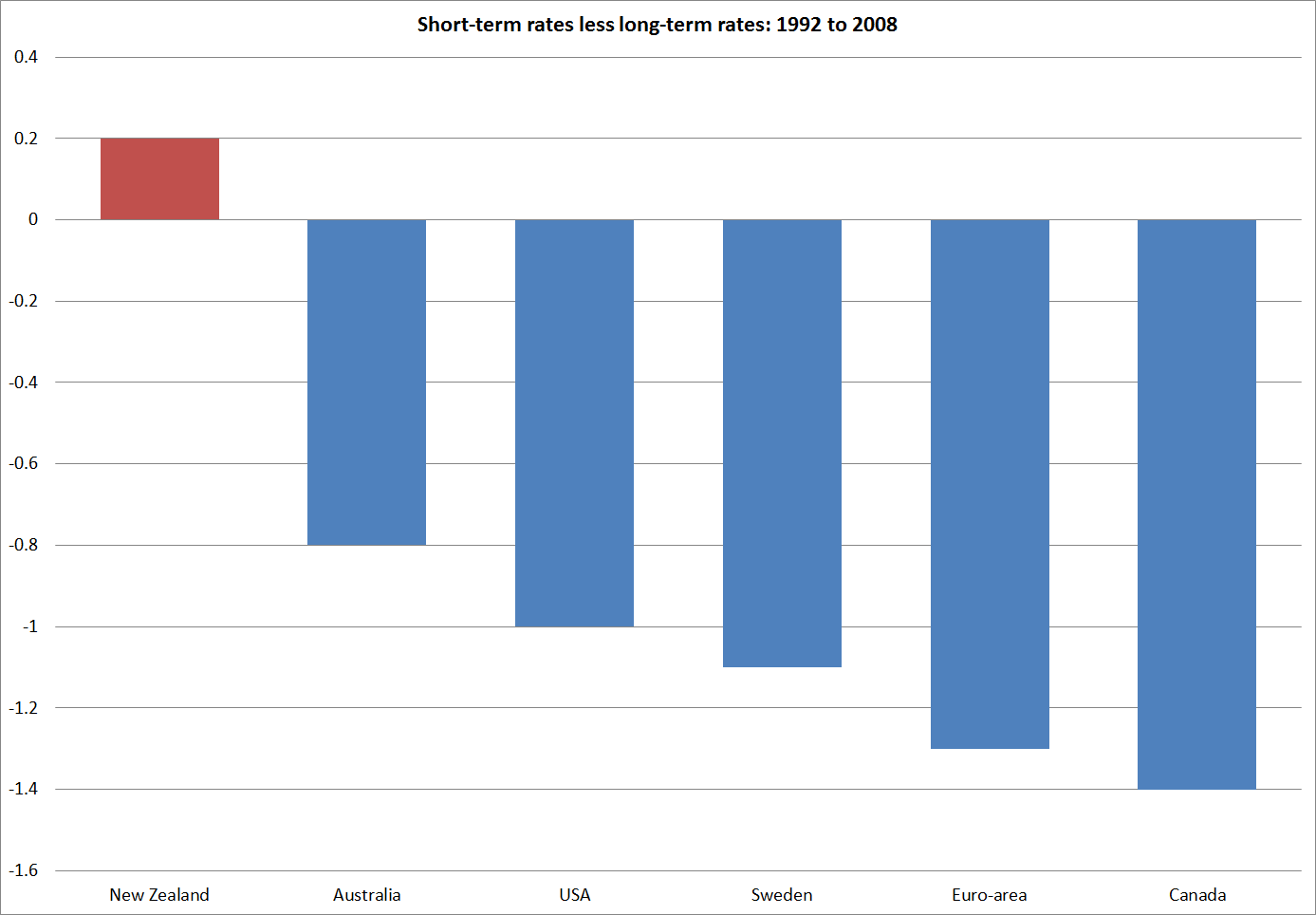

My other chart this morning is about the slope of the interest rate yield curve. Very broadly speaking, yield curves are generally upward sloping. That is, short-term interest rates tend to average a bit lower than long-term interest rates. But New Zealand has been different.

As I showed the other day, long-term interest rates in New Zealand have been higher than those in other advanced countries. But short-term interest rates have been even higher. That is what this chart captures. It uses OECD interest rate data, The data aren’t ideal: the long-term interest rates are government bond rates, and the short-term rates are those on private sector securities. But as that is so for each of the countries it shouldn’t materially complicate cross-country comparisons.

I’ve deliberately only drawn the chart to the end of 2008. Since the near-zero lower bound on short-term nominal interest rates became an issue for an increasing range of countries, looking at the slope of the yield curve has not had the same meaning (since short-term rates can’t be cut as low as they otherwise would).

Over that 17 year period – in which each country had several interest rate cycles – New Zealand stood out. If foreign investor concerns were at the heart of why interest rates were so high, long-term rates would be high relative to short-term rates (relative to what is seen in other countries). That is the situation in Greece now. But as the chart illustrates, in New Zealand it the other way round. Our short-term interest rates averaged much higher relative to long-term interest rates than was the case in the other countries shown. It suggests that we should be looking for things that drive short-term rates for our explanation as to why New Zealand interest rates have been persistently so high (again, relative to other countries’ rates). It also nicely illustrates my observation the other day that New Zealand interest rates have long been regarded as unsustainably high, and not just by government officials and other pointy-headed analysts. The slope of the yield curve is set in the market. Private investors have expected our short-term interest rates to fall relative to long-term interest rates (whereas in these other countries there was no such expectation). But those expectations have been wrong. Persistent surprises in how long our interest rates have stayed up relative to those abroad can help explain why the exchange rate has been so persistently strong. My former colleague, Anella Munro, covered some of this ground, in rather more technical terms, here.

And finally, some brief answers to a commenter’s question. On Friday a commenter asked:

Michael, your analysis seems to make sense – that it’s more pressure on resources than risk premium that explains persistently high NZD interest rates

But it also raises, for me, some further questions.My understanding is that when the NZ Government used to borrow in USD, back in the 1970s and 1980s,(when NZ was probably a worse credit risk than it is today), it did so at a rate only a small margin above the rate at which the US government borrowed. And I imagine that, today, NZ banks borrow USD at much the same rate as that at which US banks borrow. So if the only difference is in the currency of denomination (ie, the counterparties and the countries are the same) doesn’t that suggest that the explanation for the persistently high NZ interest rate has to have something to do with the currency?

Second, if there has been persistent pressure on resources, why would that not have been been closed by net imports?

Grateful for any responses you may be able to offer.

On the first question, yes New Zealand credits borrow internationally in USD at much the same interest rates as similarly-rated borrowers from other countries do. A AA-rated New Zealand bank is likely to pay much the same US interest rate on a bond issue as, say, a AA-rated Swedish bank might. That certainly helps make the point that, whatever, is accounting for the differences between, say, New Zealand dollar and Swedish krone interest rates it is not the credit quality of the borrowers. The credit ratings of our banks are as good as those anywhere.

But does that mean that it is all to do with the exchange rate? Well, yes and no. I would argue that it is the ability of the exchange rate to move that makes the material cross-country differences in interest rates possible[1]. Since expected risk-adjusted returns should be roughly equal across advanced countries, interest rates on New Zealand dollar assets can only be higher than those on assets denominated in another currency (for similar quality borrowes) for any length of time, if the New Zealand dollar is expected to depreciate against that currency over time. When the interest rate gap opens up, the New Zealand dollar tends to rise until it reaches a level that is not regarded as sustainable. At that point, the expected future deprecation more or less offsets the yield advantages. There is an alternative story, in which the NZD is such a volatile currency that we have to pay premium interest rates to attract the foreign capital we need. But again, if such premia exist, and are material, they should result in a surprisingly weak exchange rate. That hasn’t been the New Zealand story – indeed, the only sustained period of weakness in the New Zealand exchange rate was around the turn of the century when our policy rate was quite low relative to those abroad (our OCR briefly matched the Fed funds target rate in 2000). Such premia – whether to do with the NIIP or a volatile exchange rate – should tend to encourage resource-switching towards the tradables sector, in a (self-stabilising) manner that reduces future perceived vulnerability and any risk premia. I scarcely need to point out that we’ve seen nothing of that sort over 25 years.

And just briefly, the second question was whether, if there has been persistent pressure on resources, why that would not have been closed by (net) imports. The simple answer to that is because the economy can be thought of as made up of tradable bits and non-tradable bits. If everything in the economy were fully tradable, then any excess demand in New Zealand could be expected to be fully met through imports. Since tradables prices are set largely in world markets, there would be no sustained domestic pressures on the inflation rate (and no real need for a domestic monetary policy, or our own currency). Most of the interesting stuff arises from the fact that much of the economy is not freely tradable across borders, and tradables and non-tradables aren’t fully substitutable (I need a haircut, my mother needs rest-home care, and so on). So when we see persistent incipient excess demand pressures, some of the pressure shows up in the current account, and some in interest rates. As a result, despite a pretty strong government balance sheet, New Zealanders’ have run large current account deficits over the last 25 years, and we have had high interest rates relative to those in other advanced countries. Excess demand pressures, arising domestically, largely explain both phenomena.

[1] As I illustrated in one of my very early posts, back in the 1890s, when the New Zealand government was very heavily indebted, but the exchange rate was fixed, the gaps between New Zealand and UK government bond yields were much smaller than those in recent decades.

FWIW I think a lot of carry traders (who tend to be long NZD) are agnostic about the long term depreciation, but operate a stop loss strategy in order to minimise potential downside if and when that happens. But the persistent success of the carry trade in NZD for decades has been quite remarkable. A highly rated credit with a large positive carry is quite a rare thing.

LikeLike

Indeed. My point is not that each and every market participant expects a future deprecation, but the whole market – consciously or (often) unconsciously – behaves as if it does. If it were not so, we would not just see a high NZ TWI, but a super-high one (to get what would otherwise appear as a fairly free lunch off the table).

LikeLike

Thanks for those responses Michael.

Yes, the tradables/non-tradables point helps to explain why net imports do not completely ease the resource pressure.

But as Blair says, the success of the carry trade in NZD, for decades, is a truly remarkable thing. According to the theory it should not happen.

Is that where your thesis comes in? To check that I have understood your line of analysis correctly, are you saying that a combination of persistently strong population growth, in the face of persistently slow productivity growth, has resulted in persistent pressure on non-tradable resources, with monetary policy equally persistently having had to lean against those pressures to keep a lid on non-tradables inflation?

And being an economy that started from a position with a relatively high level of income, and in recent decades having performed reasonably enough not to have come to be regarded as ‘risky’ (if anything NZ may have come to be seen as ‘steady and dependable’), its a nexus that might be sustained for an unusually long time.

Is that a macro story that has a parallel with firms/individuals that ‘tread water’? The great majority do not end up at risk of bankruptcy; rather such firms mostly end up getting taken over, and individuals end up just less well off than they could have been – including as the result of the share of their income they pay away to the providers of the capital they use?

Have I understood your line of analysis correctly?

LikeLike

You are getting a bit ahead of me Bruce. My point is just one of repeated surprises – markets repeatedly surprised that our interest rates have stayed so high for so long (relative to other countries). Anella provides the formal model (but basically UIP_ under which that keeps the exchange rate surprisingly high for a long time. And the picture, in historical time, is muddied because actual interest rates (and the TWI) cycle around, and at any time no one is quite sure what is structural and what is cyclical.

LikeLike

Hi Michael:

Under a risk sharing lens high interest rates in NZ are not so puzzling, given that we are a small open economy. The recent work of Tarek Hassan, Hanno Lustig, and Adrian Verdelhan – who seem to be the bright young thinkers in international finance these days – does a good job of explaining why the carry trade persists.

Here’s something I copy-and-pasted:

Hassan proposes that is because bonds are essentially a form of insurance that is country specific. Bonds issued in the currencies of larger economies are comparatively expensive simply because they insure against shocks that affect a larger portion of the global economy.

If you buy a US dollar denominated bond, that’s insurance on the $17 trillion US economy. If you buy a bond denominated in Australian dollars, it’s insurance on that far smaller economy. However, if something goes wrong in a large economy like the United States or Japan, it’s far more likely to affect the rest of the world than a crisis in a country such as Australia or Egypt. As a result, the currencies of large economies tend to gain value when times are bad. Bonds issued in the currencies of larger countries are thus more expensive and hence offered at chronically lower interest rates. The onset of a currency union, moreover, lowers interest rates in participating countries, and stocks in the nontraded sector of larger economies pay lower expected returns.

Or see: Tarek Alexander Hassan, “Country Size, Currency Unions, and International Asset Returns,” Journal of Finance, December 2013.

Their arguments have little to do with net investment position. NZ will always be a risky investment for US based investors because it is small.

LikeLike

Thanks. I do recall some of these papers when they came out. I suppose my problem with them is that they predict that large countries will have lower interest rates than small ones, which doesn’t seem to be the case (at least not to any material extent), but also that they should result in relatively low exchange rates for the small countries (whose citizens face the high financing margins). That, of course, hasn’t been the NZ story. If one is looking for a persuasive narrative, I reckon it needs to be one which explains not just high int rates but also high exchange rates (and, to anticipate) weak productivity performance, all in the country with the rule of law and pretty good institutional quality.

LikeLike

Hi Michael:

Regarding country size: Sure there are a few outliers, like Switzerland and Denmark. But country size (in terms of GDP) is just a proxy for systemic risk of the country. Denmark is well-integrated into the EU, arguably so is the Swiss economy. At any rate, there is a negative correlation between country size (in terms of GDP) and interest rates in the float era.

Do these models predict low exchange rates? In some sense small country exchange rates have to be high in periods of global growth and low during periods of crisis. That swing from high to low compensates small country investors during global downturns. Note this is what we saw in 2008/2009 during the crisis. I guess you have a different yardstick in mind when you say small countries have high exchange rates.

At any rate: We know that the conventional exchange rate models perform abysmally. This new generation of theory does a lot better, solving some of the long-standing puzzles (e.g. forward premium puzzle). I think that is a reason to favour them, especially when the alternatives explain very little.

Regarding NZ’s poor productivity: The risk-sharing framework can tell you why lower productivity leads to higher interest rates, since lower productivity usually results in a shrinking share of world output. Of course that is not an explanation of NZ’s poor productivity performance – but it does at least provide the connection between interest rates and productivity you are looking for.

LikeLike

Hi Ryan

Sorry not to have responded sooner.

I guess my points are more macro, than finance, in nature. If (long-term) interest rates in a small country are typically higher, then the economics of producing in that country are less attractive. To some extent, that will have to be offset by a lower real exchange rate – and in a financial markets sense that effect is likely to arise because short-term rates will be set lower than otherwise, to partly offset the dampening impact on demand of the long-term rates.

I’m not convinced that conventional frameworks have done so badly re the exchange rate, and I think Anella Munro’s paper is significant in that regard.

On your final para, it is one possible connection, but…..recall that NZ’s total GDP growth has been quite rapid, because we have had rapid population growth. My argument is that the rapid population growth, in a context of lowish national savings, has driven up interest rates, driven up the real exchange, and skewed investment away from business investment, and within business investment has skewed it from tradables to non-tradables.

Michael

LikeLike

Hi Michael:

No need to apologize. I appreciate this discussion regardless of any time lag involved.

RE NZ GDP growth: It is relative growth that matters for the risk-sharing narrative. NZ’s share of world output has definitely decreased over time. NZ share of OECD output has also declined, even after accounting for new members. To undo the risk-sharing story you;d have to make the argument hat the NZ economy has become more systemic for global risk, thus mitigating the shrinking relative size of the economy. There could be a case for that, based on the fact that global investors cannot hedge against China, and therefore turn to its import partners (The AUD is sometimes discussed in those terms).

Regarding your migration-based narrative: You seem to be hinting at some form of misallocation there (e.g. “skewed”), but if low willingness-to-save is driving things, it seems difficult to conclude that we’d be better off under some counterfactual version of the NZ economy. Sure, we’d have higher output per person if we saved more, but those low savings rates are telling us that most kiwis don’t really want to defer consumption in order to reach that higher level of output.

LikeLike