I’ve been blogging about what has happened in advanced economies since 2007, with a particular focus on trying to shed a bit of light on New Zealand’s overall performance.

New Zealand’s overall performance has been mediocre at best. Of course, “mediocre” is better than we’ve done for much of the post-war period, but (a) it isn’t the impression some have had of New Zealand’s recent performance, and (b) there were reasons to think we should have done better.

Our terms of trade have been strong, we didn’t have a serious domestic financial crisis, and we neither hit the zero bound nor were under any great pressure to undertake fiscal consolidation. Add in a floating exchange rate to the mix, in a world in which fixed exchange rate countries have mostly struggled, and things looked propitious for New Zealand. On the other hand, the earthquakes required a major diversion of resources away from other activities – the repair work has been both quite low productivity in nature (which isn’t a criticism, just a description of the nature of many of the repairs) and as a major non-tradables shock it diverted resources from the tradables sector.

One factor people sometimes cite for New Zealand’s no-better-than-middling performance is the initial pressure on resources. The argument goes that the economy was stretched in, say, 2007, that inevitably growth in subsequent years would be slower. And there had been a perception – I contributed to it in one Reserve Bank article – that New Zealand had experienced more intense pressure on resources than many other advanced countries.

Absolutely, this story can’t account for much. Average annual growth rates since 2007 have been around 2 percentage points lower than they were in the decade or so previously. Most output gaps in advanced countries were around 2 to 3 per cent in total. So, yes, working off the excesses built up in the boom can explain some of the subsequent weaker growth but not much.

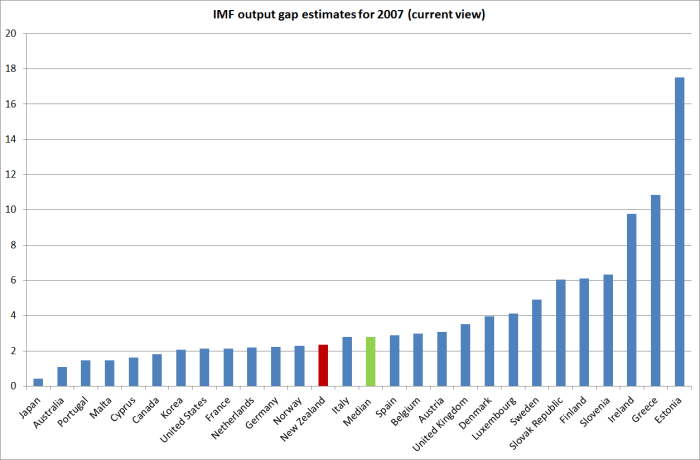

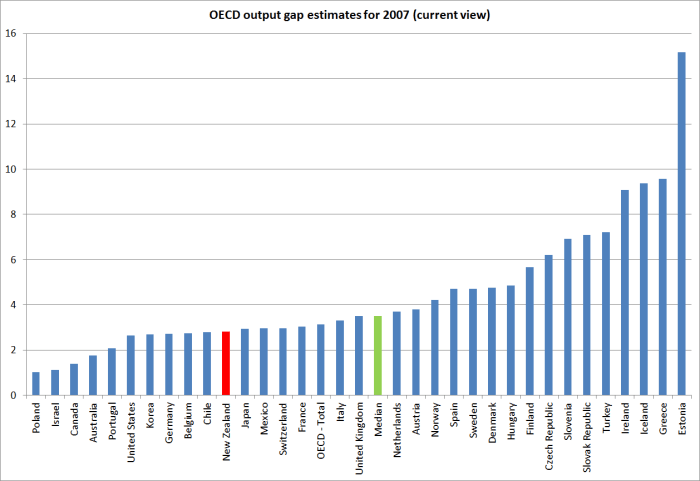

But, and more importantly, for my story, based on current international agency estimates New Zealand’s output gap prior to the recession wasn’t large by international standards. No one agency does output gap estimates for all my sample of advanced countries, and for some of the countries there are no IMF/OECD estimates at all. Since each agency uses different methodologies, estimates are comparable across countries and across time in an individual agency’s database, but we can’t simply combine the IMF and OECD estimates. I should also stress the word “current”. The next two charts are the respective 2015 estimates for output gaps in 2007 – ie with all the benefit of hindsight, and later vintages of data.

Here are the current IMF estimates for 2007. All these advanced economies are estimated to have had positive output gaps in 2007 – even Japan, which is consistent with the views BOJ officials were espousing back then, although not a view widely held in the rest of the West. The IMF estimates that New Zealand then had an output gap of around 2.4 per cent of GDP, just slightly below the median for this group of countries., and just slightly higher than that for the United States. I don’t know the details of some of the other countries, but the estimate for Spain does look surprisingly low.

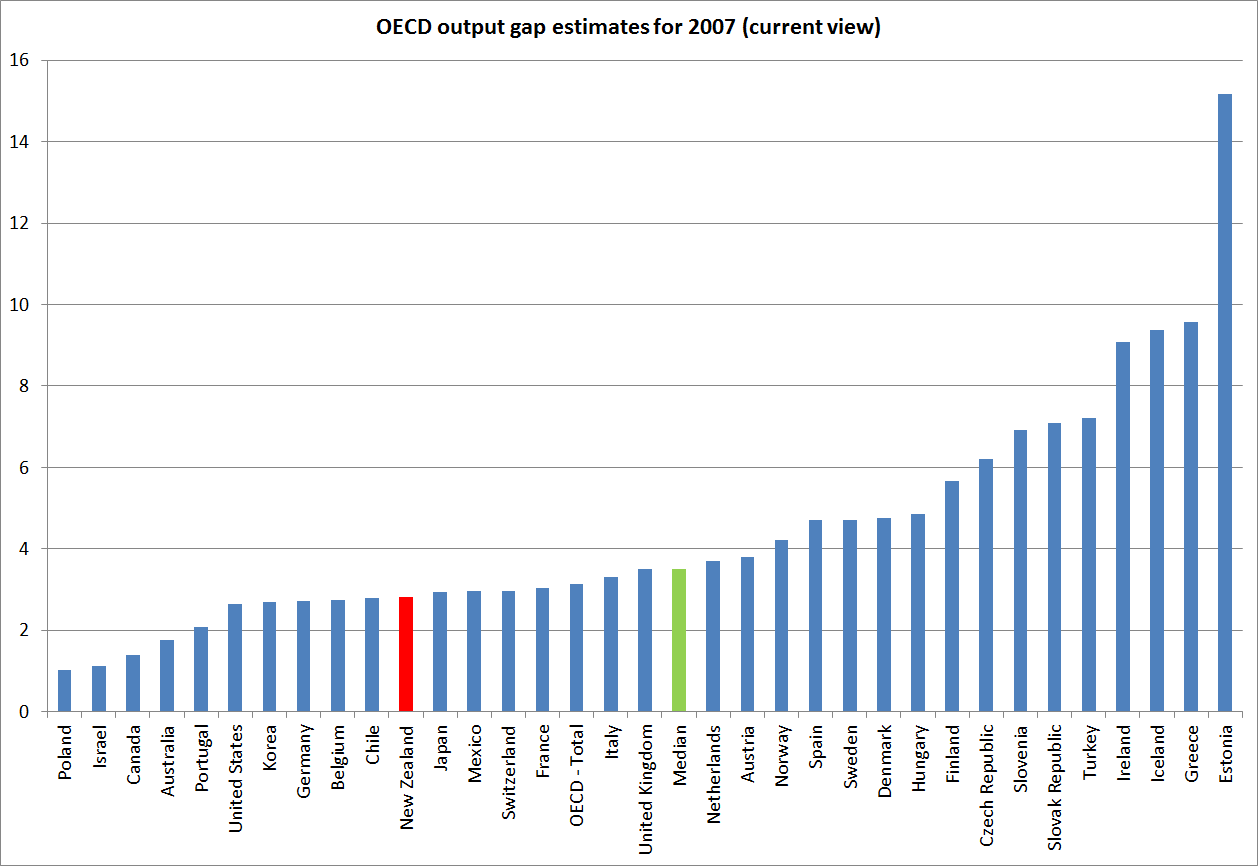

And here are the current OECD estimates for 2007 output gaps. They estimate that New Zealand had an output gap of around 2.8 per cent of GDP, not that far below the median, but only 10 OECD countries are estimated to have had smaller output gaps than New Zealand just prior to the recession. The Spanish estimate looks more sensible, and I’m not going to even try to make sense of what a 15 per cent output gap (in Estonia) even means.

So New Zealand is generally regarded as having had a materially positive output gap in 2007, but it was no higher (in fact, a little lower) than those of most other advanced economies for which we have current estimates. I’ve focused here on 2007, but the story is the same if one looks at 2006 or 2008 or the average of all three years. Extreme pressures on resources prior to the recession can’t explain our mediocre relative performance since 2007. Most countries had a little more excess to work off. If anything, since the agencies current think that New Zealand has little (or no) spare capacity left, unlike most other advanced countries, our relative performance since 2007 might overstate what proves to be sustainable.

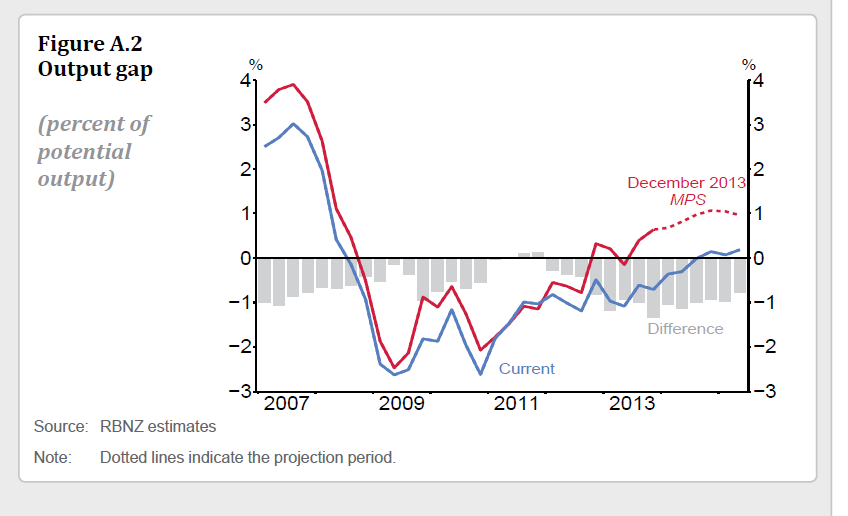

Incidentally, the current IMF and OECD estimates for New Zealand’s 2007 output gap are not so different from the Reserve Bank’s own latest estimates (around 3 per cent), in this chart from last week’s MPS.

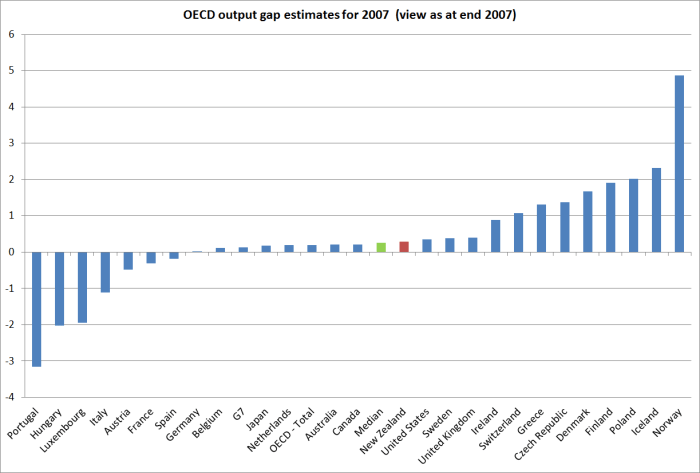

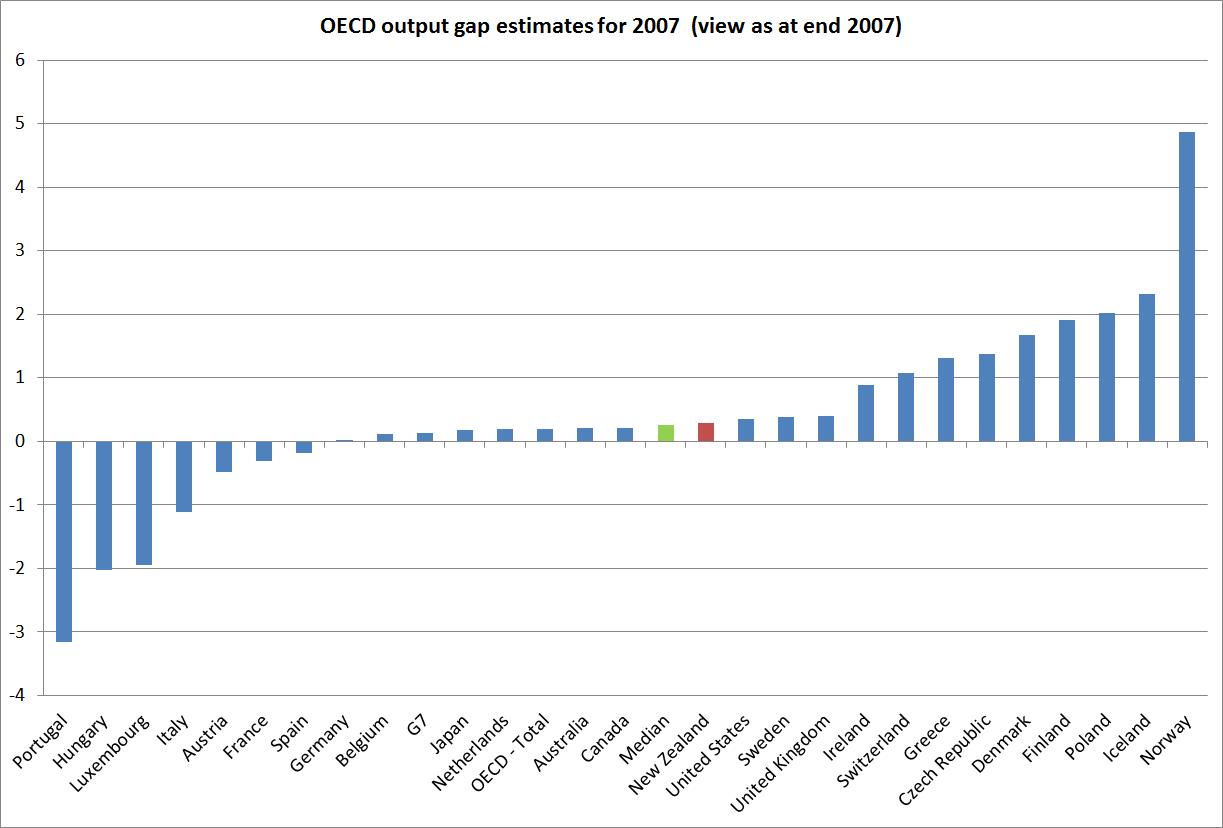

And one last chart, just to show how perceptions, and estimates, change. This is the chart of the OECD’s output gap estimates for 2007 published in December 2007 – before there was any widespread sense of a major recession looming. New Zealand was then estimated to be almost the median country, but notice how much lower the estimated output gap estimates all were. For many countries, including Spain incredibly, the output gaps were estimated to have been negative, and only a handful of countries were estimated to have had positive output gaps much above 1 per cent. This is not to pick on the OECD – my impression is that their estimates are no more variable than those of the IMF, or of our own Reserve Bank or Treasury. But it does make the point that if the output gap is a useful conceptual device, and is a useful summary metric for making sense of history, it is difficult to give it much reliable operational content in conducting policy. The unemployment rate will often provide a less murky read.