Today’s OCR decision was good news (and a pleasant surprise). The Reserve Bank has finally recognised just how persistently weak inflation pressures are in New Zealand and has cut the OCR. It has foreshadowed the possibility of one more cut. And at least for the next two years there is no hint of the OCR being raised back towards the unchanged estimate of the “neutral interest rate”.

There is likely to have been an element of deliberate smoothing of the numbers to produce such a flat track for two years ahead. If so that is something to be welcomed. I have two – slightly contradictory – reasons for welcoming it. First, no one (ever) has any good idea what the appropriate OCR will be two years hence. But, second, easing cycles (or tightening cycles) rarely stop at 50 basis points. In the 16 years of experience with the OCR, the only time the Reserve Bank has moved by only 50 points was when it prematurely raised the OCR in 2010, and then unwound those increases after the February 2011 earthquake. As I noted yesterday, if the Governor was going to cut the OCR he was most likely to back into modest cuts rather than embrace a wholesale change of view at this stage.

The document does not give a sense of a central bank with a very strong sense of what is going on. In a sense, that is a step forward. Huge uncertainty is something all central banks always face, and so many central banks have got things so far wrong over the years since the recession (repeatedly thinking that tightenings will soon be needed) that it is better to play things by ear, putting quite a lot of weight on actual developments in (core) inflation, rather than on stories about how future events might unfold.

I’m not going to comment in much detail on the numbers in the projections, but I did want to make a couple of points on them and then turn to slightly longer-term policy considerations.

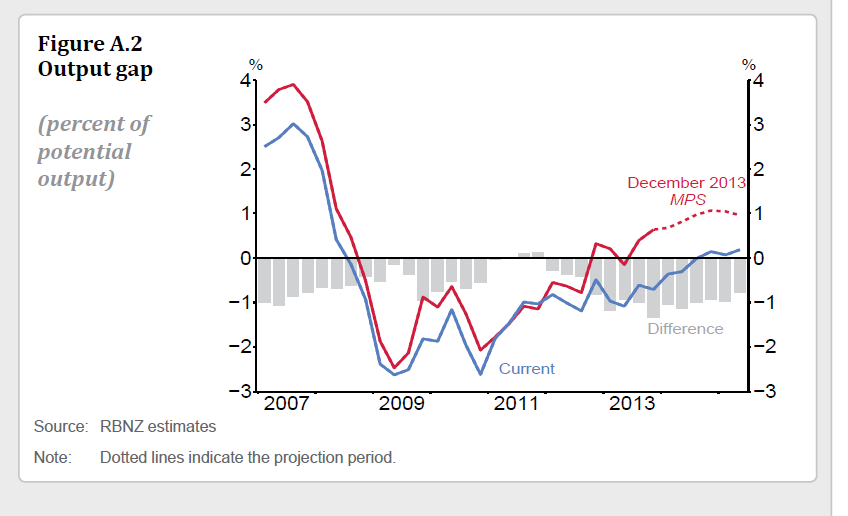

The first point was around this chart from the MPS, showing the Bank’s output gap estimates 18 months ago, and those now.

In one sense, the levels of the two estimates are not hugely different. And when we look back five years from now neither might closely resemble the best historical estimates. But the differences matter because the Bank, and its forecasting staff, have for several years been putting a lot of weight on the notion that excess capacity was exhausted (and hence it was “time to tighten”). But in this chart there is almost two years difference in the crossover point. Other indicators – notably the unemployment rate – cast doubt on whether the economy is even now operating at potential. The point is not that the previous precise estimates are wrong (that is inevitable), but that the Bank has been consistently wrong in its narrative about what has been going on.

The second was around the line, oft-repeated this morning, about the way the economy’s supply potential had expanded rapidly, enabling supply to accommodate growth in demand. It was presented as a good news story. But it just is not that good.

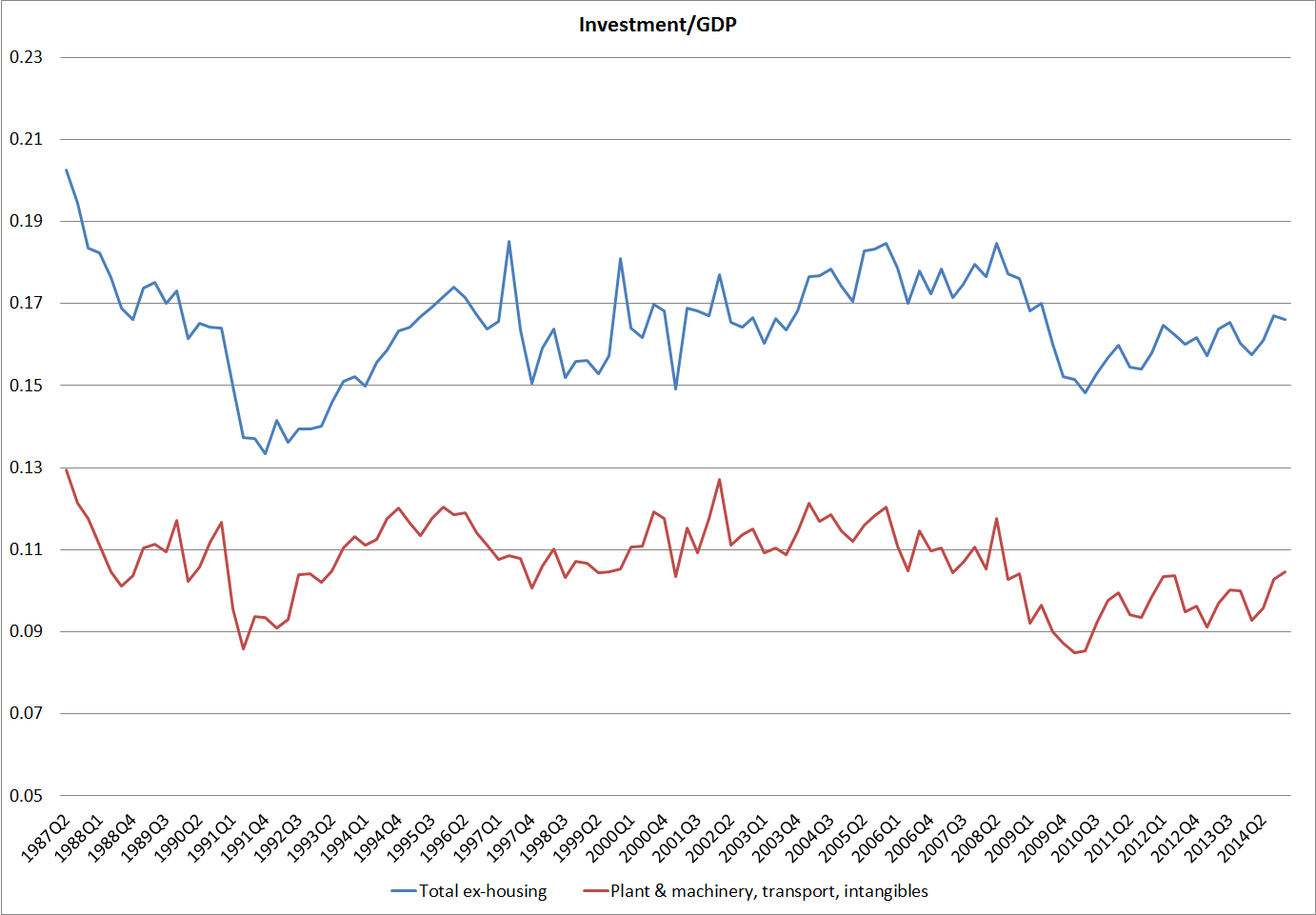

The labour supply has certainly increased rapidly, largely on the back of high (not record) net inward migration. But in the short-term increases in population growth boost demand more than they boost supply – always have done in New Zealand, and there is no sign of that changing. As the tables in the MPS remind us – and it is a point I’ve made here repeatedly – productivity growth has been lousy (on the Bank’s measure 0.7 per cent per annum). And even investment has just not been that strong. Here is a chart of investment/GDP .

I’ve shown both total investment ex housing, and investment in “plant and machinery, transport equipment, and intangibles”. Investment has been recovering, but on neither of these measures has investment as a share of GDP got back to the average levels seen in the decade prior to the recession, even though employment has been growing quite rapidly (lots of workers need equipping). And both measures (even though they exclude housing) will have been boosted by activity in Christchurch to replace lost capacity (think of that underground infrastructure work). There is no easy way to strip those Christchurch effects out, at least until we get the annual capital stock estimates, but there is really nothing to suggest that underlying growth in per capita capacity has been strong. A more likely story of what has gone on in New Zealand (as in many other countries) is just that there was quite a lot of excess capacity, which has been enough to accommodate even the demand pressures of a migration inflow without boosting inflation.

The press conference was striking for how little searching scrutiny there was of the Bank’s judgements and performance over the last year or two. Perhaps FEC will do better this afternoon? But Rob Hosking of NBR did ask whether the Bank had made a mistake in raising the OCR last year and holding it up for so long. “Not at all” was the Governor’s response. His argument was that no one 18 months ago could have anticipated the sharp fall in oil prices or the sharp fall in dairy prices (which, incidentally, are offsetting effects in the Bank’s forecasts). I’m not sure about “no one”, but even if we grant the point, the Governor is surely not arguing the continued weak core inflation, and declines in non-tradables inflation that we have already seen in the data, are a reflection of either of those forecast errors? Weak commodity prices are going to exert an increasing drag on spending this year, and perhaps beyond, but weak wage and price inflation were well-entrenched before the depth of the correction in dairy prices became fully apparent. I think it is more accurate to say that the Bank misjudged the level of spare capacity at the end of 2013, it misjudged the underlying inflation processes, it misjudged the inflation implications of the resurgence in the housing market, and thus was far too ready to initiate, and carry on, a tightening cycle. It was a mistake.

As I’ve said before, there is huge uncertainty in monetary policy. In a sense I can understand why the Governor would not want to openly acknowledge that he had made mistakes (he’s human too), but it is a shame that he did not use the opportunity to convey to journalists and the public more of a sense of the limitations of anyone’s knowledge, and the inevitability that central banks will from time to time get it wrong. And if the Governor did not want to acknowledge the mistake in the press conference, some more sustained critical self-examination in the Monetary Policy Statement itself would have been appropriate, and consistent with the spirit of the legislative provisions governing such documents. Perhaps a scenario experiment, running through the Bank’s models the implications of having held the OCR at 2.5 per cent since the start of last year, would have been an interesting basis for a conversation, including with the Bank’s Board (the Minister’s agent in holding the Governor to account).

But perhaps my biggest concern about today was an issue that won’t get any headlines. It was how the Governor and Assistant Governor dealt with a question about whether the inflation target should be changed. The Governor noted that outgoing IMF Chief Economist Olivier Blanchard had [been among various others who had] proposed raising inflation targets, to help minimise the risk that the near-zero lower bound would be such a problem in future. As the Governor noted, Blanchard [and one of his predecessors Ken Rogoff ] had not got a lot of support for his proposal. But then the Governor went on to note that monetary policy was proving a lot harder than people had expected and that it was very difficult to raise very low inflation expectations.

As I’ve noted previously, for other countries – already entrenched at zero interest rates – there is no easy way in which raising the inflation target now would make much difference. It is too late. But New Zealand (and Australia) are different. We still have materially positive policy interest rates. That means we are both still exposed to the possibility of hitting the zero lower bound in the next serious downturn. And yet the Governor seems indifferent to – or perhaps not even consciously aware of – the possibility, and the implications for the economy (and for the people who would be unemployed). Raising the inflation target is certainly not an ideal option, but as I’ve argued here previously unless governments and central banks are going to do something active about removing the near-zero lower bound (and neither the Governor nor the minister has given any hint of doing that) there should be a more serious discussion about whether our inflation target should be raised, as a pre-emptive and precautionary move. At very least, inflation outcomes in the upper half of the target range would provide slightly better buffers than a continuation of outcomes below the midpoint. There would be no excuse, given how much notice our central banks have had, if in the next serious downturn New Zealand or Australia become trapped for years with interest rates at some floor (a floor that arises out of policy and legislative choices, not as some force of nature). Perhaps, at a pinch, it was excusable not to think much about the zero bound when the Governor was signing the PTA in 2012. It can’t be excusable now.

The Assistant Governor’s response to the question about the target was even more disappointing. I suspect he was trying to help his boss, by asking the journalist whether he meant to suggest raising or lowering the inflation target. But it is difficult to believe that a serious senior central banker could, in the current climate of extremely low inflation (here and abroad), seven years on from a recession which took policy rates to their lower limit and has seen them more or less stuck there, could even toy publically with the idea of lowering the inflation target. If the Bank were to convincingly sort out the zero lower bound issues, then perhaps it would make sense to have that conversation (to aim for “true” price stability, rather than 2 per cent annual inflation). But the Bank has given no hint that it even takes these risks seriously.

McDermott concluded that “changing targets is a very risky thing to do”. Well, perhaps, but the risks in considering raising the target need to be weighed against the risks of adverse shocks that deliver New Zealand another recession before the unemployment rate has even fully recovered from the last recessions. Those are people’s lives the Bank toys with. As even the Governor recognised, the risks of something very nasty around a Greek exit from the euro are far from trivial – though how, in the same breath, he could assert that deflation risks had passed in Europe was something that eluded me.

And finally a reminder about the gaps in the Bank’s transparency around monetary policy:

- The forecasting models, developed at considerable public expense, are still not public

- We will not see, even with a lag, any minutes from the Governing Committee or the Monetary Policy Committee, and will see no hint of the advice provided to the Governor.

- Despite the Bank last week releasing 10 year old “forecast week” papers, we still have so sense as to how long a lag we might face before having access to the Bank’s forecasting papers for the last 18 months or so.

- We will not see any minutes of the Board discussion of monetary policy and the Bank’s adherence to the PTA. Nor we will see the written advice prepared for the Board.

As I’ve put it previously, the Bank is quite transparent about the things it (and we) don’t know much about – ie the future – and not very transparent at all about the things it knows a great deal about (its own analysis and deliberations and debates that went into shaping the Governor’s decisions, both today’s and those of the last 18 months).