Sometimes events determine what I write about. I had no intention of writing two posts today about Reserve Bank governance, but then I saw that Parliament had ratified the new Funding Agreement for the Reserve Bank. Since these things come round only every five years, and since the Funding Agreement is a material part of the Bank’s governance framework, today was the day to write about it.

Most government activities are funded, following each year’s Budget, by annual appropriations made by Parliament. Huge documents are published providing details of the plans the government is seeking appropriations for.

By contrast, historically most central banks were funded from their own resources, and legislatures had no real say in their spending. A statutory currency monopoly generates a lot of income, even in this era of lower interest rates and electronic payments. When the Reserve Bank was being reformed in the 1980s, everyone agreed that that model was inappropriate. Some parliamentary accountability/approval for the Bank’s spending was needed. But, equally, since the main point of the reforms was to provide operational independence for the Reserve Bank on monetary policy, no one really favoured a system of annual parliamentary appropriations for the Bank. The concern was that a Minister of Finance who wanted the Bank to run looser monetary policy could use the threat of a cut to the next year’s appropriation as behind-the-scenes leverage on the Governor. Such pressure might be particularly easy to exert since the Governor was both sole monetary policy decision-maker, and chief executive of the organisation.

The model that was settled on and passed by Parliament was a five-yearly Funding Agreement. Under this model, the Governor reaches an agreement with the Minister of Finance as to how much the Bank can spend in each of the next five years[1], and that agreement only becomes effective when it has been ratified by Parliament. In fact, it is not even obligatory to have a Funding Agreement – the Act says only that the Governor and Minister “may” reach an agreement, and if there is no agreement then, in principle, the Bank has no formal constraints on its spending.

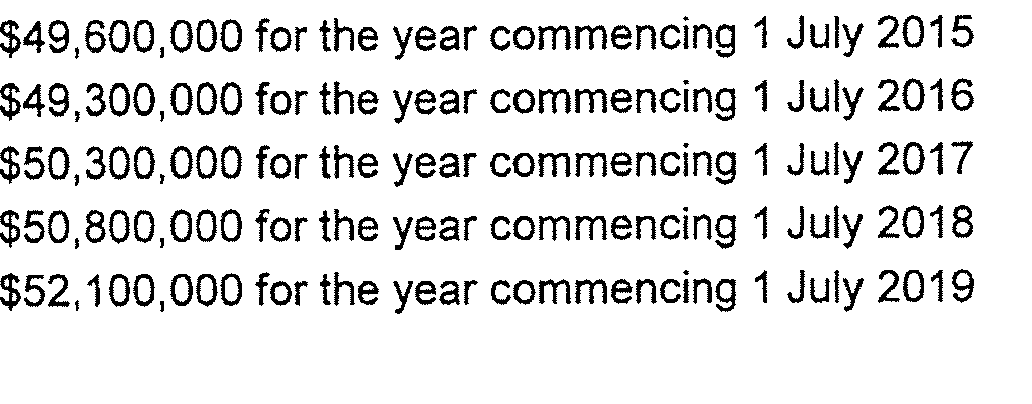

Parliament ratified the latest Funding Agreement last night, after a short debate (of which more below). The Bank and the Minister had agreed that the Bank will spend $49.6 million this coming year, rising by about 5 per cent in total over the following 4 years[2].

I don’t have any particular argument with the size of the Funding Agreement total, or the modest increase over the next few years (although it does seem to be a larger increase than many government departments, with flat baselines, have been experiencing). My concern is about process.

In particular, for one of the most powerful government agencies in New Zealand, the agreement contains almost none of the information people might reasonably need, whether as MPs or citizens, to know whether $49.6 million is the right amount. The entire document runs to just over two pages, but the meat of it is simply five lines

That is the same level of detail we get in the Estimates about the spending of the SIS – and at least Parliament (a) has to vote for the SIS’s spending, or the spending can’t happen, and (b) has to vote each and every year.

MPs were asked to vote on the Funding Agreement yesterday with no information about what the Bank and the Minister proposed that the Bank would do with the money. Presumably the Minister is aware of the Bank’s plans, but he now has no control over them beyond the top line number. In particular, the Bank has two quite distinct main statutory functions and it would be useful to know how the spending is split between monetary policy and financial stability. And within financial stability, how much is being spent on responsibilities under the Reserve Bank Act and how much on those under the Insurance (Prudential Supervision) Act? And how are those splits envisaged as changing over time?

There is nothing in the Act that requires funding agreements to be so abbreviated, and there is certainly nothing that would have stopped the Bank, the Minister, and Treasury releasing background papers to accompany the Funding Agreement, either before it was put to Parliament. That would have given MPs, and outside observers, the opportunity to scrutinise the plans for the Bank’s spending before the matter came to a vote in the House. Estimates hearings for other departments spring to mind.

The Funding Agreement system was a huge step forward when it was introduced in the 1989 Act. But it is really not good enough 25 years on. It could be made to work in much more open and transparent way without any legislative changes (as above).

But after 25 years, it is probably time for a re-think of the entire model. Why should the Reserve Bank be able to spend at all without parliamentary appropriation? Even if one doesn’t go that far, shouldn’t the (elected) Minister be responsible for telling the Bank how much it can spend, not reaching a (legally voluntary) agreement with the (appointed) Governor on the matter? The Governor can provide advice, and make a bid for spending (as all agencies around town do), but the Minister and Parliament should decide. Is there really any case for not making the Reserve Bank’s regulatory functions (at least) subject to an annual parliamentary appropriation? And if monetary policy decision-making responsibility were to move to a non-executive committee would there still really be a need for monetary policy to be funded five years at a time by Parliament[3]? I’m not sure how I’d answer that final question, but it should at least be asked.

The Funding Agreement model, as laid out in statute, and as it is worked in practice, is just another example of the gaps, the democratic deficits, in the governance model Parliament has put (left) in place for the Reserve Bank. The onus for change is with the Minister and with Parliament.

And just briefly on the parliamentary debate itself, which you can read here. It wasn’t Parliament at its finest, but then what could MPs do with so little information? Perhaps even with more information it would still have been an opportunity for hammering hobbyhorse issues? But what if there had been an estimates hearing first?

In addition to the Associate Minister, four MPs spoke:

- Grant Robertson seemed to be suggesting that the Bank needed more resources because the government had abdicated policy around the housing boom to the Bank. More seriously, he argued that the Bank “should be funded for a comprehensive overview of monetary policy and of the policy targets agreement”, arguing (and this is the first time I have heard him speak on the PTA) that New Zealand needs “the kind of policy targets agreement that would enable monetary policy that actually supports the exporters of New Zealand.”

- Russel Norman spoke, almost entirely about the housing market and financial stability.

- For New Zealand First Fletcher Tabuteau spoke. He took the opportunity to advocate significant change in the Reserve Bank, including the change in objectives proposed in private members bills in the previous Parliament by Winston Peters. Somewhat gratifyingly (I think) he quoted me, and the article last weekend on my governance ideas, noting that I considered the current Reserve Bank governance model “outdated, risky, and out of step internationally”.

- David Seymour (ACT) also spoke. It was a curious speech, perhaps intended primarily as a rebuttal of the previous speaker. He claimed that the Bank of Canada is modelled on the Reserve Bank of New Zealand (which is simply wrong), and appeared to blame the US housing bust on multiple objectives of the Federal Reserve (not a view that would be very widely shared).

But what else could they talk about when they have no more information about planned expenditure than is provided about the SIS?

[1] This is an approximation, both because the Bank can dip into capital (so the agreement does not formally cap the Bank’s spending even on the areas it covers) but also because various aspects of the Bank’s activities are not covered by the headline Funding Agreement total.

[2] Note that in the previous Funding Agreement the Bank had approval to spend $56.4 million in 2014/15.

[3] And actually one problem with the Funding Agreement model has been the difficulty of envisaging what spending will be required five years hence (in both real and nominal terms). No corporate board signs off on budgets five years ahead.