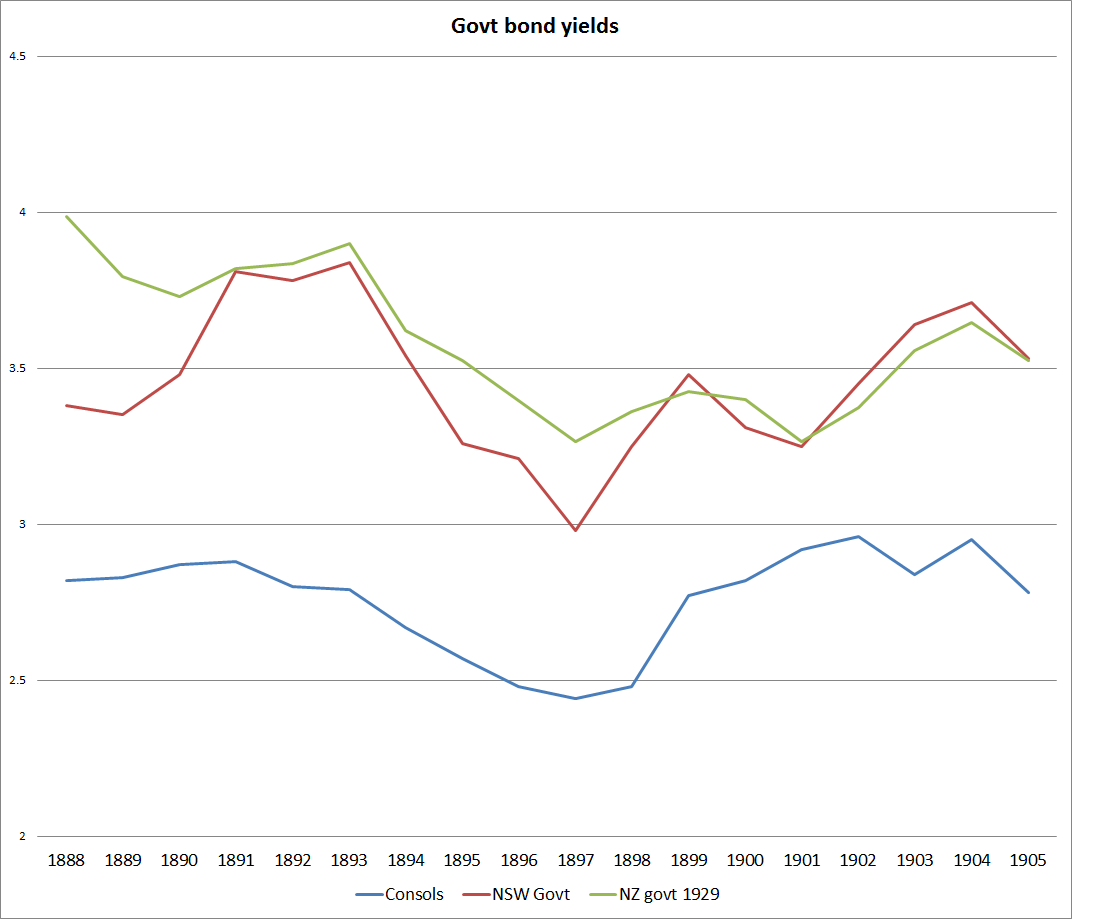

A conversation yesterday about markets in the 1890s prompted me to dig out some data on government bond yields in the period. The chart below shows a not-entirely-consistent (different maturity dates, period averages vs ends of periods) selection of data on bond yields for the UK, New Zealand, and New South Wales (Australia not existing as a political entity until 1901). There are spreads between these yields, but recall that they were, on the one hand, the securities of the most powerful country (and a major net lender) and those of two small highly-indebted colonies. The Australian colonies and NZ both went through episodes of financial crisis in the early 1890s (with severe and long-lasting effects in Australia’s case), and that presumably accounts for the spreads in the chart below widening temporarily in the early 1890s.

Rather more recent yield differentials will feature in a post probably next week (school holiday obligations permitting).

{kind=link}

[…] but the exchange rate was fixed, the gaps between New Zealand and UK government bond yields were much smaller than those in recent […]

LikeLike

[…] for New Zealand, at the turn of the 20th century our government long-term bonds (30 years) were yielding about 3.5 per cent, in an era when there was […]

LikeLike