Way back in 1990 Parliament formally handed over the general responsibility for implementing monetary policy to the Reserve Bank. The government has always had the lead in setting the objectives the Bank is required to work to, and has the power to hire and fire if the Bank doesn’t do its job adequately, but a great deal of discretion has rested with the Bank. With power is supposed to come responsibility, transparency, and accountability.

And every so often in the intervening period there have been reviews. The Bank has itself done several over the years, looking (roughly speaking) at each past business cycle and, distinctly, what role monetary policy has played. These have generally been published as articles in the Bank’s Bulletin. When I looked back, I even found Adrian Orr’s name on one of the policy review articles and mine on another. It was a good initiative by the Bank, intended as some mix of contribution to debate, offering insights that were useful to the Bank itself, and defensive cover (there has rarely been a time over those decades when some controversy or other has not swirled around the Bank and monetary policy).

There have also been a couple of (broader-ranging) independent reviews. Both had some partisan intent, but one was a more serious effort than the other. When the Labour-led government took office in 1999 they had promised an independent review, partly in reaction to their sense that we had messed up over the previous few years. A leading Swedish academic economist Lars Svensson, who had written quite a bit about inflation targeting, was commissioned to do the review (you can read the report here). And towards the end of that government’s term – monetary policy (and the exchange rate) again being in the spotlight – Parliament’s Finance and Expenditure Committee did a review.

When the monetary policy provisions of the Reserve Bank Act were overhauled a few years ago this requirement was added

It made sense to separate out this provision explicitly from that for Monetary Policy Statements (in fact, I recall arguing for such an amendment years ago) but the clause has an odd feature: MPSs (and the conduct of monetary policy itself) are the responsibility of the MPC, but these five-yearly longer-term reviews are the responsibility of “the Bank”. In the Act, the Bank’s Board is responsible for evaluating the performance of both management and the MPC, but the emphasis here does not seem to be on the Board. It seems pretty clear that this is management’s document, and of course management (mainly the Governor) dominates the MPC. Since the Board has no expertise whatever in monetary policy, it is pretty clear that the first of these reports, released last week, really was, in effect, the Governor reporting on himself.

And although plenty of people have made scathing comments about that, there isn’t anything necessarily wrong about a report of that sort. After all, it isn’t uncommon (although I always thought it odious and unfair given the evident power imbalance) for managers to ask staff to write about notes on their own performance, as part of an annual performance appraisal, before the manager adds his/her perspective. The insights an employee can offer about his or her own performance can often be quite revealing. And it isn’t as if the Bank’s own take on its performance is ever going to be the only relevant perspective (although, of course, the Governor has far more resources and information at his disposal than anyone else is going to have). The only real question is how good a job the Bank has done of its self-review and what we learn from the documents.

On which note, I remain rather sceptical about the case (National in particular is making) for an independent review specifically on the recent conduct of monetary policy. Some of those advocating such an inquiry come across as if what they have in mind is something more akin to a final court verdict on the Bank’s handling of affairs – one decisive report that resolve all the points of contention. That sort of finality is hardly ever on offer – scholars are still debating aspects of the handling of the Great Depression – and if there was ever a time when choice of reviewer would largely determine the broad thrust of the review’s conclusions this would be among them. Anyone (or group) with the expertise to do a serious review will already have put their views on record – not necessarily about the RBNZ specifically (if they were an overseas hire) but about the handling of the last few years by central banks generally. There is precedent: the Svensson review (mentioned above) was a serious effort, but the key decision was made right at the start when Michael Cullen agreed to appoint someone who was generally sympathetic to the RB rather than some other people, some of equal eminence if different backgrounds, who were less so. It would be no different this time around (with the best will in the world all round). A review might throw up a few useful points and suggestions, and would probably do no harm, but at this point the idea is mostly a substantive distraction. Conclusions about the Reserve Bank and about its stewardship are now more a matter for New Zealand expert observers and the New Zealand political process (ideally the two might engage). Ideally, we might see some New Zealand economics academics weighing in, although in matters macroeconomics most are notable mainly by their absence from the public square.

That is a somewhat longwinded introduction to some thoughts about the report the Bank came out with last week (120 pages of it, plus some comments from their overseas reviewers, and a couple of other background staff papers).

I didn’t think the report presented the Bank in a very good light at all. And that isn’t because they concluded that monetary policy could/should (they alternate between the two) have been tightened earlier. That took no insight whatever, when your primary target is keeping inflation near the middle of the target range and actual core inflation ends up miles outside the range. Blind Freddy could recognise that monetary policy should have been tightened earlier. When humans make decisions, mistakes will happen.

The rest of the conclusions of the report were mostly almost equally obvious and/or banal (eg several along the lines of “we should understand the economy better” Really?). And, of course, we had the Minister of Finance – not exactly a disinterested party – spinning the report as follows: “It is really important to note that the report does indicate that they got the big decisions right”. It should take no more than two seconds thought to realise that that is simply not true: were it so we would not now have core inflation so far outside the target range and (as the report itself does note) pretty widespread public doubts about how quickly inflation will be got down again. It would be much closer to the truth to say that the Reserve Bank – and, no doubt, many of their peers abroad – got most of the big decisions wrong. It has, after all, been the worst miss in the 32 years our Reserve Bank has been independent, and across many countries probably the worst miss in the modern era of operationally independent central banks (in most countries, after all, monetary policy in the great inflation of the 1970s was presided over by Ministers of Finance not central banks).

But there is no sense in the report at all of the scale of the mistake, no sense of contrition, and – perhaps most importantly in my view – no insight as to why those mistakes were made, and not even any sign of any curiosity about the issue. The focus is almost entirely defensive, and shows no sense of any self-critical reflection. There are no fresh analytical insights and (again) not even any effort to frame the questions that might in time lead to those insights. And no doubt that is just the way the Governor (who has repeatedly told us he had ‘no regrets’) would have liked it. And here we are reminded that this is very much the Orr Reserve Bank: the two senior managers most responsible for the review (the chief economist and his boss, the deputy chief executive responsible for monetary policy and macroeconomics) only joined the Bank this year, and so had no personal responsibility for the analysis, preparation and policy of 2020 and 2021 but still produced a report offering so little insight and so much spin. Silk, in particular, probably had no capacity to do more, but the occasional hope still lingered that perhaps Paul Conway, the new chief economist, might do better. But these were Orr’s hires, and it is widely recognised that Orr brooks no dissent, no challenge, and in his almost five years as Governor has never offered any material insight himself on monetary policy or cyclical economic developments. Even if they had no better analysis to offer – and perhaps they didn’t, so degraded does the Bank’s capabilities now seem – contrition could have taken them some way. But nothing in the report suggests they feel in their bones the shame of having delivered New Zealanders 6 per cent core inflation, with all the arbitrary unexpected wealth redistributions that go with that, let alone the inevitable economic disruption now involved in bringing inflation a long way back down again. It comes across as more like a game to them: how can we put ourselves in the least bad light possible with a mid-market not-very-demanding audience (all made more unserious as we realised that the Minister of Finance had made the decision a couple of months ago to reappoint Orr, not even waiting for the 120 pages of spin).

At this juncture, a good report would be most unlikely to have had all the answers. After all, similar questions exist in a whole bunch of other countries/central banks, and if the Reserve Bank has the biggest team of macroeconomists in New Zealand, there are many more globally (in central banks, academe, and beyond) but it doesn’t take having all the answers to recognise the questions, or the scale of the mistakes. In fact, answers usually require an openness to questions, even about your own performance, first. And there is none of that in the Bank’s report.

Thus, we get lame lines – of the sort Conway ran several times at Thursday’s press conference – that if the Bank had tightened a bit more a bit earlier it would have made only a marginal difference to annual inflation by now. And quite possibly that is so, but where is the questioning about what it would have taken – in terms of understanding the economy and the inflation process – to have kept core inflation inside the target range? What is it that they missed? (And when I say “they” of course I recognise that most everyone else, me included, also missed it and misunderstood it, but……central banks are charged by Parliaments with the job of keeping inflation at/near target, exercise huge discretion, carry all the prestige, and have big budgets for analytical purposes, so when central banks report on their performance, we should expect something much better than “well, we acted on the forecasts we had at the time and, with hindsight, those forecasts were (wildly) wrong”.) The question is why, what did they miss, and what have they learned that reduces the chances of future mistakes (including over the next year or two – if your model for how we got into this mess was so astray, why should the public have any confidence that you have the right model – understanding of the economy and inflation – for getting out of the mess? At the press conference the other day the Governor and the Board chair prattled on about being a “learning organisation” but you aren’t likely to have learned much if you never recognised the scale of the failure or shown any sign of digging deep in your thought, analysis, and willingness to engage in self-criticism. We – citizens – should have much more confidence in an organisation and chief executive will to do that sort of hard, uncomfortable, work than in one of the sort evident in last week’s report.

With hindsight one can make a pretty good case that no material monetary policy action was required at all in 2020. One might be more generous and say that by September/October 2020 with hindsight it was clear that what had been done was no longer needed. But that wasn’t the judgement the Reserve Bank came to at the time – and it is the Bank that has been tasked with getting these things right. Why? (And, of course, the same questions can be asked of other central banks and private forecasters, but the Reserve Bank is responsible for monetary policy and for inflation outcomes in this country.)

I may come back in subsequent posts to look at more detail at a number of specific aspects of the report (including a couple of genuinely interesting revelations) but at the big picture level the report does not even approach providing the sort of analysis and reflection the times and circumstances called for (in some easier times a report of this sort might have not been too bad, although you would always look for some serious research backing even then).

And if you think that I’m the only sceptic, I’d commend to you the comments from the former Deputy Governor of the Bank of Canada. On page after page – amid the politeness (and going along with distractions like the alleged role of the Russian invasion) – he highlights just how relatively weak the analysis in the report is, how many questions there still are, and a number of areas in which he thinks the Bank’s defensive spin is less than entirely convincing.

New Zealanders deserved better. That we did not get it in this report just highlights again that Orr is not really fit for the office he holds. In times like those of the last few years – with all the uncertainties – an openness to alternative perspectives, willingness to engage, willingness to self-critically reflect, and modelling a demand for analytical excellence are more important than ever.

Last week I reread Victoria University historian Jim McAloon’s history of New Zealand economic policymaking from 1945 to 1984, Judgements of all Kinds, first published a decade or so ago. Good works of economic history, let alone of the history of economic policymaking, aren’t thick on the ground in New Zealand, and as McAloon himself notes in a journal article published a year or two later:

“Economic history has a relatively low profile in New Zealand. Few economics programmes offer much in the way of economic history, and none of them offer courses in New Zealand economic history. Very few academics in New Zealand economics programmes publish in economic history. Victoria University, once boasting the only New Zealand chair in economic history, has largely abandoned the field.”

(Actually, when I was at Victoria in the early 80s – and not wise enough myself to have done much economic history – there were two professors of economic history)

Against this background of rather slim pickings, McAloon’s work is a useful contribution, including because he has gone back to at least some of the relevant archives. If you are at all interested in this period of New Zealand history – the backdrop in time to the post-1984 reforms and upheaval – I’d recommend the book, not because it is great or comprehensive but because it is (ie exists). In truth, although the title advertises coverage starting from 1945, there is quite a bit of material on economic policymaking in the 1930s and during the war too.

There is lots of interesting material, including about episodes few people now are particularly aware of (notably around the sterling area after the war). McAloon has his bugbears – not having much time for the British generally, or New Zealand farmers more specifically. And the phrase “the settler economy” keeps popping up, even when referring to events and developments decades after such a label had any more than rhetorical weight. I think he envisages the book as serving a somewhat revisionist purpose, in redeeming the tarnished reputation of the policymakers and advisers of the pre-1984 decades. I’m partial to a little of that sort of thing myself – for all his faults, for example, Muldoon clearly faced some of the most very adverse times to be a Minister of Finance almost throughout the 17 years that his terms spanned – but my sense is that McAloon sets himself rather too easy a target, in pushing back against some of the more florid rhetoric one still sometimes hears (from older politicians, economists, and business people) about the post-war New Zealand economy, and in the process acquits the policymakers, and most of their advisers, rather too readily. There is no doubt that the New Zealand economy in 1984 was a very different thing than it had been in 1945, and there had been plenty of sensible changes of policy made over the intervening decades. But the overall story remains one of deep relative decline, with no evident prospect of reversing that deterioration. And it wasn’t as if policymakers and advisers were innocents, unaware of the decline: by the very early 1960s serious independent reports from respected New Zealand economists were explicitly highlighting the extent of the relative productivity decline.

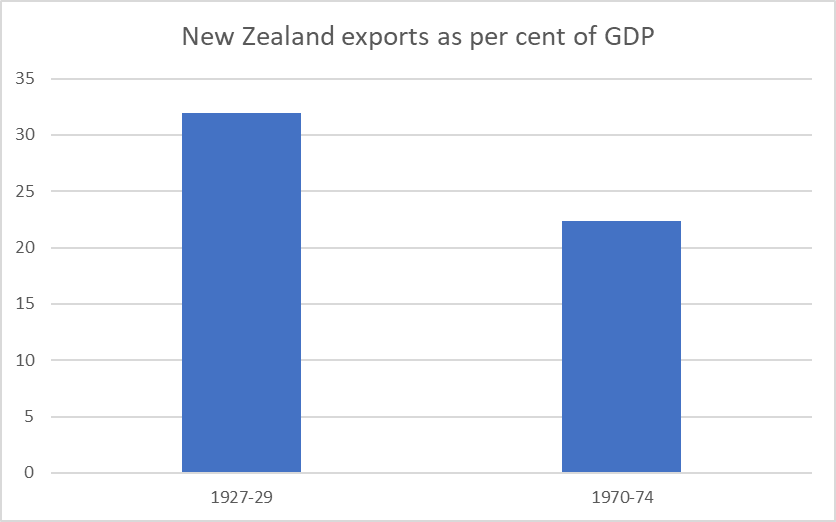

I’ve show numerous graphs here over the years highlighting New Zealand’s relative decline. But perhaps this simple one captures a significant aspect of what was going wrong. Read any book writing about inter-war New Zealand economic developments and it will make the point that per capita exports from New Zealand then were thought to be the highest of any country. That reflected a high level of GDP per capita and a high export share of GDP.

Consistent data over many decades is a challenge, but here are exports as a share of GDP as they were on the brink of the Great Depression (using as the GDP denominator the average of the three historical estimates on Infoshare) and by the early 1970s (using data from the OECD database).

By the early 1970s, not only had exports shrunk markedly as a share of New Zealand’s GDP, but that share was only around the median of the OECD countries (for which the OECD has data back that far), and that despite small countries typically trading more than large ones and New Zealand being in the smaller population grouping of OECD countries. One can debate the various possible causes of this steep relative decline, but New Zealand government policies did not, to say the least, help.

Anyway, the prompt to reading McAloon’s book again was that my son had been enrolled in McAloon’s second year New Zealand history course. If there are no specialist economic history courses at Victoria – which almost beggars belief given the way the university (and especially its commerce etc faculty) used to try to tout itself as preparing young people for careers in the public sector – at least there is some exposure to economic history topics in some of the history courses. Among the many essay topics students could choose from was one about New Zealand economic management from 1929 to 1975, and when my son chose to do that topic I suggested that reading the lecturer’s book might be worthwhile.

And here I divert into proud parent mode. I’ve included below the essay that Jonathan wrote on economic management over that period. I don’t agree with all of it (and had not read it until after the lecturer’s (high) marks came back) but – like the lecturer – I thought it was a pretty strong effort for a second-year student, and some of my readers may find the subject matter of interest. (And if anyone wants to hire a budding macroeconomist, he’ll probably be on the market in a couple of years.)

Controlling into Decline: Assessing government management of the New Zealand economy, 1929-1975.

by Jonathan Reddell

The period from 1929 to 1975 was an age of evolution in the New Zealand (NZ) economy. The upheavals of the Great Depression created a new consensus, while the economy continued to undergo the transition from a colonial to an independent economy. It cannot be said, however, that the period was an age of success. New Zealand’s relative decline during the period should not be understated. In 1939, New Zealand’s GDP per capita was $10,297, ahead of the Netherlands’ $7,079 and Canada’s $7,600. By 1975, both had surged ahead of New Zealand, as had others including Sweden.[1] New Zealand’s per capita growth rate lagged about 1% behind that of other developed market economies throughout the post-war period.[2] From 1929-1975, the performance of governments has been mixed, but that the economy was more often ill-managed than not. There are success stories, such as the diversification from Britain, and New Zealand remained one of the most prosperous countries on the planet, but on balance it was a drift into (relative) decline.

The role of the Great Depression in reshaping consensus economic thought in advanced capitalist economies is well known. The dislocations caused by the worst recession in modern history created the post-war consensus on full employment and the role of the state. This consensus would endure until the 1970s, when it was overturned by another crisis. New Zealand was no exception to this.[3] The following paragraphs will discuss government management of the Depression, and the new economic thought that was put into practice by the First Labour Government. The essay will then discuss the post-war consensus policies and assess how well governments managed the economy to achieve them.

The Depression’s impact on New Zealand was severe. A primary exporter, New Zealand was hard-hit by a shock whose hardest blow fell on commodities. Exports fell between 55-60% between 1928-29 and 32-33.[4] Rankin has estimated that joblessness peaked at over 35% of the workforce in 1932.[5] To compound matters, the New Zealand economy had been weakened by Britain’s anaemic economic performance in the 1920s due to the overvaluation of sterling from 1925.[6] Meanwhile the government’s ability to respond was constrained by the immense burden of public debt. In the 1931 Budget, public debt charges were by far the largest component of state expenditure, amounting to £10.9 million out of £24.7 million.[7] The debt burden and global loss of confidence severely constrained the government’s ability to borrow in London, while the inelastic debt payments meant that other sources of expenditure had to be cut, as a balanced budget was considered key to stability.[8]

While New Zealand did devalue against other currencies when Britain went off gold in September 1931, it did not devalue against sterling until 1933, prolonging the pain for exporters. From 1933, recovery was relatively rapid, as reforms including devaluation and the creation of a new monetary system under the Reserve Bank which allowed the Indemnity Act to lapse and monetary expansion while agricultural exports improved; by 1935 GDP per capita had recovered to the 1929 level.[9] Overall, the Coalition government’s management of the Depression was mixed. Belief in the desirability of a balanced budget constrained policy, as did the debt burden. On the other hand, the recovery was eventually strong, and as Hawke notes, actions were generally “sensible and sometimes imaginative.”[10] While it can be argued that the government could have taken more steps after Britain went off gold, overall, it is hard to argue with his judgement that, given the circumstances, the government did about as well as anyone else would have.[11]

By the time Labour came to power in 1935, the economy had generally recovered. Members of the new government had been greatly affected by the Depression and came to believe in the importance of boosting demand and that unemployment should never be allowed to reach such levels again.[12] Policy would be aimed at stabilisation, at security, at protecting the populace from the swings of the global economy. This would be achieved through polices such as expanded welfare and guaranteed prices for exporters. Nash wrote that the government, “intended to protect the producer…from the uncertainties of price.”[13] For dairy, this was done through the 1936 Primary Products Marketing Act. Labour perceived that the Depression illustrated New Zealand’s excessive vulnerability to the world economy, and aimed to counteract it, to ensure long term full employment. The state would lead industrial development to achieve both full employment and a less dependent economy. Labour’s policies marked a profound departure from the pre-Depression economy and created the basis of the post-war consensus which would last until 1975.[14] Stabilisation policy was locked in through the experiences of World War II (WW2), when the state took strong direct action and was generally successful.[15]

The post-war economic consensus consisted of several elements. National accepted the focus on full employment, and the welfare state, with Holland professing a belief that everyone had the right to employment and necessities.[16] A 1956 Royal Commission laid out the objectives of economic policy as: full employment, price stability, development, and promoting economic, social, and financial welfare of New Zealanders.[17] Governments from 1935 looked to manage the economy in pursuit of these goals, particularly full employment. The following paragraphs will assess their success regarding the economy.

The 1938-39 crisis was important in setting in the controls that would characterise the economy to 1984. From 1935 recovery continued apace, with GDP per capita one of the highest in the world in 1939. This would lead to crisis. The 1938-39 balance of payments crisis was a problem of the government’s own making, and a sign of things to come. Labour’s demand policies had resulted in a red-hot domestic economy, while a slowdown in the world economy resulted in a significant fall in export receipts. The trade balance fell from £10.5 million in 1937 to £2.9 million a year later.[18] Labour, unwilling to take actions that might harm workers like devaluation or fiscal retrenchment, opted for capital and import controls, which in some form would last until 1984. According to Hawke, the controls symbolised Labour’s move to an ‘insulationist’ economy.[19] The story of an overheated, full employment economy leading to a balance of payments crisis would be repeated periodically throughout the consensus period, including the crises of 1957-58 and 1966-67. The controls gave rise to a distorted economy and would have significant future negative impacts. Labour’s stabilisation policies undoubtedly had some value, but the obsession with full employment resulted in mismanagement in the 1930s, as it would again.

Post-depression governments would manage the economy with full employment front of mind. For Labour, it was, according to McAloon, “not negotiable.”[20] Speaking on the Employment Bill in 1945, Fraser said that “there is no greater tragedy than…being denied the opportunity,” to work, and being prevented from “contributing…to the production of goods and services.”[21] This undoubtedly succeeded, at least until the 1970s. From the late 1930s, the number of registered unemployed was incredibly low, bottoming out at 38 in 1950 and 1951.[22] While this number understates the true unemployment rate, estimates of that are as low as 1%.[23] This was a very low number by international standards.

While other countries also looked to achieve full employment, New Zealand’s unemployment was extremely low. For example, the United States, through the 1946 Employment Act declared a goal of “maximum employment.” However, even when the 1960s governments sought to make it a reality, unemployment never fell below 2.5%.[24] Therefore successive governments succeeded at managing the economy to achieve a level of full employment that was very low compared to other countries. A low unemployment rate has obvious benefits, but it also has costs. As was discussed, running a full employment economy with unemployment below the natural rate required import controls, to prevent domestic demand resulting in balance of payments crises. If unemployment had been allowed to rise to its natural level, which, as Gould notes, was likely quite low[25], the economy would have been less prone to fluctuations, whether in fiscal policy or the terms of trade, as demand for imports would have been generally weaker and there would have been less need for controls. Another negative of New Zealand’s extremely low unemployment rate was that fears of unemployment levels like other countries, particularly on the left, delayed NZ’s entry into the International Monetary Fund (IMF). Kirk exemplified those sentiments when he declared during the debate that NZ had “built up a social order that is unique,”[26] which IMF membership would imperil. In fact, non-membership of the IMF raised the cost of dealing with crises, while it did not prevent or cause higher unemployment.

Related to the full employment goal were import controls. As has been noted, successive governments looked to defend full employment while staving off balance of payments crises with import and capital controls, which would minimise the ability for New Zealand’s foreign reserves to drain. While National attempted to liberalise after 1949, controls were reimposed in 1951-52. These stop-go policies would repeat themselves, as the perceived foreign exchange constraint remained strong.[27] Import controls had major negative impacts. One was that import controls gave rise to import-substituting industries like textiles. These were often inefficient and misallocated resources away from potential export sectors. The high capital-output ratio of the economy through the 1950s and 1960s suggests inefficient usage, as it indicates a high level of capital was being used for low levels of output.[28] A 1968 World Bank report argued that “import restrictions are a hidden form of protectionism, which tend to result in a misallocation of resources,” and that they have failed to result in net exchange savings.[29] This seems believable as other sources have identified the high level of effective protection on NZ manufacturing, perhaps as high as 70% by the mid-1960s, and as a result, a functional tax on productive farmers, which weakened the NZ economy.[30]

While some level of control was understandable, particularly after WW2 given dollar shortages, New Zealand’s controls outlasted those of other OECD countries. Australia abolished import licencing in 1961.[31] A significant issue with New Zealand’s approach was the unwillingness to regard interest rates as a meaningful stabilisation tool. While many central banks abandoned interest rate control after WW2, New Zealand did not use interest rates even into the 1970s, while Australia had done so since the 1950s, due to factors including social credit influences and the sensitivity of farmers.[32] This had significant drawbacks because it meant more heavy-handed, distortionary controls were necessary to manage the economy. If interest rates, rather than direct controls, had been utilised as a policy tool, it seems likely that New Zealand’s relative decline would have been less marked. Easton argues that other OECD economies suffered from high protection of their agriculture sectors.[33] However, this mainly held up a dying industry and didn’t constrain the growth of industries like technology, while in New Zealand, controls raised the cost of inputs, effectively taxed agriculture, a growth sector, and allocated industrial capacity away from exports to import substitution.

The management of price stability is a mixed picture. An overheated economy continuously exerted inflation pressure. However, these pressures were mostly well constrained from the late 1940s. Condliffe observed that the New Zealand economy came out of WW2 “taut with supressed inflation.”[34] As wartime controls eased, inflation picked up to about 10% in 1947-48.[35] The government enacted several sensible measures to ease demand pressures and bring inflation down. These included a continued emphasis on national saving rather than overseas borrowing, which took money out of circulation, and the revaluation of 1948, which lowered the prices of exports and imports.[36] The New Zealand experience continued to be shaped by global conditions, as the Korean boom drove inflation to new heights in the early 1950s. While inflation fell and was generally relatively low between 1955 and 1970 it continued to be perceived as a threat. Hawke has observed that “prices rose by 2-3% in most years…worrying to many contemporaries.”[37] This perception is illustrated by a farmer, writing to the Press in 1961 that, “for the genuine farmer inflation is the worst thing that can happen.”[38] Thus, to the extent that governments are responsible for assuaging the fears of their citizens, NZ governments failed in that regard.

However, from a macroeconomic perspective, inflation was well managed until the late 1960s. The breakdown of the consensus between government, employers, and unions, particularly with the Nil Wage Order of 1968 was significant.[39] It combined with the overheated economy to produce significant levels of inflation that was managed inadequately through blunt instruments like freezes, due to ongoing full employment commitments. On balance, controlled inflation with overfull employment endured for a surprisingly long time. It is not clear, however, how much credit can be given to governments. New Zealand’s experience continued to be shaped by the global environment, and the inflation experience was similar to other countries, albeit at a lower level of unemployment.[40] A stronger factor seems to be the enduring legacy of Depression leading to a moderation of union militancy, which constrained wage, and thus price, inflation. However, governments do deserve at least some credit for keeping inflation as low as it was.

The third objective of economic policy was industrial development, which, from the mid-1950s linked with the need to diversify export markets as bulk purchase agreements ended in 1954 and Britain desired to join the European Economic Community. McAloon notes that “industrial development, trade development…were closely related over the decade after 1957.”[41] Industrial development was viewed as desirable from the late 1930s, as part of the quest to make New Zealand more insulated from price swings. This received greater focus under the Second Labour Government from 1957, particularly under the influence of Bill Sutch. Sutch wrote that “rapid and radical action is needed to readjust our economic structure,” towards manufacturing.[42] Sutch’s ideas reflected the flawed but orthodox view that there was a long-term decline in the terms of trade of commodity producers relative to industrial producers, known as the Prebisch-Singer thesis.[43] Its orthodoxy is illustrated by the World Bank’s report which argued that New Zealand’s fundamental problem was being “still too narrowly dependent on a few export commodities.”[44] Successive governments believed that industrial development was a priority, both for reducing balance of payments difficulties and maintaining prosperity.

The success of industrial development is a mixed picture. There were successful developments, such as the Kawerau pulp and paper mill and the wider forestry industry, and the domestic economy diversified throughout the 1960s. However, as was already noted, import controls resulted in misallocation towards import substitution, and experiments such as a cotton mill in Nelson were highly problematic.[45] The belief that too much agriculture was making New Zealand poorer seems particularly strange given that it remained the most productive industry.[46] The dominance of sheep and cow products did decline, from 90% of receipts in the 1930s to 53% in 1977/78, as new industries picked up: manufactured and forest products made up 23.4% of exports.[47] However, these exporters were often heavily subsidised, illustrated by the large incentives put on machinery in 1972.[48] These subsidies created their own inefficiencies. Again, governments were deploying distortionary solutions to questionably real problems. On the other hand, management of the diversification from Britain was successful. Trade agreements were signed with Japan in 1958, and significantly, with Australia in 1965.[49] Britain’s share of New Zealand exports fell from 51% in 1965 to 34% in 1971.[50] While there is much to criticise governments for how they handled the economy, they managed this landmark transition well, even if Britain’s relative economic marginalisation made trade readjustment inevitable.

In conclusion, the Depression shook the New Zealand economy, establishing a new order which sought full employment, price stability, and industrial development. While these were, for a time, achieved, it came at the cost of extensive controls which were a leading contributor to New Zealand’s relative decline. While successes like trade diversification cannot be overlooked, overall government management of the economy cannot be said to have been successful. The fundamental duty of government is to deliver prosperity and while New Zealand remained prosperous, it could have been much more so.

World Bank. The World Bank Report on the New Zealand Economy 1968. (1968).

Secondary Sources

Bernanke, Ben S. 21st Century Monetary Policy. New York: W.W. Norton & Company, 2022.

Bertram, Geoff. “The New Zealand Economy 1900-2000.” In The New Oxford History of New Zealand, edited by Giselle Byrnes, pp. 537-572. Melbourne: Oxford University Press, 2009.

Bloomfield, G.T. New Zealand: A Handbook of Historical Statistics. Boston: G.K Hall & Co., 1984.

Condliffe, J.B. The Welfare State in New Zealand. London: Allen and Unwin, 1959.

Easton, Brian. In Stormy Seas: The Post-War New Zealand Economy. Dunedin: University of Otago Press, 1997.

Gould, John. The Rake’s Progress? The New Zealand Economy Since 1945. Auckland: Hodder and Stoughton, 1982.

Greasley, David, and Les Oxley. “Regime Shift and Fast Recovery on the Periphery: New Zealand in the 1930s.” The Economic History Review 55, no. 4 (2002): pp. 697-720. https://doi.org/10.1111/1468-0289.00237

Gustafson, Barry. From the Cradle to the Grave. Auckland: Reed Methuen, 1986.

Hawke, G.R. The Making of New Zealand: An Economic History. Cambridge: Cambridge University Press, 1985.

Holland, Sidney. Passwords to Progress. Christchurch: Whitcombe and Tombs, 1943.

Kindleberger, Charles P. The World in Depression, 1929-1939. Revised Edition. Berkeley: University of California Press, 1986.

McAloon, Jim. Judgements of all Kinds: Economic Policy-Making in New Zealand 1945-1984. Wellington: Victoria University Press, 2013.

Nash, Walter. New Zealand: A Working Democracy. London: J.M Dent & Sons., 1944.

Rankin, Keith. “Workforce and Employment Estimates: New Zealand 1921-1939.” In Labour, Employment and Work in New Zealand, pp. 332-343, 1994.

Reddell, Michael, and Cath Sleeman. “Some perspectives on past recessions.” Reserve Bank of New Zealand, Bulletin, 71, no. 2 (2008): pp. 5-21.

Singleton, John, Arthur Grimes, Gary Hawke, and Frank Holmes. Innovation + Independence: The Reserve Bank of New Zealand 1973-2002. Auckland: Auckland University Press, 2006.

Sutch, W.B. “Colony or Nation? The Crisis of the Mid-1960s.” In Colony or Nation? edited by Michael Turnbull, pp. 163-183. Sydney: Sydney University Press, 1966.

Toye, John, and Richard Toye. “Origins and Interpretations of the Prebisch-Singer Thesis.” History of Political Economy 35, no. 3 (2003): pp. 437-467. muse.jhu.edu/article/46958.

[8] Michael Reddell and Cath Sleeman, “Some perspectives on past recessions,” Reserve Bank of New Zealand: Bulletin 71, no.2 (2008), p. 7.

[9] David Greasley and Les Oxley, “Regime shift and fast recovery on the periphery: New Zealand in the 1930s,” The Economic History Review 55, no.4 (2002), pp. 709-710.

[10] G.R. Hawke, The Making of New Zealand: An Economic History (Cambridge: Cambridge University Press, 1985), p .158.

[29] World Bank, The World Bank Report on the New Zealand Economy 1968 (1968), pp. 44-45.

[30] Geoff Bertram, “The New Zealand Economy: 1900-2000,” in The New Oxford History of New Zealand, ed. Giselle Byrnes (Melbourne: Oxford University Press, 2009), p. 557.

[31] John Singleton et al., Innovation + Independence: The Reserve Bank of New Zealand 1973-2002 (Auckland: Auckland University Press, 2006), pp. 17-21.

[42] W.B. Sutch, “Colony or Nation? The Crisis of the Mid-1960s,” in Colony or Nation?, ed. Michael Turnbull (Sydney: Sydney University Press, 1966), p. 183.

[43] John Toye and Richard Toye, “The Origins and Interpretation of the Prebisch-Singer Thesis,” History of Political Economy 35, no. 3 (2003), p. 437.

[44] World Bank, Report on the New Zealand Economy, p. 20.

[45] McAloon, Judgements of all Kinds, pp.112-115.

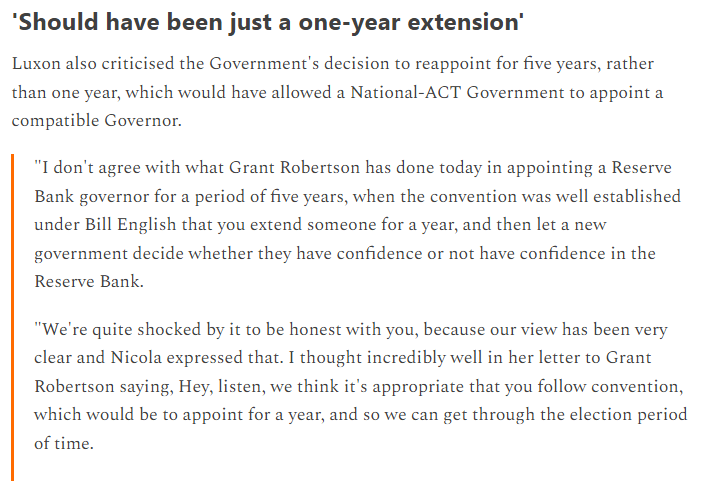

Over the last couple of months, the National Party has been running the line that a Reserve Bank Governor should not be appointed to the normal full five-year term when Orr’s existing term expires in late March, but that rather an appointment should be made for just a year so that whichever party takes office after next year’s election can appoint a Governor of their preference. We are told (although we have not yet seen the letter) that they made this case to the Minister of Finance when, as he was required to, he came consulting on his plan to reappoint Orr.

It is a terrible idea, on multiple counts.

But what is also irksome is the idea that in making a five year appointment, for a term beginning probably at least six months prior to the election, the Minister is breaching some established convention. That is simply a nonsense claim. This clip (from Bernard Hickey’s newsletter, this one opened to everyone) has some relevant quotes

There is simply no foundation to what Luxon is saying about what happened in the past. Since the Reserve Bank was made operationally independent in 1990, there have been two cases in which a Governor’s term has expired in election year but before the scheduled election. The first was in 1993, when Don Brash’s term expired on 31 August. The 1990 election had been held on 6 November 1990, so presumptively any new term was going to start within three months of the 1993 election. As it is, and partly to allay any possible market concerns (these were still fairly early days), Don’s reappointment was made and announced very early (if memory serves correctly in late 1992). I don’t recall any particular controversy about that reappointment (although the then Prime Minister had not been a huge Brash fan), but then Brash had initially been appointed by a Labour government (and the then Labour leader and finance spokesman had both sat in the Cabinet that had appointed him).

Of the next few (re)appointments:

Don Brash was appointed to a third term commencing in September 1998, not an election year

Don Brash resigned suddenly in April 2002, about three months before the general election. The then Deputy Governor was immediately appointed (lawfully) as acting Governor, both to run the Bank in the interim and to enable a proper search process to take place. Recall that under New Zealand law, the Minister of Finance cannot simply appoint his or her own person as Governor, and in those days the Bank’s Board used to guard its prerogatives (right and responsibility to nominate). The eventual appointment of Alan Bollard was not made until after the election.

Bollard was reappointed in 2007 (not an election year) and Wheeler was appointed in 2012 (also not an election year)

Which brings us to 2017. In 2016 Graeme Wheeler had advised that he would not be seeking a second term (probably to the general relief of both government and opposition parties at the time). Documents later released show that The Treasury (and the Board and minister) envisaged making a permanent new appointment some time early in 2017, well clear of the likely election date. However, those same papers also show that when the relevant authorities (in this case, Cabinet Office) were consulted it was established that the convention now (though perhaps not in 1992/93) was that permanent appointments should not be made when the new appointment would commence very close to (within three months of) an election date. In other words, the government could not get round the fact that Wheeler’s term expired close to the expected election date simply by making an early announcement of a permanent replacement. And thus they more or less had to settle on the idea of an acting Governor (Grant Spencer). Unfortunately, the then law was badly written (did not envisage the circumstances), and Graeme Wheeler (who could lawfully have been extended for six months) seemed keen to get back to commercial life ASAP, and the actual solution they landed on was almost certainly unlawful (I wrote a lot about it at the time, but here is a post that comments on the best arguments the Crown’s lawyers could make in defence).

So there is a precedent for an acting appointment (which, since the law was amended, could now be done lawfully) when the Governor’s term expired within three months of the election. That same convention, about not making permanent appointments, isn’t just about the central bank. But Orr’s term expires on 27 March, and the election seems likely to be at least six months after that, in a system with a three-year parliamentary term. It simply isn’t very serious or credible to argue that the government – otherwise still governing fully – should be unable (or even unwilling) to appoint a permanent Governor six or more months out from an election. You might argue, and I might have a bit of sympathy for such a view, that perhaps it would be better to give a Governor a six year term (the RBA Governor has a seven year term), so that overlaps with election years happened much less often, but the law is as it is, and I don’t recall the Opposition opposing five year terms when the reform bills were before the House. But there is no established precedent or convention about not making permanent appointments that start that far out from a likely election.

In passing, one might note that whereas with past appointments all powers of the Reserve Bank rested with the Governor, the various reforms put in place by this government have (at least on paper) considerably diminished the extent of the Governor’s powers, and created other appointments (notably external MPC members) which (at least on paper) provide avenues to shape and influence the Bank. I don’t want to put too much weight on this argument – I’ve spent years arguing that many of these changes in practice have been largely cosmetic – but not only could those provisions be used more aggressively by an incoming government that cared, but it would be quite legitimate for an incoming government to amend the legislation further (at the margin) to reduce the relative dominance of any particular individual serving as Governor. Our system would be better for such changes. (To be clear, like various other commenters, I would not support law changes designed directly to remove Orr: that way lies Erdogan type central banking.)

Whatever the law and precedent, it would also be a bad idea to be making acting appointments in circumstances like the present one. Our whole system around the Reserve Bank – and central banks in other advanced economies of our type – is set up around the idea that incoming governments don’t just get to pick their central bankers as soon as it suits. Instead, the system of operationally independent central banks has been built on (among others) the notion of technically capable, respected, non-partisan figures serving (whether as Governor or MPC members) for terms that do not align with the parliamentary term. Consistent with that vision, New Zealand’s legislation went further than most (too far in my view) in not even allowing the Minister of Finance to choose a Governor (or MPC members), but rather requiring that the Minister only appoint people who had first been nominated by the Board of the central bank, itself appointed for staggered terms by the Minister of Finance. Legislation was recently amended to even further reinforce this vision – of technically competent, respected, non-partisan appointees – when Labour explicitly added provisions requiring that other parties in Parliament be consulted before appointments are made (whether as Governor or Board members).

You could mount a counter-argument that this approach is a bit wrongheaded. After all, the legislation has also been amended recently to make it clear, that in monetary policy at least, the target the Bank works to is directly set by the government of the day. But notwithstanding that, the central bank still has a lot of practical policy discretion, and not just around monetary policy. Most advanced countries have made the choice that we do not want key central bank decisionmakers changing routinely when the government changes. That still seems, on balance, prudent to me, and in their calmer moments I’d be surprised if National really disagreed.

So the big problem in the current situation is NOT that an appointment has been made for five years. That should be the norm, whether or not it is six months from an election. The problem is specifically with the appointment (at all) of Adrian Orr. National seems reluctant to say that (perhaps because they may well be stuck working with him) but it is the main issue. There would be no such concern had a (hypothetical) generally highly-regarded (professionally, and among politicians), technically excellent, respected, non-partisan figure been appointed to the role. Specifically, National (and ACT) would not be raising concerns about the term of the appointment if they had any confidence in Orr. They do not. One can perhaps debate whether or not they should have such confidence, but in our system respect and confidence are earned, they are not something anyone can simply be forced to adopt. As I noted in yesterday’s post, the rank politicisation that has happened this week is not of National’s or ACT’s making, but of Robertson, in pushing ahead with an appointment – to a long-term position, where cross-party respect etc is important for the institution and its functioning – that the main Opposition parties seem to have been quite clear in opposing. It is not the job of Opposition parties to simply go along with whoever Robertson (and his, technically ill-equipped, board (itself, in some cases appointed over Opposition objections) determine). All the more so when Robertson himself was the one who introduced the formal consultation requirements, seeming to establish an expectation that strong (and reasoned) objections would be taken seriously. The responsibility was on Robertson – who holds the power to appoint or not – to respect the notion of only appointing someone who commands (even grudging) professional and personal respect. Orr no longer qualifies on that count. It is hard to think of any advanced country central bank Governor who will start a new term commanding so little respect, support, and confidence. That is really bad for the institution, and the institutional arrangements.

(Having said all this it would be good if National and ACT would pro-actively release their responses to Robertson’s consultation, rather than making us wait for OIA releases. It would be helpful to see what grounds the parties objected on, and whether they actually raised substantive concerns, or just relied on ill-founded process arguments.)

UPDATE: Having been sent a copy of the National letter of 30 September, it is now clear that National did not raise any substantive concerns about Orr, and focused wholly on the non-existent “convention” about not appointing a substantive Governor even 6-7 months out from an election.

Yesterday’s announcement from the Minister of Finance that he was reappointing Adrian Orr as Governor of the Reserve Bank was not unexpected but was most unfortunate. I was inclined to think another commentator (can’t remember who, so as to link to) who reckoned that it may have been Robertson’s worst decision in his five years in office was pretty much on the mark.

When Orr was first appointed, emerging out of a selection process kicked off by the Reserve Bank’s Board while National had still been in office, it seemed to me it was the sort of appointment that could have gone either way. I captured some of that in the post I wrote the day after that first appointment was announced, and rereading that post last night it seemed to at least hint at many of the issues that might arise and come to render the appointment problematic at best. Some things – a good example is $9.5 billion of losses to the taxpayer – weren’t so easy to foresee.

The timing of the reappointment announcement itself was something of a kick in the face for (a) critics, and (b) any sense that the better features of the new Reserve Bank legislation were ever intended as anything more than cosmetic. The Reserve Bank is tomorrow publishing its own review (with comments from a couple of carefully selected overseas people) of monetary policy over the past five years. Adding the statutory requirement for such a review made a certain amount of sense, but if there is value in a review conducted by the agency itself of its own performance, it was only going to be in the subsequent scrutiny and dialogue, as outsiders tested the analysis and conclusions the Bank itself has reached. But never mind that says Robertson, I’ll just reappoint Adrian anyway. Perhaps the Bank has a really compelling case around its stewardship of monetary policy – and just the right mix of contrition and context etc – but we don’t know (and frankly neither does Robertson – who has no expertise in these matters, and who appointed a Reserve Bank Board -the people who formally recommend the reappointment – full of people with almost no subject expertise).

But, as I say, the reappointment was hardly a surprise.

It could have been different. I’ve seen a few people say it would have been hard to sack Orr, but I don’t think that is so at all. No one has a right to reappointment (not even a presumptive right) and Robertson could quite easily have taken Orr aside a few months ago and told him that he (Orr) would not be reappointed, allowing Orr in turn the dignity of announcing that he wouldn’t be seeking a second term and would be pursuing fresh opportunities (perhaps Mark Carney would like an offsider for his climate change crusades?) Often enough – last week’s FEC appearance was just the latest example – Orr’s heart doesn’t really seem to be in the core bits of the job.

There are many reasons why Orr should not have been reappointed. The recent inflation record is not foremost among them, although it certainly doesn’t act as any sort of mitigant (in a way that an unexpectedly superlative inflation record in a troubled and uncertain world might – hypothetically – have).

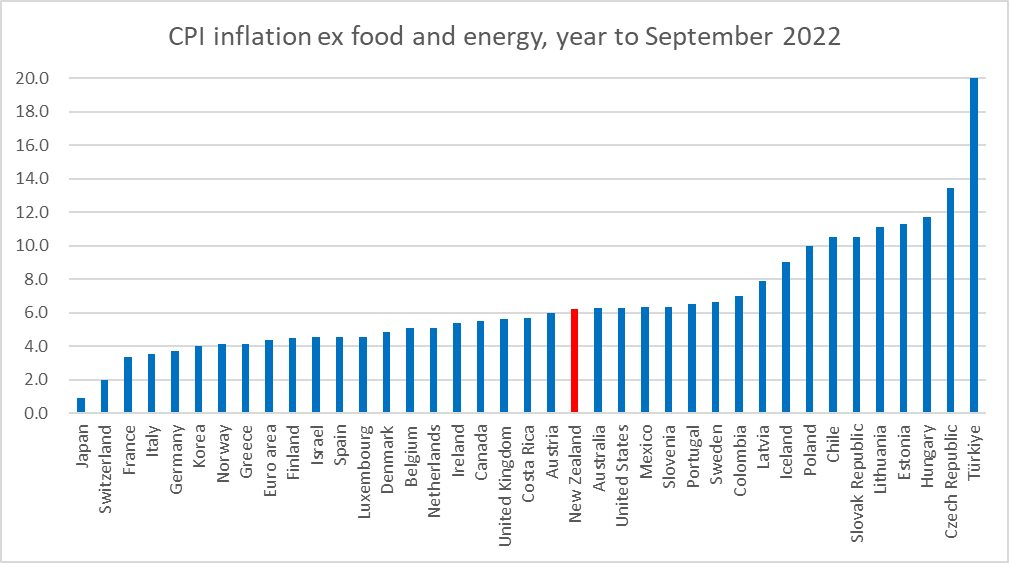

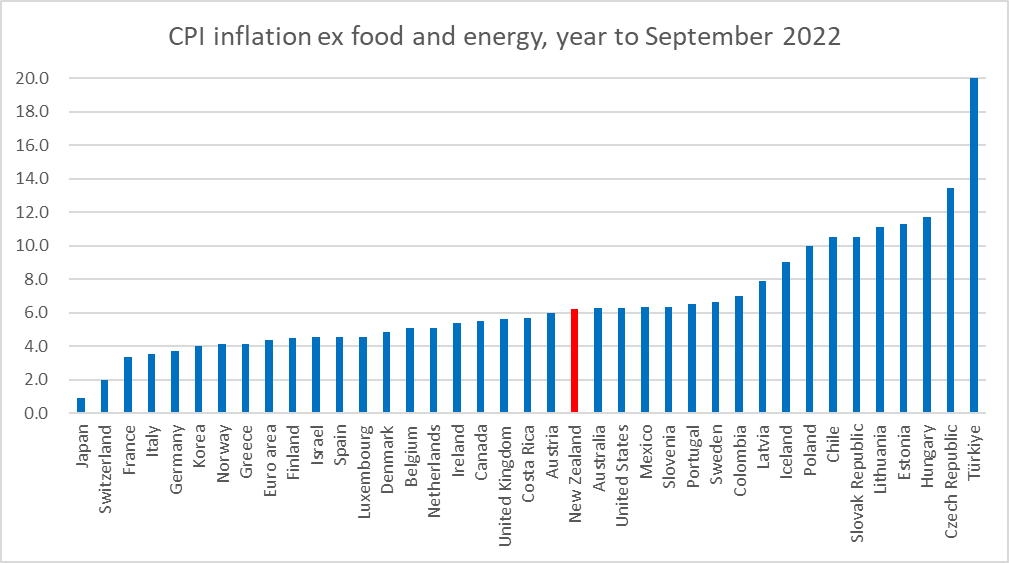

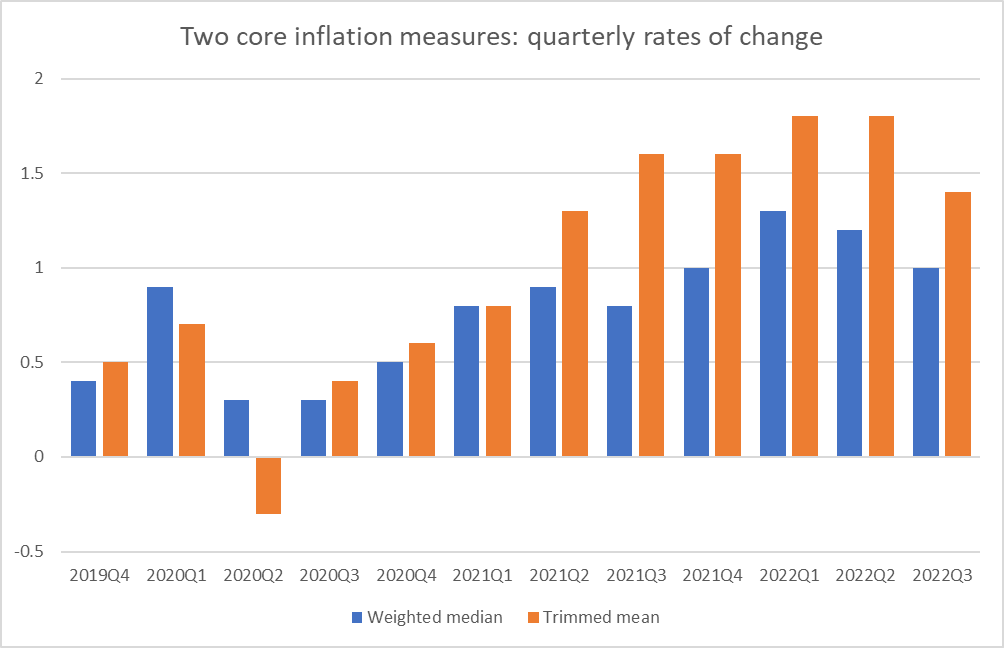

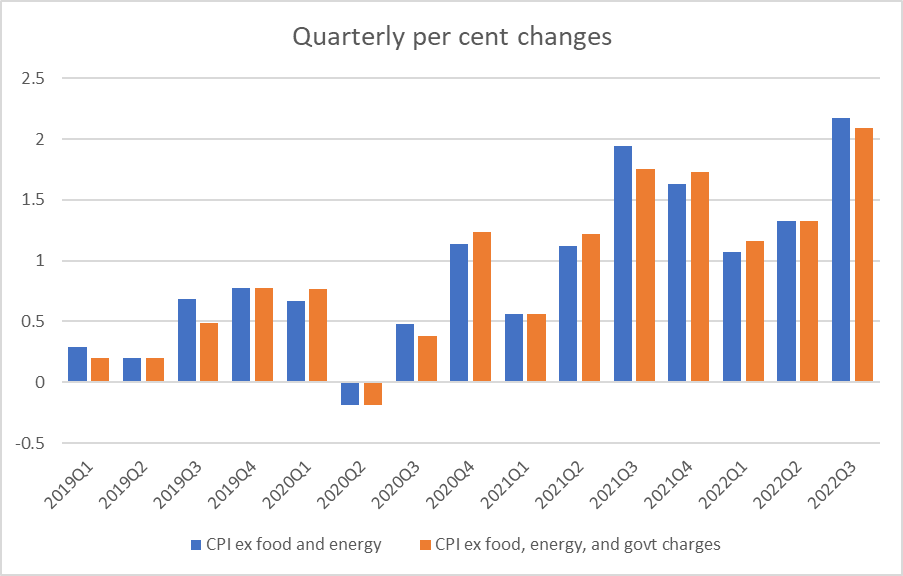

There is nothing good, admirable, or even “less bad than most” about the inflation record. This chart is from my post last week

A whole bunch of central banks made pretty similar mistakes (and the nature of floating exchange rates is that each central bank is responsible for its country’s own inflation rate). Among the Anglo countries, we are a bit worse than the UK and Canada and slightly less bad than the US and Australia. Among the small advanced inflation targeters – a group the RB sometimes identified with – we have done worse than Switzerland, Norway, and Israel, and better than Sweden and Iceland. In a couple of years (2021 and 2022) in which the world’s central bankers have – in the jargon – stuffed up badly, Orr and his MPC have been about as bad on inflation as their typical peers.

You could mount an argument – akin to Voltaire on the execution of Admiral Byng – that all the world’s monetary policymakers (at least those without a clear record of dissent – for the right reasons – on key policy calls) should be dismissed, or not reappointed when their terms end, to establish that accountability is something serious and to encourage future policymakers to do better. You take (voluntarily) responsibility for inflation outcomes, and when you fail you pay the price, or something of the sort. Inflation failures – including the massive unexpected wealth redistributions – matter.

Maybe, but it was never likely to happen, and it isn’t really clear it should. As I’ve noted here in earlier posts until well into 2021 the Reserve Bank’s forecasts weren’t very different from those of other forecasters, and I’m pretty sure that was also the case in other countries. Inflation outcomes now (year to September 2022) are the result of policy choices 12-18 months earlier. With hindsight it is clear that monetary policy should have been tightened a lot earlier and more aggressively last year, but last February or even May there was hardly anyone calling for that. Absent big policy tightenings then, it is now clear it was inevitable that core inflation would move well outside the target range. There are plenty of things to criticise the Bank for – including Orr’s repeated “I have no regrets” line – but if one wants to make a serious case for dismissing Orr for his conduct of monetary policy it is probably going to have to centre on (in)actions from say August 2021 to February 2022 (whereafter they finally stepped up the pace) but on its own – it was only six months – it would just not be enough to have got rid of the Governor (even just by non-reappointment). The limitations of knowledge and understanding are very real (and perhaps undersold by central bankers in the past), and even if Orr and the MPC chose entirely voluntarily to take the job (and all its perks and pay) those limitations simply have to be grappled with. Were New Zealand an outlier it might be different. Had the Bank run views very much at odds with private forecasters etc it might be different. But it wasn’t.

I am, however, 100 per cent convinced that Orr should not have been reappointed. I jotted down a list of 20 reasons last night, and at that I’m sure I’ve forgotten some things.

I’m not going to bore you with a comprehensive elaboration of each of them, most of which have been discussed in other posts. but here is a summary list in no particular order:

the extremely rapid of turnover of senior managers (in several case, first promoted by Orr and then ousted) and associated loss of experience and institutional knowledge

the block placed – almost certainly at Orr’s behest – on anyone with current and ongoing expertise in monetary policy nad macroeconomic analysis from serving as an external member of the MPC

the appointment as deputy chief executive responsible for macroeconomics and monetary policy (with a place on the MPC) of someone with no subject expertise or relevant background

$9.5 billion of losses on the LSAP – warranting a lifetime achievement award for reckless use of public resources – with almost nothing positive to show for the risk/loss

the failure to ensure that the Bank was positioned for possible negative OCRs (having had a decade’s advance warning of the issue), in turn prompting the ill-considered rush to the LSAP

the failure to do any serious advance risk analysis on the LSAP instrument, as being applied to NZ in 2020

the sharp decline in the volume of research being published by the Reserve Bank, and the associated decline in research capabilities

the way the Funding for Lending programme, a crisis measure, has been kept functioning, pumping attractively-priced loans out to banks two years after the crisis itself had passed (and negative OCR capability had been established)

lack of any serious and robust cost-benefit analysis for the new capital requirements Orr imposed on banks (even as he repeatedly tells us how robust the system is at current capital levels)

repeatedly misleading Parliament’s Finance and Expenditure Committee (most recently, his claim last week that the war was to blame for inflation being outside the target range), in ways that cast severe doubts on his commitment to integrity and transparency

his refusal to ever admit a mistake about anything (notwithstanding eg the biggest inflation failure in decades)

the fact that four and a half years in there has never been a serious and thoughtful speech on monetary policy and economic developments from the Governor (through one of the most turbulent times in many decades)

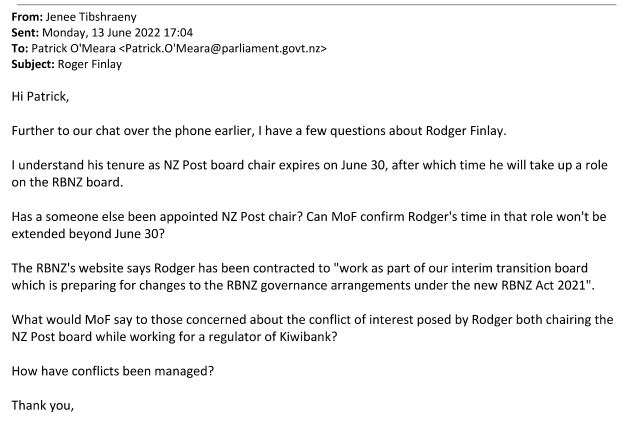

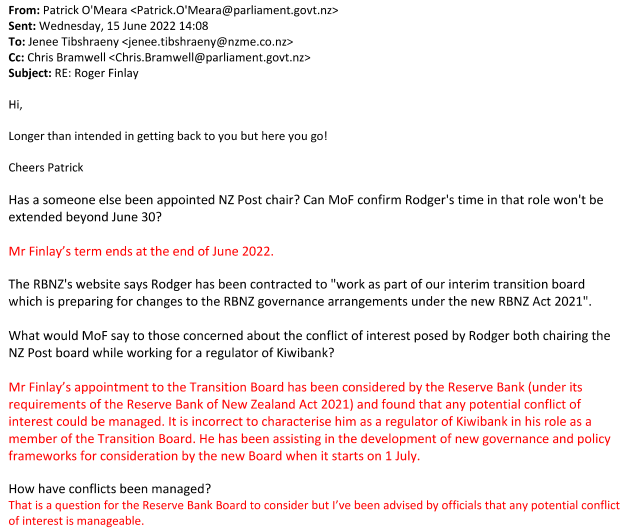

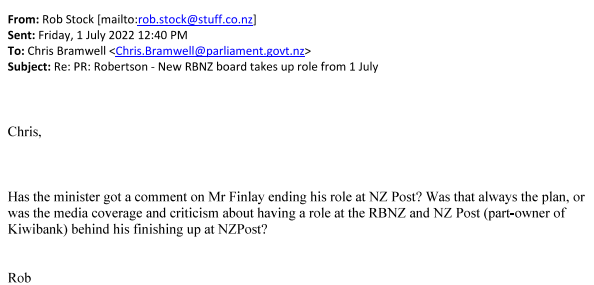

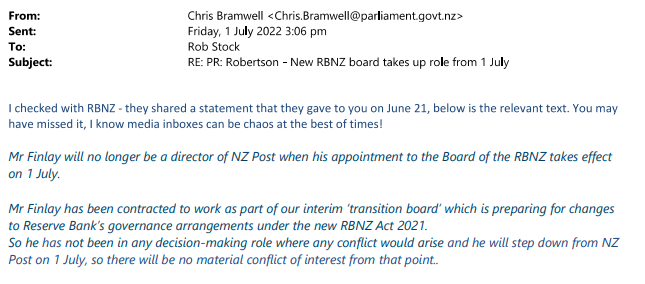

Orr’s active involvement in supporting and facilitating the appointment of Board members with clear conflicts of interest (Rodger Finlay especially, but also Byron Pepper)

his testiness and intolerance of disagreement/dissent/alternative views

his often disdainful approach to MPs

his polarising style, internally and externally

all indications are that he is much more interested in, and intellectually engaged by, things he isn’t responsible for than for the things Parliament has charged him with

organisational bloat (think of the 17-20 people in the Communications team or the large number of senior managers now earning more than $400000 pa)

the distraction of his focus on climate change, but much more so the rank dishonesty of so much of it – claims to have done modelling that doesn’t exist, attempts to suppress release of information on what little had been done, and sheer spin like last week’s flood stress test. It might be one thing for a bloated overfunded bureaucracy to do work on things it isn’t really responsible for if it were first-rate in-depth work. It hasn’t been under Orr.

much the same could be said of Orr’s evident passion for all things Maori – in an organisation with a wholesale macroeconomic focus, where the same instruments apply to people of all ethnicities, religions, handedness, political affiliation or whatever. What “analysis” they have attempted or offered has been threadbare, at times verging on the dishonest.

the failure to use the opportunity of an overhaul of the RB Act to establish a highly credible open and transparent MPC (instead we have a committee where Orr dominates selection, expertise is barred, and nothing at all is heard from most members)

And, no doubt, so on. He is simply unfit to hold the office, and all indications are that he would have been so (if less visibly in some ways) had Covid, and all that followed (including inflation), never happened.

But the crowning reason why Orr should not have been reappointed is that doing so has further politicised the position, in a most unfortunate way.

In the course of the overhaul of the Reserve Bank Act, Grant Robertson introduced a legislative requirement that before appointing someone as Governor the Minister of Finance needed to consult with other parties in Parliament (parallel provision for RB Board members). It was a curious provision, that no one was particularly pushing for (in most countries the Minister of Finance or President can simply appoint the Governor, without even the formal interposition of something like the RB Board), but Robertson himself chose to put it in. The clear message it looked to be sending was that these were not only very important positions but ones where there should be a certain measure of cross-party acceptance of whoever was appointed, recogising (especially in the Governor’s case) just how much power the appointee would wield. That provision never meant that governments could not appoint someone who happened to share their general view of the world and economy, but there was a clear expectation that whoever was appointed would be sufficient to command cross-party respect for the person’s technical expertise, non-partisan nature, dispassionate judgement and so on. Robertson simply ignored Opposition dissents on a couple of the Board appointees. That was of second order significance, but it is really significant in the case of the Governor. It isn’t easy to dismiss a Governor (and rightly so) so for a Minister of Finance to simply ignore the explicit unease and opposition of the two main Opposition parties in Parliament is to make a mockery of the legislation Robertson himself had put in place so recently. The Opposition parties are being criticised in some places (eg RNZ this morning) for “politicising the position/appointment” but they seem to have been simply doing their job – it was Parliament/Robertson who established the consultation provision – and the consultation provisions, if they meant anything, never meant giving a blank slate for whomever the Minister wanted to offer up, no matter the widely-recognised concerns about such a nominee. No one has a right to reappointment and when it was clear that the main Opposition parties would not support reappointment, Robertson should have taken a step back, called Adrian in and told him the reappointment could not go ahead, in the longer-term interests of the institution and the system. If you were an Orr sympathiser, you might think that was tough, but….no one has right to reappointment, and the institution matters.

And, of course, now the position of the Governor has inevitably been put into play, with huge uncertainty as to what might happen if/when National/ACT form a government after the election next year. (And here is where I depart from National’s stance – I never liked the idea of a one year appointment, made well before the traditional pre-election bar on new permanent appointments. We want able non-partisan respected figures appointed for long terms (it is the way these things work in most places), not for each incoming PM to be able to appoint his or her own Governor.)

A few months ago, anticipating that Orr would probably be reappointed, I wrote a post on what an incoming government next year could do about the Bank. The key point to emphasise is that a new government cannot simply dismiss a Governor they don’t like (or nor should they be able to). I saw a comment on a key political commentary site this morning noting that the process for dismissal isn’t technically challenging, which is true, but the substantive standards are quite demanding (the Governor can be dismissed only for specific statutory causes, and for (in)actions that occurred in his new term (which doesn’t start until March)). Generally, we do not want Governors to be able to be easily dismissed (in most countries it is even harder than in New Zealand). More to the realpolitik point, any dismissal could be challenged in the courts, and no one would (or should) want the prolonged uncertainty (political and market) such actions might entail. Moreover, senior public figures cannot just be bought out of contracts.

We still don’t know – and perhaps they don’t either – how exercised National and ACT would be about any of this were they to form a government next year, but unless Orr was himself minded to resign (as the Herald’s columnist suggests might happen) things would have to be handled carefully and indirectly (perhaps along lines in that earlier post of mine) to change the environment and the incentives around the institution. Most of those changes should be pursued anyway, to begin to fix what has been done over the last few years And if Orr were to be inclined not to stick around for long, perhaps an offer of appointment as High Commissioner to the Cooks Islands might smooth his way?

In my post last Friday I highlighted how the Governor of the Reserve Bank had just been making up stuff, and apparently knowingly misleading Parliament, to distract from the Bank’s own responsibility for New Zealand’s current very high core inflation. There may well be a case to be made that central banks did about as well as could reasonably be expected over the last couple of years – “reasonably be expected” here set by reference to the general views at the time of other expert observers (none of whom, admittedly, had chosen to take on statutory responsibility for inflation) but simply making stuff up blaming the Moscow bogeyman helps no one, and detracts from any serious conversation about what went on with inflation – core and headline – and why. To put my own cards on the table, there are many reasons why Adrian Orr should not be reappointed, but the poor inflation outcomes are not the most important of those reasons (of course, a superlative performance on inflation might have covered over a multitude of other sins and shortcomings).

After Friday’s post, someone got in touch to point out that I had not mentioned one other episode in that FEC appearance which could also reasonably be described as “making stuff up” and misleading Parliament. Opposition members were asking questions that included that rather loaded phrase “printing money”, to which Orr responded – apparently in reference to the LSAP – that the Reserve Bank did not create money, that all they did was to lower bond yields, and that banks etc were the people who increased the money supply.

In normal circumstances, the Governor’s comment would not be far wrong. The “money supply” – deposits with financial intermediaries (those included in the Bank’s survey) held by “the public” (ie people and firms not themselves included in the survey) – mostly increases in the process of private sector credit creation. For example, each new mortgage to purchase a house results simultaneously in the creation of either a deposit or a reduction in another mortgage as the house seller deals with the proceeds of the sale. Monetary policy operates typically by adjusting interest rates to influence, among other things, the demand for credit.

Some of the Reserve Bank’s emergency crisis tools don’t have any direct effect on the money supply measures the Reserve Bank compiles and reports. The Funding for Lending programme – a crisis programme that bizarrely is still injecting cheap liquidity now – simply lends money to banks (against collateral). That transaction boosts settlement cash balances held by banks at the Reserve Bank, but those balances aren’t part of “money supply” measures (they are deposits held by one lot of surveyed institutions – banks – at another surveyed institution – the Reserve Bank).

The LSAP is different. If, for example, a pension fund had been holding government bonds and had then sold those bonds to the Reserve Bank. the pension fund would receive payment from the Reserve Bank in a form that adds to that pension fund’s deposits at a bank. Settlement cash balances increase in the process, but so does the money supply (the pension fund’s deposits count in the money supply just the same way that your deposits do). Had the Reserve Bank bought all those tens of billions of dollars of bonds from local banks, the transaction would have boosted only settlement cash and not the money supply measures. But it didn’t. There were plenty of sellers – the Reserve Bank was eagerly buying at the top of the market – and some were local banks, and others were not. And so when the Governor suggested to Parliament that the Bank’s bond-buying did not increase the money supply, he wasn’t really being strictly accurate.

If you are now drumming your fingers are thinking this is all very technical and not really to the point, then in some respects you are correct. We’ve heard a lot about “the money supply” in the last couple of years. Most of it isn’t very accurate, but in many respects the difference doesn’t matter very much. “Money supply” measures (the formal ones referred to above) have not mattered very much to central bankers for decades, and that has been so whether inflation was falling sharply and undershooting inflation targets, or (as at present) proving very troublesome on the high side. The general view has been that money supply measures have not contained consistently useful information about the outlook for inflation, over and above what is in other indicators.

That does not mean – to be clear – that inflation is anything other than a monetary phenomenon for which central banks (and their masters) are responsible. It also does not mean that in extreme circumstances, in which say the government/central bank is flinging huge amounts of money at households without any intention of paying for those handouts now or later through higher taxes, that straight-out government money creation will not be a problem, paving the way for something that could end in hyperinflation. It is simply that specific official measures of the money supply have not proved very useful as inflation forecasters. Decades ago we hoped they did – and money supply growth targets were the rage for a decade or more in some central banks – but they didn’t.

And perhaps you can begin to see why if we go back a couple of paragraphs to the LSAP purchases. If the Reserve Bank purchases bonds from you and me (or our Kiwisaver fund) that will add to the money suply measures the Reserve Bank compiles and reports. If the Reserve Bank instead buy bonds from banks who bank with the Reserve Bank, it won’t add to the money supply measures. Does anyone really suppose there are materially different macroeconomic implications from those two different scenarios? The Reserve Bank doesn’t (from all they have said and written about how they think the LSAP works) and – for what it may be worth – I agree with them. You could add a third scenario, in which the Bank buys a bond from a non-bank entity that itself had bought the bond on credit. In that case, even RB purchasing from a non-bank won’t add to the money supply measures, but will (presumably) reduce any credit aggregates that captured the initial loan.

It might all have been different decades ago when, for example, central banks paid no interest on settlement cash balances, sometimes (as in New Zealand) banks were forbidden from paying interest on short-term or transactions deposits, and where banks were subject to variable reserve asset ratios. That was the world I started work in, but none of that is true today. Money supply measures usually aren’t very enlightening about inflation prospects, and these days neither even is the level of settlement cash balances (since the Reserve Bank pays the full OCR on whatever balances have accumulated). Thus, the LSAP may have been a dumb idea (and a very expensive one so it proved), but not because it may or may not have boosted official measures of the money supply to some extent. The pension fund that sold a government bond and now has bank CD in its books instead is no better or worse off because one asset wasn’t in the money supply official measures and the other one is. Neither are its members.

What matters is (mostly) two things: first, level and structure of interest rates, and second whether or not more purchasing power is put in the hands of public. The LSAP purports to change the former – which it seems was probably what the Governor was trying to claim at FEC the other day – but does not, and does not purport to, change the latter directly.

(By contrast, when for example the government sharply ran down its cash balances at the Reserve Bank and paid out at short notice a huge level of wage subsidy payments, not only did those payments boost the money supply measures (in most cases) but they put more purchasing power in the hands of the private sector (households supported by those payments). That isn’t a comment about the merits or otherwise of the wage subsidy scheme – I thought it was mostly great, directly counteracting what would otherwise have been a huge loss of purchasing power – just a description of how things work technically).

What about some numbers and charts?

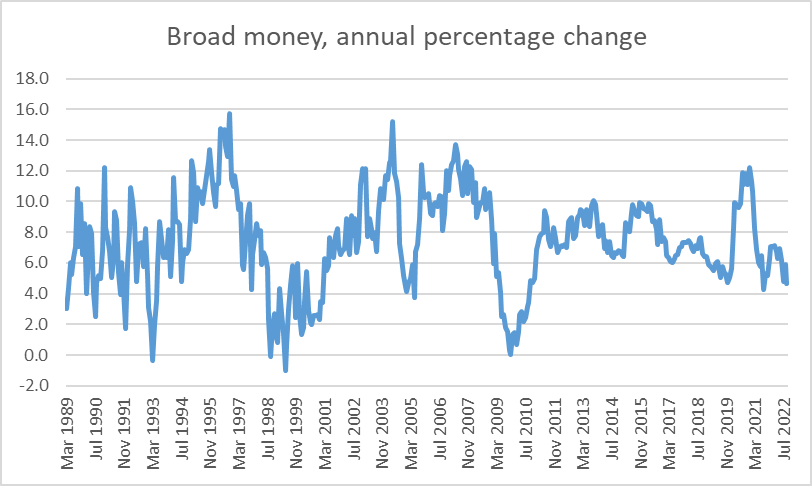

This is a chart of annual growth in the Reserve Bank broad money measure

Annual growth rates have fluctuated a lot. There was a surge in the annual growth rate in 2020 (and a 3.5 per cent lift in the month of March 2020 alone, presumably largely reflecting the wage subsidy payments) but (a) it proved shortlived, (b) the peak was still materially below peaks in the 90s and 00s, and c) core inflation in the mid 90s and mid-late 00s did not get near the current core inflation rates (depending on your measure somewhere between 5 and 7 per cent).

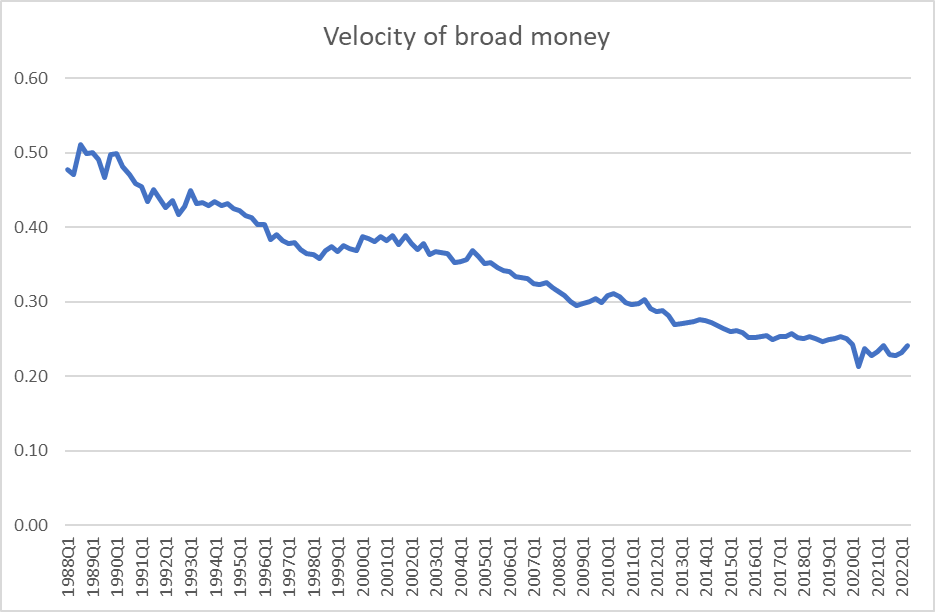

For those of you who remember studying money in your economics courses, here is a measure of the velocity of money (in this case, quarterly nominal GDP divided by the broad money stock at the end of each quarter.

This measure of the money supply has been been growing faster than nominal GDP pretty much every year since 1988 (mostly just reflecting the fact that regulatory restrictions on land use have inflated house prices to absurd levels, driving up both money and credit as shares of GDP). You can see a bit of noise in 2020 – the big initial increase in the money supply I mentioned earlier and the temporary sharp reduction in GDP – but two years on there is nothing now that looks unusual.

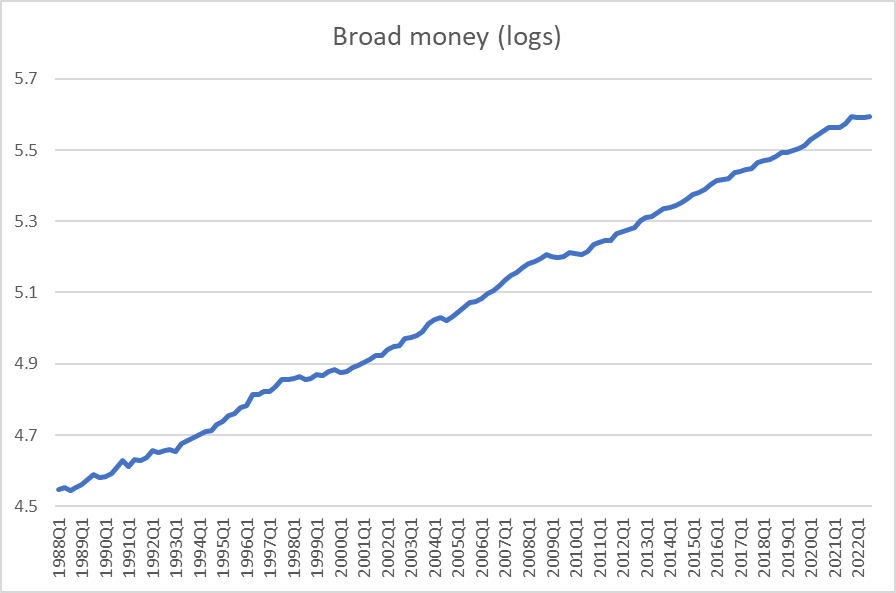

Here is a chart of the level of broad money, expressed in logs (which means that if the slope of the line is unchanged so is the percentage rate of growth in the underlying series).

Nothing particularly out of the ordinary in money supply developments (on this formal measure) over the last few years.

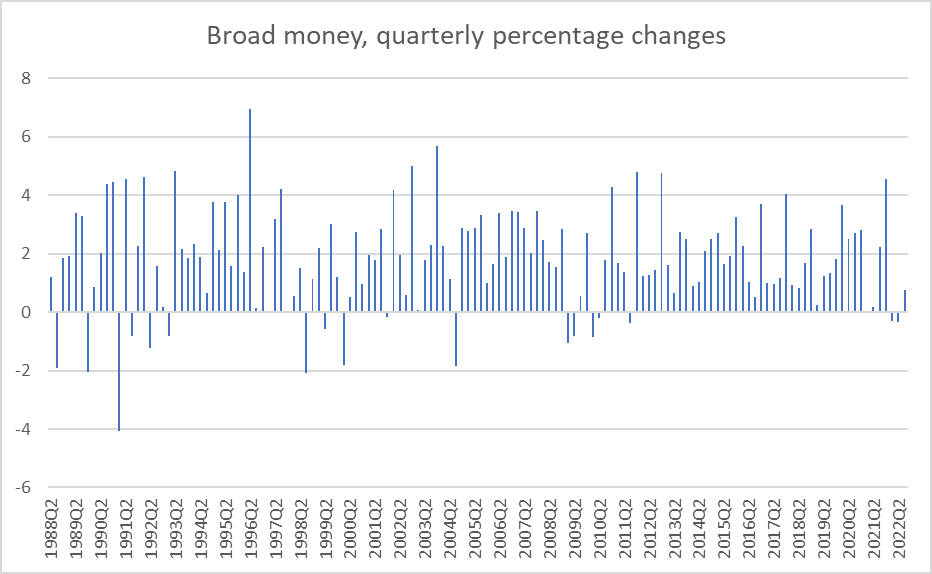

But for anyone out there who still wants to put some weight on this official measure of the broad money supply, here is the chart of quarterly percentage changes.

Eyeballing it, the most recent three quarters (to September this year) appear to have had the weakest growth since 2009. a period when nominal GDP growth and core inflation falling away sharply. Since I don’t put much weight on money supply measures, as offering anything much about the inflation outlook, I wouldn’t emphasise the comparison myself.

Inflation is primarily a monetary phenomenon, and a national phenomenon (that was why the exchange rate was floated, to make it so), and something for which central banks are responsible and should be accountable. Core inflation has been – and still is – at unacceptably high rates, as a result of choices and misunderstandings by our central bank (their misunderstandings were widely shared, among private sector economists and in other countries, but that does not change the responsibility even if it might mitigate the appropriate consequences for those central bank decision makers). Monetary policy choices matter, a lot. But official measures of the money supply don’t usually shed much additional light, and have not done so over the last couple of years.

Legislatures typically take a dim view of efforts to mislead them or their committees. This is from our own Parliament’s online “How Parliament works”

The Governor of the Reserve Bank seems just not to care, treating Parliament’s Finance and Expenditure Committee with as much contempt, and disregard for basic standards of honesty and care as some juvenile delinquent.