The Reserve Bank’s MPC will deliver their next OCR decision on Wednesday. The consensus seems to be (quite strongly, and I have no particular reason to differ) that the Bank will raise the OCR by another 50 basis points. At 3.5 per cent, the OCR would then be at the peak level it was (inappropriately) raised to in 2014, at a time when core inflation was well below the target midpoint and the unemployment rate was lingering high.

I’m less interested in what the MPC will do than in what they should do, and on that count I’m less convinced that the consensus call would be the appropriate one. In times like the last 2-3 years, no one should feel overly confident about any particular assessment of what monetary policy stance will prove to be needed: there is inevitably an aspect of feeling your way, knowing that when all the relevant data are available there is a fair chance you will be wrong one way or the other.

It isn’t the easiest situation in which to be making an OCR decision. We aren’t at the very start of a tightening cycle, rather the OCR has already been raised by 275 basis points since last October, and if that cumulative increase isn’t overly large by historical standards, the cuts in 2020 were also much smaller in total than in most prior easing phases (that would be so even if one included the 2019 cuts in a calculation). And most of the OCR increases have been really quite recent – it was only in mid April that the OCR was raised above the 1 per cent it had been when Covid hit, and we all know that monetary policy works with lags, often quite considerable ones.

But here, in some respects, the MPC has made a rod for its own back. At present, the most recent inflation data we have are for the June quarter. The midpoint of the June quarter (where the CPI is centred) was mid-May, a point at which (although more was expected over time) the OCR had only just been raised beyond 1 per cent. We’ll have the next release of the CPI on 18 October, and it would seem a great deal more sensible to have held off making the next OCR decision until then.

The annual cycle of OCR/MPS review dates was set a long time ago, and there used to be a view that the latest CPI didn’t often matter much so there wasn’t a particular problem with setting review dates just before the CPI release. But that was back in the days when the inflation rate was pretty stable (and low), not when it was well outside the target range, having been rising strongly (at least in annual terms for some time). It was even worse in July when the OCR review took place less than a week before the CPI was released.

Policymaking is suffering too from decades of underinvestment in macroeconomic data. Even when we get the September quarter CPI, that will have been centred in mid-August, and by then (eg) the United States will have had their September monthly data. I gather the Reserve Bank has now come round to wishing there was a monthly CPI – belatedly, since this was the same institution that frowned upon the idea 20 years ago when the then independent review of monetary policy, undertaken for the then government, by a leading overseas economist, highlighted the omission and recommended remedying it. Same goes for most of the labour market data: the June quarter data (latest we have) is centred (again) on mid May (although the new monthly employment indicator does represent some improvement in the New Zealand data in this area). We really need to be spending a bit more to get good quality monthly CPI and HLFS data, as almost all other OECD countries have. As it is, combining poor data with a weak MPC is not a recipe for good, robust, and trustworthy monetary policymaking.

And not too far down the track we will face again the MPC’s extended summer holiday, with no review of the OCR at all in the three months from 23 November to 22 February. That long holiday last summer almost certainly contributed to the OCR being increased more slowly than it should have been.

If it were me, I would have been postponing next week’s OCR review until a few days after the OCR review, delaying the next MPS until early December, and scheduling an additional OCR review at the end of January (after the December CPI data are available).

As it is, on the data we actually have to hand, I’m sceptical of the case for a 50 basis point OCR increase right now.

Some of the straws in the winds?

First, there was the relatively weak nominal GDP growth for the year to June (most recent we will have for quite a while yet) – the June quarter was 5.9 per cent higher than the June 2021 quarter, among the very lowest growth rates facing advanced country central banks. Nominal GDP is considerably easier to measure than real GDP, and is a relevant consideration in thinking about appropriate monetary policy.

Second, asset prices have been falling quite considerably. I’m not a great believer in wealth effects from house prices, but materially lower house prices will blunt the incentives for developers to continue to put in place new houses, and residential investment is one of the most cyclical components of the economy. There is a stronger argument for wealth effects from share prices, and share prices have also fallen back (eg the NZSE50 is below immediately pre-Covid levels), also dampening incentives for firms to undertake new business investment.

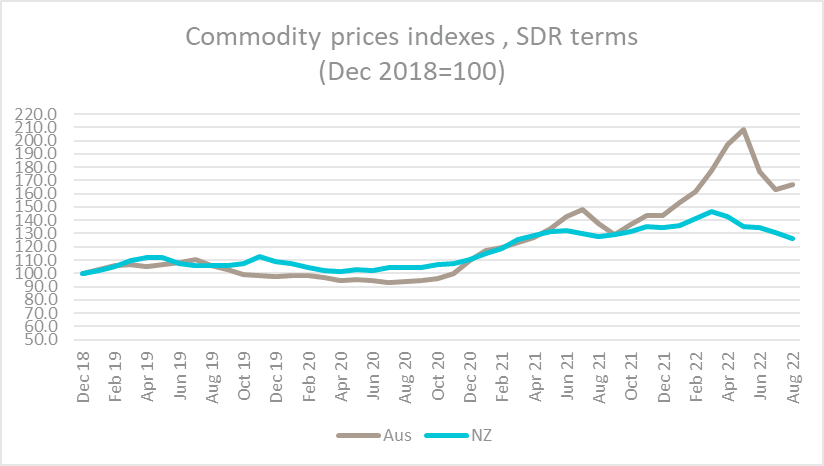

Third, if international New Zealand export commodity prices aren’t exactly weak, they are nothing like as strong as those in Australia (ANZ and RBA series respectively in the chart).

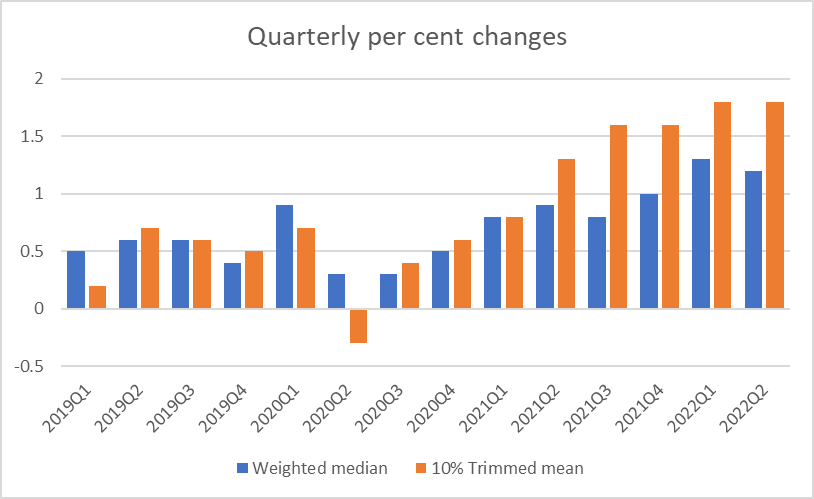

And then there are the core inflation measures. Much of the media and political attention has been (perhaps understandably) on the annual rate of inflation (complete with petrol tax cut distortions). That annual rate may well have fallen back a bit in September (petrol prices and all that), but it shouldn’t really be the focus. Ideally, we want to look at quarterly core meaaures – indicators of what is happening behind the headline “noise”. (And here the Reserve Bank’s factor model measures aren’t very useful, since they work on annual change data and thus often in effect function as lagging indicators in the face of big changes, even if they probably often provide the best medium-term and historical view.)

Here are the trimmed mean and weighted median measures (note that you cannot just multiply these by four to get an annualised rate)

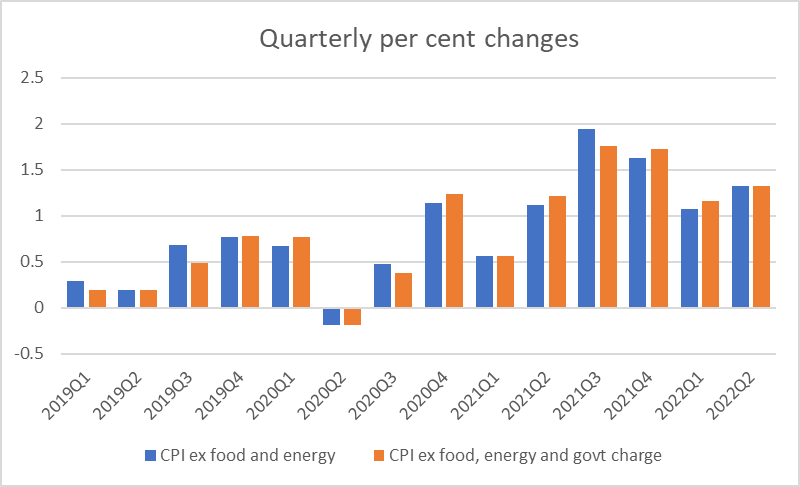

and here are a couple of SNZ exclusion measures (CPI ex food and energy is most often used for international comparisons, simply because of data availability)

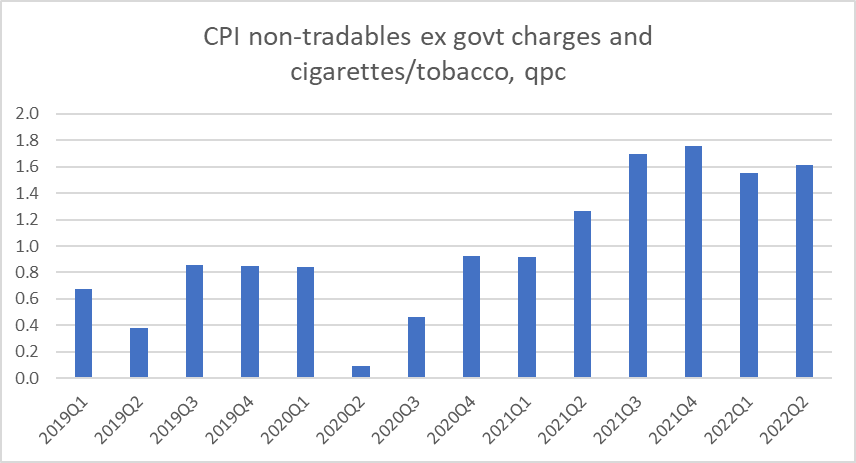

and here is one I’ve quoted a few times over the years, focused more (at least in principle) on the more domestically-generated bit of underlying inflation

Remember that all of these series are capturing prices as they were in mid-April, just short of six months ago.

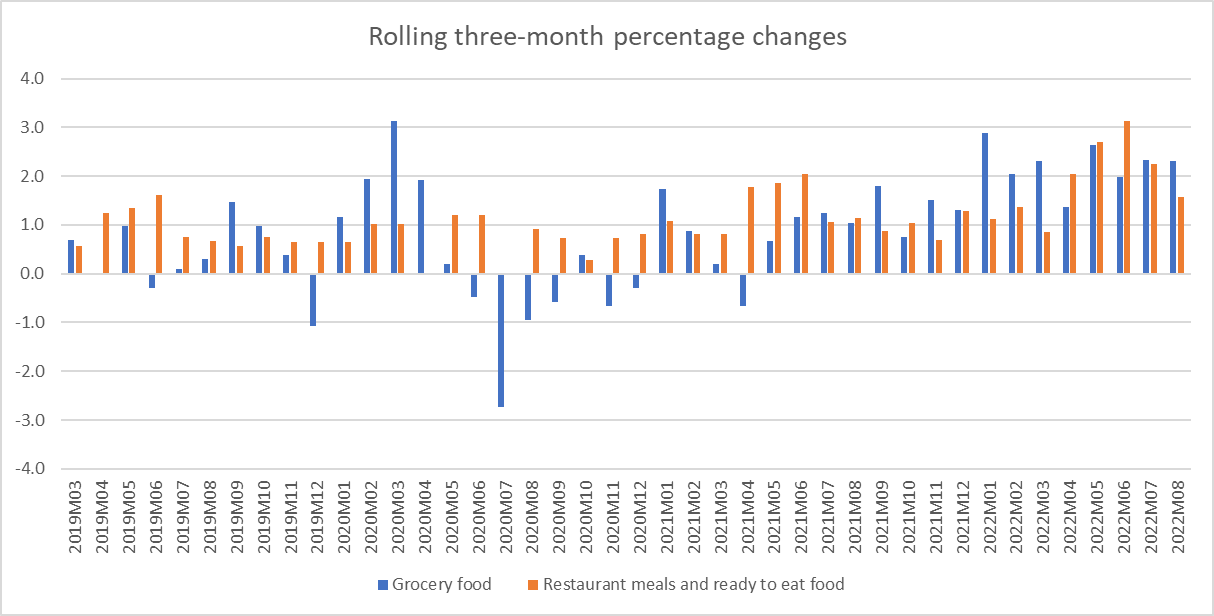

There are a few potentially useful official monthly series. I’ve long kept an eye on these two from the Food Price Index

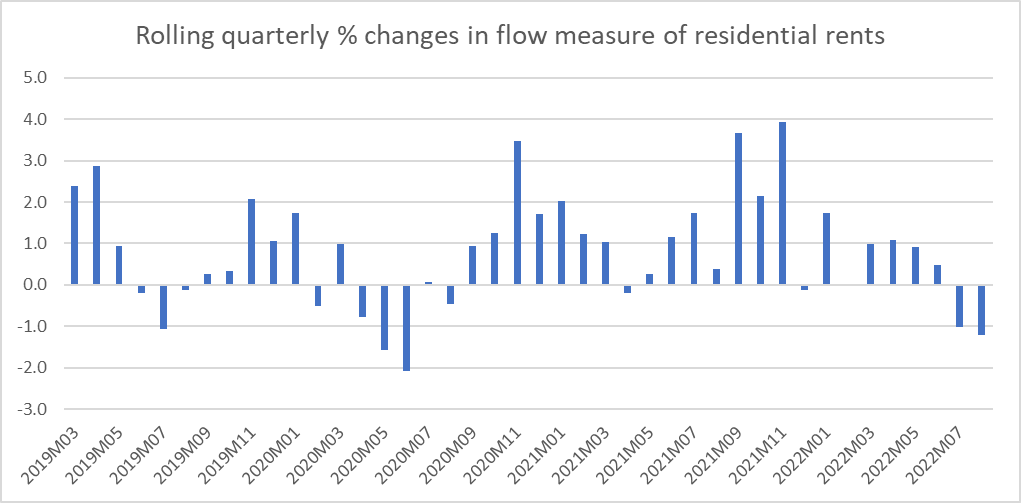

and there is the monthly rental data

Every single one of these series show a (not unexpected) trough in quarterly inflation in the June quarter of 2020 (the first, out-of-the-blue, “lockdown”). But more than a few also suggest that the sharpest increases in the inflation rate were occurring a year ago (perhaps 12-18 months on from the biggest fiscal and monetary stimulus), and that since then the quarterly inflation rates have been (high but) fairly stable or, on some measures have already fallen back a bit. And most of the most recent observations date from a time when the OCR was only just getting past 1 per cent.

If any hawkish readers are wanting to jump down my throat, can I take the chance now to stress that none of these inflation rates – from months ago – should be considered remotely acceptable. They are miles above the 2 per cent annual inflation the Reserve Bank is supposed to focus on delivering. We want inflation much lower than is evident in the most recent data.

But, again, monetary policy works with lags. And those lags may be particularly important to keep in mind when, as this year (and of necessity given how slow all central banks were to start) policy rates have been raised so sharply and quickly. Perhaps also relevant was the point in this nice post from a few days ago by Maurice Obstfeld, formerly chief economist of the IMF, highlighting that many advanced countries have (belatedly) been doing much the same thing, and those effects are likely to be mutually reinforcing. Recessions now seem unavoidable in a wide range of countries, and it isn’t clear that most central banks are taking other countries’ pending recessions into account in their own domestic policysetting.

As I said at the start of this post, only a fool would be overly confident about what monetary policy will prove to have been required over the coming year. And successful policy at this point will probably prove to have involved tightening at least a little more than, with hindsight, was strictly necessary. But on the data as they stand in New Zealand – long collection/publication lags and all – and if forced to make a decision this Wednesday (and the MPC is not forced to, the date is their choosing), I reckon there is a better case for a 25 basis point increase than for a 50 point increase. The key thing, of course, is to convey a sense that the MPC will do what it takes to deliver something near 2 per cent inflation before too long. But at this point it isn’t obvious that aggressive further OCR increases are really needed in New Zealand (Australia, the UK, or perhaps even the US may be in different positions, between even more belated starts to tightening cycles and positive shocks to demand from (eg) commodity prices or fiscal policy).

The MPC and its advisors have only a very sketchy idea of what lies ahead, and how much impact the rapid hike in OCR over the past year might have. The rest of the world faces a very trying year or two ahead, with real prospects of recession. Time to be a whole lot more cautious, in my view. I might go by 25 bp, but no more. And be prepared to talk about giving time for matters to unfold for a bit.

LikeLiked by 2 people

I agree Murray.

I did a deep dive into all of the subcomponents at the third level of disaggregation a couple or weeks ago, lining up with a range of indicators. Headline CPI looks set to fall pretty sharply over the coming year with big base effects in new dwellings and petrol leading the way, but there’s also lots of quirky stuff in there that should drop out. I’m guessing housing inflation will ease, potentially materially too. Used car prices look set to fall, some of the food components are going to ease too.

Obviously, lots of uncertainty in there, especially around exchange rate pass through, petrol and new dwellings, but my projections on the 108 or so sub-components out to June 23 showed inflation coming back to around 3%, give or take…

I’m not a fan of the trimmed mean CPI as it just follows tradable inflation. My preferred exclusion method – CPI ex-fruit, vegetables, tobacco and petrol – also has inflation settling down.

This cycle is clearly going to be short and sharp, and therefore hard for Adrian and the crew to successfully navigate. Given downside risks to activity, I hope they’re a little more cautious from here.

LikeLiked by 1 person

2008/2009 comes to mind with aggressive interest rate rises. Push interest rates too high and force a recession in NZ before the beginnings of a Global Financial crises. With a recession the NZD collaposes. We should wait to see what the rest of the world would be doing. The UK has seen a huge slide in the value of the British Pound as it too raises interest rates. Being a net importer of both energy and most consumer products inflation in the UK has jumped up even higher. NZ is also a net importer of Energy now that we have artificially banned our ability to explore for oil and gas which are likely as large as the UK North Sea Oil reserves. Since we have also decimated our local factories with aggressive interest rate rises histortically NZ is also a net importer of consumer products. Also interest rates are inherently also inflationary as it adds to the cost of products for indebted businesses.

LikeLiked by 1 person

Reblogged this on Utopia, you are standing in it!.

LikeLike

Wondering if lags have been lessened by ‘forward guidance’ – money market rates/risk premiums have adjusted quickly this year on central bank chatter.

And does seem the central banks mean business – reading through speeches, still major tightening bias and lower actual inflation outcomes needed to provide confidence the prospect of inflation persistence has been clobbered.

Recession odds on: what comes after that, very murky…….stagflation as people turn inward?; investment led recovery given energy/infrastructure but more inflation?

A puzzle

LikeLike

I guess it is possible the lags are shorter than usual, but “this time is different” is always something to be pretty wary of. Several past tightening cycles (notably 2014) have been pretty strongly and confidently foreshadowed.

I’m not suggesting great harm would come from going 50bps this week – after all, if necessary they could make no change at all next month – but there is a bit of a worry that having been slow to start, downplaying inflation last year, central banks now feel the need to display some sort of machismo.

LikeLike

OK I am going to disagree here.

Fact of the matter is that you don’t bring inflation down from 7% to 2% by pussy footing around as some of the commenters and Michael seem to be promoting. I am not aware of any country that has successfully disinflated with peak policy interest rates at less than half the rate of inflation (i.e. with severely negative interest rates). Disinflation done properly hurts. Disinflation (typically) involves growth recessions, higher unemployment and rising exchange rates – that’s part of the mechanism through which monetary policy actually works. This is why we pay central bankers handsomely to keep inflation in the bottle to begin with and not to do stupid things like stimulating economies during a supply shock. The sooner people face up to this inconvenient truth and stop treating mon pol like some kind of pixie dust, the better. I for one will welcome a 50 points hike tomorrow and look forward to more before Xmas as we need to get this inflation scourge fixed. PA.

LikeLike

Be sure, disinflation is going to hurt (recession and all). The only question is what OCR is going to be required to produce sufficient hurt.

LikeLike

PA,

History agrees with you.

So do I

LikeLike

Hello Michael, Seems like a fair observation for Central Banks everywhere. Not looking at things in a NZ context, but in the past the policy rate would normally be above the inflation rate to bring the latter to heel. However, this time around with corporate balance sheets vulnerable to significant debt rollovers in the coming 12 to 18 months; and as households are not in such a robust position as they were 9 months ago ( look at the US savings rate, which at 3.6% is back to GFC era levels) the sensitivity to a bp move in the policy rate will have much more impact this time around -higher gamma if you will.

Won’t take too much more of a tap on the monetary policy tunning fork to have some unpleasant and swift flow through effects that will be hard to back-pedal on.

LikeLike

Thanks John. Nonetheless any view at present should be held fairly lightly. I can readily imagine that if we had the Sept qtr CPI , and those numbers offered little consolation, thinking that another 50bps now was appropriate.

LikeLike

As fuel is imported and a component of many items in the inflation basket the removal of the temp subsidy and lower NZ$ may well add a higher fuel component to the index than the month dropping out. The RBNZ has very little impact on NZ inflation which is driven by international events none of which look encouraging in terms of reduced inflation or debt- quite the reverse in fact.

LikeLike

I am very much in agreement with Paul Atkinson

In particular, our current settings should be such as to push the exchange rate up, not down. We opted a long time ago for the floating exchange rate and the independent monetary policy….for goodness sake let’s use it!! Sure the inflation story has been scrappy but we didn’t have to import nearly as much of it as we did…

LikeLike

Peter, I very much agree we shld be focused on bringing nz inflation down , using mon pol to do so. But if everyone else is tightening at a similar pace you wouldn’t expect to see our exch rate rise. my only question is whether in nz we may soon have done enough. I think the RBA will find they haven’t but here some of the data I cite mean I think the question is a bit more open (at least until the next cpi)

LikeLike