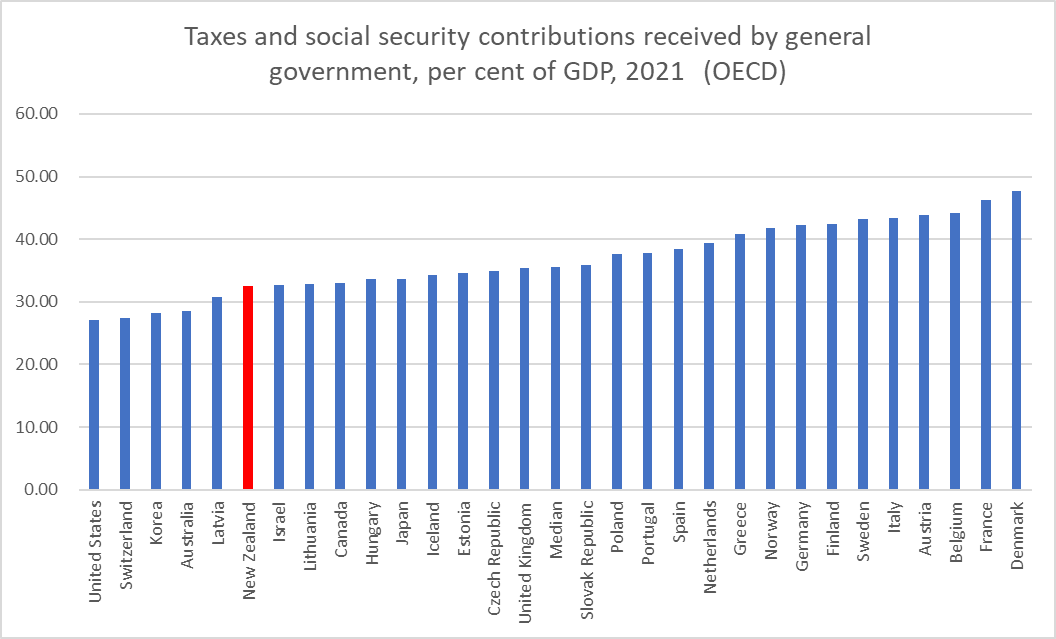

A conversation about the similarities and differences between taxes and social security contributions – my son is studying economics – prompted me to head off to the OECD website and get the data on total taxes and social security contributions as a share of GDP.

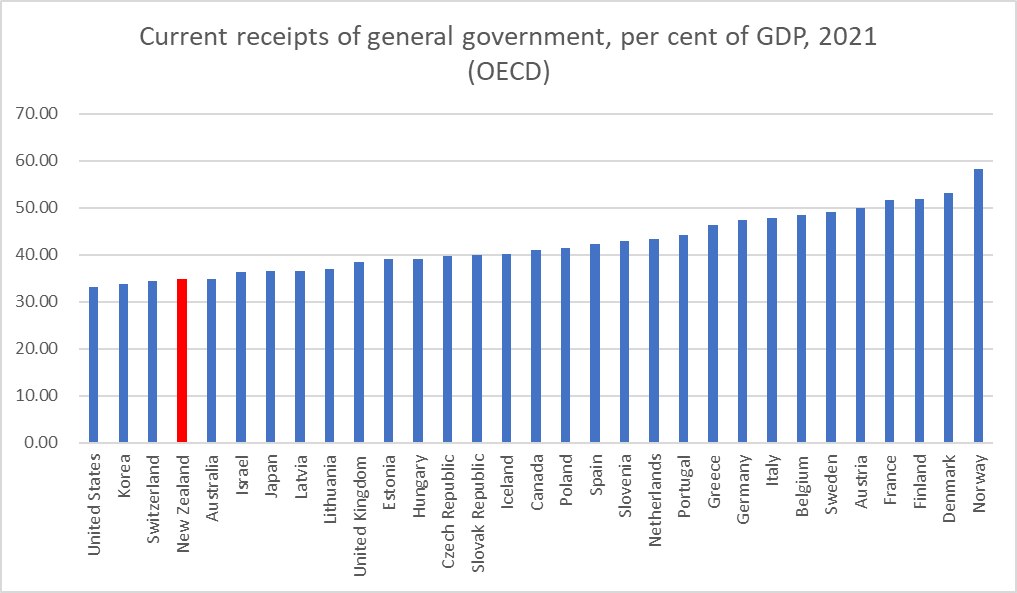

Here is what I found for 2021 (the OECD didn’t have this level of data for its Latin American members, and I omitted Ireland and Luxembourg, as their GDP numbers aren’t a suitable basis for these purposes).

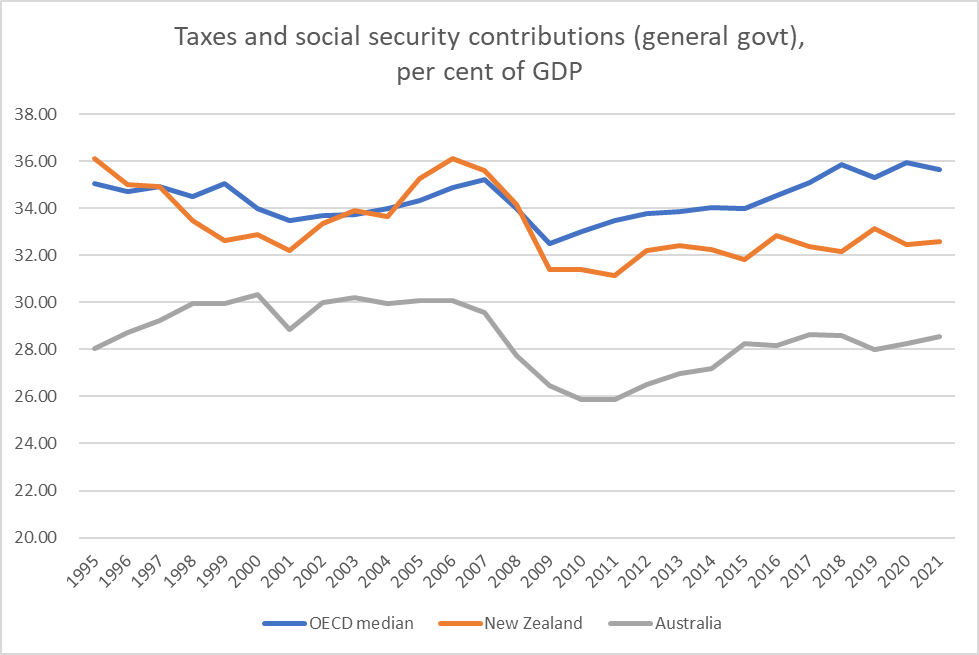

That is the snapshot for the most recent year, 2021, and here is how New Zealand has compared to Australia and to the OECD median (countries in the first chart) for the period back to 1995 when the data are comprehensive.

To be honest, I was a little surprised. I guess time passes and impressions need updating from time to time: the story I had been walking around with (probably formed a decade ago) was that New Zealand tax revenue as a share of GDP fluctuated around the OECD median. It used to but, whether under National or Labour-led governments, it hasn’t done so for some time now. It isn’t that taxes are trending down in New Zealand – as a share of GDP in 2021 they were about the same as in the first couple of years of the Clark government but (a) the contrast with huge surge in tax revenue in the 00s is striking, and b) the OECD median has been edging up.

Of course, Australia is an important comparator, given the number of New Zealanders who look at making – and often do make – the move to Australia, and there is not much consistent sign of a change in the relationship between the two countries’ tax/GDP shares. And the Anglo countries have tended to be lower taxers than continental Europeans, and of the five Anglo countries we were the median taxer in 2021. Whatever one thinks of the US, Australia is hardly some unliveable hellhole (certainly the New Zealanders who move there don’t think so), although neither is it some star productivity growth performer.

Opposition parties seem to be making a fair amount of noise about tax as we begin to head towards next year’s election. And in many respects I sympathise: I find it hard to think of a single one of the tax increases put in place in recent years that I thought there was a good economic case for, and the fiscal drag that results from not indexing income tax thresholds is just bad policy at any time. We tax business too heavily, whether under National or Labour.

But…..you have to identify the things you don’t want governments spending money on, and that is where our main Opposition party seems to struggle.

The picture is, if anything, a little more stark if we shift from taxes and social security contributions to total current revenue. Natural resources owned by the state are part of the picture here (see Norway in this chart vs the first one above)

On this measure, we are even more firmly to the left of the chart.

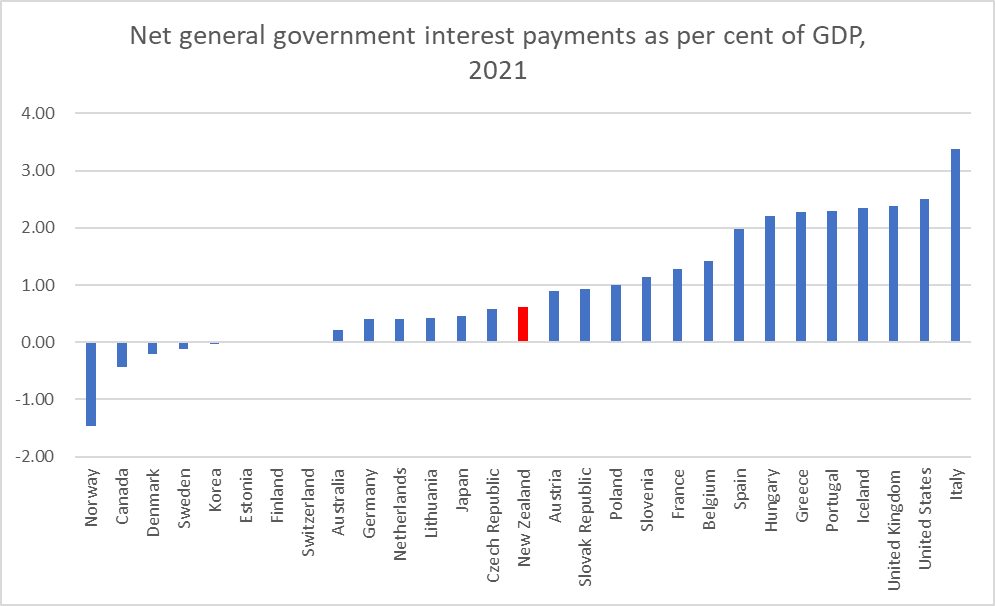

(Incidentally, there is a line – that I probably thought had merit – that we don’t need quite such high taxes because our public debt is low. But the OECD database had net interest data, and we turned out to have been the median country last year. (Low central government debt, but persistently high relative interest rates I guess)

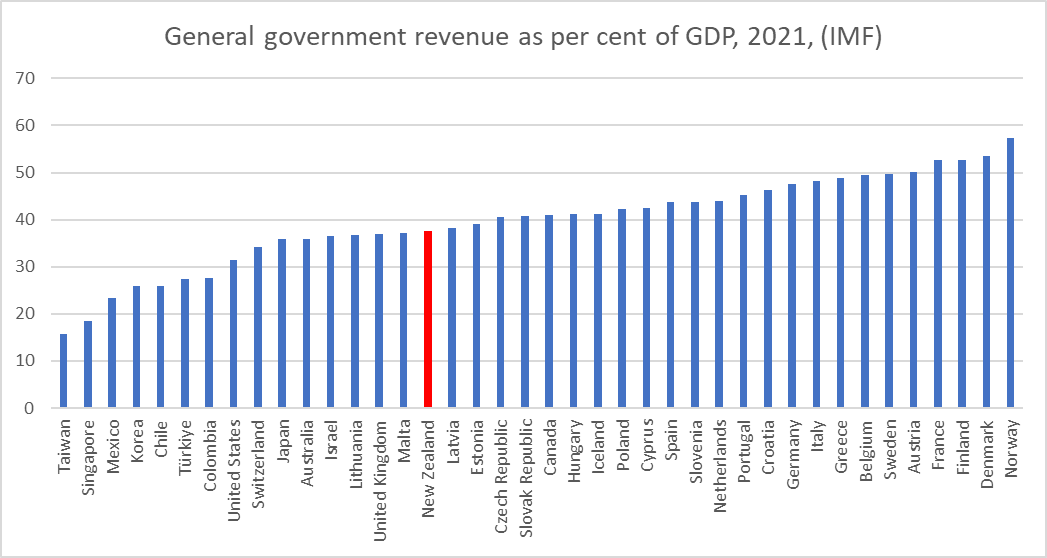

All this data has been taken from the OECD. There is some IMF data, and for a wider range of advanced countries. I don’t put a great deal of trust in the IMF numbers (too often I find NZ numbers that look odd), but they do capture places like Singapore and Taiwan.

But here is the IMF’s total general government revenue data, for 2021

On this measure and this group of countries we are somewhat further from the left. And if (like me) you aren’t overly interested in underperforming Mexico, Chile, and Colombia, note nonetheless the really low revenue/GDP numbers for Taiwan and Singapore. One can have a highly productive economy (both countries now have materially higher GDP per capita than New Zealand) with a materially low overall share of government revenue and/or taxes.

I focused on taxes in this post because (a) that is where the political debate seems to be, and (b) because in 2021 government spending was much more thrown about by Covid one-offs than tax revenue was. In the longer-run, it is the level of spending that determines how high taxes eventually will need to be. Over the recent decades New Zealand governments have had a good record of returning to balance or surplus whenever shocks push the budget into deficit (which means we are one of a minority of OECD countries like that, and very unlike say the US and UK where deficits have been normalised). But note that – with an overheated economy, and thus cyclically high revenue – we are not projected to be at balance or in surplus this year.

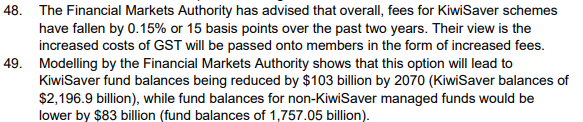

(And to anticipate questions as to what I would cut were I granted a magic wand, here are the first five that come to mind: Kiwisaver subsidies, fees-free first year tertiary education, R&D subsidies, the accommodation supplement (having freed up peripheral land and collapsed house/land prices), and NZS (raise the eligibility age to 68 in the next five years not the next 25). But realistically I do not expect New Zealand wil operate with a lower tax or revenue to GDP share than it has now.)